Statistics New Zealand released yesterday the annual data on New Zealand’s overall foreign trade (goods and services) by country. It is a nice summary set of tables for people who don’t spend lots of time looking at trade data, and the services data are only available annually.

Since the end of last year, these have also been the data the Reserve Bank now uses to calculate the weights in its trade-weighted index measure of the exchange rate. Those weights are calculated on a total trade basis (imports and exports, goods and services) for 17 currencies, covering countries that currently account for a bit over 80 per cent of New Zealand’s foreign trade. The weights are updated annually, and when they are updated in December there will be a few changes. After much noise about China becoming our largest trading partner (which it has not yet been on a total trade, or even total exports, basis), China’s share in New Zealand’s foreign trade dropped back quite a bit over the last year. By contrast, the United States’ share rose. Whereas this year, the weight on the Australian dollar was only 2 percentage points more than that on the Chinese yuan, both well ahead of the US dollar, next year the weight on the yuan will be around halfway between those on the Australian and US dollars.

There is no easy right answer as to how to weight an exchange rate index. My own sense is that the current weighting structures overstates the importance of Australia, and understates the importance of the United States and the euro area (or the EU more broadly). These latter two economies/regions are a huge share of total world production/consumption, and are major competitors in our largest (net) export products, particularly dairy. Neither element is captured in the current weighting scheme. And while Australia is our largest export market, those numbers are flattered by the fact that still more than 12 per cent of our exports to Australia are crude oil and precious metals (presumably mostly newly-mined gold), which have nothing to do with wider economic conditions in Australia, or movements in the Australian dollar.

It is interesting how much of our trade with Australia is now dominated by travel. Excluding oil and precious metals, 28 per cent of our exports to Australia are travel and transport. No other single category exceeded 7 per cent of our exports to Australia last year. The picture is similar on the import side, where travel and transportation account for 27 per cent of our Australian imports.

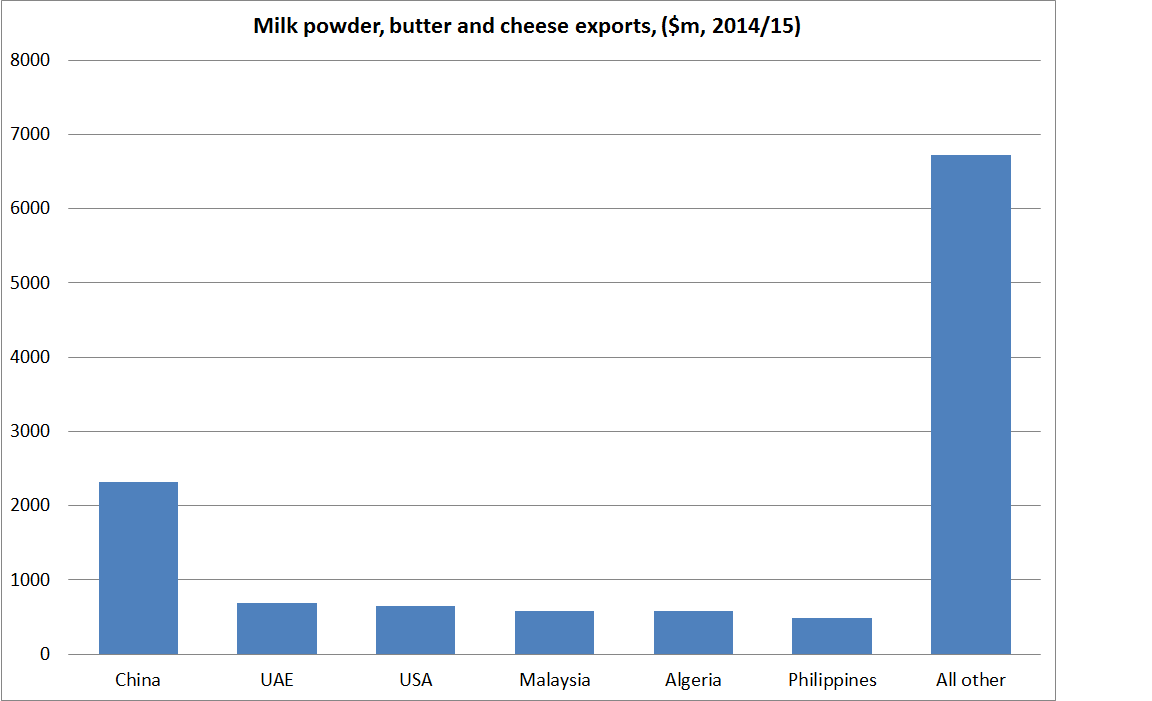

And, finally, I was interested in the dairy export data. The media has been full of discussions around dairy exports to China, which had surged in 2013/14.

Here are our milk powder, butter and cheese exports for the last five years to China on the one hand, and the ASEAN countries on the other.

It highlights both how unusual last year was, but also how important those other countries are in New Zealand’s dairy trade. In a typical year, New Zealand firms export as much milk powder, butter and cheese to these countries as to China, and yet these countries in total have annual GDP not much more than 20 per cent of China’s. Actually, the data also illustrate just how diversified dairy exports are in a typical year.

By contrast, in the 1950s almost all our dairy exports went to the United Kingdom, and there were few other export markets anywhere for dairy products.

None of this is to suggest that China is unimportant. China is now the world’s second largest economy, with a very large foreign trade for a country of its size. And is a badly-managed, highly non-transparent, economy, at the tail end of one of the bigger, least-disciplined, credit booms in history. What happens in China matters a great deal to most countries, but there is no reason to think it matters abnormally more to New Zealand.

(As one perspective on the lack of transparency – and, worse, outright misrepresentation – that plagues the rest of world making sense of China, I’d recommend the latest from Christopher Balding, who takes on those who want to defend China’s data as providing a broadly accurate and representative picture of what has been going on).

We can rubbish China’s data and the management of their economy but history shows the largest and fastest shift in the wealth stakes from West to East has occured in the last 30 years, together with at least a billion plus people lifted out of poverty. If it was such a badly managed economy this would not occur.

Our own numbers and the poor interpretation of our numbers by our top economists has led to poor government policies.

eg.

1. NZ household income stats does not include overseas income. New migrants get exempted from income tax on their overseas income for at least 4 years. 25% of New Zealanders have previously been migrants ie 1million people.

2. NZ household debt does not exclude debt used to run businesses as the debt servicing costs are much lower than business debt, small businesses tend to use residential debt as the interest is lower by as much as 3% to 4% per annum compared to business debt.

3. NZ economists trying to compare NZ household income versus NZ household debt. The two are not comparable because there is potentially 1million expat kiwis that do hold debt and houses in NZ but has an overseas income and therefore their overseas income is not reflected in NZ household income.

4. Using demographia urban stats when demographia stats do not consider the geography of the city and do not consider the infrastructure spending required to make land available for building.

5. Continuing with traditional monetary policy when clearly central bankers around the world have shifted from traditional monetary policy.

6. Using PLT migrant numbers without excluding international tourists, international students, foreign workers and returning kiwis and without property disclaimers that the interpretation can be skewed badly.

LikeLike

Take a slightly longer view and China has been a disastrous under-performer when compared to Taiwan, Korea, Singapore, and Japan. Yes the last 30 years have been better, but only after the utterly awful decades (administered by the same party in power today).

I won’t respond to the data points in detail, but on 2 the Reserve Bank earlier this year started producing a series that excludes debt in respect of investment properties. The general point you make is a fair one, altho not an issue unique to NZ. And as the Bank has noted in Bulletin articles, cross-country levels comparisons of household debt are pretty fraught for all sorts of reasons.

LikeLike

Same party but different administrators. China did have an unfortunate period with the Gang of Four seizing control with an aging and ailing Chairman Mao Ze Dong in the backdrop insistent on a cultural revolution as the way forward. Mao as a younger leader was pro reform with a emphasis on international trade and self suffiency welcoming assistance and investment from the west. Taiwan, Korea, Singapore, and Japan are tiny and far less complex compared to China which was a country previously ruled by scores of wealthy warlords with their own independent armies losely cobbled together under a KMT banner.

LikeLike

I’m enjoying Balding’s blog and twitter feed. However one thing I haven’t seen discussed much is what if an internal consumption reform China is simply impossible, because it would involve a wealth transfer away from the SOEs (which the CCP membership effectively “own” or derive wealth from via managerial capture) to households. Political change is also impossible. After a period of denial, the currency peg is abandoned and CNY falls precipitously, perhaps to 8-10 to the USD. In this case, wouldn’t the massive overcapacity in steel, aluminium and many other sectors then be forced onto world markets, forcing ROW industrial production to fall dramatically? Michael Pettis thinks this would result in trade sanctions but it must be said China has done a lot of fairly egregious things before from IP theft to island building to mercantilist trade policy in the mid-2000s without generating much of a response. So, if this were to eventualise, it would place a great deal of pressure on Western central bankers, who haven’t always inspired confidence with their crisis management skills.

A more positive interpretation would be to say that freeing the RMB would be a form of monetary stimulus in China and this would boost household incomes, thus meaning China can buy more goods from ROW.

LikeLike

Tyler Cowen notes his view that switching to a consumption-driven economy isn’t likely, or at least other than via path that involves much lower growth for a while. HIs story rings true (and to me it seems implausible that people will be keen to spend much more in a climate of heightening uncertainty and employment risk)

http://marginalrevolution.com/marginalrevolution/2015/09/a-simple-primer-for-understanding-chinas-downturn.html

I think letting the RMB go would enable more monetary stimulus (can’t do too much now, beyond offsetting the drain on reserves on account of the capital outflow, for fear of increasing the pressure on the exchange rate). But the interesting question is how much more demand would looser monetary policy bring forth. Has been a pretty slow and sluggish process in the advanced world in the last 8 years.

Re risk of sanctions, who knows (as you say, Chinese have done lots of egregious things) but a political climate in which Trump and Bernie Sanders are doing so well, and Corbyn will lead the UK Labour Party next week, isn’t normal times.

LikeLike

Regarding the graph above showing milk powder, butter and cheese exports as exceptionally high in 2014, do you think NZ oversold these products to China and they in turn have become the market leader ie NZ lost its dominant supplier role and we now have the tail wagging the dog?

LikeLike

I assume we typically sell to whoever is bidding most aggressively and that was the Chinese that year. I’m not one who believes that NZ really has much market power to lose – and any that we had is probably much less now that US producers are becoming a much more major export competitor, and EU production quotas have come off.

LikeLike

Any truth to the rumour that the Chinese drafted the investment lending RIS?

LikeLike

Hmm, not sure about the trade data with Australia , it looks that to a first approximation we only have net exports of oil and gold, everything else looks about equal in both directions. Am I missing something?

LikeLike

sure, but there is no reason to be particularly concerned about the balance with any particular country. Policy should probably only be concerned if there is too large an overall current account deficit (or perhaps – as Singapore, “too large” a surplus)

LikeLike

I was a bit shocked when I finally found the deeply hidden Table 15 showing New Zealand’s trade with Australia, it is badly laid out and doesn’t add up. Specifically the sub categories don’t add up to the totals and the categories are in a different order for imports and exports. Have these people not used spreadsheets before or heard of HTML tables for ease of access? I cannot imagine how much work goes into collecting this data, why not spend an hour or two on the front end so it’s easy to access and manipulate?

LikeLike