According to a new poll out this week, 93 per cent of New Zealanders want “financial literacy” to be a compulsory subject taught in all schools. The details of the poll don’t seem to be available, but we can probably assume that the questions were phrased in such a way as to encourage a positive answer. No doubt even a more balanced question might have drawn a positive response. To many it sounds like a “good thing”. I’m sceptical.

I’m sceptical at a variety of levels. First, and perhaps most practically, these surveys (and the reported views of advocates) never ask what people would prefer schools to stop teaching. There are only so many hours in the day/year. I’d face the same question as what should the schools stop teaching, but given a choice, personally I’d rather that schools were required to teach a sustained course in New Zealand and British/European history than that they teach so-called financial literacy. Kids are exposed every day to their parents’ attitudes to, and practices with, money and things. They aren’t directly exposed, to anything like the same extent, to maths, science, history, or foreign languages.

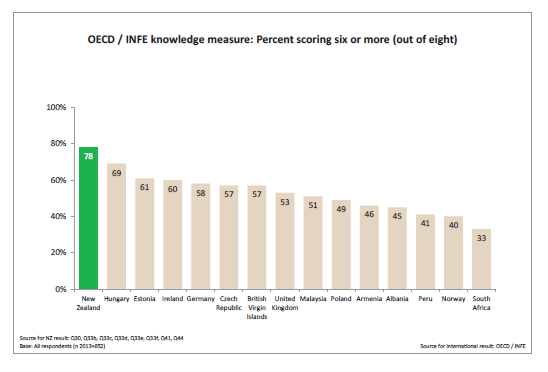

Second, as far as I can see, the evidence is pretty mixed as to whether teaching “financial literacy” makes any difference to anything that matters. Are countries with higher “financial literacy” scores richer as a result, more stable, happier? And a recent report (page 32) for our own government agency that deals with this stuff actually showed that, for what it is worth, the “financial literacy” of New Zealanders scored quite well in international comparisons. What is the nature of the problem?

Third, why would we expect that the government, and its representatives, would be good people to teach children about money? Perhaps we should judge people by their track record. The current Retirement Commissioner, as captured in this profile, does not exactly inspire confidence on that front (unless perhaps “do as she doesn’t kids”). And at a bigger picture level, in one way or another governments are the source of most financial crises – Spain, Ireland, Argentina, the United States, China. Governments are more prone than most to undertaking projects that they know provide low or negative economic rates of return. Governments face fewer market disciplines than citizens. And governments don’t have to live with the consequences of their mistakes. So perhaps I could support a civics programme that included a section on critically evaluating election promises and government policy announcements.

Fourth, much of the discussion in this area is quite strongly value-laden. And no doubt it has always been so. I recall the day when our 6th form economics class was visited by a banker, to try to promote savings etc. He brought along a hundred dollar note – this was 1978, and it was probably the first time any of us had seen one. Trying to set up a discussion about the merits of bank deposits (probably with negative real interest rates at the time), he asked us all what we’d do with the $100 if we had it. Various class mates rattled off their spending wishes, but the banker was totally flummoxed when one of my friends, a strong Christian, told him that what she’d do was to give it away. .

And where, for example, in all the discussion of financial literacy is there any reference to the findings that one of the best routes to financial security is to get married and to stay married? Finding the right spouse, and learning what is required to make a lifelong commitment work, is almost certainly a more (financially) valuable lesson that knowing that when interest rates fall bond prices rise. But it is not one we are likely to hear from the powers that be.

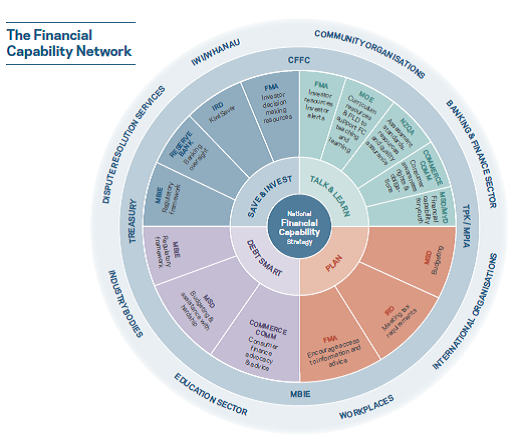

And fourth, this becomes an excuse for yet more bureaucratic/political bumf, reinforcing a sense that governments should have “strategies” about everything and anything. I was somewhat surprised to learn that our government has a financial capability strategy. Why?

Building the financial capability of New Zealanders is a priority for the Government. It will help us improve the wellbeing of our families and communities, reduce hardship, increase investment, and grow the economy.

The National Strategy for Financial Capability led by the Commission for Financial Capability provides a framework for building financial capability. It has five key streams:

- Talk: a cultural shift where it’s easy to talk about money

- Learn: effective financial learning throughout life

- Plan: everyone has a current financial plan and is prepared for the unexpected

- Debt-smart: people make smart use of debt

- Save and invest: everyone saving and investing

On this measure, might we assume that “debt-smart” would mean taking as much interest-free student debt as possible and paying it off as slowly as possible? Not an approach I will be encouraging in my children.

More generally, I’m not sure that any of these items represent areas where we should expect governments to bring much of value to the table. One might marvel that human beings had got to our current state of material prosperity and security without the aid of government financial literacy/capability strategies. And since when has a traditional Anglo reticence about matters of money been something for governments to try to change? Better perhaps might be a focus on improving the financial capability of governments.

The Commission’s own research (p 26) shows what one might expect, people develop more “financial literacy” as they need it. So-called “literacy” is low among young people (18% of 18-24 year old males are “high knowledge”), who don’t need it much. It rises strongly during the working (child-rearing, mortgage etc) years (53% of 55-64 males are “high knowledge”), and then looks to tail off a little in retirement. All of which is unsurprising, and (to me) unconcerning.

I know the so-called Commission for Financial Capability doesn’t cost that much money, but as I’m sure they would point out, every little counts. The money they fritter away on national strategies and capabilities is money that New Zealanders don’t have to spend, or save, for themselves. In fact, this graphic, from the government’s policy statement, might suggest a few other government agencies that could be a trimmed back. Governments need to do well what only governments can do. So-called “financial literacy” isn’t obviously one of those things.

As an easy way into this, consider this US-government funded online quiz, a shop window for a US project on better understanding financial literacy. I imagine that most readers of this blog will score 5/5, while the average American scores 2.9. But then stand back and ask yourself why the average American (or New Zealander) needs to know the answers to these questions, phrased rather in the manner of a school economics exam. People who read blogs like this take for granted a knowledge of the answers, but in what way has that knowledge made your life, or mine, better?

So is the government saying its wants a trend towards educating accountants? To me accountants, lawyers are ‘watchers’ ie they can only look and comment on what actually gets done by scientists, engineers. The latter in my view add value to society, the former only distract from it.

LikeLike

I think there is that tendency. Actually, I’d prob draw the contrast between accountants/lawyers (and public servants) on the one hand, and entrepreneurs on the other – people who risk everything on an idea/project. Of course, societies need all sorts, but no one built a great business by focusing on diversification.

LikeLike

That Herald profile – oh dear. Where does the Government find these people?

LikeLike

Agree, there are plenty of website games that teach financial literacy to children. My child plays Jumpstart.com which gives out gems if you have completed certain tasks. You can then use those gems earned to go to a supermarket to buy products for your next set of tasks. Each task getting incrementally more difficult and requires earning more gems to complete. Great learning tool.

I think our kids specialize too early. They are required to pick their area of study in 6 subjects when they are still young teens and no idea where life will lead them. I agree a better grounding in history and philosophy would open up their minds and widen their thoughts.

LikeLike

I’m a simple coal-face economist who operates in the global-financial sphere and had never heard of CDO’s when the world blew up in 2007-2009 – when they started talking about these sliced-and-diced instruments I had to go and look them up – now they’ve disappeared again – who could have told you about TARP and QE I and QE II and QE III back in the year 2000

LikeLike

Sorry guys, but why is history any more important than financial literacy??? In a real free market the kids would choose themselves what they want to learn, not have history forced on them.

LikeLike

In my telling just because every child is exposed, pretty much every day, to how parents deal with money and goods, but they aren’t exposed to science, maths, history, languages etc. Most people would say free markets shouldn’t apply to childrens’ choices – in a sense that is a meaning a childhood – but I’d have no particular problem with a system in which parents could choose. Some would n0 doubt make bad choices. As it is, governments make many.

LikeLike

“Every child is exposed … To how their parents deal with money.” And this is an argument against financial literacy?! I jest. But you see my point. What about that retirement commissioner’s kids?

Anecdotally, my friends growing up who were useless with money would often express sentiments in favour of financial literacy.

I don’t find your arguments convincing. Your comments regarding marriage appear to be interpreting correlation as causality.

LikeLike

I’d argue that there is not much the state can do about culture – indeed, the track record is often that the state unwittingly undermines in others the sorts of disciplines that those espousing the cause of ‘financial literacy” are often most comfortable with. Of course, I have no objection to “financial literacy”, but it isn’t an obvious role for the state, and certainly not for state compulsion.

Re marriage, on my reading there are elements of both correlation and causality. But to the extent it is correlation, I think it is largely back to culture, on which see above.

There are a lot of enthusiastic social engineers among the bureaucracy and academe. but refraining from harm may be the best the state can do.

LikeLike

In your opinion at what point does education become social engineering? I think of financial literacy as a specific form of numeracy and accounting, nothing more. It is certainly harder to argue these subjects are examples of social engineering than say history. Just look at the battles over history textbooks in Texas or Japan.

Also, please point me to any studies that you may know of that have shown that marriage *causes* better financial security, or better outcomes in general for adults and/or children. Establishing causality would require some kind of natural experiment. I am genuinely interested.

LikeLike

Yes, I wasn’t thinking of “financial literacy” in schools in the comment about social engineering, which was more about the inclinations of bureaucrats more generally – the belief in the ability of governments to generate “progress” and the ability to improve society. In terms of indoctrination in schools my favourite recent example comes from a science teacher, who had my 11 year old son watching The Story of Stuff (a fairly anti-business piece of propaganda – and quite effective as such) as a description of how the world is (with no counterbalance at all).

Will come back to you on the other point.

LikeLike

I suspect we’d have better results if we simply had a sufficiently numerate and literate population coming out of schools. Whatever ‘financial literacy’ actually is, it is probably not much more than a simple application of concepts which should really be in place by the time you leave school and my guess would be that at the heart of most money problems are basic errors in comprehension and arithmetic. Am I oversimplifying?

LikeLike

Sounds plausible to me

LikeLike