A day or two ago I started reading a new book on, among other things, the decline in trust in “experts” that is said to increasingly pervade Western societies. I’ve written previously about my scepticism that supposed experts are people we should repose much trust in, on things other than the most narrowly technical matters. I want an expert carrying any surgery I or my family need and when, for example, it comes to house renovations

A good architect, and capable expert builders and other tradespeople, can together enable an outcome that I couldn’t deliver myself. Most of us need, and value, expert advice, and expert execution, but the decision to renovate the house, and how far to go, is the customer’s. It is about choices and preferences on the one hand, and advice from experts who actually usually know what they are doing on the other.

It isn’t clear to me that there are very many areas of public policy where arrangements should be much different.

And I often wonder just how much real expertise – on matters beyond the most narrowly techical – can be found in most of the public sector agencies in which some encourage us to place our trust. The Governor of the Reserve Bank is one of those figures in whom the law places a great deal of power. Doubts about whether that is a wise choice, at least about the incumbent, were given further fuel by his performance on TVNZ’s Q&A last night.

I don’t have the time today to unpick it all, including his continued claim that fiscal policy is adding to demand/activity, when The Treasury’s fiscal impulse measure suggests it isn’t (all that has happend in the Budget update numbers is that fiscal policy is now estimated to have roughly a zero effect on demand over the next few years, rather than the slight drag previously projected). Orr seems to be champing at the bit to have the government spend more – especially capital spending – but he was careful and never quite said so last night.

Where he is much less careful is around investment more generally. Last night he followed up from his claim at last week’s press conference that the country was in a great condition, with the renewed suggestion that now was a wonderful time to invest, that businesses need to “keep going” on investing, and that it was hard to be nervous about investing with such low risk-free interest rates and (so he asserted) such low hurdle rates of return. (Doesn’t he follow the world news?) This wasn’t just so in New Zealand apparently: there were global “infrastructure deficits” and generational opportunities. Closer to home his extraordinary assertion was the New Zealand had only “quality problems” – the bizarre line John Key used to use about Auckland’s housing and transport problems.

You really have to wonder what insight the Governor thinks he is blessed with that eludes people in the private sector and in government, here and abroad. It isn’t as if he offers us a detailed piece of argumentation and analysis in support of his story. It seems to be mostly just handwaving and wishful thinking. Not exactly a sound basis for policy, or for encouraging us to put any trust in him.

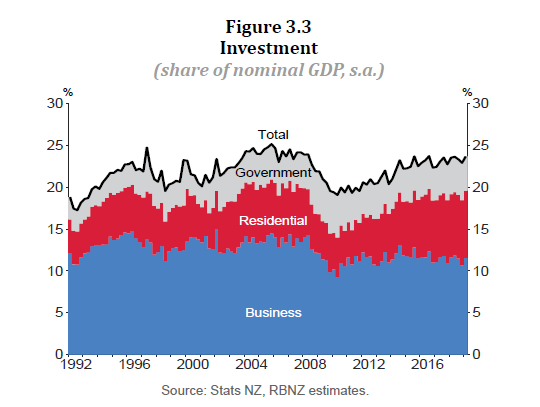

In writing about the MPS last week, I reproduced one of the Bank’s own charts about investment.

Business investment – in blue – has been fairly weak and (if anything) weakening further. It is not just some sort for post-election blues, businesses not liking having Labour and the Greens in office. The picture is pretty consistent for years now. Which suggests it might be reasonable to suppose that people who own, or are considering starting, businesses have been making rational choices, with the information available to them, about the prospects for investment in New Zealand. In sum, not particularly good – and this despite the considerable boost to demand (and need for domestic buildings etc) that a big unexpected shock to the population will have given rise to.

Consistent with that, the Governor may not be aware that productivity growth in New Zealand has also been lousy for years now – almost non-existent in the last few. Profitability and productivity are not, at all, the same thing, but they often go hand in hand – great opportunities, offering high returns to shareholders, are often ones that will tend to lift the overall productivity of the economy. New productivity opportunities are often only realised through a new wave of investment (which firms will only undertake if they expect those projects to be profitable).

And we could add to the list of symptoms – perhaps the Governor also counts them as “quality problems” – things like a tradables sector that has been going sideways, exports as a share of GDP not rebounding at all, the failure of the government to do anything material to fix the housing market, high corporate tax rates, and a range of actual or looming regulatory restrictions on investment opportunities in New Zealand. Not the sort of things most people would call “quality problems”.

Of course, the Governor is particularly keen on more public capital spending – infrastructure. But, here again, if the opportunities were so great, the numbers would be likely to speak for themselves – really high benefit/cost ratios showing up when projects are evaluated. Perhaps the Governor is privy to such estimates, but the rest of us are not so favoured. Too many of the projects that do go ahead seem like borderline cases at best.

Much of any reasoning the lies behind the Governor’s claims seems to rest on little more than the fact that interest rates are low. But in and of itself, that tells us almost nothing. After all, interest rates are (very) low for a reason, and as I noted in my post yesterday no one – including the Reserve Bank, at least based on anything they’ve shown or told us – has a compelling story about just what is going on and why. But the revealed behaviour of firms doesn’t suggest they’ve seen it as some windfall that means it is a great time to invest – with perhaps the only challenge being which of the abundance of riches of possible high-yielding projects one might tackle first.

Out of interest I had a look at other advanced countries. After all, these extraordinarily low interest rates prevail across almost all of the advanced world (and, as I’ve noted previously, implied forward rates are still higher here than in most countries). The IMF has data on total investment as a share of GDP for a group of 30+ advanced economies. In all of them, real and nominal interest rates are (of course) far lower than they were in, say, the 2000s prior to the 2008/09 recession. Notwithstanding that, for the median of these 35 advanced countries, investment as a share of GDP last year was 2.7 percentage points of GDP lower than it just prior to the crisis/recession. That is a significant reduction, despite the wonderful investment climate the Governor blithely talks of, in which it would be hard for anyone to be nervous about investing. Only four of the 35 countries had investment now higher than it was then (Sweden, Norway, Germany, and Austria – only Sweden more than 1 percentage point of GDP higher).

Now, these IMF numbers are total investment not business investment, and I don’t have the time today to recalculate the business investment numbers (for OECD countries), but it isn’t a picture that suggests that most people actually making investment choices share the blithe optimism of the Governor. It isn’t particularly confidence-inspiring, or suggestive that he knows much on this topic on which he opines so often.

He could, of course, be right. Perhaps there really are opportunities just left on the table, even though they offer high returns and/or modest risk. If so, the market is open. There is nothing to stop the Governor handing over the reins at the Reserve Bank and seeking an appointment as a private sector CEO, or indeed attracting capital from new investors to start his own enterprise.

I imagine most people will be content to respect the wisdom of crowds – without necessarily fully understanding it – and to conclude that when investment has been sluggish for years, even as aggregate demand is ok, labour is fairly fully-employed, and credit conditions haven’t been overly constraining that, despite the very low interest rates, there are huge numbers of attractive propositions going begging because people with their own money at stake aren’t persuaded by the Governor’s rhetoric.

We have very serious economic problems in New Zealand. They aren’t being addressed by our politicians or our officials, and the Governor seems more interesting in playing distraction, whistling to keep spirits up, than getting to the bottom of those really serious and longrunning economic failures. Fortunately, in his current role the Governor has almost no say over investment – other than to opine – but the lightweight rhetoric does nothing to instill confidence about his handling of those areas where he has great (and excessive) power: bank capital for example.

On other matters, an unexpected family death means I’ll be in Christchurch for the next few days and there won’t be any more posts until Monday.