The macroeconomic news of the day will be around the Reserve Bank’s Monetary Policy Statement this afternoon. But yesterday afternoon the Bank published the results of its quarterly survey of (somewhat expert) expectations.

There wasn’t much newsworthy in the survey results. Across this group of respondents, the median expectations for the inflation rate two years ahead, five years ahead, and ten years were 2.00, 2.00, and 2.00 per cent. The Bank will be pleased. Unfortunately for the Bank, market prices (from the market in indexed and conventional government bonds) suggest something close to 1.0 per cent (my own responses to the survey were not that low, but were in the lower quartile of responses).

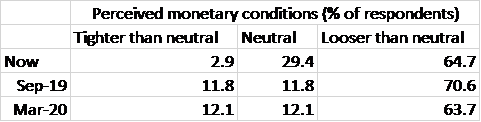

The questions that caught my eye were those around monetary conditions. Respondents are asked (on a 7 point scale) how they perceive monetary conditions at present, in three months time, and in nine months time. It is entirely up to each respondent how they interpret “monetary conditions” – what weight they put on each of, say, interest rates (short or long), exchange rates, credit conditions, share prices, or whatever. Here are the summary results

A huge majority of respondents think current monetary conditions are looser than neutral (“neutral” is the Bank’s own term) and expect them to stay that way.

But the surprise was the shift, expected over the coming quarter, from neutral to tighter than neutral. Sure, the survey was taken almost two weeks ago, but even then market prices were clearly centred on the prospect of an OCR cut – whether today or in August – with no commentator I’m aware of expecting an OCR increase. (And in the same survey three months ago, there was an expectation of a slight shift towards less-tight conditions.)

Who knows what respondents had in mind. It can’t have been the exchange rate – the survey asks for exchange rate expectations and they aren’t rising – so perhaps it was something about credit conditions. Then again, it is a fairly small sample (33 respondents) so perhaps a couple of people just read the options the wrong way round.

What about OCR expectations themselves? The survey asks about expectations for the OCR as at the end of June and at the end of March next year. The median response for June was still 1.75 per cent – no change now or at the OCR review at the end of June – in a survey taken only 10 days ago. The median expectation is for only one OCR cut by then , but the lower quartile response is 1.25 per cent, and at least one person (wasn’t me) is picking 1.0 per cent by then. (On the other hand, at least one respondent thinks the OCR will have been increased to 2 per cent by March.)

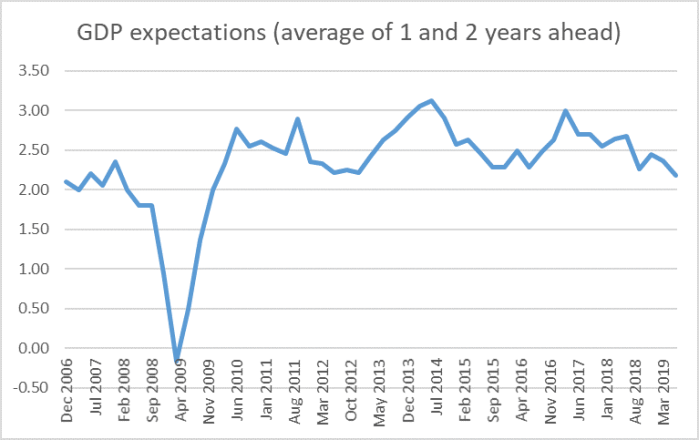

And the last result that caught my eye was this one. Respondents are asked for their expectations of GDP growth for the year ahead and then for the year beyond that. This chart shows the average of those two expectations.

The latest results are lower again, and are now at the lowest level since December 2009. Expectations of this sort aren’t particularly useful as forecasts (lots else will change), and often largely reflect what has already been seen. And the latest decline isn’t severe in the long-run history of the serious. But it isn’t exactly a rosy picture either. Respondents don’t see anything on the horizon likely to accelerate growth rates. All else equal, there isn’t much suggesting core inflation will rise.

There is a pretty good case for the OCR to be lower. Then again, there was a good case (probably stronger) for a cut to official interest rates in Australia yesterday, and it didn’t happen – the statement read like a central bank desperate not to cut, despite an agreed inflation target they’ve been badly undershooting. I doubt our Governor will be desperate not to cut, but whether he and his new colleagues actually do so today we won’t know for a few hours yet.

The question about monetary conditions puzzles me, too. When I answer it, I have some roughish overall mix of interest rates and exchange rates in my head but my feeling is that most respondents have only interest rates in mind. I’ve a vague memory of a graph someone did a while back (me? you?) showing a close link between the response to the monetary conditions question and the level of interest rates. As you note, there are separate questions about interest rates, and maybe that should alert respondents to the fact that the conditions question is different, but I’m not sure that’s how it’s actually answered.

It’s also possible that the shift in the latest reading to more ‘tighter than neutral’ responses may reflect some credit rationing or tougher credit standards – the ANZ’s business survey has been picking up large net negative balances reporting tightness of credit availability.

LikeLike

I am thinking they are overwhelmingly looking at interest rates, which is wrong.

LikeLike

So we’re down to 1.5% OCR, elderly savings are probably earning negative real after tax returns, and next stop has to be world economic stagnation/recession. So I assume we’re now totally in Harry Potter land in our crumbling command economies and NZ like US will be on NIRP for next recession. I’m thinking that, so am moving savings from all banks to treasuries and bond funds. We’ll never see rising interest rates again unless there is paradigm change.

I think central banking, via hubris, is a huge failure and everything is now broken with the only certainty being misery when shares correct by 60%. You don’t totally destroy price discovery and yield and get away with it with your shirt still on.

LikeLike

Yes, and more insidiously, it is not the savings of the elderly that matter to central banks. In general, the elderly are not the productive sector of our economy – they are not the future. When the Governor explained that the intention of the cut was to stimulate “borrow and spend”, he wasn’t aiming that at the elderly to go out and diminish their savings. He was telling the current generation of workers not to bother saving. It’s a fools game.

LikeLike