Decades ago when I was young Reserve Bank annual reports were – uninteresting accounts aside – mostly a bit of an essay on the economy (I got to write some of 1984’s and if I recall correctly one sentence survived to publication). Since the Bank had no independent authority over anything – power rested with the Minister of Finance – that model of Annual Report made a certain amount of sense. If there was any “accountability” involved, it was mostly about judging the fine line involved in offering some analysis without at the same time unduly upsetting the Minister of Finance. (The Bank was, at least in principle, accountable for analysis and advice offered to the Minister, but nothing much of that ever saw the light of day, the then recent innovation of the OIA notwithstanding).

These days, of course, the Reserve Bank is a power in the land, conducting monetary policy (with considerable discretion, but within the broad Remit set by the Minister of Finance), setting much of prudential regulatory policy (and implementing it all, with non-trivial discretion), and so on.

In recent years, both the size of the institution (staff numbers) and the size of the Annual Reports have both been growing rapidly.

The 2017 Annual Report was the last one pre-Orr.

But with all the people and all the pages, any serious sense of accountability and accounting for performance, seems to have diminished almost to the point of invisibility.

Over the years of this blog, I’ve written a series of posts about how the Reserve Bank Board – existing, per statute, primarily, to hold the Governor and Bank to account – had almost completely abdicated that responsibility. Twenty years ago Parliament required them to publish an Annual Report, and the hope had been that it might help, just a little, to sharpen accountability. Instead, the reports proved to be little more than show, mostly apparently designed to provide cover for management, rather than scrutiny and accountability for the public, the Minister, and MPs. Occasionally they showed signs of doing a slightly less bad job, but this year in their final report (the old Board and the old governance model were disbanded from 1 July) they slumped to new levels of quiescent inactivity. Perhaps – being about to head out the door – they no longer cared much, but since the chair (and one other member) were being carried over onto the new Board that shouldn’t have been an acceptable excuse for the contempt for the public that their silence and passivity display.

The full Annual Report is here. The Board’s report is on pages 6-9.

Over the last year, inflation has blown badly beyond the target range set for the Bank and the MPC. On the Governor’s own telling, that is so even if one focuses on the range of core measures. The deviation from target is by far the largest seen in the now 30+ year history of inflation targeting (and as a forecasting error would have been large even by the standards of earlier decades).

At the same time, the Bank’s speculative punt on the government bond market – the LSAP – turned very sour, and cumulative mark-to-market losses on the position are now in excess of $9 billion. The losses don’t fall to the Reserve Bank’s account – the government provided an indemnity upfront – but the losses (2.5% of GDP or so) were directly resulting from choices made by the Reserve Bank, the body the Board was responsible for monitoring and holding to account.

Oh, and during the year, two of the external MPC members were reappointed (by the Minister, on the recommendation of the Board). Given developments on the watch of those members (see above), you’d have hoped that some searching questions were asked, and some serious analysis and review undertaken by the Board. The Board might even have explained why they recommended one member’s renewed term should expire in the (likely) middle of next year’s election campaign.

As it is, not one of those issues was mentioned in the Board’s Annual Report. There is a full page devoted to monetary policy, and not once is inflation (or price stability, or the target band, or any cognate words) even mentioned. Just this

We learn that they looked at lots of papers, but nothing at all as to how they reached a conclusion that the MPC had adequately done its job (there might be a reasonable case to make, but they don’t even try).

The massive losses to the taxpayer get not a mention (again, perhaps there is a case to be made that – as the Governor claims – the benefits mean the costs were worth it), nor the reappointment of the external MPC members.

So no sign of scrutiny, no accountability. But if we heard nothing at all from the Board on such matters of substance, where the Bank has legal responsibilities, the Board was apparently keen to have us know of its other interests

But even then, no sign of evaluation, no sign of challenge? Not even (say) a suggestion that if there is going to a Central Bank Network for Indigenous Inclusion – the case for which is very far from obvious – perhaps the central banks of places like Iceland, Ireland, Poland, the UK, and France might be invited to join.

Reading this bumpf brought to mind this extract I spotted in a recent OIA release of Board minutes from a few months ago

So notwithstanding the limited tasks that Parliament has actually assigned to the Bank, the Board (which includes the Governor) thought it important that they shbould be free to used taxpayers’ time and money to decide their own priorities on things they have no statutory responsibility for. A platform for the interests and ideologies of management and board members (and recall that hardly any of the new and more powerful Board have any relevant expertise on subjects the Bank is actually responsible for).

Of course, it has long been easy to scoff at the old Board. Perhaps they were in an awkward position – most had little relevant expertise, they had no independent resources, and management controlled the papers they saw – but they still took the job (and the modest emoluments) without actually doing the job.

What of management who were, in effect, responsible for the remaining 150 pages of the report (of which much is the accounts)? (“In effect” since the new Board had legal responsibility, but hadn’t been around during the year under review).

The Governor never wastes an opportunity to claim that the Bank is very transparent (it is anything but) and so of course you’d suppose that in his Annual Report, in a year when monetary policy outcomes were so poor (inflation) and expensive (LSAP) there would be an extensive and nuanced treatment of the issues, making the best case no doubt for the Bank but at least engaging on the record. Well, no one who had ever watched Orr would actually expect that, but it is what one might have hoped for if accountability in the New Zealand public sector meant anything at all. It isn’t as if the Bank (or the MPC) has yet published much else serious on these issues, and the Annual Report is actually mandated by Parliament as a principal accountability document.

There are several sections where one might look for substance. This is the “year in review” bit on monetary policy (throughout the document you have fight your way through the tree gods imagery)

Under neither “key outcomes” or “key achievements” do actual inflation outcomes even get a mention.

There was this introductory section, about the environment they faced

It devotes one sentence to the biggest deviation from target in the history of NZ inflation targeting, but even then simply notes the fact.

And then right upfront there is the Governor’s own two-page statement, where this is all there is on monetary policy and inflation. You’d barely know from this that inflation was an outcome for which central banks were responsible, and that New Zealand inflation was an outcome Orr and the MPC had been responsible for.

No analysis, no reflection, no accountability.

Things aren’t much better on the LSAP losses, and the large bet on the bond market that is still open now. The losses do get a mention deep in the Financial Overview (they are a legal financial claim on the government) but there is nothing of substance in the policy sections, and they have the gall to run a “Balance Sheet Optimisation” section near the front of the report, which doesn’t even mention the scale of the bet ($50bn or so) they are continuing to take on future New Zealand bond rates.

By contrast, there are two pages on matters Maori (bear in mind that the Bank’s instruments – monetary policy and banking regulation – are whole economy ones, not differentiating between Catholics, Greens, lefthanders, stamp collectors, or….or…or Maori). And endless references to climate change. Eric Crampton did the comparison

Accountability – in the face, this time, of huge deviations from desired outcomes (whether the inflation or the losses) – is non-existent. The Bank is presumably confident it can get away with all this because there is no sign that the government cares either. Neither party is doing its job.

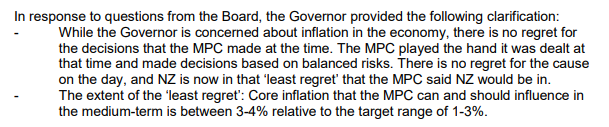

We’ve heard previously Orr boldly claim that he regrets nothing about the last couple of years. There is an arrogance to it that is almost breathtaking. Here, on which note I’ll stop, is the Reserve Bank Board minutetaker’s record of Orr articulating the same story to the Board itself in May

(Even that latter claim has now been overtaken by events as they now recognise that core inflation is even higher than they thought then).

No regrets…..not for the arbitrary redistributions of wealth (which is what unexpected inflation does), not for the grossly overheated labour market which itself has collapsed businesses and livelihoods, and not for the coming (and most likely) recession required to squeeze core inflation back out of the system.

Nothing.

Thanks for the comments Michael. I guess none of us expected much from this document. I’ve not even bothered to read it. If I did, my focus would probably be on calculating the wage inflation at the Bank. Would be interesting to know what the average compensation increase and increase for the very top is.

I was in Wellington briefly a few days ago – wasnt able to catch up unfortunately – and had an interesting and very New Zealand experience. After layering up in the hotel I hopped into the lift, thermals, scarf, hat… only to be greeted by a guy in the lift in a tee shirt, shorts and jandals. It was about 5 degrees outside and windy, and sun had just set. A real nail biting cold Wellington evening. Now you could say the guy was an optimist, but the sun had set and it wasn’t gonna get warmer. Instead, I think it highlights Kiwi’s remarkable ability to simply live in denial.

We see this in the RBNZ Annual Report and we see it in so many other areas. The Government has just announced a policy that will hammer farmers on climate change, but they ignore the horrendous pollution our cities chug out for 6-7 months over winter with their wood burners, and then wonder why people have respiratory illnesses. Lack of accountability goes hard in hand with their denial of our problems, and our reality.

LikeLike

Thanks Peter, As you say, realistically expectations of the document were rightly low.

Were he doing the job well I don’t think the Governor would be being overpaid ($834K), but as someone just noted to me they also now have 8 people earning in excess of $400K – the utterly bloated numbers of senior managers, for an organisation with just 2 big functions.

LikeLiked by 1 person

Thank you. Good read for the layman.

LikeLiked by 1 person

Kakistocracy is the word that one associates with the RBNZ these days.

In a public sector organisation which is so small and which has performed so badly that ten people can earn more than NZ$400k is obscene. How is that even remotely justifiable when NZ’s teaching and nursing professions ( to name just two) are seeing people leaving in droves because of poor pay! Talk about rubbing people’s faces in it -so much for the RBNZ’s vaunted ‘social licence’ to operate…it’s a twisted joke.

Unfortunately this rot & rort is sanctioned by a quiescent leader of the opposition who prefers to fiddle while Rome burns as his strategy ( used in the loosest possible sense) seems to be to ‘win’ in 2023 through a strategy of letting the Government lose through own goals. He needs to man up and say ‘enough is enough’ and the public deserve better from a public sector institution.

But he won’t, so we can expect a further, inexorable, slide into the cesspit of ‘dross’ when it comes to New Zealand’s Central Bank.

LikeLiked by 1 person

Many great leaders report suffering from “imposter syndrome”. We seem to have leaders who actually are imposters.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

On the LSAP losses. it’s interesting that the analysis being done on the impact of QE by central banks (the latest being the RBA) suggests bond buying programs had the effect of lowering bond yields by about 0.30%. In our case, the big decline in rates post COVID was mainly due to the cut in the OCR and the coat-tail effect of our rates following the big boys down. So $9 billion of losses simply to lower rates by an extra 30 basis points – and turbo charge the housing market.

LikeLike