On Tuesday afternoon we learned that the Minister of Finance had written to the Governor of the Reserve Bank about housing and monetary policy. At his press conference yesterday, the Governor told us that the first thing he knew about it was on Monday, suggesting that the government had become worried over the weekend that it was on the political backfoot on housing and felt a need to be seen to be doing something/anything, to change the headlines for a day or two at least.

There wasn’t much to the Minister’s press statement. Perhaps it might even have seemed not-unreasonable if he’d come into office for the first time just a few days ago, but he’s been Minister of Finance for three years, and the housing disaster has just got steadily worse over that time. Little or nothing useful has happened in that time to do anything other than paper over a few symptoms of the problem. And no one believes any agenda the government has is likely to markedly change things for the better: if they did, expectations would already be shaping behaviour and land/house prices would already be falling. Why would one believe it when the Prime Minister refuses to talk in terms of materially lower house prices, and even the Minister of Finance yesterday could only talk about wanting “a sustained period of moderation in house prices” – ie enough to get the story of the front pages, not to actually fix the problem? That makes them no better than their National predecessors.

And so he made a bid to play distraction, writing to the Governor and suggesting that he (the Minister) might change the Remit the Monetary Policy Committee operates under. The Minister can make such changes himself (he does not need the Bank’s consent), but must seek comment from the Bank first.

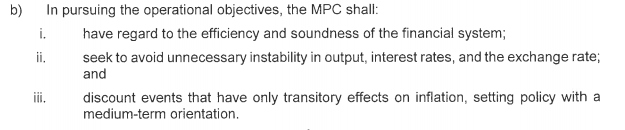

It was a limp suggestion, as the Minister must have known when he wrote the letter (and as The Treasury would almost certainly advised him, if he asked for advice from them). In the Remit, consistent with the Act, the MPC is required to use monetary policy to keep inflation near 2 per cent, and consistent with that to do what it can to support “maximum sustainable employment” (in practical terms, low unemployment). And then there is this

The Minister suggested in his letter that he might like to add “and house prices” to the end of the worthy grab-bag phrase in b(ii).

b(ii) has been in the Bank’s monetary policy mandate (the old Policy Targets Agreements – which I’d link to, but the Bank seems to have removed them from their website) since the end of 1999. It was inserted when Labour became government that year and the new Minister of Finance, Michael Cullen, wanted some product differentiation. The Bank had had a bad run over the previous parliamentary term, including the period when it ran things using a Monetary Conditions Index operating guideline, which led to us actively inducing a wildly unnecessary degree of variability in short-term interest rates. Cullen had also, for some years, been somewhat exercised about the cyclical variability of the exchange rate.

It was cleverly-crafted wording. Don Brash agreed to some new words that sounded worthy – who, after all, wants “unnecessary” variability in anything – but which really changed nothing at all. Better (or worse) still, no one has ever known quite what it meant, or if it meant anything at all beyond what was already implicit in a medium-term approach to inflation targeting (looking through short-term price fluctuations – per b(iii) now – had always been integral to the way we’d run thing). A lot of time and energy was spent trying to articulate what it might mean – the Bank’s Board were particularly exercised, since they were supposed to hold the Governor to account, and it wasn’t clear how, if it all, b(ii) changed anything. For practical purposes, in all the years I sat on the OCR Advisory Committee, with b(ii) as part of the mandate we were advising against, I’m not convinced it ever made any material difference to any specific OCR decision. If the Governor didn’t want to tighten much anyway, it was sometimes a convenient reference point – wanting to avoid “unnecessary instability” in the exchange rate – but a more hawkish Governor, or a more accurate set of forecasts, might just as easily have determined that any resulting pressure on the exchange rate, while perhaps a little regrettable, was nonetheless, “necessary”. And then there were the tensions – avoiding a bit more upward pressure on the exchange rate might actually contribute to increasing the variability in output, and so on.

The clause was, and is, largely meaningless in any substantive sense. From a purely substantive perspective I’ve argued for some years that it should simply have been dropped, but the fact that it lives on is a reminder that documents grow not necessarily because the substance requires it, but because there is a political itch to scratch.

So Grant Robertson’s suggestion that he might change the Remit to add “and house prices” to b(ii) should be seen in exactly that light. It is about scratching political itches – and distracting from the government’s own failures on housing – not about substance. We know this also because the Minister was at pains to reassure people that he wasn’t proposing to change the operational objectives the MPC is required to pursue. If not, then adding “and house prices” is really no more than getting the MPC to add another few lines to the occasional MPS, to imply that they had paid ritual obeisance. It might do no harm, but it will do no substantive good either.

But it won Robertson quite a few headlines, and even got the markets excited for a while, temporarily prompting the sort of lift in the exchange rate that might otherwise appear appear out of step with the government’s alleged desire to promote investment in more “productive assets”.

But if there was anything real to it – if the aim was actually to make the MPC set monetary policy differently (tighter at present) – it would, of course, have to have come at the cost of a more sluggish recovery, lower than target inflation, and cyclical unemployment higher than necessary. Which would have seemed very odd coming from a Minister of Finance who had explicitly introduced to the Act – what was always implicit – the cyclical unemployment dimension just a couple of years ago, complete with reminders of the importance his Labour forebears – notably Peter Fraser – had placed on full employment. (I suppose, charitably, it could have involved some more fiscal stimulus to offset less monetary stimulus, but if the Minister had been serious about that he could do it anyway – the RB sets monetary policy in the light of government fiscal choices whatever they are.)

But of course it wasn’t serious. It was political theatre, and distraction, including an attempt to distance himself from monetary policy policy that he had explicitly authorised. Thus he claims

But as the Minister knows very well, not only was the Bank well advanced in thinking about unconventional monetary policy options by then – they’d published a whole Bulletin article about it in May 2018 – and much of the rest of the world had been using them for some years, but that the LSAP programme (the one actually in effect this year) has been inauguarated with the explicit and repeated consent of the Minister of Finance himself (through the guarantees he has provided to the Bank). Unconventional monetary policy is, in any case, yet another ministerial distraction, since no supposes that whatever contribution monetary policy might have made to this year’s house price developments, it would have materially different if the Minister had ensured that the Bank had its act together in ways that meant that they used a negative OCR this year.

Anyway, the Minister’s letter prompted a quick response from the Bank. Perhaps some wonder if that was necessary – these things could be dealt with to a greater extent in private – but I’m with the Governor on this one. It was the Minister who chose to issue his letter the afternoon before the Bank’s long-scheduled FSR press conference. The Bank had no effective choice but to respond, and better to put things in writing than just rely on throwaway comments at a press conference.

I thought the Governor’s letter was mostly a fairly sensible and moderate holding response. He promised to come back to the Minister with more considered thoughts on the suggested addition to b(ii). There were a couple of bits that could be read more pointedly. For example, the Governor noted that

We welcome the opportunity to contribute to your work programme aimed at improving housing affordability. As I’ve said publicly on many occasions, monetary and financial regulatory policy alone cannot address this challenge. There are many long-term, structural issues at play.

The Bank had, in fact, had some nice lines to that effect in its Monetary Policy Statement just a couple of weeks ago

This is a government failure, not a central bank one. But I guess I wouldn’t expect any central bank Governor to be quite that pointed in public.

Several have also noted that the Governor pointed out that the Bank already considers house prices in setting monetary policy.

I can assure you that the MPC, in making its decisions, gives consideration to the potential impact of monetary policy on asset prices, including house prices. These are important transmission channels that affect employment and inflation. Housing market related prices are

also included in the Consumer Price Index, for example rents, rates, construction costs, and housing transaction costs.

But actually that was a bit cheeky. On those terms, at times like these the Bank positively welcomes higher house price inflation because of the beneficial spillovers they think that leads to in raising CPI inflation. Recall just a few weeks ago their chief economist was actively welcoming higher house prices, distinctly averse to falling prices.

Out of that first round, I’d suggest that the Governor came out ahead on points. The Minister got his headlines – lots of them in some media – but the Governor gave no hint of believing that there was likely to be anything of real substance there.

But the Governor must have over-reached yesterday. At the FSR press conference he expansively declared his pleasure that the Bank has been invited to share its expertise in advising on the wider issues of supply and affordability. In an interview with Stuff – now the frontpage story in the Dom-Post – Orr went further, talking about the tax advice they might also offer. It wasn’t clear what expertise the Governor thought the Bank had in these areas – there is nothing in their research publications or speeches in recent years that suggests any – but I guess that doesn’t often deter the Governor.

But all that talk can’t have gone down well with the Minister, as the newsroompro newsletter this morning includes this

Ouch.

All seems not to be sweetness and light between the Governor and the Minister. But then they deserve each other really. Robertson was engaged in a transparent attempt to distract briefly from the three years of failure of his own government, writing to the Reserve Bank – sure to get headlines – rather than putting the hard word on his own boss and his ministerial colleagues. And Orr, who surely knows there is nothing there and how empty b(ii) really is – and who genuinely seems to think monetary policy should be focused on boosting aggregate demand in ways that lift inflation and employment, can’t help himself in openly trying to embrace a much wider role as adviser on all manner of things that really have nothing much to do with the Bank. Meanwhile, through this period we have had precisely no serious speeches or research papers on monetary policy, we have a central bank that fell back on LSAP partly because it didn’t think to do the basics and check that banks could operate with a negative OCR, and (of course, still) the invisible external members of the Monetary Policy Committee. A high-performing central bank and Monetary Policy Committee would have done a much better job over months of articulating a story, and explaining the place of monetary policy in the mix.

Then, of course, there was the question as to whether had the proposed amendment to b(ii) been in place back in March anything about monetary policy this year would have been different. Orr – probably diplomatically – avoided answering that, but of course the straightforward answer is no. That is so for two reasons. First – and this is a point Orr made in his MPS press conference – the threat to output, employment, and inflation in March was so large that the operational objectives the Minister has given the MPC would simply have impelled a significant easing in monetary policy. But the other reason – actually more an explanation for monetary policy choices than is often realised – is the forecasts. Back in March, hardly anyone (no one I’m aware) would have forecast the rise in house prices we’ve actually seen. Most probably expected – I did – something more like 2008/09, with a dip in prices for a time. So sitting in an MPC meeting in March with an amended b(ii) the house price issues would have appeared moot. Monetary policy would have been conducted just as it was. Oh, and not to forget my point earlier: no one knows what b(ii) means in practice anyway.

But of course if the Minister took any economic advice at all before sending his political theatre letter, he’d have known that too.

So change the Remit, or don’t, in this way and (a) it won’t make any difference to the conduct of monetary policy, and (b) it won’t change the fact that the reforms that might make a real difference now to land/house prices are all matters under the control of ministers already, backed by their majority in Parliament. If my kids can’t buy houses 10 years hence, it is going to be the fault of Ardern and Robertson, and not at all that of the Reserve Bank.