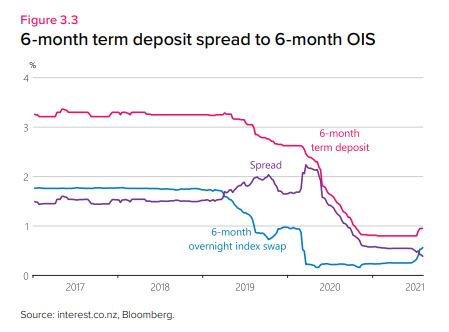

I was, conditionally, sympathetic to the Funding for Lending programme the Reserve Bank put in place late last year. At the time they thought (and it seemed plausible they were right) that more monetary stimulus was needed, and – through their own neglect and incompetence over several years – they asserted that a negative OCR could not yet be implemented. The announcement of the scheme clearly narrowed the gap between wholesale and retail interest rates, lowering the latter. This chart from this week’s MPS is one way of illustrating the point.

The effect was achieved by making it known the scheme was coming, and then available. Relatively little was actually borrowed, especially early in the piece.

The scheme works by offering funding to banks (only) at an interest rate equal to the OCR (floating rate, so the rate changes as the OCR does) for terms of three years. The loans are secured, but that isn’t much of a burden to the banks as (eg) they are allowed to simply bundle up their own residential mortgages into bonds the Reserve Bank will take as security (with a significant haircut – ie the value of the bonds has to exceed the value of the FfL loan).

It was a jerry-built scheme, but one could mount a reasonable third-best argument for having announced and deployed it last year. Among the problems with the scheme from the start:

- it was offered only to registered banks, and not to any other (regulated) deposit-takers (at odds with any notion of competitive neutrality, a principle that for a long time was important to the Bank),

- by focusing on driving down retail rates (rather than both retail and wholesale) then it may have meant the exchange rate staying higher than otherwise,

- lending for a three-year term at a floating OCR rate was, most likely, subsidised funding (it is highly unlikely any bank would have borrowed that cheaply on floating rate terms on market).

But perhaps one could tolerate those problems for a few months, while the negative OCR option was (so they said) not available. And consistent with that I had not been particularly critical of it (even though by the time the scheme was officially deployed – as distinct from announced, and announcement effects mattered – the Bank was also telling us that the negative OCR obstacles had all been sorted out).

All that, of course, was many months ago, back when monetary policy tightenings looked a long way away, and the focus was still more on the risk of unemployment lingering high and core inflation staying very low. The data moves, but the Bank doesn’t – or is very slow to.

Where we stand now – or at least earlier in the week – was that core inflation was (a bit) above the midpoint of the target range, and the unemployment rate was so low even the Bank suggested (by implication) it was now at or below the NAIRU. Tightening monetary conditions is clearly called for, and the Bank’s own numbers suggest they envisage quite a lot of tightening over quite an extended period.

So you might suppose that jerry-built interventions cobbled together late in a crisis would be among the very first things withdrawn. As the Bank’s own document states

The FLP offers secured term central bank funding to registered banks, with the aim of lowering funding costs to stimulate lending growth across the economy and help reduce interest rates for borrowers.

Is the aim of monetary policy any longer to lower funding costs, stimulate lending growth or reduce interest rates? It certainly shouldn’t be, judging by the Bank’s own forecasts and statements.

And yet they insist they are going to keep right on offering the FfL scheme for the next 16 months. It makes no sense.

I was prompted to write this post after reading a Business Desk story this morning by Jenny Ruth. In it we were told that some banks had been borrowing more money this week, including on Wednesday. The amounts involved – $1.5 billion – aren’t huge but (a) the amounts haven’t usually been the issue, and (b) monetary policy works at the margin. But there was also this report of some comments the Governor had apparently made at FEC yesterday in which he ‘described the FLP as “a contract” that the RBNZ won’t break. “We have a clear contract. We thought it was best to honour that. We’re comfortable with honouring that contract,”

This was a new line. When Jenny Ruth had asked the Governor at the press conference on Wednesday about FfL (and selling back LSAP bonds) we were simply given a line about preferring to use understood and predictable tools. And so it prompted me to look up the Reserve Bank’s page on the Funding for Lending scheme.

On my way there I had to pass through a “Tools to support the economy” page, which – still – is full of talk about what the Bank is doing to boost spending, boost jobs, encourage borrowing etc etc. At very least the page needs updating – things have moved on from last year.

The Funding for Lending programme page is here, with operational details here.

And sure enough I found this

Participants may access the funding over a 2-year transaction period. The Bank reserves the right to extend (but not shorten) the transaction period.

Presumably this is what the Governor had in mind when he talked about a “contract”, but it is of course nothing of the sort (unless there are further signed documents the Bank isn’t disclosing, which I doubt). It is a policy programme, much like the LSAP. Recall that the LSAP was originally going to be kept going much longer, but circumstances changed and even the MPC concluded it was time to change policy and stop the bond-buying. It didn’t betray anyone, no one regarded it as a breach of trust or anything of the sort. If the Governor really regards himself (and his Committee) as somehow bound by that two-year period, it is even sillier than that pledge they made last March – when they had no idea what was going on – not to change the OCR for a year come what may.

Now, just to be clear. I am not suggesting that three year loans once made could or should be revoked. The issue here is access to new loans, from a crisis programme, long after the crisis has past, and in a climate when the Bank itself says it expect to tighten steadily over a couple of years.

Does any of this matter? I think it does, for a several reasons:

- the MPC should not be making commitments it regards itself as bound by to periods well ahead where it has no idea what the economic circumstances will be. Perhaps an initial six-month commitment might have been pardonable at launch, but another 16 months from here is simply indefensible.

- since the MPC itself expects to raise the OCR steadily over the next couple of years (conditional of course on the economy) short-term market rates will tend to be above the OCR over that period. Continuing to offer the FfL lending at OCR is not only cheap (subsidised) funding for banks (and recall only banks, not their competitors), but directly tends to undermine the effect of the market-led tightening that is going on. Overnight rates really should apply to overnight money (or least money that reprices overnight not every 6-8 weeks).

- and the longer the scheme runs the more it is likely to conflict with the MPC broader policy intentions. This is so because under the rules from June next year banks can only borrow from the FfL to the extent that they are increasing their lending. Perhaps there was an (arguable at best) policy goal to have banks increase lending this time last year, but on their own numbers and plans there is no such goal next year when (on their numbers) inflation will be near target and unemployment very low. If the scheme continues to have any effect at all it will mean the OCR itself having to be pushed a little higher than otherwise.

The macroeconomic implications are probably pretty small, but it is simply bad policy by the Governor and Committee, grossly inadequately explained (if he really thought they were bound by honour or contract he should have developed the case in the MPS). The FfL scheme served a purpose – although given how the economy recovered more in prospect (from when first flagged) than by the time it became operational. But that time has long past now. The window should be closed, retail rates left to find their own level relative to wholesale rate, and the OCR should be deployed only after this abnormal crisis tool has been suspended.