A day or two ago I started reading a new book on, among other things, the decline in trust in “experts” that is said to increasingly pervade Western societies. I’ve written previously about my scepticism that supposed experts are people we should repose much trust in, on things other than the most narrowly technical matters. I want an expert carrying any surgery I or my family need and when, for example, it comes to house renovations

A good architect, and capable expert builders and other tradespeople, can together enable an outcome that I couldn’t deliver myself. Most of us need, and value, expert advice, and expert execution, but the decision to renovate the house, and how far to go, is the customer’s. It is about choices and preferences on the one hand, and advice from experts who actually usually know what they are doing on the other.

It isn’t clear to me that there are very many areas of public policy where arrangements should be much different.

And I often wonder just how much real expertise – on matters beyond the most narrowly techical – can be found in most of the public sector agencies in which some encourage us to place our trust. The Governor of the Reserve Bank is one of those figures in whom the law places a great deal of power. Doubts about whether that is a wise choice, at least about the incumbent, were given further fuel by his performance on TVNZ’s Q&A last night.

I don’t have the time today to unpick it all, including his continued claim that fiscal policy is adding to demand/activity, when The Treasury’s fiscal impulse measure suggests it isn’t (all that has happend in the Budget update numbers is that fiscal policy is now estimated to have roughly a zero effect on demand over the next few years, rather than the slight drag previously projected). Orr seems to be champing at the bit to have the government spend more – especially capital spending – but he was careful and never quite said so last night.

Where he is much less careful is around investment more generally. Last night he followed up from his claim at last week’s press conference that the country was in a great condition, with the renewed suggestion that now was a wonderful time to invest, that businesses need to “keep going” on investing, and that it was hard to be nervous about investing with such low risk-free interest rates and (so he asserted) such low hurdle rates of return. (Doesn’t he follow the world news?) This wasn’t just so in New Zealand apparently: there were global “infrastructure deficits” and generational opportunities. Closer to home his extraordinary assertion was the New Zealand had only “quality problems” – the bizarre line John Key used to use about Auckland’s housing and transport problems.

You really have to wonder what insight the Governor thinks he is blessed with that eludes people in the private sector and in government, here and abroad. It isn’t as if he offers us a detailed piece of argumentation and analysis in support of his story. It seems to be mostly just handwaving and wishful thinking. Not exactly a sound basis for policy, or for encouraging us to put any trust in him.

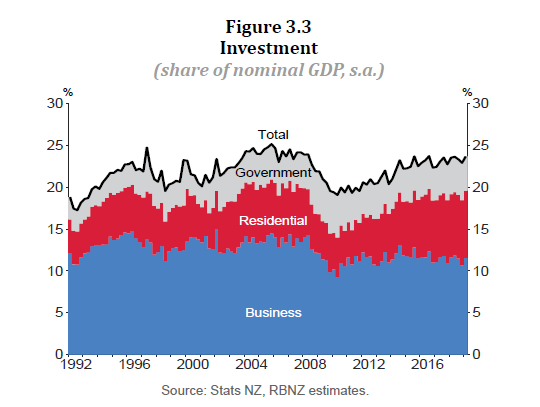

In writing about the MPS last week, I reproduced one of the Bank’s own charts about investment.

Business investment – in blue – has been fairly weak and (if anything) weakening further. It is not just some sort for post-election blues, businesses not liking having Labour and the Greens in office. The picture is pretty consistent for years now. Which suggests it might be reasonable to suppose that people who own, or are considering starting, businesses have been making rational choices, with the information available to them, about the prospects for investment in New Zealand. In sum, not particularly good – and this despite the considerable boost to demand (and need for domestic buildings etc) that a big unexpected shock to the population will have given rise to.

Consistent with that, the Governor may not be aware that productivity growth in New Zealand has also been lousy for years now – almost non-existent in the last few. Profitability and productivity are not, at all, the same thing, but they often go hand in hand – great opportunities, offering high returns to shareholders, are often ones that will tend to lift the overall productivity of the economy. New productivity opportunities are often only realised through a new wave of investment (which firms will only undertake if they expect those projects to be profitable).

And we could add to the list of symptoms – perhaps the Governor also counts them as “quality problems” – things like a tradables sector that has been going sideways, exports as a share of GDP not rebounding at all, the failure of the government to do anything material to fix the housing market, high corporate tax rates, and a range of actual or looming regulatory restrictions on investment opportunities in New Zealand. Not the sort of things most people would call “quality problems”.

Of course, the Governor is particularly keen on more public capital spending – infrastructure. But, here again, if the opportunities were so great, the numbers would be likely to speak for themselves – really high benefit/cost ratios showing up when projects are evaluated. Perhaps the Governor is privy to such estimates, but the rest of us are not so favoured. Too many of the projects that do go ahead seem like borderline cases at best.

Much of any reasoning the lies behind the Governor’s claims seems to rest on little more than the fact that interest rates are low. But in and of itself, that tells us almost nothing. After all, interest rates are (very) low for a reason, and as I noted in my post yesterday no one – including the Reserve Bank, at least based on anything they’ve shown or told us – has a compelling story about just what is going on and why. But the revealed behaviour of firms doesn’t suggest they’ve seen it as some windfall that means it is a great time to invest – with perhaps the only challenge being which of the abundance of riches of possible high-yielding projects one might tackle first.

Out of interest I had a look at other advanced countries. After all, these extraordinarily low interest rates prevail across almost all of the advanced world (and, as I’ve noted previously, implied forward rates are still higher here than in most countries). The IMF has data on total investment as a share of GDP for a group of 30+ advanced economies. In all of them, real and nominal interest rates are (of course) far lower than they were in, say, the 2000s prior to the 2008/09 recession. Notwithstanding that, for the median of these 35 advanced countries, investment as a share of GDP last year was 2.7 percentage points of GDP lower than it just prior to the crisis/recession. That is a significant reduction, despite the wonderful investment climate the Governor blithely talks of, in which it would be hard for anyone to be nervous about investing. Only four of the 35 countries had investment now higher than it was then (Sweden, Norway, Germany, and Austria – only Sweden more than 1 percentage point of GDP higher).

Now, these IMF numbers are total investment not business investment, and I don’t have the time today to recalculate the business investment numbers (for OECD countries), but it isn’t a picture that suggests that most people actually making investment choices share the blithe optimism of the Governor. It isn’t particularly confidence-inspiring, or suggestive that he knows much on this topic on which he opines so often.

He could, of course, be right. Perhaps there really are opportunities just left on the table, even though they offer high returns and/or modest risk. If so, the market is open. There is nothing to stop the Governor handing over the reins at the Reserve Bank and seeking an appointment as a private sector CEO, or indeed attracting capital from new investors to start his own enterprise.

I imagine most people will be content to respect the wisdom of crowds – without necessarily fully understanding it – and to conclude that when investment has been sluggish for years, even as aggregate demand is ok, labour is fairly fully-employed, and credit conditions haven’t been overly constraining that, despite the very low interest rates, there are huge numbers of attractive propositions going begging because people with their own money at stake aren’t persuaded by the Governor’s rhetoric.

We have very serious economic problems in New Zealand. They aren’t being addressed by our politicians or our officials, and the Governor seems more interesting in playing distraction, whistling to keep spirits up, than getting to the bottom of those really serious and longrunning economic failures. Fortunately, in his current role the Governor has almost no say over investment – other than to opine – but the lightweight rhetoric does nothing to instill confidence about his handling of those areas where he has great (and excessive) power: bank capital for example.

On other matters, an unexpected family death means I’ll be in Christchurch for the next few days and there won’t be any more posts until Monday.

There has been variety of comment on the self-fulfilling nature of business confidence. I’d say the wisdom of crowds doesn’t always work for economies – it’s more mood

LikeLike

I buy that argument in the short-term, but in the longer term (even 5-10 years) if the moods prove wrong, there will be unexploited super-profits just sitting waiting to be grabbed, and actual investment will pick up strongly again

LikeLiked by 1 person

What are we going to invest in? Clearly we are even lousy at selling milk products and we overproduce to sell at a loss.

LikeLike

As a small-time investor the rogue decision to ban further offshore exploration for oil and gas, which was done without forewarning or consultation or even “expert” advice, in order to curry favour with a small group of extremists, did it for me. Now we have the same actor jeopardizing the Treaty settlement process and the status of privately owned land. Invest in this country? Not until the coalition departs the scene.

LikeLiked by 2 people

The Treaty of Waitangi settlements are just a racist form of social welfare benefitting only one group based on their race.

LikeLiked by 1 person

The use of the word Crown is just misleading because it suggests that the British Crown is funding this welfare benefit. But these Treaty of Waitangi settlement monies come from the average NZ taxpayer, many of whose ancestral lineage has got absolutely nothing to do with what the British Crown got up to with Maori.

LikeLike

Your comments about experts are well taken. My own expertise is/was commercial computer software and many years ago I read that about a third of computer projects fail and another third fail to deliver all the customer’s initial requirements. So computer software is batting about 33%. Now retired I almost enjoy reading about Novopay.

My totally unmeasured layman’s appreciation of economists expertise is similar with all those 364 eminent economists writing to Margaret Thatcher being proven wrong and more recently the target of exports as 40% of NZ GDP also proving to be over-optimistic. Some economists are like soothsayers beholden to their employer. So I tend to trust unemployed economists.

Fortunately engineers work differently; most planes do not fall from the sky and most bridges do not collapse and when something unfortunate like that does happen usually there is a serious analysis and a lesson learned.

Incidentally if I had serious money to invest today I would choose Papua New Guinea over NZ.

LikeLike

I don’t suppose any serious economists had anything to do with that exports target – mostly the politicians at work.

Interesting call re PNG. The prospective returns are probably better, but the risks (of all sorts) must be enormous.

LikeLike

It was written about King Charles II that “He never said a foolish thing, Nor ever did a wise one” – he replied “This is very true: for my words are my own, and my actions are my ministers’….”.

Could we substitute NZ politician for words and their economic advisers for policies?

Re PNG – truly enormous risks but local knowledge is essential which means success doesn’t breed a mob of competitive imitators as per NZ. In PNG everyday is interesting. In PNG a successful business does more social good than in more developed countries so the effort is more satisfying.

LikeLike

Risks

Yesterday, the mighty Fonterra joined an illustrious group of NZ businesses who have ventured off-shore and failed. Can’t call their excursions a success

LikeLiked by 2 people

When interest rtes go down ,asset prices go up and returns are lower for longer. Thats why I won’t invest, stink returns and lots of risk.

I want an economy that can pay %10 and still be profitable. I started in business with %18 interest rates and i did fine today the economy is so bad we can hardly pay %3.

LikeLike

When interest rates hit 9% in 2007, businesses were already severely damaged with massive job losses, the complete decimation of our manufacturing industries and our building industries. The end result is now debt overburdened households and businesses due to bad decisions by a very hawkish RBNZ for decades.

Don’t forget that inflation was rising just as fast at 20% when interest rates were 18%, which allowed businesses to adjust selling prices to compensate for higher interest rates. But back then 30 years ago we were a closed economy and there was no such thing as low priced China manufactured products.

LikeLike

Consumers have the choice of spending or not, especially if things are looking risky. Friends in the UK have govt home starter loan where govt matches saving to help with deposit, two years later and underwater.

I always wondered how much OPEc was to blame for those high inflation years. Opec turned into a KSA and USA price fixing cartel.

LikeLike

PS: very sorry to hear of your breavement Michael.

LikeLiked by 1 person

Having created an enormous bureaucracy and costs to take quality and durability responsibility away from owners and developers I see they are now campaigning to add compulsory liability insurance requirements and costs to the building sector.

Little wonder productivity is poor and investment reluctant. Simply buy an existing property and wait for the Government to inflate its value by making construction more difficult and expensive.

LikeLiked by 3 people

Yes, I figured that out 18 years ago that Auckland does have serious geographical issues that prevent large scale high density building, ie 52 Volcanic sensitive zones ie potential lava flow sensitive now renamed as Viewshafts under the Unitary plan that cover 40 million sqm of Central Auckland, together with another 160 skm of National Parks in the Waitakeres and the Queens Chain that covers 8 metres along the length of every stream, puddling pools and waterways which meant all that infrastructure spend needs to go south creating enormous costs in connecting low density suburbs throughout a well spread out Auckland.

LikeLiked by 1 person

Looking at the Reserve banks credit figures (credit by sector; HC5) shows quite strong credit growth; broadly the same as a year ago. Housing and personal up about 6%, business 5.5% and agriculture 3%. All well ahead of inflation and nominal GDP growth. Employment is reasonably robust.

In light of that and the extraordinarily low interest rates generally, how and why did the RB decide we needed cheaper credit..

It really does sound like desperation and sapping of confidence in of itself: if interest rates are the lowest in four thousand years there has to be something seriously wrong with the whole thing. It feels like a frantic attempt to keep the debt on the books, the last gasp of a dying ponzi scheme almost.

Trust is the most valuable commodity there is, taking on debt or starting a family or a business is a bet on and trust in the future. This climate change hysteria and a lack of faith in the foundations of our culture can’t be helping one bit.

LikeLiked by 2 people

Not too sure what all the fuss is. Yes the property market has slowed a little but I see that as a good thing. I tried to secure good quality referred builders for a small development in Huntly and was told there are no Auckland based builders available and they are still very much neck deep in building work even if I offered extra dollars to get them on site. While there are plentiful of jobs and plentiful of tourists I really can’t see too much wrong at the moment. Managed to secure my tickets to Paris and then on to London for the Christmas and New Year holidays at a nicely discounted rate probably due to Brexit concerns.

LikeLiked by 1 person

I always thought that this was backwards: low interest rates do not create good investment opportunities, but are a consequence of the lack of good opportunities. For the last few decades, throughout the developed world, people are much richer than they used to be and are getting older. Some have maxed out their credit cards, but on balance most of them have been saving for retirement or for the kids. (Japan got there first.)

Add to that the pool of savings from China, and the world is awash in savings. What it does not have is a good range of investment opportunities – the returns to investment in manufacturing are close to “perfect competition” levels, and revenue streams protected by intellectual property law (pharmaceuticals) have been chipped away at by Government action to add cost and risk to development and shorten the patent protection. There has been a lot of investment in IT, with some good returns – but the serious money there has come from advertising revenue (Google, Facebook), which must be a relatively limited source compared to inventing the next auto industry. And finance has done well for itself, but largely by clipping the ticket on that vast pool of savings.

Good luck to Bob Atkinson for his investment in PNG – local knowledge is no doubt the essential survival skill. But opportunities in PNG are not going to absorb a few trillion dollars.

I know that central bankers are not slaves to the supply and demand for funds, but they surely cannot depart too far from equilibrium forever. The forces had been gathering long before the GFC, but that was the moment when they could no longer be resisted. So the low rates in NZ and overseas are largely the consequence of excess savings with few good investment opportunities.

If so, it won’t change until the excess savings are purged, and it is hard to see that happening. When rich folks die, their wealth is left to other members of society (largely their children, perhaps favourite charities, some to Government through taxes), but it does not simply disappear. Absent a great existential war like WWII (Syria and Afghanistan are too small to count) or outright confiscation and destruction of savings by fiat or by runaway global inflation, it is hard to see how savings could be reduced to match investment.

If that analysis is anywhere close to the truth, investors should plan for zero interest rates to continue for generations rather than for years. And Adrian Orr could use some of King Canute’s humility, because his exhortations are not going to have any effect on the global economic tides.

LikeLiked by 1 person

I agree with you Paul but something to ponder re savings and, specifically, your comment “the world is awash in savings”

Savings and debt are two sides of the same coin. What the market is saying and what the central banks are doing (and what perpetuation of the system requires) is incentivising the propensity to borrow. The way our monetary system works is that debt comes first and is balanced by an equal credit as an assett on the bank’s balance sheet which subsequently enters the system as “money”. The greatest fear is of a debt deflation and the consequent destruction of debt, credit and money itself.

Debt creates savings so perhaps it’s more useful to think of it as a “world awash with debt”.

What the Great God Tane (via his mouthpiece at the RBNZ) has decreed is: “get out there and borrow”

What could possibly go wrong!

LikeLiked by 1 person

Adrian Orr is Cook Islander of Irish ancestry. The Great God Tane is Maori. Perhaps Adrian Orr can’t hear nor understand the message?

LikeLike

Central bankers are not slaves to the supply and demand for funds but usually they are fairly disciplined in how they print money. We certainly do not want to use a wheelbarrow to shift the dollars around to pay for a loaf of bread.

LikeLike

“mostly just handwaving and wishful thinking”

Michael, you’re forgetting the magical new source of all knowledge in the Reserve Bank’s armoury: the Great Omniscient Tree God Tane.

Scientific analysis and accumulated wisdom are so Western centric, a product of the Patriarchy and driver of oppression; it’s a whole New Paradigm.

Or something.

LikeLiked by 2 people

Your remark triggered the thought why did a male RB guvernor committed to diversity choose a male deity as a guide? So googling ‘Maori goddesses’ I came across a table of Maori Gods family tree (at site labelled ‘not secure’ so no link provided). I’d be happy to be corrected and learn more about Maori mythology but the table is predominately male. However there are some goddesses so the RB could choose ‘Papatuanuku – earth goddess’ or ‘Hine-nui-t-po – goddess of death’. The same chart contains ‘Punga – ancestors of ugly creatures’ but doesn’t indicate gender.

LikeLike

Good question Bob. In mythology and across cultures, God is the masculine, the eternal ordering force, the known, civilisation. God spoke order into being from potential at the beginning of time according to genesis.

Feminine is undifferentiated potential – the sea, mother earth, the eternal mother, the unknown. It’s to do with the nature of the twin aspects of reality – order and chaos, night and day, the known and the unknown.

It doesn’t pay to get caught up in male and female though, masculine and feminine in this context are best described as spirits. Strange how these things are so widespread, universal between far flung cultures. The Dragon and the Taniwha for example and there is a fascinating, fundamental reason for that.

LikeLike

With regard to poor quality investment. The place to watch is how Wellington responds to the deteriorating housing crisis in its city. My take is that effective transformational reform is unlikely due to interlocking political constraints. Not because there isn’t economic solutions.

View at Medium.com

LikeLike

As of today, now is not a good time to invest

LikeLike

However you choose to advise not a good time to invest, you still have to invest somewhere. The choice still is invest in cash at a declining yield, investment in bonds, invest in shares, invest in plant and equipment, invest in upgrading your home or invest in a second or third property.

I don’t think bitcoin or under the pillow are viable options. I looked at bitcoin but kept getting my password with 50 keystrokes too difficult to recall and kept loosing my bitcoin account before I can even managed to buy any bitcoin.

LikeLike

Someone has profited immensely from share market downturns over the years. As per my point above, the emotion kicks in, the crowds sell out, while the long-term, clear-headed thinkers buys up the falling stock and ride out the storm.

LikeLiked by 1 person

Land, shares and bonds peaking; overvalued beyond their utility value? Faith in the system grumbling, Germany in recession, China stalling, interest rates at 4,000 year lows yet gold at what it was eight or nine years ago. Where would you go?

LikeLike

Gold has no income taxable activity and is considered speculation rather than as an investment so any profit is taxed by IRD at 33%.

LikeLike

Anyway, my thinking is still very much in favour of Auckland property as undervalued. I did think some of the premium suburbs were overvalued due to passionate bidding by foreign buyers but with the foreign buyers ban and China’s own fund transfer restrictions, the Auckland property market is starting to look undervalued in some areas especially where properties are in high density zones with the potential for multi unit dwellings.

An example would be the Terrace housing and apartment dwelling zones in Otahuhu are still priced for single dwelling properties even though many of these sites allow for 8 dwellings or more on 700sqm.

LikeLiked by 1 person

It was really intended as a rhetorical question GGS.

Having your central bank hell bent on destroying the one thing you would expect them to uphold, the time value of money, really does make one wonder if something tangible, transferable, portable and divisible outside the (current) financial system wouldn’t be a bad place to put at least some of your savings.

LikeLike

David: despite being convinced by the arguments made on this site about the mistakes of our RBNZ I’m much happier today anticipating my savings generated over a lifetime of diligent hard work, a modicum of luck and cautious family expenditure losing value by one or two percent per annum rather than my experience of the seventies in the UK where my savings were demolished by 25% inflation. Reagan’s thief in the night.

LikeLike

GGS: Do unto others as you would have them do unto you

Do you happily reside in a residence occupying 90 square metres of land (1/8th of 700 sqm)

LikeLike

I think you’re getting your Presidents mixed up there Bob.

Reagan was POTUS from 1981 to 1989. It was under his term that the high inflation was bought under control after Nixon put petrol on the fire with his decision to close the gold window – effectively defaulting on US debt and ushering in the burst of inflation that you refer to. There were also plenty of demographic and geopolitical factors at play in the 70’s that led to the high inflation apart from the final untethering of gold- oil shocks, the rise of OPEC, the arrival of the wave of boomers as consumers, restrictive and entitled unions and the lack of the billions of competing low wage economies and labour we have today.

It was the vision courage and tenacity of Reagan and Fed chairman Paul Volker that turned things round.

I know Reagan is often ridiculed but, for me, he was a great president – particularly for his faith and belief in liberty and the traditional values of hard work and personal responsibility and for his efforts to bring about the end of the hideous Soviet Union. Rest in peace Ronald Reagan.

LikeLike

Found the quote online: “” “Inflation is as violent as a mugger, as frightening as an armed robber, and as deadly as a hit man,” said Ronald Reagan in 1978 “”. The night thief may be some one else; I’m guessing there are many quotes about inflation.

From memory I believe Reagan was unusual in still being popular when he left office. The one thing he said that registered with me was something about often wondering what America was like when the first man stepped foot on it. I recall it when I get a view of Auckland city from the North Shore and wonder what the first Maori saw about 800 years ago and feel sad for what was lost.

LikeLike

Sorry Bob, I misunderstood the original Reagan reference.

Re the first steps of man; lets not forget the creativity, beauty and achievements of humanity and our ability to create a better world. I was talking recently with one of these alarmist eco types, they reacted with glee at the prospect of a global pandemic wiping out billions; frighteningly not uncommon. There is a ghastly, anti human undercurrent bordering on the genocidal within the eco movement. Be aware, the spirit of Cain is within us all.

This is what one of the Columbine killers had to say ( thoughts echoed by the recent US killers and by eco-fascist Tarrant) twenty years ago.

“The human race isn’t worth fighting for, only worth killing. Give the Earth back to the animals. They deserve it infinitely more than we do. Nothing means anything anymore”

Extract from Rule 6, 12 rules for life by Dr J B Peterson covering his thoughts on the mass killers, nihilism and the hatred of being.

LikeLiked by 1 person

While concurring with you about eco-terrorists lacking humanity you cannot say with confidence it will all work out OK in the end simply because it always has. Consider the fact that you and I and every living human being is the result of a successful live birth of parents who experienced the successful live birth and so on back to the dawn of time. But we cannot deduce from this every child birth throught history has been risk free. Read Jared Diamond’s “Collapse” for examples of societies that have collapsed and some have even disappearred (first viking settlement on Greenland).

It is known that education and pensions drastically cut the number of children parents choose to have. There are some interesting figures for Iran where despite the best efforts of a Muslim govt determined to outnumber rival nations they still cannot persuade families to have the large familes that they used to have.

It is reasonable to say for the entire world that our current way of life with its economics and use of resources is just not sustainable. The problem with those who look forward to the extinction of most of humanity is firstly their inhumanity and secondly the historic precedent that it is the noble and the worthy and the kind-hearted who get killed and the survivors are remnents of the violent and primitive (ref survival and extinction of many North American tribes).

LikeLike