I’d had more or less enough for this week of thinking/writing about Reserve Bank reform issues, when a (central banker) reader sent me a link to an interesting new survey article by a couple of researchers at the central bank of Chile looking at various institutional arrangements, including decision-making and communications, at 15 inflation-targeting central banks (all from OECD countries). I’d suggest The Treasury, and the Independent Expert Advisory Panel appointed by the Minister to assist with the review of the Reserve Bank Act, take a look at the paper.

It isn’t perfect by any means – and there were a surprising number of small errors of detail or emphasis, including in places about New Zealand – but there is a lot of interesting material nonetheless. For a start, they seem to have chosen pretty much the right group for comparison: the well-established market economies, with reasonably well-governed democratic societies. One might quibble about the inclusion of Poland, or note that if Poland is included perhaps Hungary should be too, but if you are looking for insights and ideas as to how our central bank (in its monetary policy dimensions) should be organised – and wanting something to read to complement the Reserve Bank piece I posted here yesterday – this list of central banks/countries seems about right:

ECB, USA, UK, Japan, Canada, Korea, Norway, Sweden, Australia, Israel, Chile, Poland, Czech Republic, Iceland (plus New Zealand)

I wasn’t too interested in, and won’t comment further on, the detailed material on the specification of the inflation target itself (except to note to the authors that the New Zealand target now has an explicit midpoint reference) – ground well-covered in various earlier Reserve Bank articles.

What of statutory decision-making structures? Of the 15 central banks, only New Zealand and Canada do not have a statutory committee making monetary policy decisions. That is well known. What is less well-known perhaps is that all those 13 central banks with statutory committees operate by vote. The authors note that Canada and New Zealand describe themselves as attempting to operate by consensus, but in fact of course in both places only one vote formally counts – that of the Governor, who has the legal responsibility. And even in New Zealand, although the three man Governing Committee is claimed to operate by consensus – they refuse to release any minutes, even under the Official Information Act, to allow us to really know – the members of the wider advisory group make written OCR recommendations, in effect a non-binding vote.

In some of their writings, the Reserve Bank likes to claim that consensus-building models of decision-making are superior. There may be some arguments on that side of the issue, but actually voting – after examination of the issues, discussion and debate – is typically how we make decisions in free societies: be it in elections themselves, decisions of a local tennis club committee, or our higher courts (five judges on the Supreme Court: the verdict supported by the majority rules). There is no particular reason to think monetary policy decisions are not as well made the same way – indeed, since there is a great deal of uncertainty, and decisions are revisited every eight weeks or so (so there are few irreversibilities) it seems a pretty demonstrably efficient approach.

The Reserve Bank has also sought to claim that small committees are generally better than large committees. Again, at some point no doubt there is truth to that – with all due respect to the Cabinet, the 20th person on any committee is unlikely to be adding much marginal value, and the incentives for any specific member of a committee that large to slack off (put in little effort or fresh thought) can be real. But of the 13 inflation targeting central banks with statutory monetary policy committees, the median number of members is eight. For a smaller country, a statutory monetary policy committee with five or seven members sounds about right for New Zealand (none of these statutory committees in other countries has fewer than five members). Membership numbers don’t seem to be a luxury good: the authors present a chart showing no relationship between GDP per capita and the number of MPC members in an inflation-targeting country.

It is also clear that members of the statutory monetary policy committes are almost entirely appointed by politicians – as most key positions in our societies typically are (from Chief Justice or Police Commissioner down). There are some exceptions – eg regional Fed Presidents in the US (who rotate through voting membership of the FOMC), but even that situation is now raising some concerns among scholars in the US. And almost all of the central banks with statutory MPCs have external members, in some form or another (sometimes part-time, sometimes becoming temporary full-time executives, sometimes full-time non-executive): governments rarely seem to see monetary policy decisions as matters only for some career “priesthood of the temple”.

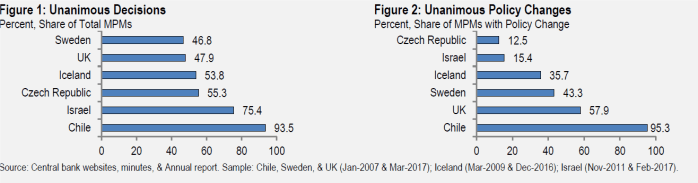

I was also interested in some analysis the authors had done on the extent of unanimity, or otherwise, among monetary policy committees where voting decisions are published.

To listen to our Reserve Bank, if voting records were published, or minutes in which individual members could outline their views on specific monetary policy decisions, it would be a recipe for mayhem. They’ve talked of it creating confusion, and uncertainty, undermining confidence in, and the credibility of, the central bank.

Here is what the Chilean authors have to say about such individualistic committees.

In individualistic committees each member is held publicly accountable for their decisions, and each member is empowered with one vote. Decisions tend to be reached by majority vote, where the Governor tends to have the deciding vote in case of a tie. The high degree of individual accountability results in regular reservations, dissents, or minority votes against the final policy decision. Two regularly cited examples of this type of committee are those of the UK and Sweden. Importantly, when a certain degree of public disagreement among committee members occurs, market participants are generally not surprised and understand the differences as part of the policy process.

That is more or less the point I’ve been making. One could say the same about the United States. And recall that these authors are themselves from a central bank with a committee more towards the “collegial” end of the scale.

And, in any case, as they illustrate, even in individualistic committees raging dissent is hardly the norm.

Roughly half of all the monetary policy decisions in the UK and Sweden in the last decade have been unanimous. (On the other hand, even for central banks at the collegial end of the spectrum, not all decisions are unanimous). I’m not sure why they didn’t include the Federal Reserve in this particular analysis, but I suspect the numbers there would show something similar to the UK or Swedish experiences.

There was also some interesting material on communications practices. For example, all 13 of the central banks with statutory monetary policy committees publish minutes – to repeat, every single one of them. The timeliness varies – the UK and Norway publish the same day as the monetary policy announcement, but a more typical lag in about two weeks – and of course the nature of the content differs: some are pretty bland, while others (notably those of Sweden) although a full and careful articulations of the arguments and issues of concern to individual members.

But there was also some surprises (at least to me). Our Reserve Bank grudgingly released background papers to a 10 year old interest rate decision, and consistently refused to release any background papers – no matter how topical – used in the preparation of their interest rate decision or Monetary Policy Statement (eg the recent refusal to provide any background analysis papers on the impact of various policies of the new government). By contrast, and at the other extreme, according to the Chilean paper the central banks of the Czech Republic and Norway “publish a version of the staff MPM [monetary policy meeting] presentations shortly after the meetings”. I struggle to see any good reason why such background analysis should not be released publically with, say, an eight week lag (eg released after the OCR decision one after the decision to which the background material relates)

And a bigger surprise still was the publication of transcripts of monetary policy meetings. I knew that the Federal Reserve was doing so, and had heard the odd mention of it happening elsewhere. In fact, the authors show that seven of their central banks are now doing so (including the Fed, the ECB, the Bank of Japan, and the Bank of England). The lags are quite long – the Fed is the shortest at five years. But, fascinating as some of the old Fed transcripts are, especially from the era before members knew they would be published, even I have my limits around transparency, and this is one of them. As the Chilean authors note

as highlighted by the Warsh Review (2014), the publication of meeting transcripts (and minutes) may to a certain extent impair a candid discussion of policy options among policy-makers, and lead them to limit their interventions to written statements that express their view (and vote) without the consideration of the perspectives of other members. In this context, it is possible that policy deliberations may be driven to other settings where a formal record is not being taken. Moreover, some existing evidence for the U.S (Meade and Stasavage, 2008) suggests that the publication of FOMC transcripts reduced the likelihood of dissent among committee members, and made members less willing to change their positions over time.

But the fact that various major (and minor) central banks are publishing such transcripts again helps give the lie to our Reserve Bank’s constant claim that it is one of the most transparent monetary policy central banks in the world.

One final aspect the Chilean authors covered was the role (if at all) of a Treasury or government representative in monetary policy decision meetings. In the Reserve Bank paper I linked to yesterday, the Bank authors attempted to minimise this issue. They noted that in Australia the Secretary to the Treasury is a voting member of the Reserve Bank (monetary policy making) Board and that in the UK there is a non-voting Treasury observer who attends (statutory) MPC meetings. Of our 15 central banks, that is all they note (although in Colombia, one of the countries they look at, the Minister of Finance is himself a voting member).

But here is part of the fuller Chilean treatment of the issue

In a second large group of central banks, an important authority of the administration, such as the Minister of Finance or his delegate, is invited to attend and speak in the MPMs, but does not have the right to vote on the monetary policy decision. Within this second group, the degree of potential government involvement differs. In Japan for example, the representatives of the government (Minister of Finance, Minister of State for Economic & Fiscal Policy) may propose issues to be discussed in the MPMs, and may even formally ask the MPC to postpone a vote on monetary policy until the following meeting. In the case of the Bank of Korea, the representative of the government (Minister of Strategy & Finance) may publicly request the MPC to reconsider a monetary policy decision if it perceives that the decision conflicts with the government’s economic policy.

Their tables also lists Chile, the Czech Republic and the UK as having non-voting Treasury representatives. In the comments on the Rennie review report from Charles Goodhart (ex UK MPC) and Don Kohn (a current member of the UK FPC) no concerns were raised about this aspect of the UK model.

I don’t have a strong view on the possible role of a Treasury representative on either a monetary policy or financial policy committee in New Zealand. But there is enough precedent in other countries to suggest that option deserves more serious consideration than the Reserve Bank – always keen to keep Treasury out of its hair – gives it. If there was to be non-voting observer, the rules of the game might be quite important – the person would be there to inform, answer questions, and report (as in the UK) and shouldn’t see themselves as having a role to try to shape decisions.

The Chilean piece was interesting and refreshing. They make it clear – without directly engaging with New Zealand issues at all – that if the government reforms our Reserve Bank Act to provide for:

- a statutory monetary policy committee,

- all appointed directly by the Minister,

- with a good mix of internals and non-executive internals,

- and timely publication of minutes and vote number,

- with perhaps even details of dissenting members’ views, and even

- delayed publication of background papers

It would be placing the Reserve Bank of New Zealand’s new model of governance. decisionmaking and communications right in the mainstream of international practice for countries of our type.

As it happens, I saw last night one other snippet reminding us of how far central bank transparency could go. The Financial Times had an interesting piece outlining concerns in some quarters about senior central bankers getting too close to private bankers (in the New Zealand in recent times – but probably not generally – the problem is more the opposite), with particular concerns about ECB head Mario Draghi. Partly in response

The ECB also now publishes the diaries of its six executive board members after officials were found to have met private sector representatives around the time of monetary policy decisions.

It might be a worthwhile model for our new central bank Governor to consider emulating, along with (in time) his deputies and members of the new statutory decisionmaking committees.

Our central bank was once at the forefront of (some aspects) of central bank transparency. These days, it has weak (formal) decisionmaking processes and doesn’t do at all well on the transparency front either. Those issues should be tackled properly as part of the current review.

The tom-toms are beating louder for the RBNZ

Today in the NBR, Kerry McDonald (one of the usual stable of the opinionated) rips into the RBNZ demanding they all chuck the keys of their cars on Grant Robertson’s desk and walk the gang-plank – he reckons they don’t have the competence to regulate the banks

Mcdonald wouldn’t be a mate of yours by any chance would he?

I’m not a follower of “Team RBNZ” so don’t have an intimate knowledge or understanding of the inner workings of the place. What I can do is understand how businesses and regulatory institutions work.

I have followed your long detailed missives about the bank for the last 2 or 3 years and still to this day I am hardly more informed than I was 2 years ago (about the daily operations). Although I do have a much better grasp on the inner workings of the governance and “claimed” power of the board and the governor and the TPA. But my knowledge of what the bank actually does hasn’t improved

In the absence of these understandings it seems what is being proposed (and touted) is equivalent to a sledgehammer to crack a peanut. It comes across as everyone being too busy planting and growing trees so you can’t see the forest. Keep them in the dark. This is secret-mens-business. Obfuscation. It’s like having a top-heavy Wellington-Centric Committee for the local Bowls-Club. That’s what it looks like.

What on earth do they do down on the floor. The Westpac Model slip-up didn’t cover them in glory- That slid by for some years.

When an outsider begins to research the RBNZ there are a lot of high-falutin high-sounding documents but the is no evidence of them actually performing those tasks

No evidence of what has been achieved with the AML/CFT oversight. Everything is good? No troubles? No Worries?

The system the RBNZ regulates is operated by the banks. The banks are supposed to notify the police. The banks have no responsibility to publish what they have done. The RBNZ has no requirement to publish what the banks have done. Secret-mens-business.

IMO this will only change when we have transparency. And I don’t mean drawing pretty graphs

LikeLike

I’ve never met Kerry McDonald, although I have a lot of time for his views on various issues (including NZ econ underperformance) so will look out for a copy of his article.

You’ve made the point previously that you don’t know what the RB actually does? (AML apart – which frankly bores me, and where policy in a matter for MoJ) what areas would you like to know more about? in fairness to the Bank, they do publish quite a lot of material about what they do – ie process, if not the substantive stuff.

LikeLike

Reblogged this on The Inquiring Mind and commented:

Michael has another useful piece on the Reserve Bank. He has strong views on this, but he makes through his many posts some valid points which bear thinking about. Plus he writes cogently and in a way which this idiot can understand.

LikeLike