In his Sunday Star-Times column this week, economist Shamubeel Eaqub announced that “I’ve bought a house at last” . He and his wife had had quite a lot of coverage for their choice to stay renting, even though they could readily have purchased a house in Auckland. As they noted in their book Generation Rent, their decision to rent had been both a lifestyle and a financial one.

Economists have form in this area. Most people want to own their own house sooner or later, and in the longer-term those who don’t are usually those who can’t. When economists don’t buy it is usually a choice.

The most prominent New Zealand economist who once chose not to buy was the then new Governor of the Reserve Bank, Don Brash. Taking up his role as Governor in 1988 involved shifting from Auckland to Wellington. At the time, after the break-up of his first marriage, Brash was on his own. But he was also struck by just how high interest rates in New Zealand were. To buy a house would involve paying mortgage interest rates that implicitly assumed inflation would not come down further, even though the mission Brash had been given was to keep on reducing inflation. Renting looked a lot cheaper than buying, at least if inflation was going to be successfully reduced. Brash pointed this out in the media and, even if there was a certain logic to his point, cartoonists had fun. This was Tom Scott’s contribution.

Not that long afterwards, Don remarried and they then had a child. Like the Eaqubs, whatever the cold financial analysis might have shown, he bought a house.

Not that long afterwards, Don remarried and they then had a child. Like the Eaqubs, whatever the cold financial analysis might have shown, he bought a house.

I went through a similar phase. In those far-flung days, Reserve Bank staff could get mortgages at 4.5 per cent. I got a secondment to Papua New Guinea in 1985, and my father urged me to buy a house before I went. I did the numbers and calmly talked him through the analysis demonstrating that if the inflation rate was going to be cut as the government and the Reserve Bank were suggesting then it wouldn’t be worthwhile to buy, even at 4.5 per cent (according to the RB website, private borrowers at the time were paying 17.5 per cent for a new first mortgage). More fool me. In the following few years one of New Zealand’s biggest credit booms ever happened, and with it a whole new last wave of high inflation.

There is nothing wrong with renting. For anyone living in a city or town only temporarily, or newly arrived and not sure where they want to be long-term, it is usually the more sensible option. Transactions costs, and the uncertainty, associated with buying and selling houses are quite a deterrent to doing it very often at all. And there is the added advantage that maintenance etc is someone else’s problem. For most people just starting out in the workforce, there aren’t serious alternatives even in well-functioning markets (ie without land use restrictions, or LVR controls).

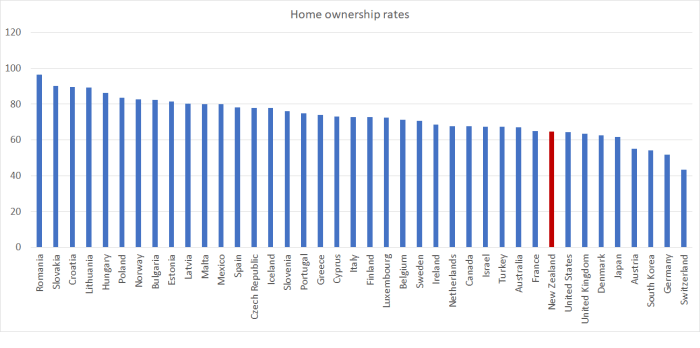

But for most people in most places renting is a phase they want to get past. Often, just as quickly as possible. This chart shows home ownership rates for a bunch of OECD and EU countries.

The median for these countries is 72.8 per cent. New Zealand was under 65 per cent at the last census, and probably falling further.

I’m not sure that home ownership is one of those things we want governments actively encouraging – that way lies, for example, the sorts of credit misallocations that, in the US, contributed to the financial crisis of 2008/09. But, equally, we don’t want governments standing in the way of people fulfilling a natural human aspiration for a place of their own (as governments do now, through some toxic mix of land use restrictions, together with policy-driven rapid population growth and credit controls). Economists sometimes fret about people having “all their eggs in one basket” – their biggest asset in the same location as their job etc – but revealed preference internationally suggests that economists have it wrong. People typically weigh the advantages of home ownership as outweighing any of the risks/costs that economists sometimes focus on.

It is sometimes claimed that the tax system materially favours owner-occupation, but it doesn’t really. The tax system (arguably) favours those with a large amount of equity in their homes, but it bears down on most people buying a first home. To be sure, they aren’t taxed on the imputed rental value of living in their own house. But, unlike rental property owners, these (typically highly-indebted) owner-occupiers can’t deduct interest or other home ownership expenses. Few/no first home buyers would be paying any more tax – many would be paying less – even if the tax treatment of housing was put on what most economists would regard as a more neutral footing.

To my mind, the main policy priority should be fixing up the land supply issues (probably supported by reduced immigration and eased credit controls). Do that – all quite readily technically feasible, whatever the political failures of nerve – and for most people renting will become a short-term proposition again. Sure, there will always be a handful of people unable to buy, or to cope with having their own house, and in many cases state housing (or state-financed housing) is likely to be the solution. But there shouldn’t be any reason why ordinary working people couldn’t buy their own house in their 20s, as used to happen. After all, they’ll have another 40 years plus of working life to pay off a mortgage – and it is quite rational for low income people to spread such a bulky purchase over a long working life.

So calls for various reforms of tenancy laws to facilitate longer-term renting seem mostly like a concession of failure – a refusal by successive governments to sort out the housing supply market itself. Shamubeel Eaqub and others sometimes talk up Germany and, to a lesser extent, Switzerland. I see nothing appealing about the Swiss housing market – hugely highly-priced (and accompanied by very high levels of – probably tax-induced – household debt), and with outcomes badly out-of-step with most other advanced countries. Sure, one could make rental tenure more secure, but is there any evidence that most ordinary citizens would prefer that over owning a place of their own?

I’m not that familiar with the details of tenancy law, but it isn’t clear to me that there is any legal obstacle to long-term fixed tenancies, mutually agreed between owner and renter. Perhaps if there is an issue it relates to the ownership patterns of the New Zealand rental stock.

One good feature of the New Zealand tax system is that it has treated individuals owning rental properties very similarly to institutional investors owning rental properties (although that has been changing over the last decade or so). That isn’t the case in lots of other countries where, for example, rental properties owned by a tax-preferred retirement savings entity will be much more favourably treated than properties owned by an individual holder. Perhaps partly as a result, most private rental properties in New Zealand have been owned by people with quite modest portfolios of properties. That probably works fine for renters much of the time when most renters have quite short-term horizons. If they have a longer horizon, it can become more problematic if the owner wants to rebalance or liquidate their modest portfolio of properties. Those problems are much less likely for an institutional owner who, in principle, might have 1000 properties, and sees themselves in the rental business for the long-term.

Even so, I have wondered why we don’t see more institutional owners of rental properties. At times, I’ve wondered whether it had to do with the nature of our housing stock – mostly detached houses. Perhaps institutional ownership was easier and more natural with, say, whole apartment blocks, or some of those squares in London all owned (but rented with long leases) by a single estate. A big portfolio of detached houses might be harder to manage, maintain etc.

And so I was interested to see a lengthy article in the Wall St Journal the other day on private companies doing exactly that in the US on a large scale.

Those four companies and others like them have become big landlords in other Nashville suburbs, and in neighborhoods outside Atlanta, Phoenix and a couple dozen other metropolitan areas. All told, big investors have spent some $40 billion buying about 200,000 houses, renovating them and building rental-management businesses, estimates real-estate research firm Green Street Advisors LLC.

It is a fascinating article (google, “Meet your new landlord: Wall Street”). It isn’t clear whether it will prove to be a viable model in the long-term, or whether it is largely a post-crisis phenomenon that might fade away again in a few years. But if people are serious about a better-functioning long-term rental market in New Zealand – if people are giving up, as they shouldn’t, on fixing the housing supply market, enabling a recovery in the home ownership rate – it is the sort of business model they should be hoping to see develop in New Zealand.

In closing, I wanted to pick up just one specific point from Shamubeel Eaqub’s article. Talking about the rent vs own choice he notes

we don’t hate home ownership at all. We just didn’t think it was the best use of our hard-earned money to spend it meeting ownership costs (such as house maintenance) that are much higher than rents, nor to deprive us of the opportunity to invest in businesses that will hopefully give us good financial returns and create jobs and prosperity for other New Zealanders.

Sadly, now that our money is tied up in one huge asset, it gives us shelter and security, but it no longer has the opportunity to be directly invested in New Zealand businesses to get them started, or to help them grow.

At an individual level, no doubt the logic seems fine. The Eaqubs did have shares in businesses (or units in unit trusts which had shares in businesses) and now they own a house. But their purchase of a house last week didn’t change, even slightly, the total number of houses in New Zealand, the number of people living in houses, or the number of companies with shares on issue. All that happened was that ownership changed: the Eaqubs purchased a house and someone else sold one. The Eaqubs sold shares and others purchased them. Renting rather than owning doesn’t change, by one iota, the volume of real resources in the economy devoted to housing.

I’m not sure there is anything particularly virtuous in preferring a smaller simpler house over a larger better-appointed house, but it would only be if people were consistently choosing smaller simpler accommodation – rather than just changing who owns those houses – and were saving rather than spending the leftover money, that additional real resources might be available to the business sector. Since the typical concern is that we have too few houses for the number of people in New Zealand, and some often highlight that many of our houses aren’t of great quality (cold, drafty etc), it seems curious for someone who is on record as generally favouring our immigration programme to suggest that fewer resources in New Zealand should be devoted to housing.

Michael is your home ownership graph -the % of houses which are owner-occupied or the % of people who live in a owner-occupied house?

LikeLike

I’m not sure, altho i suspect mostly the former. I took the data from here https://en.wikipedia.org/wiki/List_of_countries_by_home_ownership_rate where most of the entries seem to have reasonably authoritative reference sources, but i didn’t dig into them.

You may note that on the Wikipedia table Singapore shows as a very high number – that is wrong. https://likedatosocanmeh.wordpress.com/2017/05/13/why-singapore-has-the-lowest-home-ownership-rate-in-the-world/

LikeLike

Adam Posen wrote an excellent editorial in the FT a few years back on the dangers of the cult of home ownership in Western Economies: https://www.ft.com/content/00bf5968-f518-11e2-b4f8-00144feabdc0

It was focused more on dissuading Governments from proactively encouraging home ownership (ie providing subsidies and incentives like, oh, tax free capital gains?) but has some great overall insights. I like the fact it questions why some countries seem hell bent on encouraging people to leverage the bulk of their savings and net worth into a highly illiquid, highly volatile, price-opaque asset (with high transaction costs), where that asset faces serious physical risk exposure and should only be expected to generate pretty mediocre returns over the long term (absent political interference in supply and subsidies).

That said, I do own a house…

LikeLike

Thanks. Interesting piece by Posen. I largely agree with staying clear of measures designed to actively drive-up home ownership (it is the measures working in the other direction that have been the greater problem here).

But it was a little overwrought: in well-functioning housing supply markets, houses aren’t that expensive and don’t provide windfall wealth to the favoured of the next generation. As for physical risks – fire, flood etc – they are mostly diversifiable thru insurance. And there is a vital word missing from much of the discussion: hedged. My natural position is a lifelong demand for accommodation services. In owning a house, I’ve met that need, and thus am square. I don’t care whether my house price halves or doubles (well, at least not from my own position). There are labour mobility issues for some, but few people want to move at the drop of a hat.

LikeLike

..interesting article – classic quote: “The rental stigma has really subsided,” says Michael Cook, operations chief at closely held Streetlane Homes, which owns about 4,000 houses. “People are realizing that houses are not necessarily the best places to store wealth.”. Presumably Mr Cook repeats the latter comment to his investor base?

LikeLike

Re your comment on the RTA and long term tenure. You are right most of the 42 day notices given due to sale are due to small scale owners selling. However in my experience there would be perhaps 20 to 30 times more tenants moving by their own choice. Many Landlords would love to offer long tenure and hold onto their tenants. The RTA forbids longer than 5 years and the courts rarely strictly enforce fixed term contracts.

LikeLike