I wrote a post a couple of weeks ago noting how silent the competing politicians, and the media, had been on issues around the People’s Republic of China during our election campaign. The campaign has now almost come to an end, and nothing much has changed. That is, no doubt, just the way our politicians like it. No awkward questions, no challenges, no serious scrutiny of their own institutional complicity, no nothing.

I’m not going to repeat that post, but there are a few new points, and one I inadvertently overlooked and which has (or should have) acquired fresh life in the last week or so.

Perhaps you noticed that yesterday the PRC was elected to term on the UN Human Rights Council, along with a bunch of other egregious states. These elections are done by secret ballot, which must be terribly convenient for the politicians as the votes they instruct to be cast for their country normally remain secret. But there is nothing to stop journalists asking about New Zealand’s vote, or asking the Leader of the Opposition (or leaders of the minor parties) what stance they think New Zealand should have taken. It isn’t impossible that New Zealand abstained or even voted against – China’s election was far from unanimous – but surely voters have a right to know what stance our government took as regards such an egregious a human rights abuser as the PRC? It would be great if they did vote against – and they did join a recent multi-country letter on some of the PRC’s abuses – but it is pretty feeble stand if they won’t tell their own citizens they took such a stance. And if the government won’t say, what stance would National, ACT, or the Greens have taken?

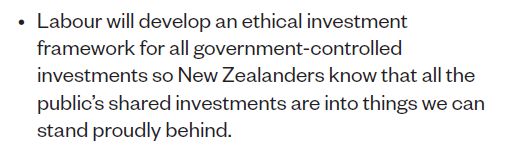

Incidentally, reading the belatedly-released Labour manifesto – which, remarkably, had no reference to China, even in the foreign policy section – I noticed this

So government agencies – including the NZSF and ACC – will no longer be taking equity exposures to companies owned or controlled by the PRC/CCP? I don’t suppose so, but it rings fairly hollow if the PM and her colleagues think New Zealanders could “stand proudly behind” such investments.

Through the election campaign it seems that the National Party has carried on with its deference to the PRC/CCP. An Australian-based China analyst drew our attention to this

Now perhaps it would be one thing for the National Party’s foreign affairs spokesman to be meeting with the PRC Ambassador (as with the ambassadors of other countries) but this is a party-to-party meeting, in the middle of a New Zealand election campaign. The same Goodfellow who previously championed Jian Yang, and who refuses to come clean on the National Party’s involvement/association with the CCP-affiliated people now facing electoral finance charges. What values, one wonders, do the ordinary members of the National Party share with the CCP? Few, if any, I imagine, but if so what is the party hierarchy doing holding party-to-party exchanges with the CCP. Pretty confident that in days gone by it was only the Socialist Unity Party that had much to do with the USSR Communist Party.

But the real prompt for this post was something I forgot to mention in the earlier one.

A couple of months ago, Professor Anne-Marie Brady at the University of Canterbury (with a couple of research assistant co-authors) published a paper titled “Holding a Pen in One Hand, Gripping a Gun in the Other: China’s Exploitation of Civilian Channels for Military Purposes in New Zealand”. It had been submitted as supplementary paper to the Justice select committee of the New Zealand Parliament and is substantially devoted to documenting the connections between New Zealand entities, especially universities, and PRC PLA-affiliated institutions and organisations. As she noted in the first of her Key Points

The People’s Liberation Army’s (PLA) rapid militarisation program is accelerating via an international technology transfer strategy, which includes academic exchanges, investment in foreign companies, espionage and hacking. Scientists work globally, so by accessing universities or tech companies in states with an advanced technology

sector like New Zealand, the PLA can get a foothold within the international network of scholars working on a given subject area.

It didn’t seem terribly controversial – previous papers by other authors have documented the PLA connections with many universities here and abroad – and I didn’t read it at the time.

But a few days later I noted the news that Canterbury University itself was ordering a review into the publication of this paper. Other academics apparently did not like it one little bit, and the Canterbury seemed ready to play along

Canterbury’s deputy vice-chancellor, Professor Ian Wright, said the complaining academics believed the publication contained “manifest errors of fact and misleading inferences”.

Brady herself appears to have been, at least temporarily, silenced and her voice has been totally absent from the public square in this year’s election campaign. You’ll recall that it was during the 2017 campaign that she released her Magic Weapons paper on PRC influence/interference activities in New Zealand, to the discomfort of much of the political class.

It seemed a very odd approach from the University of Canterbury. Academics often like to remind us that they have some sort of “critic and conscience” role in society, and that the freedom to speak openly and publish their material – in turn exposed to scrutiny from the public and peers – is a big part of how academe is supposed to run. And so if there were problems with Professor Brady’s paper, wouldn’t the normal approach have been for those who thought they had identified problems – whether of fact or interpretation or emphasis – to have published something themselves, and let the issues be fought out openly.

I’m, of course, not an academic myself, but many/most of the signatories to an open letter that was released last week are. Addressed to the Vice-Chancellor of the University of Canterbury, the (now in excess of 150) signatories wrote

Professor Anne-Marie Brady’s work has had a far reaching impact on public and policy discussions globally, which is why we were dismayed to read Martin Van Beynen’s report in Stuff entitled “Canterbury Uni orders review into publication by China expert Anne-Marie Brady”. All of us are familiar with Professor Brady’s superb report “Holding a Pen in One Hand, Gripping a Gun in the Other” that was submitted to the New Zealand Parliament’s Justice Select Committee this past July. We are shocked to read that your Deputy Vice-Chancellor, Professor Ian Wright, gave a statement to the press confirming that the University was entertaining the complaints, and giving them currency by explaining that they allege that the paper contains “manifest errors of fact and misleading inferences.”

We, who know this area, can see no manifest errors or misleading inferences based on the evidenced material provided in the report. The paper does not make “inferences.” People who study it may draw some, but that does not mean the paper made them, misleading or otherwise. Since Professor Wright publicly voiced the allegations a group of us peers again went through Professor Brady’s Parliamentary submission. We find in it no basis for the allegations. Some of the links in its comprehensive sourcing have gone stale since she submitted it but those URLs all still work if put into Wayback or archive.today.

We are disappointed to see no prompt follow-up, explanation or clarification of the University’s position concerning the allegations. The impression left by that published report should have been corrected to show that the University did not intend any endorsement of the complaints, nor an approval or acceptance of complaints to the University as the appropriate way to criticise academic work. The silence has been interpreted as collaboration in slander against a very distinguished scholar whose work has been consistently based on sound social scientific methodology.

We would have expected you to stand up for your university, the right of any of its members to publish their research freely, however contentious, and for Professor Brady as a brave colleague. She has been the target of a harassment campaign and threatening menace because of the serious implications of her important research.

We ask that you issue a prompt and full apology to Professor Brady on behalf of the University of Canterbury for not rejecting the complaints against Professor Brady and instead referring the complainants to the normal way of disagreeing with a paper – publishing their criticism. Professor Wright should publicly apologise for allowing his statement to give credence to the complaints, whether or not he intended that.

We know of no valid basis for any “review” of Professor Brady’s work other than by her peers and other researchers and commentators, as is normal for academic research and publication. That will and should include informed criticism as and if grounds emerge. Her publications are subject to peer review. They have brought great international credit to your University. You risk destroying that credit, to leave it with her alone.

And yet this fairly stinging attack on the university, and robust defence of Anne-Marie Brady’s paper has had almost no coverage in New Zealand. And this even though the signatories include, from abroad, some leading academic authors on issues around modern China, as well as several local academics and – to my surprise – two Labour MPs.

(Regular readers may recall that this is not the first open letter in defence of Professor Brady in the years since she first went public on these issues – the earlier one was about the apparent indifference of our political leadership to the break-ins to Professor Brady’s home and office that were widely regarded as most likely to have had PRC origins.)

One might suppose that in the middle of an election campaign, when academics – including many from abroad – and MPs have signed an open letter about attempts to silence or intimidate a leading academic writing on important public policy issues it would spark some serious coverage. Questions, for example, to the Prime Minister, questions to the Leader of the Opposition, questions to the Minister of Education (what sort of system is he presiding over than sees such chilling “reviews” of controversial material), of the two Labour MPs who signed the letter, and perhaps even of the Natiomal MP – Simon O’Connor – who has sometimes put his name to efforts to push back on the PRC but who is strangely silent this time. But not a word. It is all-too-easy to see why the politicians would prefer the issue, and probably Professor Brady, to just go away. But why almost all the media make themselves complicit with this shameful silence is a bit more of a mystery, but not to their credit.

The publication of the open letter finally prompted me to read Professor Brady’s paper. To be honest, I was prompted by this line from the open letter

We, who know this area, can see no manifest errors or misleading inferences based on the evidenced material provided in the report. The paper does not make “inferences.” People who study it may draw some, but that does not mean the paper made them, misleading or otherwise.

In the past, sometimes when I have read Professor Brady’s pieces I have thought she drew stronger inferences and implications than the facts, as she presented them, seemed to warrant. But reading through the latest paper I was struck by the almost-complete absence of inference. She offers, and appears, to document a long series of fact, and offers some thoughts on possible policy responses. I can quite see that some of those involved would prefer (a) that the facts weren’t know, and/or (b) that people looked more benignly on the PRC/PLA connections that benefit their universities, but the significance of those connections is a matter for debate, not for chilling attempts at academic censorship. But neither our politicians nor our media seem to care. Coming on top of how Professor Brady has been treated over the last three years it is a sad commentary on (a) what New Zealand has come to, and (b) how in the thrall of the PRC our universities and business/political sectors seem to have become. And all this without even mentioning things like the Confucius Institutes that our universities host and partly pay for, providing access to our schools for PRC entities and messaging.

At this election, the two previous United Front connected MPs – Jian Yang, he of the CCP/PLA, and Raymond Huo (the one who tried to stop Brady even testifying to the foreign interference inquiry) will pass from the scene and back into private life. But it is not as if any of the parties seems to have had a change of heart, as they’ve rushed to select new Beijing-comfortable ethnic Chinese candidates – one of whom, former head of the Chinese Students Association (consulate-controlled entities), is now certain to enter Parliament.

And then there is ACT. Not long ago it might have seemed almost irrelevant, but now seems likely to emerge from the election with quite a few MPs. ACT leader, David Seymour, has from time to time been heard uttering some quite encouraging words on the PRC, including some forthright comments at the time of the Hong Kong unrest last year. However at least one person, who knows his stuff in this area, has become quite disillusioned with ACT, suggesting that principle has been traded in for opportunism to some considerable extent.

At the request of people with associations with him I’ve previously published links to translations of a couple of pieces by Auckland-based dissident Chen Weijian, who edits the Chinese-language online publication Beijing Spring. Here is a link to an authorised translation of a new piece, Has the ACT party betrayed its principles on China?

The views are solely those of the author. He begins noting his previous enthusiasm for ACT

It’s voting time in New Zealand. Until fairly recently, I had the comfort of knowing that there was a party and politician that stood for the values I cared about: David Seymour’s ACT.

When Seymour supported the Hong Kong protests here in Aotearoa he captured my interest. He was the only New Zealand politician to express solidarity by appearing in person at gatherings of students in this country supporting the rights of Hong Kong.

Seymour delivered well-considered, passionate speeches backing the demonstrators. That was when I decided to vote for the ACT Party.

However, David’s recent actions are inconsistent with the words he spoke when I took him for that rarest of species: a politician of principle.

But then proceeds to discuss the extensive advertising ACT has apparently been doing in the CCP-aligned Chinese Herald, including apparently in the 1 October special edition devoted to the PRC national day and the celebration of the Party.

He goes on to highlight’s ACT’s selection as a candidate – albeit well down the list – who has an extensive background in missile technology (and from whom, apparently, never a discouraging word has been heard about the PRC). The article ends

Most Chinese immigrants, even if highly educated in China, do not rise to such high status positions so soon after settling overseas. However, Ms. Xiao’s ascent has been preternaturally rapid.

Right now, fellow liberal democracies such as the USA and Australia are working hard to squeeze out CCP influence through party-state organs such as the United Front and other limbs of Beijing. Many people with special relationships and obligations to the CCP are in a panic.

It is my strongly held conviction that New Zealand must do the same, and ACT, as a leading voice for liberty, should do the same. Until that happens, they will never get my vote.

I’m much less convinced than the author that ACT has, for a long time, been much of a party of principle – rather they tend to hunt where the votes are, whatever it takes, and this time Chen suggests that that is among the Beijing-sympathetic bits of the ethnic Chinese community. So in many respects I’m less bothered about ACT, which will always be at most a peripheral player in New Zealand, but his penultimate paragraph is one that rings truer to me.

Unfortunately there is little or no evidence that our major parties – notably this time the Labour Party, which will certainly lead the next government – really care at all, or even take seriously these issues. There is a complete absence of any moral leadership on these issues, whether from National or Labour, and too many establishment institutions – notably the universities – seem to quietly cheer on, even egg on, that failure, that choice.

If the silence and complicity of both National and Labour is telling, there is no sign of the minor parties is any better (I’ve been through almost all their websites in a fruitless quest for a party I might consider voting for).