Last week it was reported that the Reserve Bank’s chief economist Yuong Ha had told assembled journalists (at a media briefing on the Bank’s proposed new tools – all while they refuse to use the core one they already have) that

“The worse situation we’d face right now is actually if we had house prices falling.

Ha isn’t just any official. He is one of the four internal members of the Reserve Bank’s Monetary Policy Committee. He was appointed as chief economist by the Governor, but serves on the statutory MPC with the endorsement of the Bank’s Board (themselves appointed by the Minister of Finance) and of the Minister of Finance himself. His department delivers the forecasting and analysis that typically guides the rest of the MPC in their deliberations. In principle at least, he wields quite some clout.

In practice, there is reason to doubt just how much influence he has. He was appointed 18 months ago (somewhat to the surprise of many observers, and perhaps with more emphasis on his service as an Orr-lackey, including around the generation of Orr’s tree-god rhetoric, than for any particular analytical or policy depth). And in that time he appears to have given not a single on-the-record speech – this in the Orr administration that claims to be more pro-active in its external communications and speaking – or paper. It is a striking contrast to, say, the Reserve Bank of Australia or the Bank of England. And it is not as if management has held back to allow the external members of the new MPC to shine: they’ve either been unwilling to, or been forbidden from, speaking at all. And all this through turbulent and uncertain economic times.

But the Bank obviously feels they have to wheel Ha out from time to time so he gets to do the odd interview and the like. Some of them have been quite odd, and all too often reading Ha’s remarks one gets the sense that he just hasn’t really adjusted to operating in the major leagues (he’d had almost no external profile or media experience prior to taking up this job), and that many of his comments probably leave his colleagues wincing just a bit. From a senior statutory officeholder the Bank – and more importantly the country – deserves better. If they were doing their jobs, the Board and the Minister would insist on it.

As just one example, earlier in the year – mid-March actually – we saw this in the Herald reporting comments in a panel discussion Ha had participated in, and casting doubt on just how much difference asset purchase programmes might make.

As it happens, I think he was right then. In fact, he was running the fairly standard line the Bank had run for some time. It is just that within a few days there was going to be volte face and suddenly the Bank would be claiming that large scale asset purchases were making huge amounts of useful difference.

There was also this little snippet I’d forgotten until I went looking for the quote above.

Perhaps there really is/was a good reason for the Bank’s ongoing resistance to any serious transparency, but that certainly isn’t a compelling argument.

I’m not going to try to track down all the quotes I’ve seen this year – and no doubt some have been perfectly reasonable articulations of the (poor) policy Ha is a consenting party to.

But I suspect that the most charitable interpretation of last week’s comments is that it was just another such mis-step. That Ha had simply never taken a moment to reflect on how what he was about to say would sound – most particularly in the last days of an election campaign. Or lifted his perspective from some equation in which these dubious “wealth effects” might have shown up. There was a – highly arguable – narrow point that he might have made, but instead he ranged expansive appearing the welcome New Zealand’s iniquitous house prices as somehow “a good thing”. (And, contrary to at least one commenter I saw, I don’t suppose it had anything to do with the personal financial positions of Ha or any other members of the MPC – very comfortable as they all no doubt are.)

Here is the fuller quote from the interest.co.nz article

There is a quite confused mix of things going on in those comments. On the one hand suggesting that higher house prices are “a good thing” in terms of supporting demand at present (a monetary policy commentary) and then shifting into financial stability matters for which Ha has little or no responsibility. And it is here that he suggests that falling house prices at present – any falls apparently – would represent a worrying (“worse”) situation from a financial stability perspective. But the subsequent comments are then all over the place. Clearly journalists pushed back and suggested that modest falls in house prices are hardly likely to jeopardise the stability of the financial system – as indeed the repeated Reserve Bank stress tests show – and so then Ha is left floundering, falling back on “wealth effects” again, suggesting – at least by implication – that these could threaten the financial system. It was all just very badly done (on the assumption that his remarks are fairly reported in context). And he ended up simply feeding the narrative that somehow the New Zealand economy is a house-of-cards reliant on house prices staying high, or rising, indefinitely, and that the Reserve Bank is somehow party to this conspiracy against the nation’s young and poor. And comes across as backing the reluctance of our political party leaders to do anything that might lower house prices.

I don’t really believe it is the institutional view. If I’m not a great fan of the Governor I have heard him do much better on this issue (and have even used those remarks to defend the Bank on occasion). He’s pointed out the falling house prices only pose a serious systematic threat when (a) house prices have fallen a long way, and (b) when the unemployment rate goes very high and stays high for some considerable time. That is the consistent result of the Bank’s stress tests, including those done in the last three months. One could easily add that whether one approved or not of the Bank’s LVR restrictions – I didn’t and don’t – they did have the effect that few people buying a house since 2013 will have had a deposit less than 20 per cent, and prices have mostly risen quite a bit since then. That is really quite a large buffer (ie if house prices fall even 15 per cent – a bit more than they fell in the 2008/09 recession – very few people are going to have any modest negative equity.

And I’ve heard the Governor better articulate even the wealth effect (dubious) story, to be rather clearer that the Bank has no vested interest in high or rising house prices, but that one way monetary policy can work – all else equal – is by affecting asset prices. What, of course, no one at the Bank points out is that in 2008/09 real house prices fell by 15 per cent – and took five years to get back to previous peaks – even as the Bank cut the OCR by 575 basis points). There is nothing necessary about cuts to the OCR – in recessions – driving up house prices, as for example we also saw after 1987/88 and in the late 90s. Why is that so? Because recessions typically involve income loss, heightened uncertainty, and some tightening in lending standards. (What has made the last few months a bit different? Massive income replacement in the near-term, and the removal of the LVR restrictions – temporarily ending financial repression will tend to have the sorts of effects we’ve seen.)

For myself, I remain very sceptical of the idea of any material housing wealth effect at all. The Bank has been running this line for the last 15 or so years – really since the 00s boom got into full swing – but its case has never been very persuasive, and it remains a story one hears much more vocally from our central bank than from others operating in countries with high/rising house prices. My scepticism on this count is now of long standing, and has both a conceptual and empirical strand. At a conceptual level, higher house prices do not represent greater wealth for the population as a whole (that makes them quite different from, notably, higher stock market valuations, especially those resting on business innovations and rising profit opportunities etc). There is, of course, a distributional effect affecting some people (although not generally owner-occupiers, who have a natural position owning one house and wish to consume housing services for the rest of their lives). Those holding rental properties, who can reallocate their portfolio are certainly better off when prices rise (and worse off when they fall). But their gain is exactly offset by losses to the renters, and to those in a demographic wanting to shift into home ownership.

Ha himself was asked about part of this

Asked whether there was a point at which high house prices would actually have an inverse effect – IE leave people, especially renters, with less cash to spend on stimulating the economy, Ha said this was something the RBNZ was constantly monitoring.

But it doesn’t suggest they have done any serious work on this hardly-new issue.

That it isn’t new is documented, no doubt inter alia, in this article published in the Reserve Bank Bulletin as long ago as 2011 (of which I was editor and co-author). It was mostly an article about understanding consumption behaviour in aggregate, and the abstract read as follows (emphasis added)

Household spending is typically the largest component of economy activity. This article sets out some ways of thinking about what shapes household consumption decisions and looks at New Zealand’s experience over the last decade or so – a period marked by rapid growth in asset prices and debt, and by big swings in economic performance. Large unexpected, but sustained, shifts in incomes appear to have been the biggest influence on total household consumption. Fiscal policy also appears to have played a role. It is less clear that the large increases in asset prices played a substantial role in influencing total household spending.

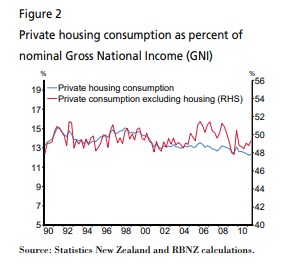

Among the many points traversed was this chart

If you think there is nothing very interesting to it, that is sort of the point. Private consumption – even consumption ex housing – as a share of GNI showed no consistent trends or even cycles over (then) 20 years, and nothing to even hint at any sort of material economywide wealth effect, even as real house prices had risen enormously.

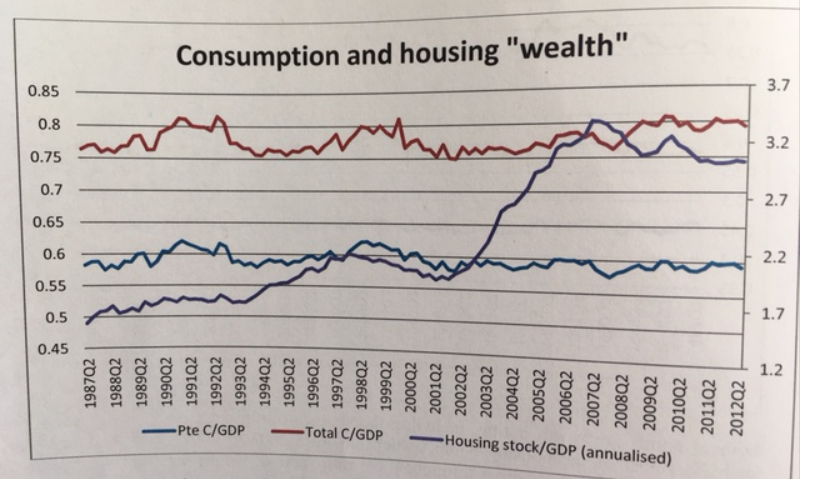

And this chart is from a followup discussion note I did a year later, showing the sharp increase in housing “wealth” over the decades.

Some individuals will have felt wealthier. Some will have been wealthy. But many others will have felt or been poorer. In aggregate – as you’d expect , since we don’t export houses to any considerable degree – not much sign of any material economywide effect. I’ve seen nothing to suggest things have been different in the wake of the rise in house prices of the last decade. It is very hard to unpick what is causing what in a business cycle – and so house prices are often rising when the economy is growing quite strongly, both influenced by similar third and fourth and fifth factors. But as I noted almost a decade ago

If one looked at NZ consumption and savings data for the last decade unaware that there had been a house price and credit boom, one would not immediately think there was anything unusual to explain.

More generally, the Reserve Bank needs to find better, and consistent across their people and across time, ways of communicating that it is not responsible for house prices and it does not, or should not, have a view on where house prices should go (up, down, sideways). As a bank regulator, the Bank has a responsibility to ensure that banks are adequately placed to cope with sharp falls in house prices, especially those accompanied by sharp sustained rises in unemployment (which one would not expect to be the case if land use was substantially liberalised). The Bank appears to have done that – perhaps overdone it with the new capital, requirements. Beyond that, house prices are just one of those thing they may need to factor into their forecasts (of which there are many), not something it should be opining about the merits of. And while I would never encourage them to weigh in, given the Governor’s politicised remarks on all manner of other policy issues, if they are going to weigh in you might hope it was on the side of more affordable house prices and better opportunities for the young and the poor.

Finally – and this post has gone on quite long enough – you’ll have noticed the story yesterday that Heartland Bank is now offering a mortgage product at (just) less than a 2 per cent interest rate. From a housing affordability perspective this should have been a cause for muted celebration. Instead, we get headlines about driving prices to even more unaffordable levels.

The (real) cost of housing really should now be at an all-time low. The cost of using a house (rent, actual or imputed) is the cost of using a long-lived assets. With very low interest rates, the alternative returns from other assets should be expected to be very low, driving real rents down. Lower interest rates also slightly lower the cost of bringing new houses to market – holding costs of land, financing costs during the construction phase etc. And the cost of building materials themselves shouldn’t be materially affected by interest rates (and lows in interest rates are often reached in very low-inflation environments). Ah, but I hear you say, what about land, which is after all in fixed supply. But even there two things weigh against a very substantial effect. First, sustained low interest rates are often associated with low productivity growth (few investment opportunities) and that may be a true of rural land as anything else. But second, and more important, it is only the unimproved value of the land under a house (actual or potential) that should be affected by interest rates, and – in a liberal land market – that unimproved land value will be a relatively small part of the overall price of a house+land. That, of course, is not the way it is in modern New Zealand, but that has nothing whatever to do with the Reserve Bank or monetary policy, but with successive waves of central and local governments that make land – abundant in New Zealand – artificially scarce for housing purposes.

And a few days out from an election we, of course, don’t hear a single significant political party either pointing this out, or promising to make a real and substantial difference.