I’ve come to think so.

The Reserve Bank has two main functions:

- conduct of monetary policy (and supporting activities – currency issues, foreign reserves management, interbank settlement accounts), and

- prudential regulation of banks, non-bank deposit-takers, insurance companies (and roles around payments system and AML thrown in for good measure.

These quite different functions are conducted in one institution, but they needn’t be. In fact, in most advanced countries they aren’t.

Historically, there wasn’t much prudential regulation in New Zealand at all. There was lots of direct regulation of various types of financial intermediaries (banks, building societies, savings banks and so on) but most of the regulation (reserve ratios, interest rate controls etc) was macro policy focused, not about financial system stability or depositor protection per se. That regulation – often administered by the Reserve Bank, but individually approved by the Minister of Finance – was a substitute for the sort of market-based monetary policy all advanced countries now rely on. As interest and exchange rates were freed up, the panoply of direct controls was stripped away. Our great bonfire of such controls took place in 1984 and 85.

By the time what became the Reserve Bank of New Zealand Act 1989 was going through Parliament, the primary conception of the Reserve Bank was as a monetary policy agency. Sure, there were some regulatory provisions – and in particular provisions around the handling of bank failures – but it was seen as pretty peripheral activity. If anything, it became more peripheral as the 1990s unfolded: the framework covered only banks (increasingly a foreign-owned group), there was a shift to a largely disclosure-based regime, and the function took very few staff (from memory, only around 10 or 12 staff). For practical purposes it probably wasn’t too much of an issue that the two functions were in one institution.

But as the 21st century unfolded so too did a dramatic change in the supervisory and regulatory activities the Reserve Bank was involved in. There were new classes of entities to regulate or supervise, new functions (payments system and AML) to regulate or supervise, new statutory reporting obligations, a reduced reliance on disclosure (even for banks), and new powers and new appetite for more direct and discretionary regulatory interventions (culminating, for example, in the numerous iterations of LVR controls in recent years). The Reserve Bank now is at least as much of a financial regulatory and supervisory agency as it is a monetary policy one. A large share of the staff, a large share of the budget, and a large share of the Govenor’s time is now devoted to these functions.

I’m not here offering a view on the merits, or otherwise, of these new activities. The point is simply that Parliament has either specifically mandated the Bank to do these new things, or written legislation that has allowed the Bank to do them. And those functions don’t look like going away any time soon. After all, if many details are a bit different from models used in other countries, the broad direction – more comprehensive, more intensive, controls – isn’t exactly some idiosyncratic New Zealand thing. It is the way of the world, for good or ill.

At times, the Reserve Bank has tried to make a virtue of this “all in one” model. In the wake of the 2008/09 recession, the former Governor Alan Bollard made much of the idea of a “full-service central bank”, very well-positioned to carry out the variety of different functions because they were all located in a single institution. More often, the Bank has pointed out that there is a range of ways of organising these activities, suggesting that no one model is clearly superior.

There is certainly a range of models used in other countries, but once one looks a bit more closely there are also some pretty clear patterns which emerge. Specifically, New Zealand’s current model is out of step with the main stream of advanced countries.

People here often, and naturally, look to Australia. Once upon a time their Reserve Bank and ours had a lot in common in what the institutions were responsible for, and both had evolved through a phase where direct controls had been mostly about monetary policy. But about 20 years ago, the emerging regulatory functions were spun out of the Reserve Bank and a separate Australian Prudential Regulatory Authority (APRA) was established. There has been no sign that the Australian authorities are unhappy with that model, which seems to work well, allowing both the RBA and APRA to concentrate on their own primary areas of responsibility.

There are plenty of advanced country central banks which are responsible for bank supervision. But in most cases now those national central banks are part of the euro-area: they don’t themselves set monetary policy (although each Governor has a vote at the ECB), and would struggle to justify existing as independent entities were it not for the supervisory roles.

But if we look at advanced countries that do have their own monetary policies, I could find only three others – Czech Republic, Israel, and the United Kingdom – in which the same agency is responsible for monetary policy as for prudential supervision. The US is – in this area as so many – a curious hybrid system, in which the Federal Reserve has some – but not remotely all – responsibility for prudential supervision. But as far as I could tell, the following OECD countries have monetary policy and prudential supervision conducted by separate agencies:

Canada, Australia, Norway, Sweden, Korea, Japan, Poland, Chile, Turkey, Mexico, Switzerland, and Iceland

I’m not sure that Turkey or Mexico offer models of governance for New Zealand, but the presence on that list of small well-governed countries like Norway, Sweden and Switzerland – as well as tiny Iceland – gave me pause for thought.

And the more I reflected on the issue, the harder it was to identify good reasons why New Zealand should now stay with the all-in-one model:

- probably the most common argument made is about the possible “synergies” between financial regulatory and monetary policy functions. But there are snyergies, connections, and potentially valuable information overlaps all over the place. Between fiscal and monetary policy for example, and yet we – and every other advanced country – keeps fiscal policy advice and governance quite separate from monetary policy. And I could mount arguments of possible synergies between the Reserve Bank’s financial market activities and the role of the Financial Markets Authority, and yet no one seriously argues for putting the FMA into a mega Reserve Bank. Specialisation, and specialist agencies, has tended to be the way in which advanced country governments have organised themselves (often backed by information-sharing protocols, and effective working relationships across agencies – eg a typical Cabinet paper will reflect perspectives or comments from a range of agencies with relevant perspectives on the topic),

- as it is, the synergies between the monetary policy related functions and the prudential regulatory ones are generally pretty slight – almost vanishingly so in normal times (and there are some conflicts). The timeframes are different, the instruments are different (indirect influence vs direct controls), the required mindsets are different, the Bank’s own financial market operations are typically quite mundane, and its research capability (developed mostly for monetary policy purposes) has rarely been used to produce research around the regulatory or supervisory functions. One of my former colleagues likes to argue that one should conceptualise the Bank’s regulatory role as akin to that of a banker knowing his or her customers, and (eg) maintaining covenants on the credit facilities of those customers. But mostly monetary policy isn’t about lending to banks – and certainly not to insurers or credit unions – and when there is lending involved in monetary policy, the Bank typically seeks to expose itself to minimum credit risk. Crises can be, and are, different – lender of last resort, and provision of emergency liquidity is a core part of a central bank role – but it doesn’t seem to have been an obstacle to other small well-governed countries separating out the monetary policy and regulatory functions into different institutions.

- organisational cohesion and culture are likely to be better-fostered in institutions that have a single main purpose,

- the same goes for the senior leadership of the organisation. 20 years ago it would have been inconceivable that the Governor would be focused primarily on anything other than monetary policy – that was overwhelmingly the Bank’s role – but now it is not so at all, and yet the sort of skills, expertise, and even relationships that might be needed to be responsible for monetary policy – with considerable macroeconomic discretion, and associated accountability, may be quite different from what best suits a regulatory agency. We might well benefit from having both a highly capable macro and markets focused Governor of the (monetary policy) central bank, and the head of a specialised financial regulatory agency.

- governance structures and accountability models would be likely to develop more naturally if the two main functions were structurally separated into different institutions. (And it is more difficult than it should be to hold the Governor effectively to account when he is responsible for two, quite different. big areas of policy).

- Specifically, the Bank’s regulatory activities would quite naturally fit with something much closer to a standard Crown entity sort of model (as with the FMA) – in which key big picture policy matters were decided by the Minister of Finance (with advice from Treasury and the agency), while the Board of the agency was responsible (with operational autonomy) for the implementation of the framework. The monetary policy (and related) functions don’t fit that sort of model, partly because of the inevitable quite substantial degree of policy discretion – and hence need for ongoing transparency and accountability – that are (largely rightly) seen to need to go with monetary policy.

I’ve argued previously that it seems mistake to push ahead with the proposed Stage 1 reforms flowing from the review of the Reserve Bank Act, without first completing an overall review of how the functions the Bank currently undertakes should best be organised, governed and held to account.

And so here is my model:

- the Reserve Bank becomes responsible for the conduct of monetary policy (and directly associated functions – interbank settlement, notes and coins, foreign reserves management. In my post on Monday I outlined how I would establish a statutory Monetary Policy Committee. The same people, appointed the same way, would comprise the Board of the Reserve Bank, and would be responsible for all the functions of the Reserve Bank. Specific statutory provisions – of the sort outlined in Monday’s post – would cover them when meeting as the Monetary Policy Committee. Note that this model would also increase the chances that the executive members of the Monetary Policy Committee would be genuine experts in the area, devoting of their time and energy to monetary policy,

- a New Zealand Prudential Regulatory Agency – parallel to APRA – would be established to take responsibility for the regulatory and supervisory functions the Bank currently has (but with a revision and streamlining of powers, so that major policy framework decisions are once again matters for the Minister of Finance). There is a variety of possible structures. A typical Crown entity would have a non-executive Board responsbile for the institution, employing a chief executive to run the day to say organisation, generate advice, and implement the policies of the Board. But a small executive Board (akin to APRA) is an alternative approach.

- perhaps the (formal) establishment of a Financial System Council, with representation from the Reserve Bank, the NZPRA, and the FMA, to offer advice – perhaps especially systemic advice – to relevant ministers.

There is no role in this model for anything like the current Reserve Bank Board. That Board is almost totally useless, and I’m not aware of anyone who thinks it adds value. In many ways that isn’t surprising. The Board was designed as agent for the Minister and the public holding the Governor to account, in particular for his conduct of monetary policy (but also for his more general stewardship). It isn’t a model found anywhere else in the New Zealand public sector, and for good reason. The Reserve Bank Board has no independent resources, it meets at the Reserve Bank, its Secretary is a senior Reserve Bank manager, and the Governor himself sits on a Board whose prime purpose is to hold the Governor to account. It is a highly successful recipe for “duchessing”: the Board comes to see itself more as part of the Reserve Bank, acting to defend the Bank and the Governor, lulled by all the smart people who present to it (and with few/no formal powers), rather than as some sort of independent source of scrutiny or critical analysis.

Part of the failure is structural – the system was set up in a way that meant it would almost inevitably fail (at least once monetary policy was conceived of as anything other than mechanical, and once the functions broadened out) – but that doesn’t remove responsibility from the people (often otherwise quite able) who have served on the Board over the years. In the 15 years the Board has been required to publish Annual Reports – which, bad sign, they choose to publish buried in the midst of the Governor’s Annual Report – they have never once made even a slightly critical or sceptical comment about the performance of the Governor or Bank, on policy or other areas of performance. Disgracefully, they stood by silently while Graeme Wheeler and his senior management tried to silence Stephen Toplis’s criticism – and, of course, they cheered on Wheeler’s public attack on me when I drew the Bank’s attention to an apparent leak of an OCR decision. They serve no useful function, and should be disbanded as part of the current review, and amended legislation.

Of course, that doesn’t mean there is a reduced need for scrutiny and accountability. My point about the Board is that, in effect, over almost 30 years they simply haven’t served that role – they just function as a department of the Bank, protectors of the insiders. Effective accountability doesn’t really involve the power to fire – or to recommend dismissal – the main formal accountability power the Board has: no Governor (or MPC member) will ever be fired for policy-incompetence related cause during their term (and nor should they be), and the same goes (and should) for independent financial regulators. But reappointment is another matter altogether. And much about accountability is the quality of the questions, the bringing to bear of alternative perspectives etc. The new government has proposed – in fact promised before the election, although nothing has been heard of it since – to establish a Fiscal Council, to help provide genuinely independent scrutiny of fiscal policy and associated analysis. I’ve argued previously – and repeat the call today – that this new entity should actually be set up as a Macroeconomic Review Council, responsible for independent scrutiny (published reports etc) on fiscal policy, monetary policy, and systemic financial regulatory policy. Operating at arms-length from all the agencies – Treasury, Reserve Bank, NZPRA, and FMA – and not resourced by them, it would have a better chance of making a material contribution than the Reserve Bank Board has done, and could help promote scrutiny and associated debate.

A little anecdote of how the Reserve Bank’s Board seems to allow itself to be subsumed into the Bank

A month or so ago I lodged an Official Information Act request with the Reserve Bank’s Board – explicitly asking for it to be delivered to the Board chair – asking them

- how many OIA requests the Board had received in 2016 and 2017, and

- for copies of the Board’s policies and procedures for handling OIA requests.

It seemed to be a pretty straightforward request. The Board is, after all, statutorily distinct from the Bank, is required to publish its own Annual Report, and (in my experience) had good, well-filed, sets of Board papers. With a new emphasis from SSC on agencies reporting on performance with OIA requests, I felt sure it would be an easy request to answer. At most, surely, counting the number of OIA requests might require a quick flick through, say, 10 sets of minutes for each year. I guess I also – naively – assumed that, with the current review underway, the Board would be keen to demonstrate the independent way in which it operated.

More fool me.

A couple of weeks ago, I had a response from one Roger Marwick in the Reserve Bank’s Communications Department telling me that under the Reserve Bank’s charging policy – note nothing about the Board – they would want to charge for this information, but noting that I might be able to reduce the charges by narrowing the scope of my request.

So I asked them what the cost would be if I simply restricted the request to the number of OIA requests. And Mr Marwick responded that it would make no difference because all the costs were associated with that limb of the request.

So I then went back to him – this was 12 days ago now – suggesting that if that was the case, I presumed he could now provide me with the Board’s policies and procedures (since he’d just told me that all the costs were associated with the other limb of the original request.

I’ve heard nothing more since. Last Friday, I went back to Mr Marwick and specifically asked for clarification as to whether the Board was refusing to release the policies and procedures, or were still considering the matter (as fast as reasonably practicable – the statutory standard). And again, I’ve heard nothing more. My suspicion is that there are no Board policies and procedures for handling OIA requests, and that even though the Board’s whole role is to operate at arms-length from the Bank, holding it to account, they’ve just made themselves part of the institution, and left the same management they are paid to hold to account to handle such things. And, clearly, have no interest themselves in the number or nature of requests being made of them.

In short, they are useless and ineffectual, at least for anything other than giving cover to the Governor. But perhaps it shouldn’t really be surprising: this was the same Board that, on the basis of their own disclosed papers, doesn’t even comply with such basic requirements of good public sector governance as the Public Records Act.

UPDATE: A day after posting this, I had an email from the Reserve Bank backing down. I have now been provided with the number of OIA requests made to the Board, and a copy of the Bank’s policies for handling OIA requests, with this observation

requests addressed to the Board are processed in the same way as those addressed to any other part of the Bank. The policy for handling OIA requests addressed to the Board is the same as the Reserve Bank’s policy. In the case of OIA requests made of the Board, the Bank informs and consults the Chair on the requests, and the Chair informs the Bank of the preferred response.

But since the decision to waive charges – and thus avoid an appeal to the Ombudsman – is described as having been made by the Bank, not the Board, I think it largely serves to illustrate my point, that the Board works hand in glove with management rather than serving as an sort of independent check on them.

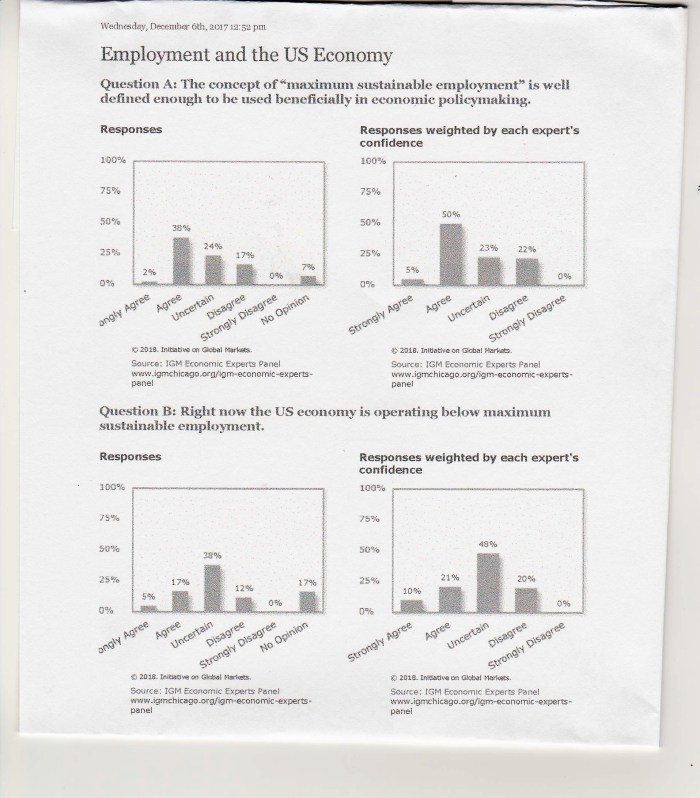

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.