We expect inflation to strengthen reflecting the accommodative stance of monetary policy, increases in fuel and other commodity prices, an expected depreciation in the New Zealand dollar and some increase in capacity pressures.

So said Graeme Wheeler in his MPS press release this morning. I thought it sounded like a familiar line, so I went back and had a look. This seems to have been the Governor’s 30th OCR decision. Back in his very first OCR announcement in October 2012 he said this

While annual CPI inflation has fallen to 0.8 percent, the Bank continues to expect inflation to head back towards the middle of the target range.

And in all those 29 statements since then – with perhaps just one exception – he has been saying much the same thing: inflation will increase. And actual inflation – headline, and the range of core measures – just keeps on being below target.

At the Bank’s press conference, Bernard Hickey asked if the Bank could be regarded as having done its job, given that even on its own forecasts (persistently too optimistic) there would have been six years of inflation below the target midpoint by the end of 2017, when the Bank again expects headline inflation to be back to 2 per cent (the Bank doesn’t publish forecasts of the core inflation measures, but I doubt the picture would be any different if they did – it has also been four or five years since the various core measures were clustered around 2 per cent). There were a range of possible plausible answers to that question, but I wasn’t prepared for the one Assistant Governor John McDermott actually gave: he said “your timeframe is very short”. Six years……when monetary policy generally works over perhaps a two year horizon, and when the Governor’s term – in a system built on personal accountability – is only five years.

Yes, it wasn’t a very good day at the Reserve Bank today. Inflation is apparently expected to increase partly because the exchange rate is expected to fall. At 8:59am, the exchange rate was already above what the Bank was assuming in the MPS projections, and a few minutes later it was another per cent higher, and it rose a bit more in the course of the press conference. I’m not sure why the Governor expects the exchange rate to fall back if his rosy domestic economic story is correct. Perhaps he expects a lot more tightening in the US. But, again, he has been expecting that almost since he took office in 2012.

Some of the other bits in that statement as to why he expects inflation to rise were a bit puzzling too. The Governor apparently thinks “accommodative monetary policy” will do the trick, but in real terms the OCR is probably a bit higher than it has been for much of his term (certainly than in the year or so before the unwarranted tightenings), and the TWI this afternoon is only slightly lower than the average level for the Governor’s term to date. Set aside for now the question of whether conditions are actually “stimulatory” or “accommodative” in absolute terms, but if they are more accommodative now than over the last four years, the difference isn’t large. Core inflation didn’t pick up over those four years, and it isn’t obvious why it is going to do so now.

The Governor also apparently expects “some increase in capacity pressures”. One would hope so, given that on the Bank’s own estimates we have had eight consecutive years of a negative output gap. But it isn’t clear why the Bank expects capacity pressures to increase from here. They are forecasting quite an increase in residential building, but we’ve already had four or five years of increasing residential investment activity, through two very large shocks to demand for residential investment – the Canterbury earthquakes, and the large unexpected surge in immigration. All of that, on top of buoyant commodity prices earlier in the period, wasn’t enough to turn the output gap positive or get the unemployment rate back to more normal levels, or lift inflation back to target. It isn’t obvious why things should change now – especially as, like other forecasters, the Bank expects the net migration inflow to fall away quite sharply.

The Governor could be right. Macroeconomic forecasting is, in many ways, a mug’s game. But he has been wrong for several years now, as his predecessor was in his last couple of years. It isn’t obvious that he has a compelling story to tell as to why inflation pressures are finally about to pick up. But if he has such a story it isn’t in the Monetary Policy Statement.

Meanwhile, there is a great deal of complacency. I heard the Governor talk of significant real wage increases, strong tourism, strong immigration, significant building activity, and so on. All without any sense that per capita income growth has remained disappointingly weak. Neither the Governor in his comments nor the text of the MPS itself even mention an unemployment rate that lingers at 5.7 per cent, years after the end of the recession. If anything, the Bank appears to believe that excess capacity in the labour market is already exhausted (see Figure 4.8).

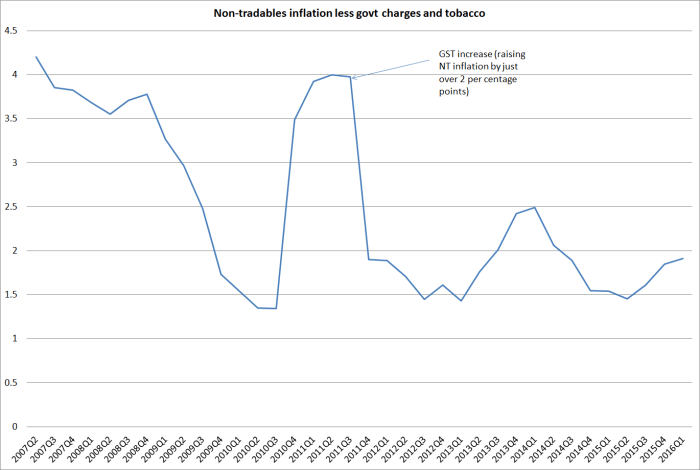

The Governor also made great play of non-tradables inflation. He is quite right that, over time, non-tradables inflation (or at least the core of it, excluding government taxes and charges) is what monetary policy can really influence. Even exchange rate effects – which the Governor weirdly tried to play down – over the medium-term work by influencing overall pressure on domestic resources and thus non-tradables inflation. But non-tradables inflation typically runs quite a bit higher than tradables inflation, even in a stable exchange rate environment. That is partly about the labour intensive nature of many of the services included in non-tradables inflation (hair cuts are the classic example, where there is limited scope for productivity gains). With an inflation target centred on 2 per cent, the common view among economists inside the Bank used to be that one might expect non-tradables inflation to average perhaps a bit above 2.5 per cent, while tradables inflation might average a bit below 1.5 per cent per annum. Together, they would be consistent with medium-term CPI inflation (ex taxes etc) of around 2 per cent.

But here is what non-tradables inflation looks like in recent years. This series excludes government charges (eg the cut in ACC motor vehicles levies) and tobacco taxes (which have been increasing sharply each year). It doesn’t take out the effect of the 2010 GST effect, but it is easy enough to visually correct for that – it accounts for about 2 percentage points of the inflation rate over 2010/11.

There is a bit of variability in the series, but it has been years since this measure of core non-tradables inflation got even briefly as high as 2.5 per cent, let alone fluctuating at or above that level. And this is the series that should have borne the brunt of the Christchurch rebuild pressures – which probably explained the increase in this measure of inflation in 2013/14. Non-tradables inflation is what the Bank can influence. It really needs to be quite a bit higher to be consistent with the target specified in the PTA – and on current Bank policy, there is no particular reason to think it is going to happen.

I outlined again yesterday my take on how the Governor operates: he is really bothered about the housing market, and really doesn’t want to cut the OCR. But he can’t afford to see core inflation drift much lower – he can get away with it holding around current levels (somewhere, in the MPS words, in a 0.9 to 1.6 per cent range) – so will cut if data surprises really force him to, but not otherwise. Today was a classic example of that model in action. In the run-up to the March MPS it was, he said, the expectations survey data that really rattled him. There has been nothing comparable since and so, mediocre economic performance and weak inflation notwithstanding, there was no OCR adjustment.

Instead, today was all about housing, and financial stability. Perhaps we were supposed to have forgotten that the FSR was released only a few weeks ago and in his press release on that occasion the Governor began by extolling the resilience of the New Zealand financial system. Often enough the Governor has been reluctant to comment on financial stability issues in monetary policy press conferences, and it is only three months since I praised him for his response on house prices at the March MPS press conference

And when asked about the impact of a lower OCR on house prices, he succinctly observed “well, that’s just something we’ll have to watch”. By conscious choice, house prices are not part of the inflation target, either in New Zealand or in most (if not all) inflation targeting countries. It is one, important, relative price, influenced heavily by a range of other policy considerations. And if bank supervisors should pay a lot of attention to house prices, and associated credit risks, it is a different matter for monetary policymakers.

All that was long gone today. It was, in effect, all about house prices and the possible threat to financial stability. I don’t recall hearing, or reading, anything about stress tests (they’ve been pretty positive), or capital requirements (they seem to have been quite – rightly – onerous by international standards), or even about the Bank’s benchmarking exercise to better understand how individual banks are modelling similar risks. High house prices can be a source of risk if they are financed with poor quality lending, backed with inadequate capital. But there was none of that analysis today. Instead, there was a regulator champing at the bit to impose even more controls, touting the LVR restrictions to date as “very successful”. Apparently more LVR controls could be only weeks away – although of course they will have to consult on any new controls, with a mind open to considering alternative perspectives and evidence – while loan to income restrictions seem to be a bit further down the track (they are doing analytical work on them, rather than detailed instrument design, or so it seemed from the Governor’s comments). The Governor really seems to have it in for people buying residential properties for rental purposes, and yet can never quite tell us why. He reminded us again today that some 40 per cent of property turnover involves such purchasers, but never ever addresses the simple point that in a badly-distorted system where the home ownership rate is dropping towards 60 per cent, the remaining homes have to be owned by someone.

The Governor and Assistant Governor were at great pains to emphasise that monetary policy is required to have regard to “financial stability”. The relevant phrase isn’t new – it has been in the Act since 1989 – but it isn’t quite what the Governor said it is either. Section 10 of the Act requires that

“In formulating and implementing monetary policy the Bank shall have regard to the efficiency and soundness of the financial system”.

Efficiency is listed first, both there and in the Policy Targets Agreement. And yet, puzzlingly, I didn’t hear anything today – or in the FSR press conference a few weeks ago – about the efficiency of the financial system. New controls, ever more detailed controls, overlapping LVR and DTI controls, all imposed on some classes of lenders and not on others, some classes of borrowers and not others, are usually considered ways of seriously undermining the efficiency of the financial system. But the Governor seems not to care.

Perhaps more importantly, in a discussion about monetary policy, neither financial soundness nor financial system efficiency – nor the avoidance of “unnecessary instability in output, interest rates and the exchange rate” – are equal objectives with the inflation target. Price stability is the Bank’s primary statutory objective, and the inflation target centred on 2 per cent in the practical expression of that. It doesn’t mean headline CPI inflation is, or should be, bang on 2 per cent each and every quarter. But six years – with no assurance that even six years will be an end of it – below target really is too much. It was, after all, the Governor who added explicit mention of the midpoint to the PTA.

The Governor also found himself on the backfoot over communications, coming on the back of the recent BNZ analysis and yesterday’s Dominion-Post article. In some obviously-prepared lines, the Governor went to great lengths to argue that there was simply no problem. For a start, he and his colleagues agreed, people simply hadn’t read his February speech carefully enough (set aside for a moment that point that if people misread your carefully prepared communication, it probably says something about that communication itself). Oh, and we shouldn’t be surprised that there had been quite a few surprises in monetary policy lately, because the OCR was actually changing. He seemed to ignore the fact that, as I noted yesterday, in 2014 the OCR had moved quite a lot and there were no major communications problems. It got worse when he then argued that if one looked at 2006 to 2010 there were similar surprises – as if he thought we’d forget that 2008/09 saw one of the biggest global financial crises ever, and huge – unprecedented – OCR changes. It simply wasn’t a very convincing performance. The Governor’s communications haven’t been good enough recently.

A journalist asked him about the sharp reduction in the number of on-the-record speeches. I hadn’t really noticed this, but when I checked it was certainly true. In his early years, the Governor made much of how the Bank was going to do more on-the-record speeches. In 2013 there were 17 and in 2014 there were 18. Last year there were only eight – a fairly normal sort of level in pre-Wheeler years – and this year so far there have been only four, only one of which was given by the Governor himself. The Governor could offer no particular reason for this, but then fell back on a rather petulant anecdote, citing one business journalist who the Bank had asked for comment on the Governor’s speeches. This journalist had apparently described them as “too complicated and with too many ideas”. The Governor’s plaintive response was “I hope they get read”. It was a slightly sad performance. Unfortunately, it is true that neither the Governor’s speeches nor those of his colleagues really match the standards of those of their peers at the RBA, the Bank of England, the Bank of Canada, or the Fed. We should expect better – considered reflections, expressed clearly. Part of accountability often involves such speeches, especially when – as with this Governor – he is apparently so reluctant to give interviews. Embattled, the Governor appears to have withdrawn to his fortress.

Oddly, John McDermott offered the thought that while the number of speeches had dropped, there had been a “massive increase” in the number of other publications: “we don’t just communicate through speeches”. I was a bit taken aback by this claim and went to the website to check. There does seem to have been a small increase in the number of Analytical Notes (author’s own research, including the standard disclaimer that it doesn’t speak for the Bank) and Bulletin articles (although there the increase seems to relate mostly to financial markets and the regulatory functions). But there has been a big increase – perhaps “massive” is not too strong a word – in the number of Discussion Papers. This year, so far (five months in), there have been eight published, compared to a typical annual total of six each year in recent years. But…again, Discussion Papers are authors’ own research, complete with the standard disclaimer. In most cases, DPs are intended as the basis for submissions to academic journals by the Bank’s research staff. Sometimes they have interesting material, but often – abstract and introduction aside – they are fairly incomprehensible to someone who is not a specialist in the particular area. They don’t attract much attention outside academe, and have never – to my knowledge – been used as part of official policy communications. If senior policymaker speeches have a role, publications like DPs aren’t a substitute for them.

All in all, neither the MPS itself nor the press conference were the Reserve Bank anywhere near its best. They will probably get away with it because the domestic banks seem mostly unbothered about the persistent undershoot of the inflation target. But they really shouldn’t. The Board, the Minister and Treasury should be asking hard questions – both about the substance of policy and its presentation.

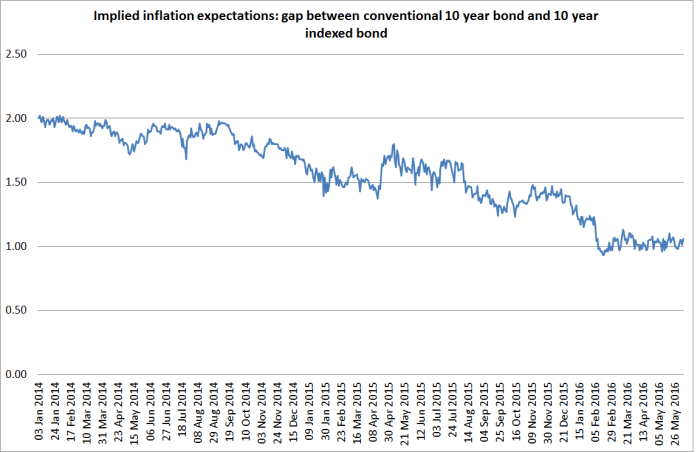

Finally, the Reserve Bank’s “modelling” of long-term inflation expectations got elevated as far as the press release today. We are assured that these expectations are “well-anchored at 2 per cent” (not even “around” or “near” but “at”). For these purposes, the Bank uses a couple of surveys of a handful of economists. It isn’t clear what useful information the results have for current policy, since respondents will reasonably assume that some other Governor, and some other chief economist, will be setting monetary policy before too long. But it also gives no weight at all to the market-based measure of implicit inflation expectations we do have.

125 points of OCR cuts has still not been enough to convince people actually buying and selling government bonds to raise their implied 10 year expectations above 1 per cent.

People just don’t believe – whether on this measure or in the other surveys – that inflation is going to settle back at 2 per cent any time soon. They’ve been right to be skeptical. That should trouble the Bank, and those paid to monitor it. Expectations surveys aren’t an independent influence on inflation – often they are a reflection of past actual outcomes – but the way the Governor was talking today it sounded as though it might take another inflation expectations shock, or perhaps a GDP surprise, to bring about another cut. The next expectations survey data won’t be available until after the next MPS.

In the current governor’s term they have consistently spotted inflation on the distant horizon- like the economists who forecast 18 of the last 2 recessions etc. Sadly, in their case it has consequences for the real world. It is their inability to recognise the consistent bias to their forecasting errors which is most surprising. I guess if 6 years on the trot is too short a time frame to fairly judge the quality of forecasting or efficacy of monetary policy it lets the RBNZ board off the hook in assessing the Governor’s performance.

On a technical note is monetary policy fairly measured as accomodative when it is clearly tighter than the rest of the developed world? I can understand their dilemma but about November last year I seem to recall the Governor commenting on the difficulty of running independent monetary policy in the current environment- i.e. it all becomes relative if capital can flow freely across borders. Makes one wonder why they are so confident in their views on the likely or fair value path for the currency.

LikeLike

The last recession was completely predictable. Allan Bollard just kept pushing interest rates to break 10% which drove NZ into a recession, decimated the building industry and 61 plus finance companies.

LikeLike

On your second para, in principle it should depend on where each country’s neutral interest rate is. Since our actual rates have been higher than those of the rest of the advanced world for 25 years – and for most of that time inflation was if anything a little high – I’m quite comfortable with the idea that our neutral rates (relevant for domestic inflation pressures) is higher than those in the rest of the advanced world (even Aus, altho the margin there is probably smaller).

Who knows what the absolute level of neutral rates is, either here or abroad, But the slowdown in population growth and productivity growth gives us good grounds for thinking real neutral rates are materially lower than they were, and falling inflation expectations have furthered lowered the nominal neutral rate..

LikeLike

Re the BNZ analysis on policy surprises, clearly the Governor doesn’t read his own economists’ research reports. I refer to DP2008/1 which analysed the OIS market between 2002-2007 and showed an absolute mean error of circa 5bps for the surprise factor, in line with the BNZ analysis pre the communication mis-firing.

Also, splitting hairs a bit, I think you’ll find an interpolated 2025 nominal bond matched with the inflation-indexed bond currently shows implied inflation expectations at circa 0.9%, which is even lower than your 1% estimate.

LikeLike

Thanks – yes you are quite right about the less than 1%. It was bad enough with the crude version, I couldn’t be bothered doing anything slightly more complex.

LikeLike