I don’t have that much to say about the HYEFU and the Budget Policy Statement released yesterday. If governments are going to keep on with the insane and destructive (to the economic wellbeing/prosperity of New Zealanders) policy of supercharging population growth then, sooner or later, they are going to need to spend more on increasing the associated public “infrastructure” (roads, schools, hospitals etc). One can, of course, question the quality of some of that expenditure – baseline or projected – but more people pretty reliably means a need for more capital.

That said, if the population is growing rapidly you’d usually expect to see all sorts of investment growing quite strongly. As I illustrated in a post last week both government and business investment have been really rather subdued in recent years. The Treasury doesn’t give us forecasts that separate out government and business investment, but here is a chart of their forecasts for total non-housing investment (public and private) as a share of GDP. The first observation is an actual, the rest are forecasts.

Note the scale. These are not huge moves, but they are falls. Treasury expects that non-housing investment will be a smaller share of GDP in the coming years than it has been in the recent past. Something doesn’t seem right about the economic policy settings, at least if the governments cares about lifting average material living standards of New Zealanders. Treasury forecasts on the basis of policy as it is, and (fiscal) policy changes the government has told them it will be making.

The picture in the forecasts also doesn’t look very good if we concentrate on trade with the rest of the world. Here is exports as a percentage of GDP.

When it first took office, the government occasionally used to talk about a more export-oriented economy and all that. No sign that the Treasury thinks that policy settings are consistent with delivering that. I didn’t include imports on the chart, but the fall in imports as a share of GDP over the forecast period is slightly larger than the forecast fall in exports. Taking on the world and winning, consuming more of the best the world has to offer, it isn’t.

And it isn’t as if The Treasury is forecasting doom and gloom: they expect overall GDP growth to pick up and be running at around 2.75 per cent per annum.

You’d hope that, faced with projections like these, the Minister of Finance would be demanding from the Secretary to the Treasury – and that the Secretary would be proactive in offering – robust advice on what might, after all these years, begin to reverse New Zealand’s woefully poor long-term economic performance. It doesn’t seem very likely, but the Secretary is new. Perhaps she is genuinely shocked at how poorly New Zealand does. Perhaps she is demanding answers, analysis, and advice from her staff.

On page 2 of the HYEFU I noticed this claim

The Treasury is in a unique position to focus on improving the way our economy can raise New Zealand living standards. Along with delivering first-rate economic and financial advice,

Treasury certainly is in a unique position. They have a lot of staff, have had their budget increased, and have (or should have, if they are doing their job) ready access to Ministers and input across all major areas of policy. And yet, the actual performance has been poor, and there is little visible sign of that “first-rate economic and financial advice”. It might be bad if governments were consistently rejecting such advice, but that is their prerogative. But there isn’t much sign that The Treasury has been offering hard-headed searching advice on the failures of overall economic performance, whether or not successive governments had been inclined to give it heed.

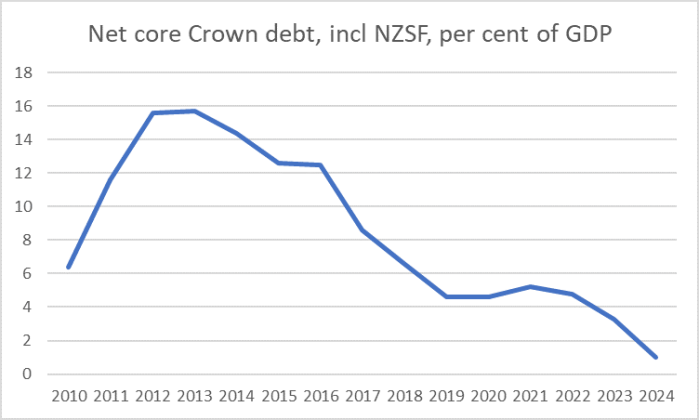

All that said, one can’t argue too much with the fiscal performance. Here is a chart of the best of the debt indicators Treasury publishes forecasts for.

Modern New Zealand governments manage debt and the aggregate public finances in a pretty responsible way (I’m not one of those who thinks low interest rates mean governments should take on more debt: rates are low for a reason), and government debt levels near zero seem pretty prudent given the way other government policies remove some of the need for private savings. And while Treasury thinks we have a small positive output gap, my own inclination – and the balance of the other estimates they quote – is that things are a bit weaker than that. Commodity prices are pretty high to be sure, which always flatters the public finances a bit, but overall I’m pretty comfortable if the operating balance is somewhere just either side of zero.

Successive governments have done aggregate fiscal management pretty well. It is just a shame they’ve haven’t shown the same degree of interest, passion, commitment etc to fixing the longrunning productivity failures. Overall fiscal management matters, but in terms of the long-term material living standards of New Zealanders, it is a bit akin to keeping the garden pretty and the fences well tended even as the house itself slowly – ever so slowly but surely – rots.