On Friday afternoon a reader sent through a copy of a Bloomberg story quoting Geoff Bascand, Deputy Governor, on the health of the New Zealand economy. As reported, it was pretty upbeat to say the least. But the foundations for such an upbeat tone seemed more akin to sand than to solid rock. Storms expose houses built on sand.

This was the opening section of the article

New Zealand’s central bank doesn’t expect its new bank capital rules to present a headwind for the economy, which looks to be near the point of entering a recovery, Deputy Governor Geoff Bascand said.

“We don’t expect major economic impacts” from banks raising their capital buffers, Bascand said in an interview Friday in Wellington. Furthermore, latest developments are “supportive of the story that we’re near or around that turning point” in the economic cycle, he said.

Bascand had been interviewed by Bloomberg’s local reporter, Matthew Brockett, following the announcement on Thursday of the final bank capital decisions: very big increases in required bank capital ratios, even if some portion of that can be met a bit more cheaply than the Governor’s initial proposal had envisaged. So I guess we should expect spin. Bascand’s day job is as the senior manager responsible for financial stability, banking regulation etc. All the advice and the documents published on Thursday emerged from his wing of the Bank. But he is also a statutory member of the Monetary Policy Committee, with personal responsibility – with his colleagues – for actual delivering inflation rates near target, something the Bank hasn’t managed for years now. For most of that time, the Bank has been consistently too optimistic about the economy, and about the prospects for getting inflation back to target (fluctuating around the target midpoint, perhaps especially in core inflation terms).

I guess the characterisation “doesn’t expect its new bank capital rules to present a headwind for the economy” is the journalist’s, and there is quite a lot of leeway in Bascand’s own words: “we don’t expect major economic impacts”. If “major” here means “singlehandedly tip the economy into recession” then I suspect everyone would agree, but that shouldn’t be the standard. The Bank’s own numbers tell us that they think the base level of GDP – absent crises – will be lower as a result of the change in the capital rules. And their modelling effort focuses on the long-term, not the transition. The headline out of last week’s announcement was that the transition period had been stretched out, from five years in the consultative document to seven years. But (a) in making decisions now, and in the next couple of years, people will sensibly factor in changes in the regulatory environment that have already been announced (and are final, in the Governor’s words) – expectations matter, as the Bank often (and rightly) tells us, with its monetary policy hat on and (b) for the big banks a significant chunk of the policy change is frontloaded, because the change in rules to increase risk-weighted assets calculated using internal models to 90 per cent of what would be calculated using the standardised rules happens right at the start. That change alone is equivalent to a 20 per cent increase in minimum capital.

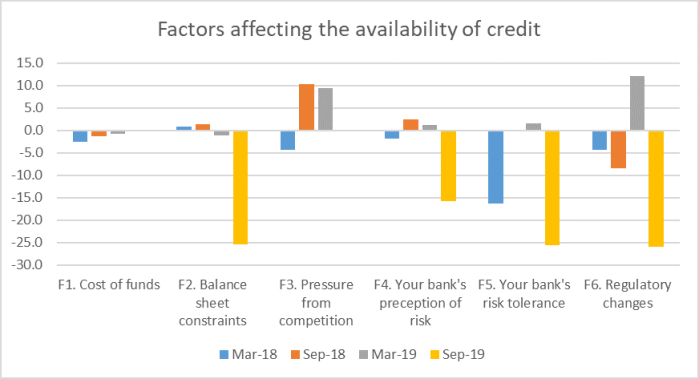

And it isn’t as if there are no hints of effects already, even before the final decisions were made. The Governor and Deputy Governor clearly prefer to avoid addressing these data, but the Bank’s own credit conditions survey showed not only that credit conditions (a) have already been tightening, (b) are expected to continue tightening, and (c) respondents ascribe much of that effect to the impact of regulatory changes.

Perhaps the banks were just making it up when they responded to this survey? Perhaps, but the Bank was happy to cite either components of the survey in its recent FSR, just not these awkward ones.

And why wouldn’t much higher capital requirements, in a world where there is no full MM offset (as the Bank itself recognises), no full or immediate scope for disintermediation to entities/channels not subject to the Bank’s rules, constrain credit availability to some extent, especially in the early stages of a multi-year transition period? And, as the Bank also keeps telling us, the availability of credit is one of lubricants to economic activity. If credit isn’t as readily available, all else equal economic growth is likely to be dented.

And what about Bascand’s other big claim that indicators are

“supportive of the story that we’re near or around that turning point” in the economic cycle,

Count me sceptical. At best, what we’ve seen so far might support the possibility of an inflection point. If you want a nice summary, with charts, I thought last week’s ANZ economics weekly was about right.

It is worth remembering just how subdued economic growth rates have been this decade – headline, not even per capita – and that the slowing has been underway for several years.

On the home front, business confidence and related measure seem to have bounced a bit, but aren’t outside the range we’ve seen over the last couple of years (when actual growth has been falling and low). Some agricultural products prices are doing very well, but (a) surely the best estimate is that many of these lifts will be shortlived, and (b) debt overhangs and tightening credit constraints locally will limit the extent to which near-term income gains materially increase activity. Bascand makes quite a bit of the promise of fiscal stimulus, but recall that on the Treasury fiscal impulse indicator there was a fairly substantial fiscal stimulus in the year to June 2019, and growth was low and slowing.

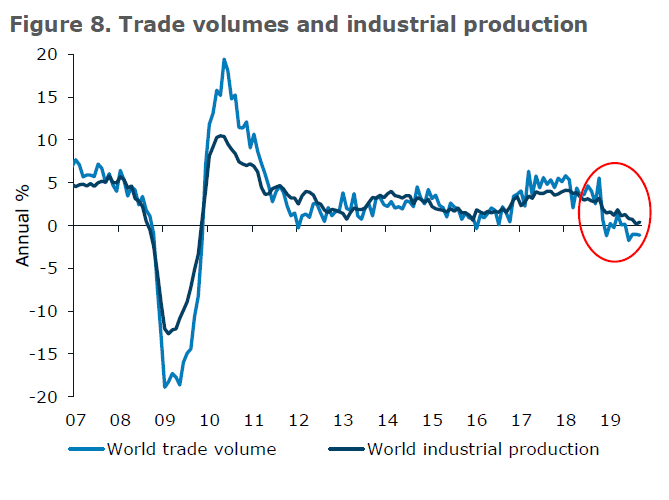

And that is before we start on the rest of the world. Here is an ANZ chart of growth in world trade and industrial production

Data out of Europe, Australia, and the PRC (the latter two being the largest New Zealand export markets) have remained pretty downbeat, even as sentiment ebbs and flows at the margin. The latest Chinese export data offered little encouragement, And there isn’t much optimism about the US either, with a considerable chunk of US forecasters expecting a recession in the next two years. And all this against a backdrop in which people (markets in particular) know that there are quite severe limits on how much macro policy can do if a new serious downturn happens. That alone is likely to engender caution.

The TWI doesn’t move independently of all these domestic and foreign influences, but it is worth noting that it is now a bit higher than it was when the Bank surprised everyone with their 50 basis point OCR cut in August.

Perhaps time will prove the Deputy Governor right, but at present I’d suggest his claims should be taken with a considerable pinch of salt. Things probably aren’t getting worse right now, but it seems heroic – against the backdrop of both domestic and foreign constraints and headwinds (including those capital changes) to be talking up the idea of a turning point in the economy. And rather concerning if this is the sort of sentiment shaping the Bank’s monetary policy thinking right now, after a decade in which things have kept disappointing on the downside. It doesn’t have that “whatever it takes” sound about it, of which we heard quite a bit in the wake of the August OCR cut. It sounds more like the sort of spin we hear repeatedly from the Minister of Finance and Prime Minister, who go on endlessly about headline GDP growth rates here and abroad, and never once mention how much faster population growth is here than in most advanced countries.

A few weeks ago I wrote a post about the sudden mysterious, but very welcome, appearance of inflation expectations as a factor in the Bank’s storytelling about policy. For a few weeks the Governor was outspoken in his desire to act boldly to boost inflation expectations, and do what he could to minimise the risk of hitting lower bound constraints in the next downturn.

And then, like the morning mist, all that concern was gone again – totally absent in the presentation of the latest MPS. If anything, inflation expectations measures had fallen a bit further from August to November.

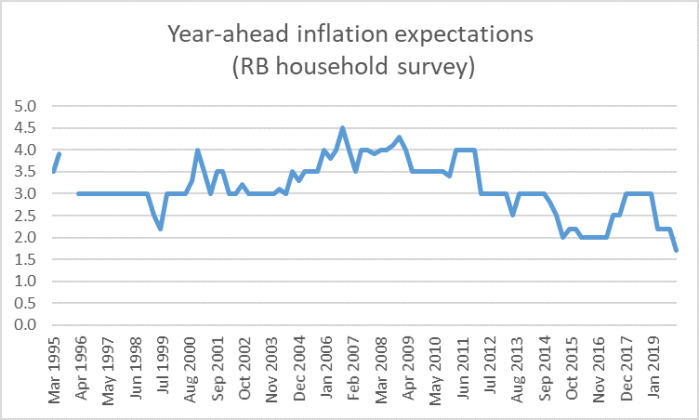

I don’t typically pay much attention to the Reserve Bank’s survey measure of household inflation expectations. Neither, I expect, do they. But it has been running for a long time now, and the latest numbers – finally released late last month – look as though they should be a bit troubling for the Bank.

This series is nowhere near as volatile as the ANZ’s household expectations survey (although, for what it is worth, recent observations in that series have also been pretty low). It began in the far-flung days when the inflation target was 0 to 2 per cent (centred on 1 per cent) and yet this is the first time ever that household year ahead inflation expectations (median measure) have dropped below 2 per cent. At one level, that might be welcome – the series has historically had quite an upward bias – but when household expectations are converging towards professional and market expectations, and all those are below the 2 per cent target midpoint it shouldn’t be a matter of comfort at all. This is the sort of drop the Governor claimed (at least in August and September) he was trying to prevent. In the same survey, respondents are also asked whether they expect inflation to rise, fall, or stay the same over the next year (probably easier to answer than a point estimate). There too respondents have become less confident that inflation is going to pick up.

For a brief period a few months ago it looked as though the Bank, and the Governor, were really taking seriously the challenges we face, in a context where conventional monetary policy just does not have much more leeway. More recently, they seem more interested in talking things up again – keeping pace with the political rhetoric, and perhaps playing defence re the bank capital changes. A more realistic tone would offer a better chance of getting through tough times with as little damage as possible, including by better preparing firms and households for the risks that arise if the global downturn intensifies, with little monetary policy leeway, the risk of significant policy-induced tightening in credit conditions, and inflation (and particularly at present inflation expectations) falling away.

We are getting very late in the business cycle and we’d be better served by a strongly counter-cyclical central bank, rather than one playing defence for its own (deeply flawed) other policies, and whistling to keep spirits up (and political masters, making decisions about the future of the Bank, happy). With the sort of mindset on display at present they risk being blindsided by events, in a context where – as the Governor himself put it only a few months ago – the costs and consequences of being wrong the other way (inflation gets to say 2.3 per cent) are pretty slight and inconsequential after a decade of such low inflation.

It’s a sugar-rush. The sun is shining, house prices are rising and all is well with the world…

LikeLike

What I was surprised is that our Space Sector is now a $1.7 billion dollar contribution to GDP with the government only contributing $90k research grant for Peter Beck to start off in his early years. Too bad the only privately owned Space Port in the world is in NZ but owned by the US, sold for $300 million. We can easily waste $1 billion on culling cows and compensating Kiwifruit farmers but we can only spare $90k for our the latest high tech industry.

What happened to keeping strategic assets in NZ national interests?

LikeLike

Don’t forget the $10 billion sugar rush that Jacinda Ardern is getting from moving the Auckland Port up north. And so far we have spent $90k on our future Space Port in an industry now worth $1.7 billion?

LikeLike

Pure vapourware at present…….

LikeLike

Isn’t talking up the econmy their job?

LikeLike

I’d say not. Their job is to act in ways that help stabilise the economy and build consciousness of the potential limits of policy. Let the data then speak for themselves. Talking up the economy risks, inter alia, being ((or being seen as) partisan.

LikeLike

in an academic sense I would agree but in a real politic sense no

LikeLike

In mild doses and in normal times perhaps it does little harm. My concern is about the specifics of the last decade when central banks have been consistently too keen to look to the next tightening.

LikeLike

A Central Bank can either be optimistic or ‘realistic’.

I am happy for them to be the former rather than the latter. They maybe looking at the next tightening over there but they have not tightened have they?

LikeLike

We’ve had two tightening cycles initiated in the last decade, both of which had to be quickly reversed. And core inflation has consistently undershot target.

LikeLike

They have been quickly overcome. They are not the only Central Bank to get it wrong.

You still have not addressed the question of how any Central Bank can be realistic.

Over here our Central Bank tries to tel the Government to boost Infrastructure spending but has not criticised therm for only addressing 2 0f the 32 vital Infrastructure protests that Infrastructure Australia has noted. mind you it is the Opposition’s job not theirs

LikeLike

They were, I think, the only central bank to get two cycles wrong like that. But my criticism generalises: central banks were far too slow to recognise what was going on and adapt.

I didn’t realise you were posing the second question. But my answer would be “by staying in their lane” and over time building a reputation for calling it is as it is, without fear or favour to either side of politics. It doesn’t seem any part of a central bank’s job to be urging govts to do this, that, or the other sort of spending or structural reforms (avoiding doing so was one of our historic mantras at the RBNZ) and thus nor is their job to criticise govts for not acting. (As you note, that is what we have Oppositions, and think tanks, columnists, even bloggers for).

LikeLike