All sorts of items of public spending have attracted attention since March 2020 when the Covid-related spending really began. Some of the things money has been spent on – the wage subsidy for example – were large but necessary and appropriate. Some things, often quite small in scale, were pure waste. Others were dressed up under a Covid label but were really just poor-quality (but quite large scale) spending.

One of the items that has had almost no attention is the huge losses that have resulted from the Reserve Bank’s Large Scale Asset Purchase (LSAP) programme. I guess it is a bit harder to report on, since neither the Bank nor the government puts out press releases boasting of losing $4bn or so.

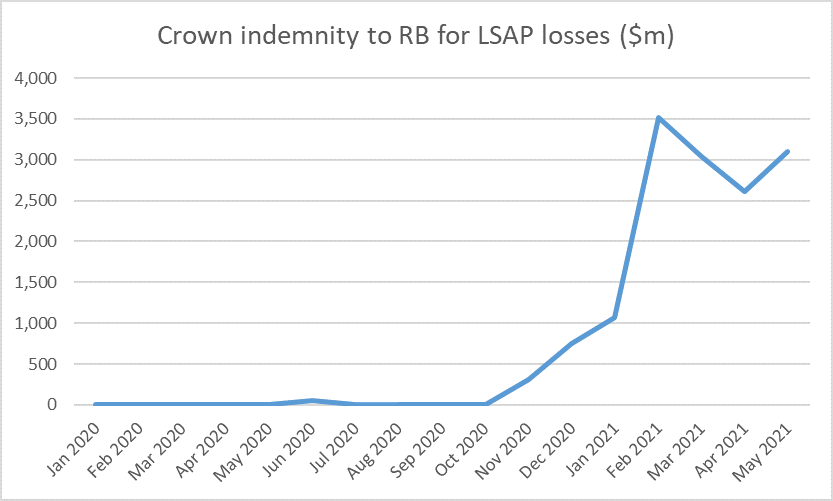

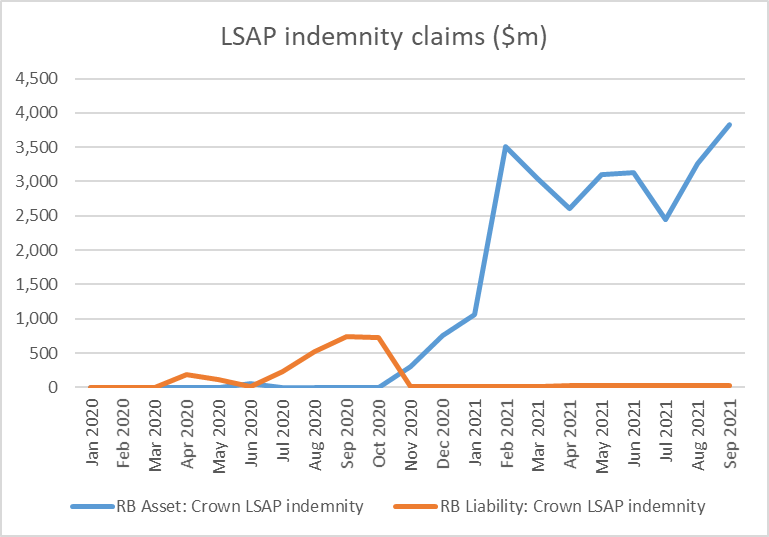

The government has, with no parliamentary authorisation or scrutiny, agreed to idemnify the Reserve Bank for any losses it incurs on the LSAP. That, at least, has the merit of encouraging/requiring some transparency. On the Reserve Bank’s balance sheet there are two line items, show in this chart

To be honest, I’m not quite sure what the orange line is, since as I read the indemnity the liability is one-way only (Crown pays Bank if Bank loses) but it looks like it may reflect periods early on when the LSAP bonds were valued at more than they had been purchased at (lower yields than is). In any case, it is irrelevant now as the remaining number is tiny. The blue line – the Bank’s claim on the Crown – is where the focus should be. That claim was almost $4 billion at the end of September, and nominal yields have risen further this month.

Since the Bank discloses all its purchases, in principle someone could go through and identify the losses on each and every purchase undertaken over the period (more than a year) that purchases were undertaken. But for our purposes here, suffice to say that government bond yields are a lot higher than they were. Here are few medium-long term government bond yields

Recalling that bond prices move inversely with yields, September/October last year would have been a great time to have been selling bonds (top of the market and all that). But the Reserve Bank went right on buying more bonds (albeit at a slower pace), all of which will now be valued at less than the Bank paid for them. They were still buying (lossmaking) government bonds right through the June quarter – when core inflation was already above the target midpoint, and unemployment was back at pre-Covid levels – not finally stopping the purchases until mid-July.

Accounting for the LSAP isn’t simple. In some quarters, there is a tendency to say “well, since the bonds are (almost) all government bonds and the Bank is owned by the government it is all a wash, and nobody is any the worse off”. That is simply wrong, as I will demonstrate shortly.

But it is also wrong to simply look at the indemnity claim (blue line in the first chart above). If all the bonds were held to maturity – in some cases 19.5 years from now – the indemnity claim would come back closer towards zero (since, whatever the market value of a bond now, eventually it will pay the full face value). But it would also be quite wrong to deduce from that correct observation that if only the bonds are held long enough no one is any worse off. Bottom-drawing doesn’t address the issue. (It is worth noting that a few of the bonds the Bank purchased have already matured).

Instead, we need to think about what difference has been made to the overall Crown finances as a result of the independent choices of the Reserve Bank and its Monetary Policy Committee. Assume the rest of the government would have made exactly the same choices they did – spending, taxes, bond and Treasury bill issuance- and assess the marginal financial impact of the Bank’s choices and actions.

The government, of course, did quite a lot of spending and quite a lot of borrowing through the course of the Covid crisis. The Reserve Bank publishes tables of the monthly influences on settlement cash (deposits banks hold at the Reserve Bank). There is a weirdly long lag (for data which really should be available next day), but for illustrative purposes between March 2020 and August this year the government issued domestic debt (bonds and bills) on market, net of maturities, that raised $73.2 billion of cash. Over the same period, its cash outgoings exceeded cash revenue by $33.6 billion. In other words, the government issued a great deal more debt than the net spending it needed to fund. As a result, the balance in the government’s account at the Reserve Bank went up sharply. The balance used to be kept just modestly positive, but this is how things have unfolded since the start of last year.

Mostly the government issued so much debt because it expected to need the cash. Tax revenue came in a lot stronger than the fiscal forecasts had allowed, as the economy rebounded more strongly than forecast (and inflation came in stronger than forecast). But the debt issuance plans were about fiscal policy. As it happens, the Crown ended up issuing a lot of debt earlier than it needed to, at yields that were mostly attractive. The gain to the taxpayer arises from the fact that the bonds were issued last year at, say, 0.5 per cent rather than this year (or next year?) at 2 per cent.

But as far as the Reserve Bank was concerned, all that was a given.

And, incidentally, it is also why a large part of the huge increase in the size of the Reserve Bank’s balance sheet since Covid began is also a given, largely outside the Bank’s control.

When the government overfunds (raises more than its net outgoings) all else equals that reduces the balances commercial banks hold at the Reserve Bank. The net of tax payments, settlement of bond purchases, and government disbursements results in money flowing from the private sector (who bank with commercial banks) to the Crown.

But when Covid began, aggregate settlement cash balances held by commercial banks were about $7 billion, and had been so for some years. A net $40 billion drain to the Crown (see numbers above) needed to be funded somehow.

In normal times, if there were to be a persistent drain it would typically be countered by (funded by) a large buildup in the stock of short-term Reserve Bank loans to the financial system (typically fx swaps or repurchase agreements. Those loans would be rolled over quite often, until the underlying imbalance (government borrowing more than it needed to) was remedied. Doing so would have been pretty much of a wash all round: the Bank would be paying something like the OCR on the Crown Settlement Account, and earning something close to the OCR on its short-term collateralised loans. There would have been little or no market risk or credit risk (the loans would have been well-collateralised) and short-term interest rates would have been kept near the OCR. Most likely, the Bank would have made a small profit (monopoly provider of settlement cash is a position of some strength).

But nothing like this happened.

Instead, we had the LSAP. Now, to be clear, the LSAP was not launched with the intention of filling a hole in system settlement cash. No doubt at the time the Bank assumed that the government would, more or less, be borrowing as required to fund its own deficit, and that if anything, borrowing might be a bit less than the deficit at least while the programme was scaled up (recalling the global bond market illiquidity pressures in March 2020). The Bank’s primary intention – this isn’t a matter of dispute – was simply to lower market interest rates, buying bonds and driving (as they expected) a long way up aggregate system settlement cash balances. Had the government more or less funded just what it was spending over the last 18-20 months, then all else equal settlement cash balances now would be a lot higher than the $37 billion they were last Friday. Recall too that the Bank changed its policy in March 2020 such that all settlement cash balances – without limit – now earn the OCR (previously there was a quota system in which the Bank really only fully remunerated banks for the balances they “needed” to hold for interbank settlement to operate smoothly).

The intent of the policy was to take a big punt on interest rates (that is why they sought and obtained a Crown indemnity). The intent was to buy tens of billions of dollars of long-term fixed rate bonds to which the counterpart would be tens of billions of floating rate settlement account deposits. The Bank initially expected that all those deposits would be held by banks, but because the government overfunded the real counterpart is now in the much-increased balance in the Crown settlement account. But it was a large scale asset swap, which would turn very costly if bond yields went up rather than down. It represented a staggering amount of market risk, assumed by unelected (and not very accountable officials) on a scale with no precedent in New Zealand central banking history.

Views will differ on whether the LSAP made (or is still making) any material sustained difference to (mainly) long-term government bonds rates, and whether even if so that made (or is making) any material difference to New Zealand macroeconomic outcomes. I’ve been consistently somewhat ambivalent on the former, although my reading of the international experience with QE leaves me fairly sceptical. But since long-term interest rates do not matter in the transmission mechanism here in a way they do in (in particular) the United States – since very few fix mortgages for more than a couple of years, and most corporate borrowing is swapped back to floating – I’ve been consistently sceptical that the bond-buying programme (heavily focused at the long end) was making any material macro difference (the more so once the Bank decided to pay OCR on all settlement cash balances, actively preventing one possible transmission mechanism from working). Even if I did – which I do not concede at all – that usefulness ended long ago now (given what we know of the subsequent inflation outcomes and the push to raise the OCR quite aggressively now).

Whatever useful macro impact the Bank might sought last year – simply exploring the hypothetical – could as readily have been achieved by cutting the OCR further, including into modestly negative territory. And using that mechanism would not have involved big financial risks for the taxpayer

And instead now they are stuck with tens of billions of dollars of bonds, many with very long-term maturities, sitting on the Bank’s balance sheet, while the cost of funding (the counterpart liability) looks set to rise quite rapidly further.

In the end, what the MPC has done in effect is to neutralise or reverse the gains the Crown would otherwise have made through the good luck (mostly) of issuing so heavily last year when interest rates were so low, over and above what they were spending then. The Crown will borrow less in the next (more expensive) couple of years and the CSA balance wil no doubt over time be returned to more normal levels. Because more than all the excess bond issuance was, in substance, reversed through the Reserve Bank’s action, bringing tens of billions of long-term bonds back onto the wider Crown balance sheet. If they were to sell the bonds now (or in a scheduled programme over the next couple of years) the loss would be crystallised. That might be a good thing, to help sharpen debate and accountability. But whether the bonds are sold back now or held to maturity, the loss has already occurred. (This is not to say that rates might not go lower – perhaps even much lower – again in future, but that is just another bet at the expense of taxpayers, and no more likely than that bond yields rise further from here, deepening our (taxpayers’) losses.

But it as well to keep the choices by two parts of government separate, reflecting the different sets of decisionmakers. In borrowing as it did (and probably largely by luck re the revenue rebound) the government’s overfunding programme saved taxpayers a lot of money (for which there is no line item in the government accounts). By contrast, the Reserve Bank’s choices — quite conscious and deliberate ones – have cost the taxpayer a great deal of money.

The LSAP simply was not necessary, and it clearly was not well thought through. If there was an arguable case for some action in March 2020, that need quickly passed, and any bonds purchased then could relatively easily have been offloaded back to the market – probably at a profit (crisis interventions should generally be profitable) – by late last year. One might blame the Minister of Finance for providing the indemnity, but the main responsibility rests with the (supposed) technical experts at the Bank and on the MPC (albeit appointed by Robertson). It has cost us billions of dollars already – a $4bn loss is $800 per man, woman, and child, and most families could think of better things to do with such money – and the Bank now sits with a huge open market risk position, the value of which fluctuates by the day.

Having outlined my story – on which I will welcome comments – it is worth pondering why this hasn’t been an issue elsewhere or previously. A lot of bonds have been purchased by central banks in the decade after the 2008/09 crisis. Most likely there will have been two reasons. The first may be around transparency. It is great that we have the indemnity claim is reported each month.

But the much bigger factor must surely have been the continuing decline in global bond yields over the decade. This chart shows long-term bond yields for some of the more significant places where central banks reached effective lows on policy interest rates and engaged in large-scale asset purchases.

When yields just keep trending downwards, having built up a portfolio of long-term bonds is (a) profitable, and (b) much less likely to be controversial. Who knows how much this was a subconscious backdrop to Reserve Bank (and Treasury/Minister) thinking here.

Finally, throughout this post I have treated government and Reserve Bank choices are separable and assumed both parties would have done what they did pretty much regardless of what the other did (around debt issuance and bond purchases). That seems sound for the most part, although the extent of the Crown overfunding is such that it is conceivable that without the LSAP – pouring huge amounts in settlement accounts – pressure (including from the Bank) might have mounted on the government to wind back the borrowing programme more aggressively than it did. But even if there is something to that argument, it is unlikely it would have become salient for several months – it took quite a while for the extent of the economic rebound to be fully appreciated, and by that time the bulk of the LSAP purchases had already been done.

As for where to from here, the losses from the LSAP have already occurred – the mark to market estimates largely capture that – but that is no excuse for the Bank continuing to maintain a large open position in the bond market. The bonds can’t be offloaded very quickly, but there is no reason not do so in a steady predictable preannounced way over the next year or two (say $2 billion a month). Given the extent of the CSA balance, there could even be merit in considering a partial government repurchase of the LSAP portfolio (say half of it). Doing that would not change the substance, but would put duration choices around the public debt and overall Crown liabilities back more nearly where they belong, with The Treasury and the Minister of Finance.