As part of the review of (parts of) the Reserve Bank Act, The Treasury is inviting comments and suggestions, on how the changes in stage 1 of the review (statutory goal of monetary policy, establishment of a statutory monetary policy committee) should be implemented, and on what else should be reviewed in the forthcoming stage 2 of the review.

Last Thursday I went along to a Stakeholder Engagement Roundtable, in which Treasury had invited various private economists in to offer our perspectives on those issues. My post on Thursday – on the statutory goal of monetary policy – was, in effect, part of my notes in preparation for that meeting. In the discussion, opinion was fairly mixed on the merits of making a change, but it was generally recognised that the government had committed to change and so the main issue was how best to give it legislative form.

The second chunk of the discussion was about the establishment of a statutory monetary policy committee. Here there seemed to be greater unanimity that reform was desirable, and that part of any reform should be a greater emphasis on transparency, including individual accountability.

I’ve covered my own views on various of these points in earlier posts, but for ease of future reference, I thought I’d bring them together in a single post. My model would not replicate that in any single other country, but is probably closest to the monetary policy committees in the United Kingdom and Sweden.

Who should appoint the members of the committee?

All of the members should be appointed by the Minister of Finance. People who exercise significant statutory power – and the conduct of monetary policy is certainly that – sholu.d either be elected themselves or appointed by those who are themselves elected. That is the general approach we take to governing New Zealand: whether it is Cabinet, the courts, the boards of Crown entities, the Commissioner of Police, or the Auditor-General. There is no particularly good reason why members of a Monetary Policy Committee should be different. There are probably unique aspects to all governance appointments, but nothing around monetary policy marks it out as warranting putting another layer between the elected and the decisionmakers.

This is, of course, in contrast both to the current model (single decisionmaker – the Governor – in effect appointed by the Bank’s Board), and to the model Labour campaigned on (where external members would be appointed by the Governor – putting them at a further removes from someone who has to actually face the voters). Allowing the Governor to appoint the external members would risk substantially undermining the reasons for the reforms.

In the United States nominees for the Federal Reserve Board of Governors are required to win Senate confirmation. That isn’t our constitutional model. In the United Kingdom, appointees are required to face a parliamentary select committee hearing before taking up the role. The committee can’t block the appointment, but can report on the suitability of otherwise of the nominee. This might be a useful feature to add here. It isn’t an approach we take generally, but monetary policy makers exercise wide powers of discretion (much more, say, than a typical Crown entity Board member) and, with ex post accountability difficult to maintain, it seems reasonable that those taking up such roles should face some open scrutiny at the start.

There is a counter-argument that the Governor should be free to appoint his or her own Deputy (as might be normal in a commercial context). To which my response would be that if the deputy was not serving on a statutory committee, exercising statutory powers, that model would be fine. But if the Deputy Governor is to exercise statutory powers, they should be appointed by someone who was elected, and who is accountable to voters: as far as I can tell, that is the typical model (including, for example, in Australia and the United Kingdom).

How many members should there be?

I’d favour either five or seven. Any larger number would make it unduly difficult to fill the roles with good people consistently through time.

Either way, I’d favour having two internals (executives) – the Governor and a Deputy Governor – with the remaining members being part-time non-executives. It is highly desirable to have a majority of members who are outside the managerial hierarchy of the Bank. Put the structure the other way round and there is a high risk that, over time, the non-executive members will be neutered (with management coming to block vote), and that then good people will be unwilling to put themselves forward to serve on the committee. Non-executives will always be at some disadvantage – re access to analysis, and ability to influence the research agenda etc – and only be holding the majority of votes on the committee will they be able, if they choose, to consistently push back against that pressure.

The counter-argument often made is often about technical expertise: the choice between internals and externals is often presented as a choice between experts and non-experts. To which there are several responses to be made. First, as the Reserve Bank is currently structured, the internals will often not be “experts” on monetary policy at all – none of the Governors since 1989 could really be classed as “experts” on monetary policy, although of course over time they acquired considerable experience, and even among Deputy Governors there have been considerable differences of expertise and background. And the skills of being a good chief executive – running the organisation, generating the analysis, managing the operations – also aren’t necessarily those of a leading monetary policy expert.

But perhaps as importantly, while I think it is vital to have expert advice and analysis, as inputs to decisionmaking, it isn’t clear that we want technical experts making policy decisions, and exercising the (inevitable) degree of discretion that monetary policy makers do. Some people with technical expertise may be able to serve effectively as decisionmakers (and communicators) but the skills aren’t the same at all. And if the internal members of a Monetary Policy Committee, with all the technical resources of the Bank staff at their command, cannot convince one or two non-executive members of the merits of their case, it seems unlikely that they will be able to convince the wider public.

What sort of non-executive members should be appointed?

I’m wary of making much of an internal vs external distinction, and instead focus on that between executives and non-executives. After all, there has been no internal candidate appointed as Governor since 1982.

But in considering non-executive appointments (three or five in my model) there are a few relevant considerations:

- no one should be appointed to represent a particular interest group. Of course, everyone has a background, but once one takes up a position on an MPC your commitment has to be to implementing the Act and serving the interests of the country as a whole,

- there should be no prohibition on non-resident or non-citizen members (although I would favour no more than one at a time). We are a small country, and there can at times be valuable perspectives that people employed abroad can offer (and it is a model the UK has used), as one vote among five or seven,

- it would be desirable to have one member with some reasonable academic exposure to monetary policy, but undesirable to think of a Monetary Policy Committee as, say, a research conference or an academic seminar,

- people with sound general Board-level skills can make a valuable contribution to an MPC, regardless of their formal academic background. One doesn’t typical want an telecoms company Board stuffed full of tech people, and there isn’t any obvious reason why a Reserve Bank MPC should be different. The ability, and willingness, to ask hard questions, and even just to say “tell me that again, in ways I can understand” is a valuable part of the mix.

How long should MPC members’ terms be?

I would favour five year terms, perhaps with a limit of one reappointment each. With five or seven members, one appointment would come up every year or so, enabling a government is the course of a three year term to replace gradually around half the members of the committee, but not to launch a purge on newly taking office. Terms of this length seem reasonably conventional (and are the same as those of the Governor, and Board members, at present).

Individualistic or collegial?

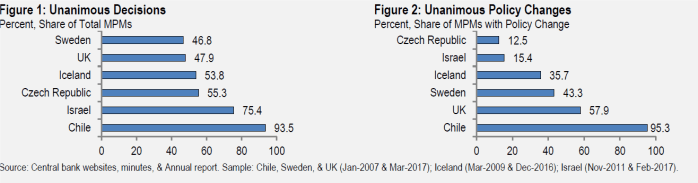

I’ve outlined here previously why I strongly favour the sort of individualistic model adopted in the UK, the USA and in Sweden, in which individual members of the MPC are individually accountable for their votes. The current management of the Reserve Bank really dislikes the model, but they have never been willing, or able, to articulate – from the experience of other countries – what the nature of their concerns is, and how they balance any such concerns against the interests of democratic accountability, in a model in which decisionmakers exercise considerable discretion.

As I’ve documented here over the years, formal effective accountability for monetary policy decisions is hard – much harder than those who devised the current law thought at the time it was drafted. In practice, accountability can be exercised only through public scrutiny and challenge, and at the point where a member of the MPC is up for reappointment. Against that backdrop – and in a game where there is so much uncertainty – it is highly desirable that individual MPC members’ votes should be recorded and published, and that members should have the opportunity to have their views recorded in minutes that are published in a fairly timely fashion. The Reserve Bank’s management has at times expressed concerns about this approach – used elsewhere – “muddying the message”, but in fact there is so much uncertainty about the way ahead (what is going on with the economy and inflation) that over time it will usually be preferable to have in public the sorts of issues and concerns that were bothering decisionmakers, rather than just some sort of somewhat-artificial consensus about an immediate OCR decision.

In a similar vein, MPC members should all be free to make speeches, give interviews etc articulating their own views on the issues the MPC is facing. I’m not suggesting some sort of chaotic free for all: it would no doubt be desirable for members to develop protocols in which members ensured that other members were aware of forthcoming speeches and interviews, agreed to circulate draft texts to each other in advance, and perhaps agreed to avoid comment altogether in the week or so (say) prior to an OCR announcement. Commonsense and common courtesy can resolve many potential issues.

Who should chair the MPC?

The Governor. I hadn’t particularly thought of this issue, but it came up at the Treasury meeting the other day. There is an argument for a non-executive chair – the approach in most Crown entities – but provided there is a majority of non-executive members I’m not sure I see the case for departing from the universal international practice, in which the Governor chairs the MPC. (It is also perhaps worth noting here that in other countries – including the UK – it has not been a problem if the Governor has at times voted with the minority. Smart people will often view the same data quite differently.)

Transparency

The amended Act should require the publication of minutes, and the record of individual votes, within a reasonable time – perhaps to be determined by the Minister – of the particular OCR decision. As I’ve noted previously, I do not favour either keeping, or eventually publishing (even with very long lags), transcripts of MPC meetings.

I would also favour moving to a system where the background papers for MPC meetings are routinely and pro-actively published (perhaps six weeks after the OCR decisions to which they relate). Ideally, I would not consider this something that should be legislated, but given the obstructiveness of the Bank, and the willingness of successive Ombudsmen to aid and abet the Bank in keeping such papers secret even well after the relevant decision, the legislative option may need to be considered.

As I’ve noted repeatedly before, the Reserve Bank is quite transparent about stuff it knows little abour – eg where the OCR might be a couple of years hence – but isn’t very transparent at all about what it does know about. Transparency is valuable in itself – an essential part of democracy – but in a small country with limited pools of expertise, the ability of greater transparency to facilitate more informed and debate and scrutiny of the issues is almost instrumentally useful.

Should there be a Treasury representative on the MPC (in a non-voting capacity)?

I don’t have a strong view on this issue, but it is a model that is used in a number of countries, and could help to formalise a recognition of the relationship between various bits of economic policy. The model appears to have worked, without undue problems, in the UK. But if it is to be done, it needs to be recognised that it would involvement a non-trivial time commitment by someone reasonably senior in Treasury – and time/resources are scarce.

The Policy Targets Agreement

At present, Policy Targets Agreements are (a) signed with the Governor personally, consistent with the single decisionmaker model, and (b) have to be agreed with an incoming Governor before that person is formally appointed or takes office. It is a poor model, and not one that is much imitated abroad.

Under my reform model, the MPC as a whole would be responsible for monetary policy and the onus of a PTA should also rest on them. To do that probably requires rethinking the PTA model, and might suggest moving to the system adopted in some countries – eg the UK – where the goal (PTA) is specified by the Minister of Finance, and the MPC is simply responsible for conducting policy consistent with that goal. The UK model isn’t ideal – the target can be changed at the Chancellor’s whim in the annual Budget – but a system in which the target is specified every few years, after advance consultation with the MPC of the day (and ideally with the wider public, and with FEC), would seem to have some attractions. To get the right balance between responsibility for setting overall goals – resting with the elected government – and a degree of stability, perhaps the appropriate review period might be six months after a change of government (with provisions for other changes to the PTA only in exceptional circumstances – say with the agreement of the majority of the MPC.)

The final issue Treasury asked us about under this heading was about the role of the Bank’s Board. There seemed to be pretty universal agreement among attendeees that the Board adds little or no value. But, as I’ve noted here previously, you can’t really answer the question about the appropriate role of the Board without thinking harder about the overall organisation of the institution (rather than simply one function – monetary policy). I’ll come back to that on Wednesday.

And on a completely different topic

Regular readers will know that I live in Island Bay. Some will have seen the story in yesterday’s Sunday Star-Times suggesting that our local primary school was “New Zealand’s richest primary school”, based on reported donations in 2016 of $490000. This qualifies as pretty poor journalism. Island Bay School is a decile 10 school (although I suspect in the poorest 10 per cent of the top 10 per cent of neighbourhoods). It was reported that

“Island Bay school’s 460 students contributed $490000 donations in 2016 – an average of $1065.46 per student for the year’s schooling”

In fact, those parents who paid the scheduled annual donation paid around $250 per child, in other words only around a quarter of the total. But one, very wealthy, old boy made one very generous donation. Here is the Principal’s newsletter from 10 March 2016

I awoke to the best news ever this morning: Sir Ron Brierley, an old boy of the school, has generously agreed to donate a sizeable sum to the Rimu Block modernisation project. This gift, combined with Ministry of Education funding, gives us sufficient funding to realise our full vision for the modernisation of Rimu. This would not have been achieved without the generosity of Sir Ron, who has been a wonderful friend and supporter of Island Bay School over the years. In 2011 he kindly contributed towards the Learning Hub and now he has made this contribution towards Rimu Block.

As a parent, it always amused me that such a left-leaning school (and successive Principals) were taking such large amounts of money from a generous capitalist. It is a real gain to the school, but it is almost totally irrelevant to the debate around the “donations” that parents are asked for each year.