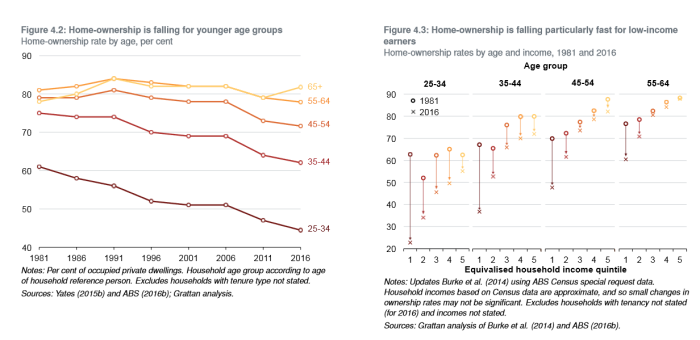

Last week a reader sent me the right hand part of this set of charts

The data are for Australia, but it is hard to believe that, if we had up-to-date census data, the pictures now would be much different for New Zealand.

I’ve seen charts like the left hand one for New Zealand, but what I found sobering – and frankly scandalous – were the results for lowest and second lowest quintiles in the right hand chart.

A decent society has to be judged, in considerable part, by how it treats the poorest and most vulnerable among us. People can run all the clever lines they like about how many of the people in those bottom quintiles have things now that comparable people in 1981 didn’t have. But it is doesn’t excuse the entirely manmade disaster of the housing markets in New Zealand and Australia (and various other places).

In 1981, when our societies as whole were substantially materially poorer than they are now, (Australia’s real GDP per capita was about 80 per cent higher in 2016 than in 1981), young people at the lower end of the income distribution was just as likely to own their own home as those at the upper end of the income distribution. But now people at the bottom are less than half as likely to own their own place. In a well-functioning market that simply wouldn’t have happened. But we – and Australia – having housing and urban land markets rigged by central and local government politicians and their officials, and the people at the bottom are the ones who how most severely and adversely affected.

Sometimes people will try to tell you that preferences have changed, such that young(ish) people no longer want to own their own place to the same extent. But look at how little the home ownership rates for the upper quintiles have changed. That alone suggests that people are being forced to adjust to new affordability constraints, not that a whole generation of young people – given the opportunity – no longer prefer to own their own place.

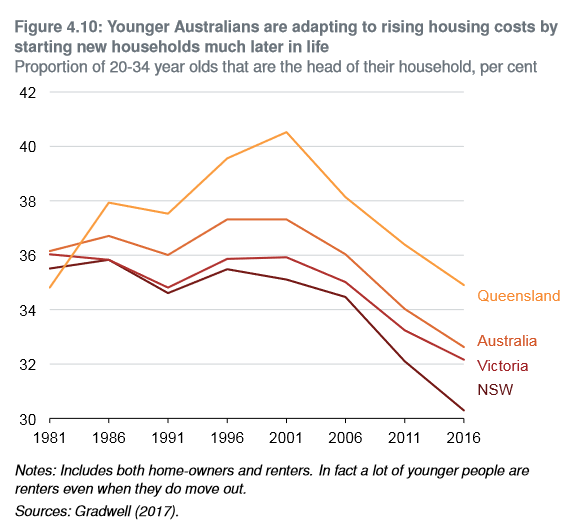

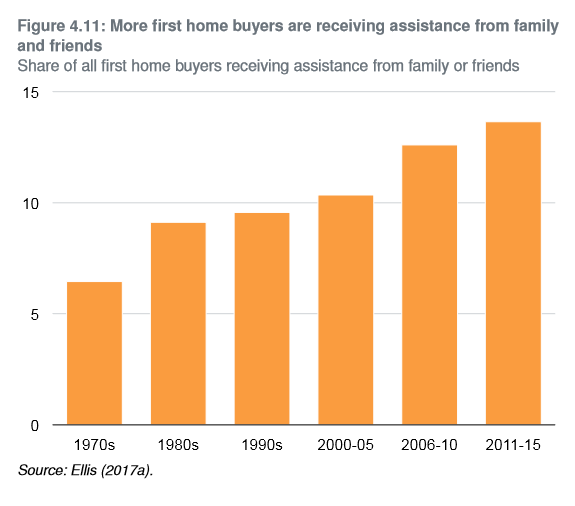

The chart is taken from a pretty substantial report by the Grattan Institute, a centre-left think-tank in Australia. Flicking through some of the report, I found a couple of other charts.

One of the ways of adjusting to new, artificial, affordability constraints is simply to stay living at home for longer.

Another is to get financial support from family.

Back when real incomes were half what they are now (1970s), most people (in all quintiles) buying a first house by the time they were 34. Now only about 35 per cent of lower income people are buying a first house by the time they are 44, and a much increased share of the (reduced percentage) buying a first home at all are needing financial help from family (presumably mostly) to do so.

There is simply no need for any of this – the more so in a decade in which interest rates (and thus mortgage servicing costs) are lower than they been for generations. It is what our governments have done to us, most notably to the poor among us. It is shameful.

There are no excuses. One day, those responsible (from both sides of politics) will face the judgement of history for their active complicitly, or quiet indifference.

And no, a capital gains tax would have made no material difference to any of these outcomes – these are, recall, Australia data, and Australia had no CGT in 1981 but does now. But perhaps some of the passion that fired those now so upset with the Prime Minister did reflect a sense of the failure of leadership in addressing this fundamental, longrunning, failure of policy around housing and urban land. There is a real opportunity for the Prime Minister – or for the Opposition – to take a decisive policy lead, and actually make a change for the good, for the poor in particular.

You are angry and you are right to be angry.

What is the target – back to a house price three times an average income? Moving average Auckland prices from about $1m to $400k with entry properties about $150k? Not too difficult to achieve but how to get there without great unfairness? I’m thinking of hard working couples who have bought in the last five years who have a mortgage burden for their working life unless there is significant inflation.

Another point is the wide difference in prices from rural to urban – from what I saw along the Otago cycleway there are empty houses just waiting for inhabitants.

LikeLiked by 1 person

I’ve argued previously for a partial compensation scheme for owner-occupiers

https://croakingcassandra.com/2017/08/03/a-fresher-approach-for-ordinary-new-zealanders/

LikeLike

“Another point is the wide difference in prices from rural to urban – from what I saw along the Otago cycleway there are empty houses just waiting for inhabitants.”

Unless someone is working entirely from home, housing has to be within commute distance of a job. Cities exist for that reason – i.e. people have to live near their jobs.

LikeLike

Fairly self-evident. But there are many who work from home: artists, some computer programmers and call centre responders for example. But they choose to live near other people despite the housing costs.

This weekend’s Country Calendar told the story of the forestry contractor unable to find employees – his best staff come from Fiji leaving their families behind. I’ve heard much the same about dairy workers from the Phillipines and fruit pickers from everywhere. The same forestry contractor said how when he started working a hard-working forester earned above NZ average wage but now it is barely above living wage despite the jobs risks and physical demands.

Our current accommodation allowances maximums are based on location:

(a) $305 a week, if the applicant resides in Area 1: most of Auckland

(b) $220 a week, if the applicant resides in Area 2: eg Hamilton urban zone

(c) $160 a week, if the applicant resides in Area 3: eg Gisborne urban area

(d) $120 a week, if the applicant resides in Area 4: Rural

If they were reversed some low waged New Zealanders would move away from our over-crowded cities. The extra money would assist small towns more than Shane Jones efforts.

LikeLiked by 1 person

It would be interesting to get Phil Twyford and Judith Collins together in a room and ask each in the presence of the other to ask for their solutions.

Time for Jacinda to spend some her recently acquired political capital. Also for Grant Robertson to give up some of his right-leaning deficit aversion in pursuit of lowering land values.

LikeLike

Your analysis ignores the beneficiaries of the housing shortage. So long as a significant proportion of voters have a financial interest in high property values the housing situation will never be fixed.

LikeLike

As I’ve argued here for several years, I’m not at all optimistic about anything worthwhile being done in horizons relevant to me (my lifetime and the purchase horizon of my kids). But “never” is a long time, and rebellions happen.

Practically, I’ve argued previously for a partial compensation scheme for owner-occupiers (most of whom don’t benefit from high property prices but some of whom could be very badly hurt by sharp falls in property prices).

https://croakingcassandra.com/2017/08/03/a-fresher-approach-for-ordinary-new-zealanders/

LikeLiked by 1 person

Without any plan on my part I’ve doubled my wealth just living semi-retired in Auckland for 15 years. If house prices returned to a level that was optimum for the benefit of all New Zealanders my property (which is my only wealth) would be worth about 30% of its current value. So I am part of that proportion of voters who you might think would have a financial interest in stopping any fix to the housing situation. However we have adult children.

Before the last election at a public meeting held by TOP the majority of the audience were elderly and remarkably enthusiastic for policies that would have made them poorer. It is the young who are more selfish than the old. If you want to start a family you have little choice but to be graspingly materialistic.

It is time a political party made a clear case for reducing house prices, setting clear targets, protecting those who would unfairly suffer from such targets and then explaining the policies they would use to achieve their objective.

LikeLiked by 2 people

Your property under the Auckland Unitary plan now allows for multiple dwellings. Even single dwelling zones allow 2 dwellings with 2 separate kitchens but must be attached to the main dwelling. The only restriction is a 6 metre Outlook space which is roughly around a 25 sqm living space.

LikeLike

I’m not sure that yelling about central Govt is really getting anyone anywhere. A root cause analysis would likely reveal that one of the biggest cost drivers for new builds (and by extension the flow on effect through all property prices) is the actions/inactions of local councils.

In Auckland, once you’ve paid $25k for the development contribution and $13k for the Watercare connection and the GST on the purchase its easily over $100k… not to mention the plethora of council inspections (they all have to be paid for by the developer/builder) and the council fees for getting a consent in the first place.

Building materials are expensive in NZ; no question about that. However, useful and meaningful innovation in building systems is almost unheard of in NZ. My thesis is that local councils, through they building codes/inspections etc are actively biased against anything new/different that could make a meaningful contribution to lowering costs. If they don’t like anything they won’t issue a Code of Compliance Certificate (CCC) and then the property, even if finished, cannot be occupied.

And yet… there are houses 70 – 80+ years old that resolutely fail to fall down; however, one look at the building code would suggest that all houses more than 10 years old should be in ruins… It just doesn’t add up…

So my view is that in no small part the excessive cost of housing in NZ (and other places) can be laid at the feet of capricious and malevolent local councils and their bevy of inspectors and officials. They cannot and will not innovate and we all suffer from their actions.

LikeLike

You left out the $60k to $100k in public drainage facilities which the developer has to also pay. This cost is usually a council cost or a government cost previously and in most other cities. The public drainage has to be completed and then gifted to Council. The amount gifted is only the cost of the materials. The artificial perception created is that the cost is only say $20k. What is missing is the earthworks cost and the cost to install and a drainage engineer to sign off.

LikeLike

I’m sympathetic to all these points, but the biggest single component in an urban house price is the land price – and that is largely regulatorily-created artificial scarcity.

LikeLiked by 1 person

In Auckland, the Waitakere National park covers 160 skm and the Viewshafts or previously known as Volcanic Sensitive zones cover 40 million sqm with 57 volcanos. In effect, it is not an artificial restriction but a sensible geological restriction. If any one of these volcanos spews lava, you don’t want high density high rise anywhere close by.

LikeLike

+1 – A decent society has to be judged, in considerable part, by how it treats the poorest and most vulnerable among us.

There are some external forces

1) deregulation of the credit markets since the 1980’s

2) worldwide low interest rates pushing up asset prices

3) previously – some flow of international money looking for a safe haven

but most of it lies with the government

i) immigration rate too high

ii) RMA rules – zoning & density & urban design

iii) construction materials duopoly

iv) developer contributions (up front captial cost) instead of targeted rates (rather than paid through cashflow)

v) individual certification of prefab building sites rather than by prefab type

vi) Councils arent required to rate on land value only (effectively a land tax by other means)

vii) Intergenerational equity & failed policy – Students saddled with student debt (unable to raise enough capital for a house deposit)

8) Local government is screaming for additional funding (I dont mind as long as its backed by business cases)

Hopefully we’ll see some change

a) Twyford is making the right noises

b) Government is paying a fortune in emergency accommodation & accommodation supplements

c) Productivity commission looking at local government funding (personally I’d prefer local government being able to rate central government land as the way to raise revenue but it seems to be purposely out of scope – its the simplest way to remove the distortion & funding shortfall)

c) Articles like this one continue to point out the injustice

LikeLiked by 3 people

Sensible summary. Your idea of applying rates to central govt land is new to me and I like it. I have trouble with the cost of rates in cities being too low and in quiet small towns with minimal infrastructure development too high. Of course it works well for me and I complain like everyone else when the Auckland rates demand arrives but I have a vague recollection of London’s rates being higher.

LikeLike

With Jacinda Ardern taxing CGT she is now looking at a Landbankers tax. Bob, unfortunately you are likely to be considered a landbanker now that your 900sqm site allows for perhaps as many as 4 dwellings.

LikeLike

Correction: Jacinda Ardern axing CGT.

LikeLike

Very good your list of external forces however needs to be expanded

There are some external forces

1) deregulation of the credit markets since the 1980’s

2) worldwide low interest rates pushing up asset prices and the subsequent suppression of interest rates

3) previously – some flow of international money looking for a safe haven

4) The Central Banks printing trillions of $ after the GFC as per above

5) Our Banks borrowing 10’s of billions offshore and funnelling these funds into housing mortgages.

LikeLike

As a reminder of why I don’t buy the story that monetary policy or financial deregulation is really at the heart of the issue

https://croakingcassandra.com/2019/04/13/entry-level-house-prices-in-us-cities/

It is domestic choices around land use and related policies – here, Australia, in the UK, and in many areas in Canada and the US as well, but not (importantly) in many other parts of the US.

LikeLike

Actually, if you are highly indebted, the easiest way out of debt is to inflate your assets.

LikeLike

I think a basic problem with our nation is that only the favoured few get to ask questions of the favoured few.

LikeLike

My view is that monetary inflation has played a part. In 1985 M3 money was about $85 billion… Now is is around 300 billion.

Lowell Manning wrote an interesting piece, …which I largely agree with

https://www.interest.co.nz/opinion/64724/lowell-manning-says-problem-housing-stems-current-account-deficits-and-foreign

LikeLike