The annual national accounts data were released a few weeks ago by Statistics New Zealand. They got little media attention, which isn’t surprising, but I like fossicking in the spreadsheets. Apart from anything else, they provide an annual update on some of the longest official time series data we have. Australia has full national accounts data back to 1959, and the United States provides official data back to 1929, all on current methodologies. By contrast, we have real quarterly data only back to 1987, and annual nominal national accounts data back to 1972.

The (flow) national savings rate has had a lot of focus in the New Zealand debate over the years. Indeed, early in the term of the current government, there was even an official Savings Working Group. A lot of discussion focuses on household savings, but I prefer to focus on national savings (ie the savings of New Zealanders, New Zealand-owned companies, and the New Zealand government). It provides a good basis for international comparisons, and isn’t messed up by the somewhat-artificial boundaries between households, corporates, and governments.

I also prefer to use net savings data rather than gross savings (the difference is the estimate of depreciation, or “consumption of fixed capital”). Net savings is the real resources added to wealth. And if I’m using net savings data I need to use net national income data.

As I highlighted a few weeks ago, our national savings rate has been relatively low by the standards of the typical OECD country. And it is really quite low when compared with the net national savings rate in Australia – but it has been for decades, including the period well before Australia introduced compulsory private superannuation savings. On the other hand, our net savings rate has been strikingly similar to median of the other Anglo countries.

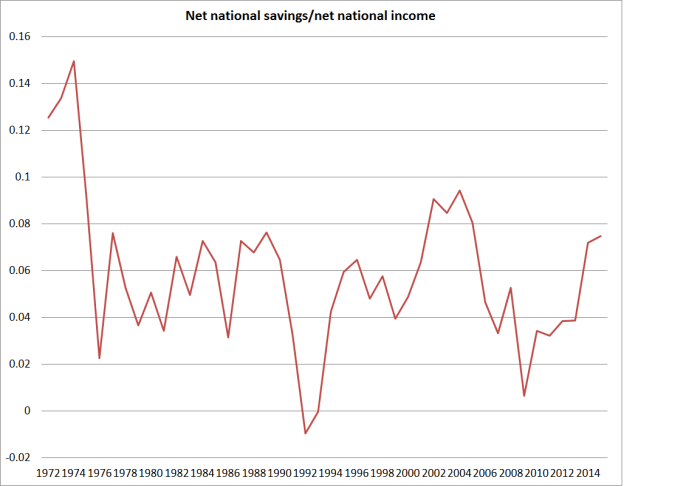

This is what the chart looks like, starting in the year to March 1972, and end in the year to March 2015.

Of course, the sharp fall in the series at the start of the period really catches the eye. But the other thing that strikes me is just how stable average the savings rate has been over the subsequent 40 years, fluctuating around 5 per cent. As you’d expect, it falls quite sharply in recession (see 1991 and 2008/09) – corporate profits tend to fall in recessions, and fiscal deficits widen – but since 1975 there has been no trend in the series at all [1] .

Which creates difficulties for those looking for explanations for our relatively modest national savings rate:

• Some reckon tax incentives might help. But actually we had a very generous tax treatment of superannuation and life insurance until the late 1980s, and a rather ungenerous one (defenders would say “neutral”) since. But the difference isn’t visible in the aggregate data.

• Some reckon a liberal approach to New Zealand Superannuation might explain something. But in the years to March 1975 and 1976 we had a compulsory private scheme, then we had very liberal universal NZS at 60, then we had means-testing and a fairly rapid increase in the age of eligibility. None of it is very evident in the data.

• Some talk about “wealth effects” from rising house prices dampening savings. But the biggest house price bust in modern New Zealand history was after 1974, and the biggest boom was over 2003 to 2007. None of it is very evident in the data.

• The (non-superannuation) welfare state has got bigger over the period, while tertiary education went from being largely “free” for a small group of people, to really rather expensive for a huge number of people. None of it is very evident in the data.

• Some reckon financial liberalisation will have dampened savings, enabling people to bring forward consumption in ways they couldn’t previously. The real freeing-up of the system didn’t start until the mid 1980s. But the difference isn’t obvious in the aggregate data.

• Kiwisaver hasn’t been compulsory, but the take up was sufficiently large that if advocates had been told in advance that it would be that high most would have thought it would have boosted national savings rates. But neither in the more formal research nor in a simple chart like this is it particularly evident.

I’m not suggesting none of these factors made any difference. I’m sure in many cases they did, and (for example) the increase in the NZS eligibility age helped put the government in the position of running large surpluses in the years leading up to the 2008 recession (which was also the peak in the national savings rate). But it isn’t easy to point to a single factor, or even an identifiable set of factors, to explain New Zealanders’ savings choices. An alternative way of saying that is that it is not easy to point to what one might change if one were convinced (which I’m not) that the national savings rate is a policy problem. 40 years of a constant mean is really quite a long time. More-formal modelling might shed some light, but I wouldn’t be optimistic.

Discussions of savings often focus on households, and then secondarily on the government’s own finances. But they tend to ignore the role of business savings. I’ve wondered whether the modest rate of national savings partly reflects the perceived lack of profitable opportunities in New Zealand. As I’ve pointed out before, business investment as a share of GDP has been quite low in New Zealand for decades, and less than one might expect in a country with quite a fast-growing population (Austria or Belgium need to devote a smaller share of their income each year to adding new shops and offices etc than, say, New Zealand or Australia do). Firms might save more if the growth prospects were better – if, say, real interest rates were nearer those in the rest of the world, and if the real exchange rate had been lower. But in that case, savings rate wouldn’t be the cause of any problems, but just another symptom.

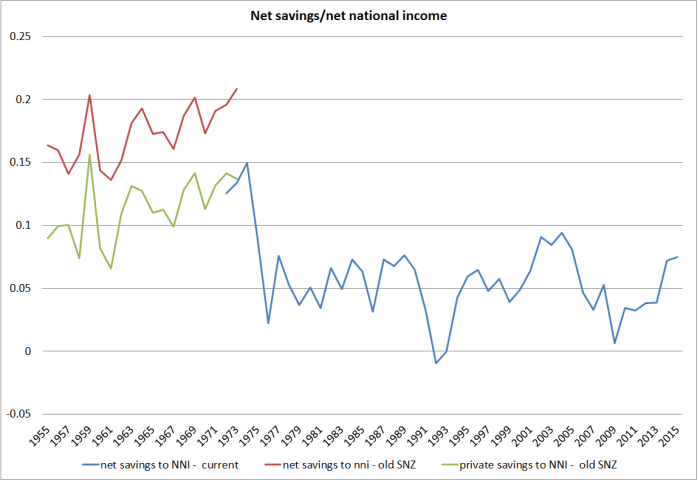

It is one of those areas where better data might help shed a little further light. What was going on with that fall in the national savings rate in 1974/75? It looks a lot like the impact of the collapse in the terms of trade. But the savings rate has never recovered, and we don’t even know if it was exceptionally high in the early 1970s. Contemporary estimates suggest that business savings were almost half of private savings – from perhaps a third a decade earlier. Unfortunately, the earlier estimates aren’t compiled on the same basis as the modern national accounts. For what it is worth, here is a chart for the full period since 1954/55, using data published in the New Zealand Official Yearbooks (in this case the 1975 one). There is a hint of national savings rates rising in the late 1960s and early 1970s, but it is hard to know, and hard to know whether the average savings rate for the last 40 years is really lower than it was in the earlier post-war decades.

Surely we should be funding Statistics New Zealand – or at a pinch some good academic researcher – to produce longer backdated series of our national accounts. Better data on its own probably wouldn’t answer all our questions about New Zealand’s longer-term economic performance, but it surely couldn’t hurt. Would it provide value to the plumber from Masterton? Hard to tell, but good data at least opens the possibility of better policy.

NB: Before anyone comments, this post is dealing entirely with the flow rates of savings from current income. It is not dealing, at all, with stock measures of wealth, or how they might aggregate to some sort of national balance sheet.

[1] In the years of high inflation and high public debt, the story is a little complicated because much of what is recorded as interest is in effect a principal repayment. Grant Scobie (and co-authors) looked at that effect here.

Surely savings is the stock (saving being the flow)

LikeLike

yes, fair technical point. I’ve never found it a particularly helpful one tho, so tend not to use it.

LikeLike

Maybe part of the answer is that group behaviour changes only slowly in response to economic incentives. This fits with our understanding that even business managers have little idea about current inflation data for example. We know that in 1974 there was a massive fall in the terms of trade and in 1984 we transitioned to a floating exchange rate and the high real exchange rate regime that has prevailed since then. So perhaps the real exchange rate was also too high from 1974-84, not all the time, but enough of the time to prevent business transitioning back to a higher-saving mentality.

Regarding household savings, no doubt it’s very complicated, but I do think the policies of the Third Labour Government acted as a kind of gateway transition to a period of economic and cultural decline in the 1970s and 1980s. Many anti-savings changes were made and the the one notable pro-savings change made, compulsory super, was soon repealed. Much of the increased regulation and made-up jobs would have moved the supply curve to the left, increasing prices and making it harder to save.

LikeLike

Was the Third Labour Govt really that bad on the regulatory side? My impression was of poor macro management, faced with some very large shocks (and questionable official advice – eg to borrow through the TOT decline), but of largely carrying forward the regulatory state they inherited. Did you have specific new distortions in mind?

LikeLike

I was very young at the time, but WIkipedia states “The government tried to avoid inflation via massive overseas borrowing and a variety of local regulations. A scheme was introduced to fix maximum retail prices, while to keep people in employment it added the post office, the railways, milk, lamb, mutton, and wool to the number of industrial subsidies.Office, rail, and bulk power charges were controlled.” The whole article is interesting, and paints a picture of an incredibly activist government the likes of which we can scarcely imagine today.

LikeLike

I was (I suspect) only slightly less young. I noted the sources for those 2 comments in the Wikipedia articles aren’t exactly authoritative. The MRP scheme was, from memory, never implemented, and if it was was very quickly reversed by Muldoon. There was a lot of borrowing – on official advice that the TOT fall would be temporary – but most of the regulatory stuff was largely a continuation of the previous regimes. The subsidies became more burdensome because in the face of high inflation the govt wouldn’t allow eg the retail price of milk to rise, but they weren’t new subsidies – and again the Muldoon govt quickly got rid or, or substantially reduced many of the subsidies.

LikeLike

It would be interesting to know the breakdown of households, corporate and government savings, and whether there were any patterns/trends within each of those.

The points you make about what may have impacted savings mainly refer to household savings(?), so 1) did anything influence corporate/government savings, 2) what are the relative sizes of household, corporate and government savings?

I don’t understand what savings really constitutes in this measurement. is it just income that is not spent each year? What about changes in values of assets? Are dividends from NZ corporates to overseas owners reflected?

How would the following examples be reflected in savings, if at all?

A NZ farmer buys a farm, makes some improvements and sells it, say, 10 years later for 100% more.

An Aus prospector buys rights to prospect in the outback, finds gold, raises some capital, sets up a mine and sells it, say, 10 years later for 10000% more.

I thought of these examples in your earlier posts this week about GDP growth etc. By and large, agricultural countries don’t “create” new farms, they just make existing farms more productive/valuable in relatively small increments. Mining countries “create”/discover/develop new mines and create large increases in value (compared to the value of the unprospected land).

I had some other doubts about whether the exchange rate really affects GDP growth in the long term, but I’ll leave that for now.

LikeLike

…LS, I thought this paper by the BIS could help (or hinder!): puts an emphasis on the distinction between ‘Saving’ and ‘Financing’ in a monetary economy; a bit of a brain ache (to me at least!) but might be of interest, cheers

Click to access work525.pdf

LikeLike

I might do a post later in the week on the sectoral split of saving, altho the data are not as up to date.

Here, saving is just the difference between income and consumption spending. Changing asset values don’t affect it, although they do affect nominal measures of wealth (the biggest fluctuations in asset values in NZ are house prices, and higher house prices do not make the people of the country as a whole better off – we all have to live somewhere).

On your specific examples.. The NZ farmer making improvements would result in an increase in national accounts investment. Whether there was an increase in saving would depend – if he funded the improvement by increasing the reinvestment of profits that would be saving, but if it were debt funded and the debt was repaid only from capital gain there would be no recorded increase in flow saving.

Actually much the same goes for the mine. Saving is about the financing side. Investment can be funded by domestic saving or foreign saving, and if there is more investment and no more local savings, the difference will be financed by an increase in foreign saving (this is an identity).

LikeLike

Funny how the drop in savings coincides with Muldoon’s becoming prime minister.

LikeLike

actually, it dates more closely to the introduction of Roger Douglas’s compulsory savings scheme!. Muldoon didn’t become PM until Dec 1975, and the first two low observations in my chart (yr to Mar 75 and to Mar 76) really ante-date him

LikeLike