The upside of a decent memory and a pretty comprehensive diary is that one is reminded of how many things one misjudged, or at least sees differently now, over the course of decades. In my case, the stock market crash of 1987 was one of those events.

There were excuses I suppose. I was young – just 25 – and had only just come back from two years at the (central) Bank of Papua New Guinea – a place where I’d learned a great deal about economics, politics, regulation, statistics and so on but where, from memory, there were about five, rarely-traded, public companies. In late August 1987, I’d taken up the role of Manager, Monetary Policy at the Reserve Bank, working for (current “acting Governor”) Grant Spencer. The Reserve Bank wasn’t (formally) operationally independent at the time, and my section was responsible for our monetary policy analysis and advice, including that to the then Minister of Finance. It was a very different world. The Bank produced macroeconomic forecasts, but they weren’t that important in how policy was run. We didn’t set an official interest rate, and to the extent we were guided by any financial market indicators, the “yield gap” – between 90 day bill rates and five year government bond rates – was the most important indicator. My diary suggests my team spent a considerable portion of late 1987 working on a paper on the yield gap and the making sense of the slope of the yield curve, for a new Associate Minister who had trained as an economist and was intrigued.

Official doctrine was that it was very hard to interpret the level of interest rates. It was only three years since we’d liberalised, so didn’t have much sense of an appropriate interest rate in normal circumstances, and these circumstances were anything but normal (hence the focus on the yield gap – if short-term rates were well above long-term rates then, in a climate where we were trying to drive down inflation, we couldn’t be too far wrong). Much the same line applied to interpreting the exchange rate. Both interest rates and the exchange rate were extraordinary volatile.

We didn’t really have a good model for forecasting, or making sense of, inflation either. Again, that wasn’t really surprising. So much had been liberalised quite quickly and a lot of economic relationships that had once held up no longer did. Our basic approach was that inflation was a monetary phenomenon, but it wasn’t as if the monetary or credit aggregates could then give us much useful guidance either.

The focus was on bringing inflation down. It was the one thing we knew the Reserve Bank could do, especially once the exchange rate had been floated, and I don’t suppose there was anyone who opposed that broad goal. There wasn’t a very specific goal, but for some time the talk had been of “low single figure inflation” which was, at least at times, seen as emulating the success of the UK and the US earlier in the 1990s in bringing inflation down.

But inflation itself was all over the place.

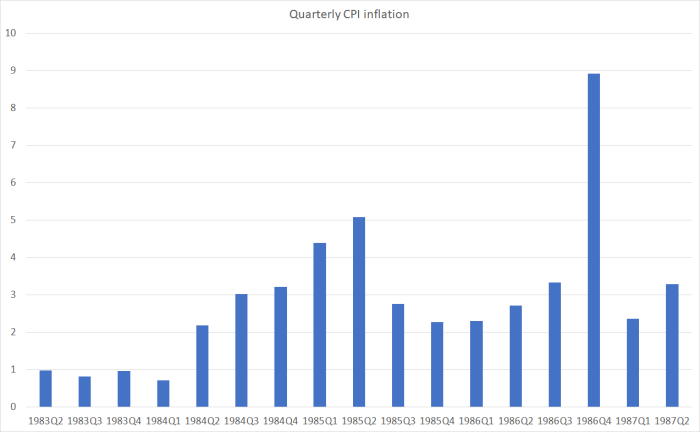

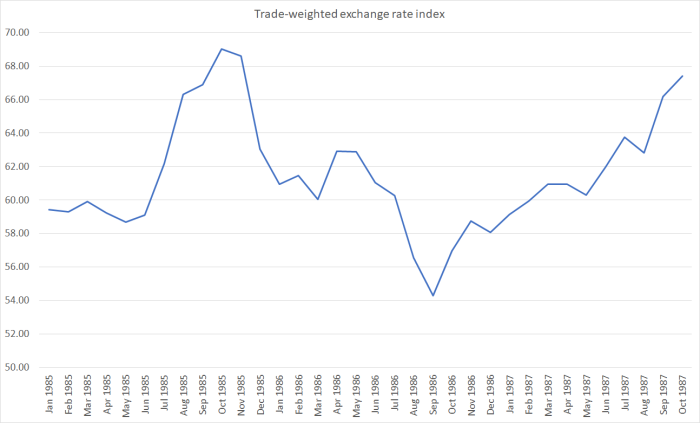

Annual headline inflation was 18.9 per cent in the year to June 1987. Much of that reflected the introduction of GST in October 1986, but even abstracting from that quarterly inflation was volatile, and disconcertingly high. There had been a sense that by early 1986 things were coming under control – hence the sharp fall in interest rates in mid 1986 (see earlier chart) – but that proved illusory. Just before I came back to the Bank in August I recall seeing Grant Spencer interviewed on TV after the June quarter 1987 CPI numbers came out: quarterly inflation of 3.3 per cent (I think the Bank had been expecting something nearer 2 per cent) left the Chief Economist “flabbergasted”. Low single figure inflation seemed a long way away, as the commercial construction boom, and the debt-fuelled sharemarket boom and associated strength in consumption raged on. The (volatile) exchange rate offered some solace – at the time, the pass-through from the exchange rate into domestic prices was still quite strong (we assumed something like a 46 per cent pass through) – although I’m sure we all remembered that after the devaluation of 1984, a key policy priority had been cementing-in a much lower real exchange rate. (As a young graduate analyst, I’d been the minute-taker in various meetings on that theme involving the great and the good of the Reserve Bank and The Treasury).

And so in September 1987, the biggest concern in the Economics Department of the Reserve Bank was that we were making little or no progress in getting inflation back down again. Perhaps we weren’t going back to the 15 per cent inflation we’d often seen before the wage and price freezes of 1982 to 1984, but there didn’t seem much reason for confidence that once the GST effects dropped out we’d settle at much below 10 per cent annual inflation. That wasn’t good enough for the government – newly re-elected, and just about to launch the next wave of reforms – or for us.

Other parts of the Reserve Bank may have had different perspectives. We didn’t do much banking regulation or supervision in those days, but a new function was just getting going, and I didn’t have much to do with them. Our Financial Markets Department was probably a little more focused on the excesses in the markets – including the big speculative plays on the NZD – but the Bank wasn’t responsible for equity markets, and we didn’t have a “macro-financial stability” type of analytical function there or in Economics. At the time we didn’t pay very much close attention to what was going on in other countries, but had we done so, we’d probably have seen a bunch of smallish economies undergoing similar post-liberalisation experiences (Australia and the Nordics), while congratulating ourselves that at least we’d floated our exchange rate (which the Nordics hadn’t).

But our focus in September/October 1987 was on tightening monetary policy if at all possible. And on 7 October 1987, we’d actually announced a discrete monetary policy tightening (implemented by an increase in the margin above market rates at which we would buy back short-dated government securities from the market). We’d tried to buttress the case for a tightening by arguing that the strength of the stock market was an indicator of demand and inflation pressures, but an older and (with hindsight) wiser senior manager insisted we remove that line. My diary records that I thought the tightening was “pretty feeble” and that at a market function immediately after the announcement at least one of the market economists I talked to agreed (Grant Spencer, to his credit, disagreed). Actual interest rates didn’t rise very much at all – at least in the way we thought about things then – but by 16 October 90 day bank bill rates were 20.56 per cent. There was no unease from the Beehive – my diary for 15 October records of a meeting with Roger Douglas and his associate only “the latter almost gleeful at having closed almost 450 Post Offices”.

In many ways, our stance to this point was quite justifiable. A key element of the macroeconomic management agenda ever since the 1984 election had been to end New Zealand’s really bad record of inflation. And that was the Reserve Bank’s job. Moreover, even if we had properly recognised the ever-growing fragility of the financial system etc, neither we – nor anyone else – had any way of knowing when those risks would crystallise. Persistent strong domestic demand, even if built on foundations of sand, represented a serious threat to any sort of success in lowering inflation to what were, by then, becoming more internationally conventional levels. So it probably wasn’t wrong to have tightened on 7 October, and may not even have been wrong for people like me to think that more tightening might yet be required. Annual money and credit growth rates were, after all, still running at around 20 per cent – indeed, a couple of days after the crash began we got new numbers that I called “presentationally (and factually) very embarrassing when [our chief critics] get hold of it”. If there was a real squeeze on the tradables sector – and there was – the unemployment rate in mid 1987 was stable at around 4.2 per cent (lower than it is today). At the time we didn’t really believe that seriously high unemployment would, for a time, be required to get inflation down – I recall an IMF mission chief at the time reproaching us for this view – probably partly because after three years, unemployment hadn’t risen. But whatever the truth of the matter, 4.2 per cent unemployment, amid a major economic restructuring, wasn’t exactly the 3 million unemployed of Thatcher’s Britain earlier in the decade.

So if there was a criticism to be made – and I think it is probably fair that one should – it was that we simply weren’t prepared for what followed. There may have been people at the Bank – older and wiser than me – who saw things differently then, and if so all credit to them. But I was pretty closely involved on the monetary policy side throughout the following five years and I don’t think my blindspots were particularly unusual (I wrote many of the major papers, including the first ever Monetary Policy Statement, which has little or no sense of a post credit-boom bust to it_. Again, it is possible that our banking supervision people saw things differently, but banking supervision – such as it was – didn’t impinge on monetary policy or our macroeconomic forecasting and analysis. We never really worked through what an asset bust and financial crisis meant for economic developments and prospects, and mostly treated them as peripheral issues.

On 20 October itself – the first day of the crash in New Zealand – I recorded in my diary “Bank not at all twitchy yet, which is good, and Douglas put on a brave face tonight”. I saw the risk of economic contractions and real wealth effects, but for some reason seemed to see the risks as mainly those from abroad (commercial property busts overseas associated with potential credit contractions, recessions, falls in commodity prices etc) and thus potentially helpful in our own disinflation efforts. For some – now unaccountable – reason I noted that I didn’t see the New Zealand fundamentals as particularly problematic. As I say, records of the past can make one wince.

A week or so later – in one of those events I’ve never needed a diary to recall – Paul Frater and Kel Sanderson, then the leading figures at BERL – pretty vocal critics of our approach to monetary policy – came in to see Grant Spencer and me. Sitting in Grant’s office

“among other topics, they gave us their gloomy assessment of the impact of the share price falls – very pessimistic about comm. property and about the future size of many broking firms and merchant banks”.

They foreshadowed a financial crisis, and a lot of stress on bank balance sheets. We were pretty dismissive of their concerns.

Within a day or two, concerns were mounting even within the Bank, focused on the fate of some of the investment companies (“Judge, Rada and Renouf”) and those they might drag down with them. There was, I recorded, no panic over financial institutions themselves, but we’d had internal discussion of a possible liquidity response, agreeing in principle to raise the target level of settlement cash and perhaps cap the level of the discount rate (which normally moved with market rates) – I think, from context, this hypothetical response was envisaged if interest rates rose (as, say, they did in the 2008 crisis).

A week later we acted. It was never represented as a monetary policy easing – although it was – and so even today there is a mythology abroad (I saw it in a recent Liam Dann article on the crash) that the Reserve Bank did nothing in response. On the day, 90 day bill rates – which hadn’t risen since the crash, despite increase risk concerns and limit cuts – fell 1.5 percentage points on the day. (By August the following year, 90 day bill rates were down to 14 per cent – a similar-sized fall to the active cut in policy rates the Reserve Bank implemented in 2008/09.)

My diary entry that day is sufficiently long, and embarrassingly wrong, that I won’t quote from it at any length: suffice to say that I called it a “precipitate panicky move”. To be sure, the issue in the market at the time wasn’t the interest rate (which hadn’t risen) – it was blind fear and an often-quite-rational newfound reluctance to lend – and we had no evidence that inflation or inflation expectations would fall, and the Bank had over the years been too receptive to pressure from banks. But, such were the genuine fears and rising risk aversion, that the response was only prudent. Immediate responses can always be revisited once the immediate panic passes and, frankly, there wasn’t much, if any, moral hazard risk in the sort of action we took. We weren’t lending more to anyone, let alone to bad credits.

But it wasn’t the way I saw it. A few days later, apparently, I circulated a discussion note “provocatively titled ‘Is it time to lower the cash target’, (ie tighten up again) arguing strongly in the affirmative”. The same day I recorded that Grant Spencer had deleted a description in a draft Board paper of the 6 November easing as “temporary”, observing to me “nice try”. My approach wasn’t totally hawkish – I also toyed with the idea of a cap on our discount rate, in case renewed crisis pressures spilled back into higher interest rates. As the month went on and interest rates fell further, my arguments (in another “longer and more reasoned note”) starting commanding more sympathy among my colleagues, and some hawkish market economists. The Deputy Governor even did the courtesy of ringing to discuss it. But this was one of those times when – at least with hindsight – the more senior were better judges of the situation than those of us further down the food chain. In mid-November, I recorded a conversation with Iain Rennie – then an analyst at Treasury – in which he told me that the distribution of views was much the same at Treasury.

The (apparent) tensions betwen the financial stability and inflation control perspective must have been very real. When my latest note was discussed at (the equivalent of) the Monetary Policy Committee, I recorded that there was plenty of agreement with the analysis and none with the recommendation (to reverse some of the easing) – “terrified of the possibility of collapses corporate and financial” , with rumours rife.

Of course, there were plenty of collapses to come, of corporates and fringe financial institutions. Of the things that were feared, most come true. In fact, reality was worse, because the crisis eventually engulfed mainstream large institutions on both sides of the Tasman. Really bad lending – whether to investment companies, or on a massive commercial propety boom – eventually does that – enabling a really big misallocation of real resources, and then eventually being found out. Most of the waste isn’t in the crisis-aftermath; rather the bad seed is sown – the waste actually happens – when all feels exuberant and the new investment is being recorded as an addition to GDP.

If I look back on my views during that frantic couple of months after the crash began, I was clearly wrong. Even if monetary policy wasn’t going to do anything to save Judge, Renouf, the listed goat companies or whatever – and nor should it – it was quite clearly, even on the facts available at the time, a shock to the system which meant that lower interest rates were warranted. Credit demand and associated activity would be weaker. Interest rate falls would have happened anyway, even without our intervention (that was how the system worked then), but the nudge downwards, and the willingness to accommodate lower interest rates was clearly the right thing to do.

But it is also worth wondering what we might have done if we had correctly understood financial crises, asset busts etc, if we had envisaged several years of little or no growth, and two near-failures of our largest bank. (That we didn’t, even later, is evident in a major article written by Grant Spencer and one his colleagues in late 1988 – published the following year in a book on the liberalisation process, and which I reread last week – in which the crash appears as not much more than a corrective to the excess enthusiasm for consumption up to 1987.) The doves – of whom there were plenty including Spencer and then Assistant Governor Peter Nicholl – would, almost certainly have argued for further easings, allowing interest rates to fall materially further. And yet it is far from clear that that would have been the right approach to have taken.

Inflation edged downwards only relatively slowly over 1989 and 1990, and it wasn’t until the big fiscal consolidation after the 1990 election, and as the 1991 recession unfolded, that we felt comfortable letting bank bill rates fall below the 14 per cent they got to in the months after the crash. We, and other forecasters, misread the 1991 recession, but until that hit us we didn’t appear to be on track to getting inflation to target any sooner than the government had (by then) asked us to. Inflation at the end of 1990 was still 5 per cent, and the target – by then agreed by both main parties – was 0 to 2 per cent inflation. Getting inflation down isn’t technically difficult, but when real people and real institutions (with all their biases, incentives etc) are involved it can, and usually has been, costly and difficult. Sometimes, a little learning can be a dangerous thing. Perhaps a proper appreciation of the looming crisis, and the wasted real resources, at the end of 1988 would have made it even harder, perhaps even eventually more costly, to have secured something like price stability here. I wouldn’t like to be seen as suggesting that we should welcome blind spots, or even ignorance, but sometimes perhaps they end up being less costly than idle theorising might suggest.

Finally, a week or so ago the Herald ran an interesting series of articles on the New Zealand experience in 1987. The thing that most surprised me about those articles – and in a way what prompted the thinking that led to this post – was the almost complete omission of the role of banks in making it all possible. Every over-optimistic borrower needs an over-optimistic lender if the loan is to happen. There were plenty of the former, but all too many of the latter too – whether state-owned lenders like the BNZ or the DFC or private sector ones, new entrants (NZI Bank anyone) or old, New Zealand owned or foreign-owned. And the few institutions, on either side of the Tasman, who didn’t participate boots and all often weren’t particularly virtuous and far-seeing, but just slow. Given another year or two, they’d probably have got into the mix too, and if existing management wouldn’t do so, well other managers could soon be found.

In many ways it was a classic financial crisis – the definitive history of which has still to be written. There was the displacement of genuine new opportunities, enough of a narrative for even the cautious to believe that the future would be quite a bit different and better than the past, official backing (indeed, at times, cheer-leading), extraneous feel-good factors like the America’s Cup, relatively weak market disciplines (especially in the financial sector), little experience in lending or borrowing in such a different world. There were probably even some real success stories (I’m struggling to think of them, but readers can nominate some). And it didn’t, to any material extent, involved lending to households.

It all happened surprisingly quickly. 14 July 1984 was the election day that brought the fourth Labour government to office, and 20 October 1987 began the crash – just over three years. It took far longer to unwind the mess than it did to create it. It is the deterioriation in lending standards that happened so quickly that market monitors, and central banks, really need to be watching out for. When they start sliding, a bank can be destroyed remarkably quickly. Such marked deteriorations in standards aren’t every day events – we, after all, have seen no bank failure since 1990 – and they rarely arise out of the blue. They usually take some shock – some innovation – that is likely to leave regulators just as uncertain what to make of it as the lenders are. That’s inescapable, but is a reason to be cautious about just how much useful difference even the best regulators can make. Seeing no harm for 98 years earns you no real credit (and should not either) if you aren’t much better than the lenders in the other two years each century.

How much money has the taxpayer given to financial institutions (or rescue their lenders) after the 2008 crash? Over a billion I believe. interest.co.nz had a list, but can’t find it that quickly.

Perhaps no bank has been involved, but I’m guessing we have far more lenders than in 1987.

LikeLike

The net amount was under $1bn, and even that arose only because we felt the need to put on guarantees in the midst of the global crisis. Without those developments in Ireland and Australia, we’d have had zero taxpayer exposure. But yes, lots of finance companies failed, but most were very very small, and even South Canterbury was tiny compared to the size/significance of DFC or BNZ in the 80s.

I’d be surprised if we now have more lenders than in 87. And, of course, we have fewer decent-sized banks – just the big four plus the state-owned KiwiBank.

LikeLike

Investors lost $6 billion so the impact to lots of small shareholders was huge.

LikeLike

It certainly hurt individuals, but $6n wasn’t much more than 3% of annual GDP.

LikeLike

Decimated 61 Finance companies with the loss of development finance and an entire building industry which brought on a deep recession. The building industry is still trying to recover to the level of building capability we had prior to 2008.

LikeLike

I’m not sure what we are disagreeing about (if anything). Fairly reckless lending felled those institutions. Fortunately the decline in lending standards at the main banks was nowhere near as severe (and thus, unlike 87, the banks came thru unscathed).

LikeLike

Hard to believe that all 61 Finance companies were reckless and deserved to crash and burn. Certainly the market segment that most of these companies operated in was mainly in offering development finance. Developers work with very small margins and is usually highly indebted due to the boom crash and burn nature of property cycles in NZ. The result is that we do not have large entities that have built up a wealth of equity to ride a crash.

I am more inclined to point the finger at a reckless RBNZ institution that negligently forgets that rapid interest rate rises has a severe and immediate impact on builders and developers that operate on very small margins and high debt.

LikeLike

interesting; so, LTV / DTI one way to insure against those two years of unbridled exuberance? 🙂 perhaps not equitable but does seem an effective way to curb a deterioration in lending standards (also noting a bank will shed liquidity faster than regulatory capital in a crisis….)

LikeLike

Two thoughts in response:

1. Housing is very rarely the key element of a decline in market-led lending standards (the US was as much about govt-led declines), and it isn’t anything like as easy to come up with similar, sensible, rules for say property development lending (the heart of the Irish/nordic losses), and

2. You are assuming that such rules are robust through time. In fact, if housing ever were at the epicentre, it might well involve a period in which both bureucrats and bankers were taking a different view on risk, quite possibly involving removal of such controls. In a way, that is part of what happened in 1984.

On Mon, Oct 23, 2017 at 5:52 PM, croaking cassandra wrote:

>

LikeLike

…re 2, taming the ‘financial cycle’ seems to becoming embedded in central bank mindsets and my guess is macro pru policies look set to become a permanent feature even if the menu of options change with time; but, just a guess and take your point

LikeLike

Time will tell of course, but (a) the 08/09 crisis is still a fairly fresh memory, in a way that it won’t be in 2030, and (b) almost all the interventions seem aimed at the housing market, which typically isn’t the source of the big loan losses. There are higher capital requirements of course, but of themselves they won’t prevent the waste that comes with very bad lending – only, perhaps, limit the frequency of actual bank failures.

And then, of course, there is the US where it isn’t obvious how much has changed at all. A country where the state is still, for example, a dominant player in housing finance.

LikeLike

1987 crash did not seem to have affected me too much and largely forgotten. Probably because I had a cushy job with a salary that was growing at 20% per annum wage increases with a vehicle and a small $100k mortgage when houses cost $130k for a 4 bedroom in Mt Roskill. But at the time I recall thinking that Don Brash was rather aggressive, too much of a grandstanding superstar with interest rate rises with no thought to the implications to the sharemarket and the companies that had grew out of aggressive use of debt.

LikeLike

of course, in fairness to Don Brash, he didn’t become Governor until Sept 88. At times we were slow to allow interest rates to fall, but the first serious interest rate increases Don presided over weren’t until 1994.

LikeLike

One could write about ….

Paul Keating helped bring to Australia a tidal wave of economic modernisation from the mid 1980s: a floated dollar, deregulated banking system, the end of centralized wage-fixing, the privatization of the Commonwealth Bank and Qantas, and the beginnings of Reserve Bank independence.

But let me tell a different story about events that transpired …

As a result of deregulation of the banking system, foreign banks arrived in their droves, setting up their shingle and competing and taking market share off the incumbents, you know who, the usual 4. One of the new arrivals was Bank of New Zealand.

Well, it’s history now but the existing banks did not take the sudden intrusion lying down … they competed hard … very hard … they put on their lipstick, fishnet stockings, hot-pants and 8″ stilletos and prostituted themselves (I use that term intentionally because its what they did) they weren’t going to give up their birthright that easily … and by 1990 they had won … they had driven every single interloper out .. the interlopers all failed miserably … at great cost and great losses … including Westpac Bank which also nearly went down the tubes

Whether the cost of this sortie contributed to the demise of BNZ I dont know

Did any of the influences and turmoil in the Big 4 AU Banks blow across the Tasman? I dont know that either

LikeLike

A big chunk of BNZ’s losses were on its Australian operations. I guess a bigger market, where it was a new entrant, meant lots of opportunities for taking the sorts of risks they needed to take to win business. At least as I see it, the NZ and Aus experiences were very similar, indeed really much the same phenomenon, and many of the same institutions.

LikeLike

I know Michael doesn’t agree with me but I just can’t see how we can avoid the effects of a reduction in private sector credit growth; growth that injected over $30,000 million into our economy last financial year – that’s one dollar in nine of GDP or the wages of 660,000 full time median wage earners. With our trading partners facing similar issues and a certain credit growth reduction coming at a time when household debt, immigration, equities and house prices are at an all time record, seems very dangerous to me. There will certainly be some challenges for our new government and the new RB governor.

LikeLike

on

LikeLike

One thing to bear in mind is that most of that debt just facilitated changes in ownership in the housing stock: for every buyer there was a seller, and thus a compensating credit in someone else’s bank account. Unless there was some exogenous easing of credit standards – and if anything, the effect went the other way, as the RB forced banks to tighten up, and they were pulling in their horns to some extent anyway – the credit growth isn’t much of a boost to econ activity.

All that said, I suspect the next year or so will be quite weak. business confidence is likely to dip (as it did in 2000), there will be less net immigration (partly trends underway anyway and partly whatever modest changes the new govt brings in), there will be quite a bit of business uncertainty (restraining investment) around the carbon/methane and water situation, and the housing market will also be weakened by eg the extension of the brightline test and the new Andrew Little bill on rental standards, all reinforced at the margin by whatever they do about foreign buyers (and the continuing Chinese clampdown on capital outflows),

In a post earlier last week, before the govt was known, I concluded that the next OCR move could as easily be a cut as an increase. That seems more probable now, even allowing for some additional fiscal pressures (beyond what was in Labour’s numbers or in the PREFU).

LikeLike

If the NZD continues to weaken as international investors take fright as it becomes clearer that some of these coalition deals will cause some massive budget blowouts eg, planting 100 million trees a year equates easily to $2 billion a year in tree planting say $20 a tree. then that will inevitably flow on to upward pressure on inflation with the consequence of higher upward pressure on interest rates.

LikeLike

When you have agreed $1 billion to NZF for regional development and the cost to plant trees a year is $2 billion then you either have no budget for any regional development other than tree planting or you already have a $2 billion cost blowout. I wonder if Shane Jones gets any new underwear out of the deals with Labour?

LikeLike