When the Reserve Bank Act was passed back in 1989, decision-making power was taken away from the Bank’s Board and given to the Governor (even as, overall, the Bank gained a greater degree of autonomy). The Board was retained but in a quite different sort of role. Their new role was primarily to hold the Governor to account, on behalf of the Minister and the general public. Later reforms were made to try to strengthen (the appearance of?) that role: somewhat belatedly the Governor was to no longer chair the Board (although he remained a member of a board whose primary role was to hold him to account), and the Board was required by statute to publish an Annual Report. More recently still – in a well-overdue move – the current government amended the Act to provide that the Minister of Finance would in future appoint the Board chair, making it clearer who the Board was responsible to.

Over the years, the powers of the Bank and the range of activities it undertakes has also grown, and the policy discretion exercised by the Bank has grown well beyond what was orginally envisaged. And latterly most of the formal monetary policy powers have been handed over to a statutory Monetary Policy Committee, and the Board is now also responsible for holding them to account.

But through all these changes, one thing has been constant: the Board has never really acted to hold the Governor to account at all, and instead the Board – through numerous waves of different members and different chairs – seems to have acted as if its primary role was to have the Governor’s back, and reinforce the gubernatorial spin. (In previous posts I’ve argued that in some respects this was always likely, since (a) the Board had no independent resources (eg for external advice), (b) the Governor remained a member, (c) the secretary to the Board was for a long time a member of the Bank’s own senior management, and (d) there were no real incentives to rock the boat.)

There seems to have been a belated general acceptance that the Board is useless, and not readily able to be fixed, in its current role. In fact, the government has introduced legislation which will, if passed, scrap the current model and give the Board primary decisionmaking responsibility for most of the Bank’s non-monetary policy functions (it is a hodge-podge model, itself not likely to work that well, but that is a post for another day).

The Bank’s latest Annual Report was released last week. It didn’t get attention. The Board’s Annual Report got even less (pretty sure it was none). That is hardly surprising. The Board buries its report in the middle of management’s report, and the press release the Governor puts out never mentions that there is an independent report by an entity paid and mandated by Parliament to hold he and his colleagues to account.

As it is, had anyone read the Board’s Annual Report (start on page 6 here), they could only have come to the conclusion that the Board was determined to prove its utter uselessness and ineffectualness in any role other than covering for the Governor. It is spin and/or unquestioning acquiescence, from start to finish.

There is, for example, the nonsense inflation of the Bank’s importance:

We are pleased with the decisive actions that have been taken by the Bank to deal with the potential collapse in economic activity.

75 basis points off the OCR, and whatever lowering of near-term government bond rates the LSAP achieved, simply did not – on any serious reckoning – avert a “potential collapse in economic activity”, and could not conceivably have done so, when the shock to economic activity was primarily about things (fear of virus, policy response to virus) that monetary policy has no affect on.

Remarkably they also claim to be “pleased by the communication and transparency the Bank showed in delivering these innovative tools”.

All while making no mention of, for example, the Governor’s substantive interview last year (in the year under review) expressing a strong preference for a negative OCR as a first cab off the rank, or the public comments of one of his own senior managers in March this year playing down what anyone might reasonable expect from a bond purchase programme. Or the failure to release any research/analysis around the LSAP. Or the failure to release the detailed background papers – promised by the Governor in a speech in March – on the various unconventional instrument options. Or the weird pledge the MPC made in March not to alter the OCR for a year come what May.

And, of course, they make no mention of expressing any concern that despite (a) years of lead time, and (b) the Governor’s explicit preferences expressed last August, it only emerged quite belatedly that it was not until the end of January that the Bank took any steps to discover whether the banking system was operationally ready for a negative OCR (perhaps that is because, as they note, “well before Covid-19, we were briefed on the Bank’s preparations”, and presumably none of them asked the question either).

There is no suggestion of any unease around the policy/communications inconsistency from the MPC in the middle of last year (they could perhaps have explained it away as teething issues with the new MPC, but they seem resolutely determined to utter no cautions on anything at all sensitive).

The Board was quite as determined, it appears, to have the Governor’s back when it comes to financial stability as well. They are firmly behind the big increase in capital requirements and seem quite unbothered about concerns and questions raised, and (if anything) even less bothered about the abusive style adopted by the Governor on many occasions during the course of the consultation. Reflecting the Bank’s own lines, the Board both championed the much higher capital requirements – which had not come into effect and made little or no difference to capital levels by the end of last year – and repeat the Bank’s spin about how sound the system is/was in the face of the (large) Covid shock at the old capital levels. Taxpayers’ money is wasted on this.

Lest you thought that they never uttered a challenging word – to encourage or discourage – there is in fact one quiet dissent in the report, although presumably only allowed to get this far because the Governor himself was on board. We learn that

Policy work on the Deposit Takers Act is highly complex and significant for the Bank’s operations; the Board has expressed concern that the policy development process should be thorough and not rushed.

And that is it – and even then a comment on something not largely under the Bank’s control (Treasury and the Minister having a large say).

For the rest of the report, it is just gush. Perhaps the Board is less than enraptured with the Governor’s climate change ambitions – they just get passing mention – but they are all-in with the Maori strategy; this in an institution that operates at a wholesale, not primarily individual-member of the public facing, level:

The Board believes the incorporation of Te Ao Maori into the Bank’s work will help develop a central bank with a distinctive New Zealand approach and character.

Tree god myths and other pandering, but with not a shred of evidence for how any of this expenditure of public resources (from memory of my OIA it was $1m) will enhance macroeconomic or financial stability. But I guess when the Board chair is accused in his day job of fostering “systematic racism” (universities and all that being, in current form, a western development) he probably had to be seen to go along.

The gush continues to the end. We learn that the Governor and Deputy Governor have provided “outstanding leadership” – so much so an accountability body finds no fault at all – and the report ends having lost all touch with reality observing that the Bank is “realising the Bank’s vision to be a – Great Team, Best Central Bank.”

You might conceivably think the Bank does, on the whole, not a bad job. But there is no conceivable basis – in outputs or outcomes (or actually in inputs for that matter) – to think that the Reserve Bank is even close to being the “best central bank”. As I’ve noted previously, in a not-so-wealthy small economy it might not ever be realistic as an aim. But it could do a great deal better than it is on numerous fronts – and presumably if the decisionmakers did not agree they would not recently have decided to throw lots more taxpayers’ money at the Bank to help them do better.

Most likely, there will only be one more of these puff pieces, and by 2022 the new legislation is likely to pass and any pretence that the Board is an accountability body will pass out of law. When it finally does, of course, it will only reinforce how weak the accountability mechanisms are around this very powerful independent agency. I’m still of the view that New Zealand would benefit, slightly and at the margin, from establishing a small Macroeconomic and Finance Policy Monitoring agency, operating at arms-length from both The Treasury and the Reserve Bank.

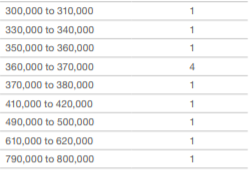

The final thing of interest in the Bank’s own Annual Report is the higher salaries table. This is an excerpt from this year’s.

As I noted last year, Orr himself seemed to be getting more than the Minister had suggested when the appointment was made. And there seem to be a lot of senior colleagues – in a still not very large organisation – pulling in very high salaries. I’m not one of those who generally thinks top-tier public service salaries are too high in principle. These are probably something like fair salaries for excellence, but there is little sign of consistent excellence at the top of the Bank, particularly not from the Governor.

(Incidentally, government department chief executives earlier this year took a temporary 20 per cent pay cut in the wake of Covid. I’ve seen no hint that the Governor – exercising significant public policy powers, and better paid than most of them, and apparently thwarting a collapse in the economy – followed their lead. Perhaps some journalist might ask why.) UPDATE: Thanks to the reader who drew my attention to the footnote describing the Governor’s temporary pay cut.

The Board itself pulls in a couple of hundred thousand (in total) in fees – the largest chunk going to the chair who, one woud have thought, had a demanding day job. The Governor might be getting his money’s worth, but the public is not.