A couple of months ago the Institute of Directors approached me about doing a talk to their members in Wellington on monetary policy as it had been conducted by the Reserve Bank over recent times. Somewhat to my surprise, my name had apparently been suggested to them by Alan Bollard.

I gave the talk this morning, and although the date was set ages ago it could hardly have been more timely given the labour market data yesterday, which in a way finally marks the completion of not just the last 18 months’ of monetary policy, but in some ways the last 14 years (for the first time since the 2008/09 recession we have core inflation a little above the Bank’s target midpoint and the unemployment rate back to something that must be close to the NAIRU.

The full text of my remarks, and a few more points I didn’t have time to deliver, are here

Monetary Policy in Covid Times IoD address 5 Aug 2021

What I set out to do was to review how the Bank had done, and what monetary policy had (and hadn’t) contributed over the last 18 months or so. While I was quite critical in places, and headed the overall talk “Should have done better”, I was also willing to defend them, noting that the surge in house prices had little predictably to do with monetary policy, and was neither sought nor desired.

I’m not going to reproduce the full text in this piece, but here are a couple of sections from towards the end

The unemployment rate is now 4 per cent and the inflation rate – the sectoral core measure the Bank tends (rightly) to focus on – is 2.2 per cent. Those are really good outcomes – first time in 10 years that core inflation had crept above the target midpoint. After the last recession it took 10 years to get unemployment back down, not 10 months.

But those outcomes to celebrate aren’t much credit to monetary policy, since when the MPC was setting the policy that was having an effect now they thought their policy was consistent with much worse outcomes.

But where to from here? The MPC has belatedly terminated the LSAP. They really should be ending the Funding for Lending programme, which was explicitly a crisis programme, a stop-gap for when they couldn’t cut the OCR further, and which was not operated on a competitively neutral basis. But more likely the next step is the OCR.

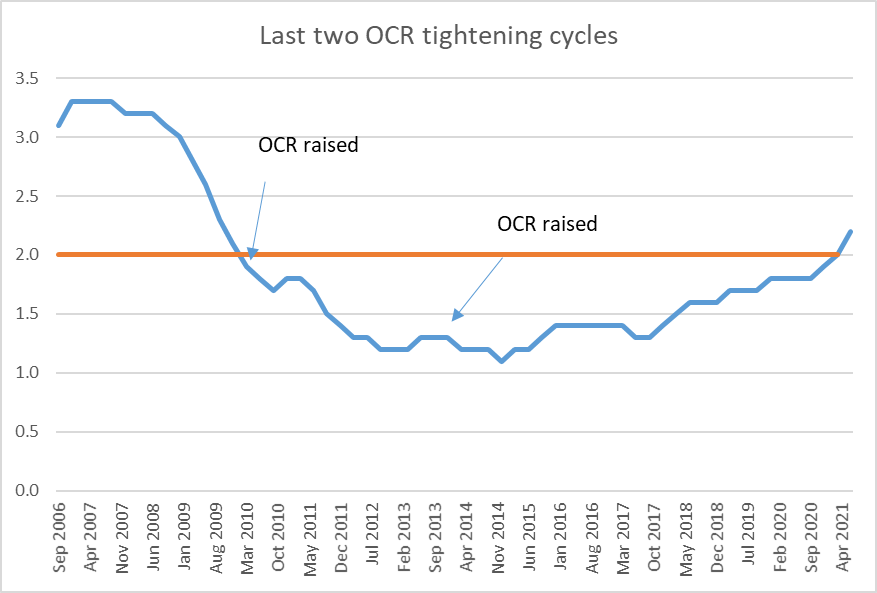

One possible reason for caution is that coming out of the 2008/09 recession, central banks (and markets) were too keen to start getting interest rates back to what was thought of as “normal”. The RBNZ made that mistake twice, and quickly had to reverse themselves. But both times there was no sign of core inflation rising and the unemployment rates were still quite high, so quite different circumstances than we have now.

[Figures 7 and 8]

Some will doubt whether 4.0 per cent is the lowest sustainable rate of unemployment but it is getting pretty close to the cyclical lows of the last two cycles (and some measures may have raised the NAIRU a bit). Wage inflation is rising faster than at any time since 2008, at a time when there is no productivity growth. But the real guide – especially amid considerable ongoing uncertainty – is core inflation itself. If it is above 2 per cent, and no one thinks it is about to drop back, then it is time to start tightening – not necessarily aggressively (there is no harm if core inflation goes a bit higher for a while, as it is likely to do), not part of some predetermined programme, but step by step, review by review, keeping a close eye on fresh data. They need to be tightening at least a bit faster than inflation expectations are rising (on which new data next week). And since the world economy could be derailed again, and fiscal policy (here and abroad) may start tightening, and very long-term interest rates are still at or near multi-decade lows, be ready to stop or reverse course if the data warrant that. The great thing about monetary policy is that when the data change, policy can be altered quickly and easily.

The same can’t be said for fiscal policy. There are plenty of things only government spending can do. For example, income support to those rendered unable to earn because of pandemic restrictions. There are plenty of other programmes for which one might make a careful well-analysed and debated medium-term case for spending taxpayers’ money on. But cyclical stabilisation policy is a quite different matter. Many fiscal programmes are – rightly or wrongly – hard to get underway, and slow to start (many of those “shovel ready” projects), some are easy to start but hard to stop. And almost all involve playing favourites, rewarding one group or another – with other people’s money – according to the political preferences of the particular party in power. Fiscal announceables, once announced, are very hard to take back off the table.

By contrast, the MPC can and does act overnight, it can reverse itself, and it coerces no one, and picks no winners. Market prices shift and people and firms make their own choices whether or not more or less spending is now prudent for them. There has rarely been a better illustration of how much more suited monetary policy is to short-term cyclical stabilisation than the surprises of the last year.

And an overall assessment

How then should we evaluate the MPC’s performance?

It is clear they were poorly prepared. There is really no excuse for that. It was always only a matter of time until the next severe shock came along.

When they finally began to appreciate the severity of the Covid shock their actions were in the right direction.

But they can’t be credited with the good outcomes we are now experiencing – inflation and unemployment – because when policy was being set last year they expected their policy to deliver much worse outcomes, and did nothing about it. We can’t blame them for the economic uncertainty, but they should be accountable for their own official forecasts and what they did with them[1].

The overall contribution of monetary policy to how things have turned out was pretty small. Mostly what has happened was down to private demand reorganising itself and holding up much more than expected – notably by the Bank – greatly reinforced by the really big swing into structural fiscal deficits.

As for monetary policy, the OCR cut was modest, and the exchange rate barely moved. The Bank claimed far too much for the LSAP, which was more noise than substance, and in the process they fed a narrative (“money-printing”) that made trouble for them and the government. If they really believe the LSAP is as potent as they’ve claimed, perhaps they could make a start on tightening by first selling ten billion of bonds back to market.

And if they accomplished little buying lots of long-term bonds at the very peak of the market in the process they have run up big losses. They dramatically shortened the duration of the overall public sector portfolio and then rates went back up. These are real losses – at about $3 billion currently, four times the cost of the Auckland cycling bridge, without even the sightseeing bonuses.

We can’t realistically expect policy perfection but we can and should expect authoritative, open, and insightful communications. But MPC’s communications have been poor:

- They never published the background papers they promised.

- They never explained their weird ‘no OCR change for a year’ pledge.

- There has been no pro-active release of relevant papers (unlike the wider central government approach to Covid).

- They refuse to publish proper minutes – that actually capture the genuine uncertainties and inevitable, appropriate, differences of view, and which would allow individual members to be held to account.

- Little serious research is published, and insightful analytical perspectives are rare.

- From not one of them have we had a single serious and thoughtful speech on how the economy and policy are evolving.

In its first major test, the best grade we could give the MPC “could try harder, needs to avoid other shiny distractions, can’t continue to count on good luck”. Oh, and just as well for them that the individuals aren’t on the hook for those huge losses.

As with so many of our public institutions now, we deserve better.

[1] Note that just under three months ago, in the May Monetary Policy Statement, the MPC unanimously concluded that “medium-term inflation and employment would likely remain below its Remit targets in the absence of prolonged monetary stimulus” going on to note that “it will take time before these conditions are met”.

Those huge losses they have incurred for the taxpayer in running the LSAP – which by their own lights would have been unnecessary if the Bank had been better prepared – have not had much attention. They should. Some are inclined to downplay them on grounds of “think of all the macro good that was done”, but as I argue there is little evidence the LSAP made any useful macroeconomic difference to anything. Others downplay them on the feeble grounds that if the bonds are held to maturity the bond portfolio itself will not realise any losses (bonds are paid out at face value). But we can already see the cash cost to the taxpayer beginning to loom rather directly. The LSAP was simply an asset swap – the Bank bought long-term fixed rate bonds, and issued in exchange variable rate settlement cash deposits, on which it pays the OCR. The strong consensus now is that the OCR is about to rise quite a lot. Even if the OCR rises by 1 per cent and settles there indefinitely, the Bank (taxpayers) will be paying out hundreds of millions a year in additional interest. Of course, it could avoid those payments by selling the bonds back to the market – which it should be doing – but that would simply crystallise the losses on the bonds themselves. The taxpayer is materially poorer for the poor policy and operational choices of the Bank – they could have focused on short-term bonds (which are the maturities that matter in New Zealand), they could have had the banking system ready for negative rates, but instead they choice the flamboyant performative signalling routine of buying huge volumes of long-term bonds at what was (reasonably predictably) close to the very peak of the market. All while accomplishing little or nothing macroeconomically.

In a couple of months we’ll see the last Annual Report from the Bank’s old-style board (to be replaced next year). The Board has spent 31 years providing public cover for management. It is hard to envisage them changing approach at this later date. They really should, but the fact that they almost certainly won’t tells you why it was such a poor governance approach (even if the government’s replacement model if something of, at best, a curate’s egg sort of improvement).

(Circumstances, data, and perspectives do change. Some, but not all, of my views have shifted over the 18 months – as I’m sure everyone else’s has. The text of another lecture on monetary policy and Covid, from last December, is here.)

When was this written Michael?

SOME THOUGHTS ON IMMIGRATION

(In the previous issue Professor Holmes introduced his subject and analyzed the pattern of New Zealand’s immigration. In our next issue the relationship between immigration and economic growth will be examined.)

PART lI

Immigration, Labour Shortages and the Balance of Payments

There has been a great deal of argument about whether more immigration would alleviate or, accentuate labour shortages. Many manufacturers or retailers who are short of staff, and many workers who are worried about competition for their jobs, looking at the problem from the viewpoint of the impact of more workers on their own immediate or short-run future positions, imply in their arguments that immigration must necessarily alleviate the labour shortage. The employer knows that he needs more workers to make more effective use of the plant and equipment which be now has or has planned to install to meet what be gauges to be the likely demand for his products; the worker fears that if the employer succeeds in getting more workers from overseas then the extra labour must mean that his wage packet and fringe benefits will not grow as rapidly as they otherwise would, or worse still, that he will be paid less or even displaced.

Both sets of arguments are based on the impeccable principle that, given demand, if supply increases, price must tend to fall. Unfortunately for those who like to be able to reach conclusions quickly and simply about these things, we cannot assume that demand is unaffected by the increase in the supply of labour, because more workers not only produce more goods and services but also earn and spend incomes, have families and by their actions cause the demand of a variety of agencies in, the community for goods and services to expand, in turn calling for more labour to produce them. What we need to know, in trying to decide whether immigration helps to cure labour, shortages and inflation or not is whether it tends to increase supply more than demand or not.

Now before we go into the theory of the matter, I hope that we can agree that the existence of a labour shortage, along with rising costs and prices and/or balance of payments difficulties, does not necessarily call for an increase in immigration. Give me control of the Government and the Reserve Bank and I can create a Labour shortages easily by rapidly increasing Government expenditures and or giving generous tax concessions. The resultant boost in demand for goods and services would soon have employers competing vigorously with one another for more workers to help them meet it. If we had started with full employment, we should soon have plenty of vacancies, money wages and prices would rise, and there would be a splendid rise in demand for imports. I think that you /might agree that the best cure for that problem might be not more immigration but my replacement by a politician with less generous impulses towards the community.

I hope that you will also agree with me that our experience in New Zealand indicates that a big increase in the supply of labour does not necessarily cure

LikeLike

1966

LikeLiked by 1 person

The RBNZ has been unlawful and should be taken to court. It has not met the purpose of the Act

(1A)

The economic objectives are—

(a) achieving and maintaining stability in the general level of prices over the medium term; and

8Function to formulate monetary policy through MPC

(1) The Bank, acting through the MPC, has the function of formulating a monetary policy directed to the economic objectives of—

(a) achieving and maintaining stability in the general level of prices over the medium term; and

As a former politician recently noted the Act states “general level of prices” not a specific price index.

LikeLike

The Act also provides for a Remit (formerly PTA) in which a more specific index has consistently been specified, incl specific reference to the midpoint of a band for inflation in that index,

On a legal point, I think the Bank could convincingly argue that they formulated a monetary policy directed towards those objectives, even if they did not do that well in achieving the specific goal. The Act focus on the policy choices, bearing in mind that officials cannot with certainty deliver a particular inflation rate in a particular index.

As you know, I have been quite critical of the Bank over the years, but I would strongly defend them against any such legal challenge.

On the other hand, challenges (not judicial) on competence, authority, expertise, accountability etc would command my full support.

LikeLike

“The Act also provides for a Remit (formerly PTA) in which a more specific index has consistently been specified, incl specific reference to the midpoint of a band for inflation in that index”

Yes, agreed, but still the chosen index is not necessarily consistent with the purpose of the Act and thus is challengeable.

LikeLike

It is a longstanding argument. I once wrote a paper (that I was reasonably convinced by) arguing that in fact the specific target was consistent with section 8 provision (as it then was). Given the reluctance of courts to interfere in a matter of technical judgement of that sort I’ve always thought any such challenge – which now would have to be to the Minister (who issues the Remit unilaterally) rather than the Bank had only a trivially small chance of success. The Bank’s view (and my own) has tended to be that an exchange rate target or a nominal GDP target could probably be reconciled with the overarching statutory goal,

LikeLike

I note:

“..The central question is, why are 190,257 people on a Jobseeker benefit when only 117,000 are officially unemployed?”

https://lindsaymitchell.blogspot.com/2021/08/the-conundrum-of-low-unemployment-and.html

I would have (obviously naively) assumed that if you are collecting a jobseeker benefit you would be counted as being unemployed, but apparently not. Has this always been the case?

LikeLike

I think there may have been some changes in classification so that eg people who are sick receive Jobseeker’s Allowance but do not have work requirements. But to be officially unemployed (HLFS) you have to have actively searched for a job (not just skimmed adverts) in the last week and be ready to start work straight away. Also people on the benefit can work a few hours a week without the benefit abating but even 1 hour’s work in a week makes you HLFS employed.

LikeLike

When my wife was unable to work for 6 months due to a severe illness WINZ offered us the choice of applying for Job Seekers benefit with job search suspended because of health or being a dependant on my Superannuation. The latter was better. Last year when my daughter took 9 months off work after childbirth with the first 6 months on half pay she ended up being offered a job seekers benefit of ~$9pw presumably also with job search suspended. The accommodation benefit was fairly generous (because she lives in Auckland). She would have received more total benefit if she hadn’t declared the father as her partner. Her employer was willing to keep her job open for 12 months but she had little choice but to return to work 3 months earlier when she ran out of money. Governments seem to like tinkering and means-testing. I much prefer a universal benefit especially a universal child benefit and if Mr Reddell receives it I don’t mind – the IRD will get it back in taxes.

LikeLiked by 2 people

You comment “If it [core inflation] is above 2 per cent, and no one thinks it is about to drop back, then it is time to start tightening”. I thought the reason given overseas (USA) for not raising rates at the moment is because they think current inflation is just a blip, and it will drop again. Does no one think it is the same in NZ? Is there data that NZ is different?

LikeLike

Operative word in my observation was “core”. I didn’t reference headline inflation at all, precisely because the current peaks are likely to be transitory, and shouldn’t be the focus of policy. The Bank’s sectoral core factor model measure – the series shown in the chart in the post re last two tightening cycles – is quite persistent and designed to strip out one-off types of pressures.

More generally, one big thing that is now different in NZ is the 4% unemployment rate – as low as pre-Covid – and (less certainly) the material pick-up in wage inflation, at a time when productivity growth is probably non-existent.

LikeLiked by 1 person

At face value, it would be easy to conclude that New Zealand faces a significant acceleration in inflation and that, along with tight capacity, means the country must embark on a rapid rate hiking cycle but the picture is more nuanced:

1. Much of the rise in inflation IS transitory,

2. Much of the tightening in capacity pressures are COVID-19 related,

3. The underlying real interest rate in the economy, r*, appears to be very low and may be falling.

Looking at the CPI at a detailed level – 107 sub-components – reveals that much of the rise in CPI can be attributed to temporary factors due to direct effects of COVID-19 (e.g. on restaurants, international airfares, health insurance costs, dental costs), indirect effects on transportation (e.g. used cars), and commodity prices (oil). What we are seeing in these sectors is price-level adjustments and once that adjustment is complete, the inflationary effect will dissipate. Stripping just these components out of the CPI, we see that inflation is not accelerating, and that it’s hovering around the level of the Sector Factor Model, with only a gradual uptrend evident.

While the Banks love to show the charts of the QSBO saying that capacity pressures are tight, it’s apparent that much of the tightness is coming from: 1) the closure of the border, preventing immigrants and migrant workers from coming to NZ (even Kiwis offshore can barely come home), 2) transport and logistics difficulties are leading to supply issues for many products, and: iii) demand was strongly stimulated by last years large-scale fiscal transfer, which ceased in late 2020 with fiscal and monetary conditions becoming progressively more restrictive. Measures of capacity from survey’s are always fraught with difficulty in interpreting and I think there are good reasons for skepticism about them right now.

Finally, given the behavior of the yield curve and in particular the 5y5y IRS, it’s clear r* is currently around zero, and looks to be falling.

Add in the potential scope for a significant lift in mortgage rates coming from higher wholesale rates (which banks have yet to pass through) and elevated household debt levels with marginal borrowers facing significant serviceability constraints, and you have the recipe for only a modest rate hiking cycle.

My bank manager laughed at me when I locked in my commercial loan in January. I got him to reprice it as of today, it’s up 100bp and climbing. Now those same clowns at the local banks are all running around like headless chickens screaming about the sky falling…

Adrian needs to hike rates, but should do so cautiously, crossing the river by feeling the stones.

LikeLiked by 1 person

Thanks Peter. Largely agree, and especially with your final sentence,

For what it is worth, long-term real rates are – as you note – very very low, often negative, and possibly still falling, and despite that market-implied inflation expectations still sit under 2%.

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLiked by 1 person