It has always been the policy of this blog to try to call it as I see it. That means that even when people – officials, politicians – whom I think are doing a generally poor job, and are perhaps even unfit for office, do or say something significant I largely agree with, I will try to say so, even (perhaps especially) when people I might otherwise normally agree with are attacking them. That standard – probably inevitably adhered to fitfully – applies to Reserve Bank Governors as much as anyone else.

My next post will be quite highly critical of the Reserve Bank and the Governor, but in this one I am going to defend some remarks the Governor is reported to have made yesterday in an interview with a Stuff journalist. There was some other stuff in the interview I was quite uncomfortable with but here – because various people have raised concerns with me about them – I want to focus just on these remarks.

The Reserve Bank would consider additional stimulus beyond the $33 billion it had committed to quantitative easing so far, he said.

Orr would not rule out the Reserve Bank directly lending money to the Government, rather than only buying central and local government bonds on the secondary market from other investors.

But he said that former “heresy” came with risks.

“Blurring monetary and fiscal policy together can lead to very relaxed fiscal policy … and high inflation, if there isn’t that operational independence to tighten when you need to tighten, when the economy is back on its feet.”

It was a bit loose, but that’s Orr. I don’t suppose he went into the interview wanting to openly raise the option – although perhaps he did – and it seems more likely he was just answering a question.

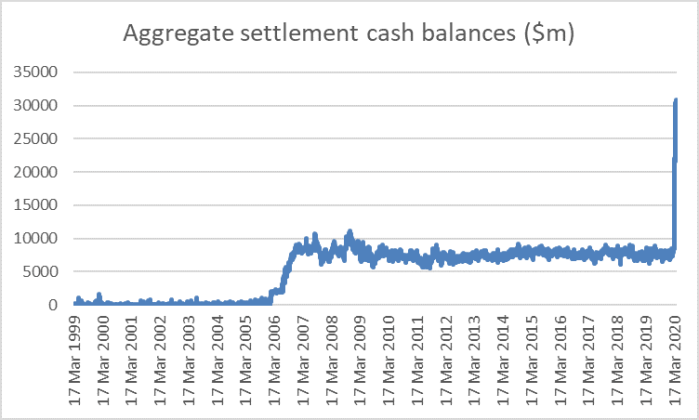

At present, the Reserve Bank has committed to buying $30 billion of government bonds on the secondary market over the year from March. When the Bank goes into the secondary market and buys government bonds, it acquires the bonds (yielding on average a bit less than 1 per cent, judging by current secondary market yields) and it credits the proceeds of the purchase to banks’ settlement accounts at the Reserve Bank (the Bank isn’t necessarily buying the bonds from a bank with a settlement account, but all transactions between the Reserve Bank and private sector parties eventually end up affecting settlement cash balances in total). The Reserve Bank could choose to “sterilise” that impact – do short-term open market operations types of transactions, to reduce settlement cash balances and increase some other bank asset/Reserve Bank liability – but they don’t appear to be doing so at present. There is no real need to: the Bank is paying 0.25 per cent of all settlement cash balances at present, which underpins the level of short-term rates near what the MPC is (rightly or wrongly) targeting. Between Reserve Bank liquidity management operations to stabilise the fx forwards market (initially), bond purchases, and the heavy government deficits at present, there has been a huge increase in the level of settlement cash balances since this crisis really got going. The Bank isn’t that good at releasing timely high frequency data, but they do release this series

It is no longer easy to see from the chart but there were significant increase in aggregate settlement cash balances in the 2008/09 crisis. But the scale of those interventions is totally swamped by what we have seen in recent weeks. In normal times, banks get by with about $7bn of settlement cash in aggregate (and the Reserve Bank actively capped demand) but the last observation was $29.725 billion.

Is this a problem? Well, not in and of itself. Recall that the statutory authority here, the MPC, set the OCR at 0.25 per cent. Consistent with that, the 90 day bank bill rate was yesterday 0.35 per cent – more or less what you’d expect if markets put little probability on the OCR changing in the period ahead. The fact that the Reserve Bank is paying 0.25 per cent on all those $30 billion of balances means there is no obvious problem of excess supply – the Bank’s price supports, underpins, demand.

(There is potentially relevant background in an old post on some of these issues in a US post-crisis and New Zealand context.)

Are the bond purchases on the secondary market lowering the interest rate the government is paying on its newly-issued debt? Well, of course. That probably isn’t the main intention of the purchases – asset purchases might well have been appropriate even if the government had no new debt to issue – but it is a clear and well-understood implication. In fact, the Reserve Bank’s announced and actual purchases – and the possibility/probability of an increase in the purchase programme at the MPS next month – will make the Bank by far the dominant player in the market for government securities over the period ahead. The Bank is, to all intents and purposes. “setting” – or hugely influencing – the government’s borrowing costs. It is, of course, doing much the same – albeit a little less directly – across the economy as a whole.

Note that I said that one of the influences on settlement cash balances will have been the government’s cash deficit over the last couple of months – taxes will be down, $10 billlion of wage subsidies has been paid, and on the other hand some new bonds will have been issued. The government typically operates with credit balances at the Reserve Bank (the Bank and the government are not very transparent, but as at 30 June last year government deposits at the Reserve Bank were $6.2 billion) but it does not need to, at least if the Bank agrees.

Unlike many central bank laws that were overhauled in the last few decades, the Reserve Bank of New Zealand Act was deliberately written in a way that did not prohibit direct lending from the Bank to the government. Instead, the ability to lend – whether by overdraft or by purchase of government bonds – was made a matter for the Governor. And the Governor’s binding constraint was that he had an inflation target to pursue, and could lose his job if he was not adequately pursuing that target. The target itself could, of course, be changed, but that had to be done transparently by the Minister of Finance. And the Minister of Finance has not been able to direct the Bank to lend to the Crown, let alone set the interest rate on any such advances. The logic of this model was that Reserve Bank credit to the Crown was not a threat or a macro risk so long as the Bank had the inflation target and unfettered ability to adjust monetary policy to counter inflationary risks wherever they arose from. The Bank could agree to lend to the government at (in ye olden days, as Social Credit used to advocate) 1 per cent, so long as it could, say, impose an interest rate of 10 per cent on the rest of us. It might be inefficient – and this was mostly hypothetical – but the point of the Reserve Bank Act was mostly to sustain low stable inflation, and voluntary lending to the Crown on terms agreed by the Bank did not threaten that.

The extremes were hypothetical, but the moderate practice was not. We used to have a standing agreement with The Treasury as to the rates the Crown would be paid on its deposits and the rate it would be charged on any overdrafts it had from the Bank. And overdrafts were simply not that uncommon – nor was there anything obviously wrong with them, given the seasonal patterns in government finances. The terms used to be set out in an Agency Agreement between the Bank and The Treasury’s Debt Management Office. I’m not sure how things work these days. but there was nothing wrong or threatening about the arrangements.

What is more, the Reserve Bank has significant holdings of government bonds in normal times. These are normally thought of, although not mechanically so, as the counterpart to the Reserve Bank’s note issue liabilities and historically represented the Bank’s main form of income. The Bank typically does not – or at least did not, and I have no reason to suppose things have changed – go to the secondary market to purchase the bonds. Rather they had an arrangement with The Treasury to pick up tranches of bonds directly at new issue, at the same weighted average yield private auction participants pay. In normal times, this is a direct addition to settlement cash balances – the Crown gets some money it can spend without borrowing it from the private sector or raising it in taxes – but is usually offset by the Bank’s regular open market operations (which keep settlement cash balances in aggregate fairly steady in normal times – see chart) and over time by the trend increase in, for example, currency on issue.

This is probably a bit longwinded, but it is by way of establishing the point that Reserve Bank lending to the government, whether by overdraft or direct securities purchase is not unknown or, within the overall monetary framework (target, operational independence), at all particularly problematic.

So what got people excited? Well, the Governor touched on the possibility that instead of going into the secondary market to buy tens of billions of dollars of bonds, the Bank might at some point, and on some scale, simply buy the bonds direct from the Crown itself.

I’m not sure why they would choose to go that route – and it didn’t have the feel of something the Bank was just about to do – but the key point of this post is that it really would make almost no difference macroeconomically if that was an approach the MPC and the Minister of Finance at some point agreed to take.

For a start, the amount of settlement cash in banks’ accounts at the Reserve Bank would not change. Instead of private bidders buying the bonds, and paying for them by having settlement accounts at the Reserve Bank debited and the Crown account credited, only to have the Reserve Bank then buy the bonds in the secondary market, in turning crediting the same amount to banks’ settlement accounts at the Reserve Bank, the Reserve Bank would simply cut out the middleman: the Crown account would be credited and the Reserve Bank would have the bonds. By assumption, the level of deficit spending itself wouldn’t be changed.

Recall that as the law stands, it is the Reserve Bank that has full discretion over whether it agrees to such purchases and the terms on which it does them. The Minister of Finance cannot direct them.

So what might the objections be? One I heard was about price discovery – if the Bank is buying bonds directly, how will we know what the market price is? But the objection is largely moot because every individual bidder in the bond auctions, or the secondary, is bidding conscious of the Reserve Bank behemoth that has promised to be a huge presence in the market for the next year. The Reserve Bank is already the dominant influence on the market and that would not be changed if they were to buy direct during this extreme period – and there would still be a secondary market operating on the sidelines. It is really no different than if, say, the government insisted on buying huge numbers of new houses off the secondary market rather than direct from builders/developers – if the government is the dominant purchaser, it will have a dominant influence on price either way. In the government bond case, the relevant constraint is the inflation target.

There are old central banking mantras about the dangers of direct government finance. And that is certainly an issue if (a) your political system is breaking down, and (b) the Minister can insist on the borrowing and set the terms (or have appointees more aligned to government interests than to macro stability). Direct credit in Weimar Germany fed and facilitated the hyperinflation. But that simply isn’t the world modern New Zealand finds itself in. As I’ve already shown our institutional arrangements – under the dreaded hardline 1989 Act – have always allowed direct purchases and even direct overdrafts, but the critical point was (a) the control by the Bank ,and (b) the transparent inflation target.

Some of the old rhetoric popped in an otherwise quite good speech yesterday by the RBA Governor Phil Lowe.

I would like to restate that we are buying bonds in the secondary market and we are not buying bonds directly from the government. One of the underlying principles of Australia’s institutional arrangements is the separation of monetary and fiscal policy – that is, the central bank does not finance the government, instead the government finances itself in the market. This principle has served the country well and I am confident that the Australian federal, state and territory governments will continue to be able to finance themselves in the market, as they should.

As I noted, this wasn’t the way our Act was written, even though in normal times and on average across the year that separation was observed in practice (appropriately enough).

Lowe goes on to argue that

While we are not directly financing the government, our bond purchases are affecting the market price that the government pays to raise debt. Our policies are also affecting the price that the private sector pays to raise debt. In this way, our actions are affecting funding costs right across the economy as they should in the exceptional circumstances that we face. But our actions should not be confused with the Reserve Bank financing the government.

But this is really a distinction without a difference in the current climate, even more so in Australia than in New Zealand. A key aspect of the RBA policy response has been

the introduction of a target for the yield on 3-year Australian government bonds of 25 basis points, and a preparedness to buy government bonds in whatever quantities are needed to achieve that target

They have bought A$47 billion of bonds so far, have effectively pegged the three year yield, and are willing to buying whatever it takes. The distinction between secondary and primary market activity is without any material macro significance, especially as long as these actions are under the Bank’s control. The Australian government could issue as many bonds as they like and the RBA is committing, in effect, to pick them up at a stable yield, just on the secondary market rather than the primary market.

Could such activities become problematic? Well, of course.

A hypothetical government might respond to an agreement to buy bonds directly by greatly increasing its deficit spending. But that in itself does not pose a macroeconomic problem (around inflation) unless and until such spending gets to the point where new demand is outstripping the economy’s capacity to supply, or is expected to do so. That doesn’t seem to be the presenting problem in advanced economies at present. And were it to look like doing so you would (a) expect the MPC to alter the terms on which they were buying bonds, and (b) potentially raise the OCR. In other words, to do their job and aim to keep inflation near the inflation target.

Which brings us back to the real issue/risk. Inflation could become a problem a little down the track if (a) the MPC went rogue and decided to simply ignore their mandate or (b) the Minister of Finance was either complicit with the MPC (“don’t bother about the target; there’ll be no sackings”) or simply used his entirely-legal statutory powers to change the inflation target (raise it) either temporarily or permanently. A Minister could do that, of course. But there is not the slightest sign of it happening, here or in the rest of the advanced world. Indeed, there have been some highly reputable overseas economists calling for inflation targets to be raised for the last decade – precisely because of lower bound concerns at the next crisis – and decisionmakers took precisely no notice.

More generally, the biggest challenge central banks have faced here and abroad in the last decade or so has been getting inflation up to target, and that despite huge bond purchases – often unsterilised – in other countries that used that tool earlier.

Which brings me to my more overarching point: the biggest risk around inflation at present, here and abroad, is deflation not an acceleration in inflation. That isn’t just some idiosyncratic Reddell view: it is reflected in market prices from the bond markets, and in survey measures of inflation. It is what tends to become a predominant risk when central banks can’t or won’t lower interest rates much and yet demand falls away quite sharply. As I’ve noted in various posts – and there will be more – the more appropriate criticism of central banks here and abroad is that they are doing too little to stabilise the economy, support inflation expectations, and support conditions for the recovery, not too much.

(Oh, and for other related precedents, a week or two back the independent Bank of England agreed to extent its direct overdraft facility for the UK Crown. Again, this is done by an operationally-independent central bank, still operating within the constraints of an inflation target.)

So, there you go, another post in support of the Governor. For cleanness/appearances sake, I’d probably prefer the Bank didn’t go the direct purchases route, but the macroeconomic risks if they did so in these exceptional circumstances, are small to non-existent. So long as the MPC remains independent and the inflation target is unchanged, and their lodestar, it is simply not macroeconomically different from what they are doing now.

cf

Why the Federal Reserve doesn’t just buy Treasury securities directly from the US Treasury?

The Federal Reserve Act specifies that the Federal Reserve may buy and sell Treasury securities only in the “open market.” The Federal Reserve meets this statutory requirement by conducting its purchases and sales of securities chiefly through transactions with a group of major financial firms–so-called primary dealers–that have an established trading relationship with the Federal Reserve Bank of New York (FRBNY). These transactions are commonly referred to as open market operations and are the main tool through which the Federal Reserve adjusts its holdings of securities. Conducting transactions in the open market, rather than directly with the Treasury, supports the independence of the central bank in the conduct of monetary policy. Most of the Treasury securities that the Federal Reserve has purchased have been “old” securities that were issued by the Treasury some time ago. The prices for new Treasury securities are set by private market demand and supply conditions through Treasury auctions.

https://www.federalreserve.gov/faqs/money_12851.htm

LikeLike

How could MMT fit in here? I saw a Bloomberg article today on the topic (https://www.bloomberg.com/opinion/articles/2020-03-18/here-s-hoping-the-mmt-crowd-is-correct) and to a layperson doesn’t look any less convoluted than what you describe here. I presume the US would have to amend their legislation regulating the Fed, and presumably the NZ leg would have to be amended too.

LikeLike

In many ways MMT is a quite different issue – altho were what the advocates championing ever to be implemented it would involve a fairly different legislative structure (cen bank mon pol independence isn’t really a thing in MMT).

The existing huge fiscal deficits, being funded at near-zero interest rates, are not a particular problem with a massive negative output gap (esp if you believe that mon policy itself is constrained), but the MMTers are often running arguments about how things shld be in a more-normal economy (eg the US last year), overlaid with (technically correct) point that a country with its own central bank need never default (technically correct, but with manyfewer implications that adovocates claim).

Here were some comments of mine on MMT after a seminar I attended with one of chief academic proponents who visited NZ a few years ago..

https://croakingcassandra.com/2017/07/31/a-radical-alternative-to-macro-policy/

LikeLiked by 1 person

Central Bank direct purchases of Government bonds bypasses the market with its differing strategies and objectives – keep it up and the market fails. Perhaps the reason why as a general rule direct purchase is not favored. Despite the influence of the OCR it is the market that establishes price/term relativity even to the extent that what terms are delivered into open market operations.

LikeLike

Yes, in general I’d prefer they continued current procedures. But I suppose it becomes possible that the auctions simply start failing – a possibility MoF appears to have alluded to – in which case taking at least some of bonds directly from Crown to Bank isn’t necessarily a problem.

LikeLike

I was wondering whether in these unprecedented times, the ‘route’ for borrowing/deficit spending should be treated differently for operational vs capital spending.

For example, let’s say the government decides it needs to step in as a much larger employer as a means to reduce unemployment (a number of organisations have suggested the establishment of a Conservation Corps). This borrowing could be made directly from Crown to Bank at a 0% interest rate.

Whereas capital works (i.e., infrastructure) spending could remain as per the current route.

My idea being that operational spending becomes a ‘whatever it takes’ and infrastructure spending maintains a focus on a rigorous cost-benefit analyses – i.e., prudent spending – in the eyes of the NZ public, as well as the wider bond market.

LikeLike

Could do altho bear in mind that the difference between 0% and something under 1% isn’t that large, and that if the RB were actually doing its job and setting the OCR deeply negative there would be much bigger effects from the private sector as well as even cheaper short term govt borrowing.

LikeLike

Yes, I understand the OCR argument. I was thinking that such an approach would see a fixed 0% operational deficit spending reflecting the RBNZ’s employment mandate. Then the OCR setting for market/bond purposes (whatever the number and perhaps it should be negative as you say) would reflect their inflation-targeting mandate.

I was just wondering whether such a differential route might give the RBNZ an improved monetary policy flexibility/ability to influence.

If inflation gets away, and it might, as we just don’t know how scarcity – both for goods and credit – will play out in this post-COVID environment, It might be useful to be able to raise the OCR without all of the government’s deficit spending having to meet those inflationary challenges. And in doing so, the government has to be mindful of the constraints it would normally be operating under.

In other words, if, for example, the cost-benefit case for light rail in Auckland didn’t stand up under normal circumstances, I don’t really see the case for that changing simply because we are in an expansionary period

I guess my overall question is about fiscal discipline – and I think we have to have some constraints going forward.

LikeLike

I guess my point is only that whatever the interest rate (0 or 1) it won’t make that much difference. I’m not opposed to the sort of differentiation you suggest, and if anything my view remains that fiscal policy has in aggregate been far too cautious so far (hence my 80% pandemic income insurance proposal). In the short term we prob need more fiscal action, beyond the next 6 mths mon pol needs to take the weight – partly because, relevant to your final para – I think the public/politcal resistance to big/growing fiscal deficits will be exhausted fairly quickly.

LikeLike

Michael, I agree with pretty much all you say above. The risk of inflation arises, doesn’t it, if down the track the government flags away raising the taxes – a claim on income or, in other words, on future production of real goods and services – to repay the debt. And instead turns to the central bank to ‘monetise’ it, that is, to provide (increasingly) generous (non-market) refinancing terms, ultimately to the point that the government bonds on the asset side of the central bank’s balance sheet are no longer a claim on anything (real). The Mugabe regime in Zimbabwe knew how to do that.

And what we rely on to guard against that is, as you put it:

“Recall that as the law stands, it is the Reserve Bank that has full discretion over whether it agrees to such purchases and the terms on which it does them. The Minister of Finance cannot direct them.”

LikeLike

Yes, but with the caveat that at present the bigger risk is deflation and some mix of monetary policy and fiscal policy (ideally rather more the former) needs to be deployed en masse to lean against that non-trivial risk.

LikeLike

The last March quarter shows rising inflation at 2.5%. The last days of the March quarter would have relected the early days of our lockdown and stampede buying. The inflation in essential goods already register a 30% increase in inflation which is not registered in the CPI because the supermarkets discounted heavily on most goods prior to Lockdown which have since stopped.

The NZD has also dropped from 0.64 to 0.54 against the USD. Deflation will only be within the next 3 months as existing stock in warehouses stuck in warehouses are soldoff. After that new stock will be at higher prices.. I see only rising prices after the next 6 months unless Chinas factories restart full production. With social distancing global supply chains are at less than 50% of pre virus capacity.

LikeLike

It’s a very short way from Modern Monetary Theory to not so – Modern Monetary Practice. A few examples of the practical application of the former:

Austria 1922

Bolivia 1985

Brazil 1994

Germany 1923

Hungary 1946

(…)

Zimbabwe 2008

Beware of “progressive” economists reinventing the wheel, the Phoenicians invented not just the money, but also limits for its amount. For a very good reason. And the Reserve Bank Act can easily be changed.

LikeLike

Yes, altho bear in mind that hyperinflation is usually caused, at a deeper level by complete political breakdown and unsustainable distributional conflicts. Central banks are the fuel, but they aren’t the lighter.

And for the last 20years really the disinflationary/deflationary impulses have been stronger than the inflationary ones, revealed first in the trend decline in neutral interest rates and, for the last decade, in cen banks consistently undershooting inflation targets.

LikeLike

Yes, but ultimately it comes down to the divergence between production and consumption, other contributory factors notwithstanding. Provision of a various “economic stimuli” works to a point, especially if the gulf between production and consumption does not become too wide. As long as central banks remain truly independent the resemblance of balance can be maintained, however, in the current political climate this could easily change. Some public pronouncements from certain politicians do not leave one with an excess of optimism.

LikeLike

Indeed, Milton should have perhaps added “at full employment” to his quip.

I think what gets overlooked is if the RBNZ is buying off the non-bank sector, the latter gets a credit at a bank which is avaliable to ‘reach for yield’ in riskier asset markets: that might force the RBNZ to buy more risk at the next downturn as we have seen with the Fed.

In short, QE seems harder to reverse than to put into gear…and not sure where that road ends.

LikeLike

Oh my…..I do declare reading this I was confused for a moment as I thought I was on Bill Mitchell’s blog! This is word for word what MMT has been pointing out for years. Fiscal deficits are fine as long as spending does not outstrip real economy’s capacity to respond. Central bank can control interest rates government’s pay always and not bond vigilantes. Deflation is the problem right now not inflation. Hyperinflation

is caused by turmoil and supply collapse. ….now the next step for the new MMT embracers is to check out the Job Guarantee as an alternative to the NAIRU. Heartening to read this post.

LikeLike

My take on MMT from a few years ago (which Mitchell got in touch to say he thought was a fair treatment).

https://croakingcassandra.com/2017/07/31/a-radical-alternative-to-macro-policy/

LikeLike

Mitchell’s reflections on his visit to NZ in 2017.

http://bilbo.economicoutlook.net/blog/?p=36568

LikeLike

Cutting out the middle-man would be acceptable providing the proceeds are sterilised and held on the RB balance sheet as an identifiable amount until redemption day

LikeLike

Sent from Yahoo Mail on Android

LikeLike

Hi Bruce

Was there supposed to be something more in this comment?

LikeLike