All sorts of items of public spending have attracted attention since March 2020 when the Covid-related spending really began. Some of the things money has been spent on – the wage subsidy for example – were large but necessary and appropriate. Some things, often quite small in scale, were pure waste. Others were dressed up under a Covid label but were really just poor-quality (but quite large scale) spending.

One of the items that has had almost no attention is the huge losses that have resulted from the Reserve Bank’s Large Scale Asset Purchase (LSAP) programme. I guess it is a bit harder to report on, since neither the Bank nor the government puts out press releases boasting of losing $4bn or so.

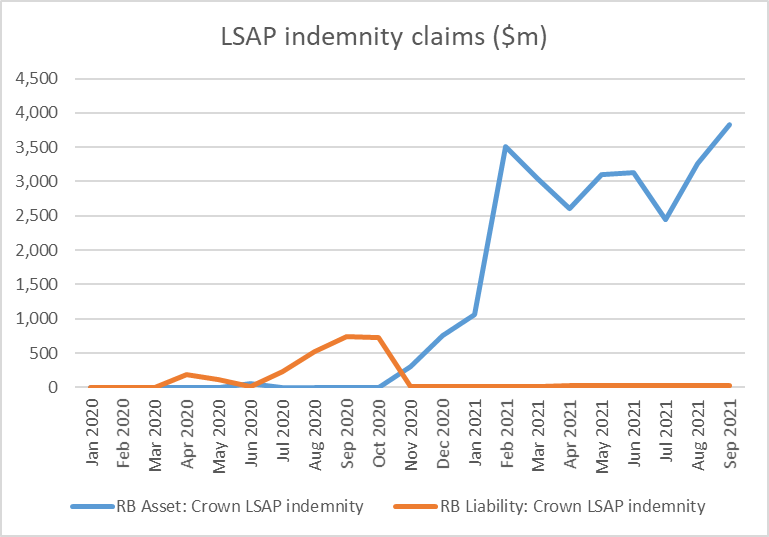

The government has, with no parliamentary authorisation or scrutiny, agreed to idemnify the Reserve Bank for any losses it incurs on the LSAP. That, at least, has the merit of encouraging/requiring some transparency. On the Reserve Bank’s balance sheet there are two line items, show in this chart

To be honest, I’m not quite sure what the orange line is, since as I read the indemnity the liability is one-way only (Crown pays Bank if Bank loses) but it looks like it may reflect periods early on when the LSAP bonds were valued at more than they had been purchased at (lower yields than is). In any case, it is irrelevant now as the remaining number is tiny. The blue line – the Bank’s claim on the Crown – is where the focus should be. That claim was almost $4 billion at the end of September, and nominal yields have risen further this month.

Since the Bank discloses all its purchases, in principle someone could go through and identify the losses on each and every purchase undertaken over the period (more than a year) that purchases were undertaken. But for our purposes here, suffice to say that government bond yields are a lot higher than they were. Here are few medium-long term government bond yields

Recalling that bond prices move inversely with yields, September/October last year would have been a great time to have been selling bonds (top of the market and all that). But the Reserve Bank went right on buying more bonds (albeit at a slower pace), all of which will now be valued at less than the Bank paid for them. They were still buying (lossmaking) government bonds right through the June quarter – when core inflation was already above the target midpoint, and unemployment was back at pre-Covid levels – not finally stopping the purchases until mid-July.

Accounting for the LSAP isn’t simple. In some quarters, there is a tendency to say “well, since the bonds are (almost) all government bonds and the Bank is owned by the government it is all a wash, and nobody is any the worse off”. That is simply wrong, as I will demonstrate shortly.

But it is also wrong to simply look at the indemnity claim (blue line in the first chart above). If all the bonds were held to maturity – in some cases 19.5 years from now – the indemnity claim would come back closer towards zero (since, whatever the market value of a bond now, eventually it will pay the full face value). But it would also be quite wrong to deduce from that correct observation that if only the bonds are held long enough no one is any worse off. Bottom-drawing doesn’t address the issue. (It is worth noting that a few of the bonds the Bank purchased have already matured).

Instead, we need to think about what difference has been made to the overall Crown finances as a result of the independent choices of the Reserve Bank and its Monetary Policy Committee. Assume the rest of the government would have made exactly the same choices they did – spending, taxes, bond and Treasury bill issuance- and assess the marginal financial impact of the Bank’s choices and actions.

The government, of course, did quite a lot of spending and quite a lot of borrowing through the course of the Covid crisis. The Reserve Bank publishes tables of the monthly influences on settlement cash (deposits banks hold at the Reserve Bank). There is a weirdly long lag (for data which really should be available next day), but for illustrative purposes between March 2020 and August this year the government issued domestic debt (bonds and bills) on market, net of maturities, that raised $73.2 billion of cash. Over the same period, its cash outgoings exceeded cash revenue by $33.6 billion. In other words, the government issued a great deal more debt than the net spending it needed to fund. As a result, the balance in the government’s account at the Reserve Bank went up sharply. The balance used to be kept just modestly positive, but this is how things have unfolded since the start of last year.

Mostly the government issued so much debt because it expected to need the cash. Tax revenue came in a lot stronger than the fiscal forecasts had allowed, as the economy rebounded more strongly than forecast (and inflation came in stronger than forecast). But the debt issuance plans were about fiscal policy. As it happens, the Crown ended up issuing a lot of debt earlier than it needed to, at yields that were mostly attractive. The gain to the taxpayer arises from the fact that the bonds were issued last year at, say, 0.5 per cent rather than this year (or next year?) at 2 per cent.

But as far as the Reserve Bank was concerned, all that was a given.

And, incidentally, it is also why a large part of the huge increase in the size of the Reserve Bank’s balance sheet since Covid began is also a given, largely outside the Bank’s control.

When the government overfunds (raises more than its net outgoings) all else equals that reduces the balances commercial banks hold at the Reserve Bank. The net of tax payments, settlement of bond purchases, and government disbursements results in money flowing from the private sector (who bank with commercial banks) to the Crown.

But when Covid began, aggregate settlement cash balances held by commercial banks were about $7 billion, and had been so for some years. A net $40 billion drain to the Crown (see numbers above) needed to be funded somehow.

In normal times, if there were to be a persistent drain it would typically be countered by (funded by) a large buildup in the stock of short-term Reserve Bank loans to the financial system (typically fx swaps or repurchase agreements. Those loans would be rolled over quite often, until the underlying imbalance (government borrowing more than it needed to) was remedied. Doing so would have been pretty much of a wash all round: the Bank would be paying something like the OCR on the Crown Settlement Account, and earning something close to the OCR on its short-term collateralised loans. There would have been little or no market risk or credit risk (the loans would have been well-collateralised) and short-term interest rates would have been kept near the OCR. Most likely, the Bank would have made a small profit (monopoly provider of settlement cash is a position of some strength).

But nothing like this happened.

Instead, we had the LSAP. Now, to be clear, the LSAP was not launched with the intention of filling a hole in system settlement cash. No doubt at the time the Bank assumed that the government would, more or less, be borrowing as required to fund its own deficit, and that if anything, borrowing might be a bit less than the deficit at least while the programme was scaled up (recalling the global bond market illiquidity pressures in March 2020). The Bank’s primary intention – this isn’t a matter of dispute – was simply to lower market interest rates, buying bonds and driving (as they expected) a long way up aggregate system settlement cash balances. Had the government more or less funded just what it was spending over the last 18-20 months, then all else equal settlement cash balances now would be a lot higher than the $37 billion they were last Friday. Recall too that the Bank changed its policy in March 2020 such that all settlement cash balances – without limit – now earn the OCR (previously there was a quota system in which the Bank really only fully remunerated banks for the balances they “needed” to hold for interbank settlement to operate smoothly).

The intent of the policy was to take a big punt on interest rates (that is why they sought and obtained a Crown indemnity). The intent was to buy tens of billions of dollars of long-term fixed rate bonds to which the counterpart would be tens of billions of floating rate settlement account deposits. The Bank initially expected that all those deposits would be held by banks, but because the government overfunded the real counterpart is now in the much-increased balance in the Crown settlement account. But it was a large scale asset swap, which would turn very costly if bond yields went up rather than down. It represented a staggering amount of market risk, assumed by unelected (and not very accountable officials) on a scale with no precedent in New Zealand central banking history.

Views will differ on whether the LSAP made (or is still making) any material sustained difference to (mainly) long-term government bonds rates, and whether even if so that made (or is making) any material difference to New Zealand macroeconomic outcomes. I’ve been consistently somewhat ambivalent on the former, although my reading of the international experience with QE leaves me fairly sceptical. But since long-term interest rates do not matter in the transmission mechanism here in a way they do in (in particular) the United States – since very few fix mortgages for more than a couple of years, and most corporate borrowing is swapped back to floating – I’ve been consistently sceptical that the bond-buying programme (heavily focused at the long end) was making any material macro difference (the more so once the Bank decided to pay OCR on all settlement cash balances, actively preventing one possible transmission mechanism from working). Even if I did – which I do not concede at all – that usefulness ended long ago now (given what we know of the subsequent inflation outcomes and the push to raise the OCR quite aggressively now).

Whatever useful macro impact the Bank might sought last year – simply exploring the hypothetical – could as readily have been achieved by cutting the OCR further, including into modestly negative territory. And using that mechanism would not have involved big financial risks for the taxpayer

And instead now they are stuck with tens of billions of dollars of bonds, many with very long-term maturities, sitting on the Bank’s balance sheet, while the cost of funding (the counterpart liability) looks set to rise quite rapidly further.

In the end, what the MPC has done in effect is to neutralise or reverse the gains the Crown would otherwise have made through the good luck (mostly) of issuing so heavily last year when interest rates were so low, over and above what they were spending then. The Crown will borrow less in the next (more expensive) couple of years and the CSA balance wil no doubt over time be returned to more normal levels. Because more than all the excess bond issuance was, in substance, reversed through the Reserve Bank’s action, bringing tens of billions of long-term bonds back onto the wider Crown balance sheet. If they were to sell the bonds now (or in a scheduled programme over the next couple of years) the loss would be crystallised. That might be a good thing, to help sharpen debate and accountability. But whether the bonds are sold back now or held to maturity, the loss has already occurred. (This is not to say that rates might not go lower – perhaps even much lower – again in future, but that is just another bet at the expense of taxpayers, and no more likely than that bond yields rise further from here, deepening our (taxpayers’) losses.

But it as well to keep the choices by two parts of government separate, reflecting the different sets of decisionmakers. In borrowing as it did (and probably largely by luck re the revenue rebound) the government’s overfunding programme saved taxpayers a lot of money (for which there is no line item in the government accounts). By contrast, the Reserve Bank’s choices — quite conscious and deliberate ones – have cost the taxpayer a great deal of money.

The LSAP simply was not necessary, and it clearly was not well thought through. If there was an arguable case for some action in March 2020, that need quickly passed, and any bonds purchased then could relatively easily have been offloaded back to the market – probably at a profit (crisis interventions should generally be profitable) – by late last year. One might blame the Minister of Finance for providing the indemnity, but the main responsibility rests with the (supposed) technical experts at the Bank and on the MPC (albeit appointed by Robertson). It has cost us billions of dollars already – a $4bn loss is $800 per man, woman, and child, and most families could think of better things to do with such money – and the Bank now sits with a huge open market risk position, the value of which fluctuates by the day.

Having outlined my story – on which I will welcome comments – it is worth pondering why this hasn’t been an issue elsewhere or previously. A lot of bonds have been purchased by central banks in the decade after the 2008/09 crisis. Most likely there will have been two reasons. The first may be around transparency. It is great that we have the indemnity claim is reported each month.

But the much bigger factor must surely have been the continuing decline in global bond yields over the decade. This chart shows long-term bond yields for some of the more significant places where central banks reached effective lows on policy interest rates and engaged in large-scale asset purchases.

When yields just keep trending downwards, having built up a portfolio of long-term bonds is (a) profitable, and (b) much less likely to be controversial. Who knows how much this was a subconscious backdrop to Reserve Bank (and Treasury/Minister) thinking here.

Finally, throughout this post I have treated government and Reserve Bank choices are separable and assumed both parties would have done what they did pretty much regardless of what the other did (around debt issuance and bond purchases). That seems sound for the most part, although the extent of the Crown overfunding is such that it is conceivable that without the LSAP – pouring huge amounts in settlement accounts – pressure (including from the Bank) might have mounted on the government to wind back the borrowing programme more aggressively than it did. But even if there is something to that argument, it is unlikely it would have become salient for several months – it took quite a while for the extent of the economic rebound to be fully appreciated, and by that time the bulk of the LSAP purchases had already been done.

As for where to from here, the losses from the LSAP have already occurred – the mark to market estimates largely capture that – but that is no excuse for the Bank continuing to maintain a large open position in the bond market. The bonds can’t be offloaded very quickly, but there is no reason not do so in a steady predictable preannounced way over the next year or two (say $2 billion a month). Given the extent of the CSA balance, there could even be merit in considering a partial government repurchase of the LSAP portfolio (say half of it). Doing that would not change the substance, but would put duration choices around the public debt and overall Crown liabilities back more nearly where they belong, with The Treasury and the Minister of Finance.

To what extent were the bonds issued by the Treasury purchased (directly or indirectly) by the RB?

It does seem that the purpose of the LSAP was at least to take pressure off the bond market – reflecting any concerns that the volume of TY issues might cause a rise in market rates (a natural response to Govt deficit financing, but a politically unpalatable outcome). Higher market rates, while consistent with Government deficit financing and an expansionary signal from the RB lowering the OCR, would be unappealing to house buyer/voters seeking to take advantage of lower mortgage rates…

I agree that the economic effect of the LSAP was limited at best, and consider that supporting or encouraging the Govt to borrow at low rates encouraged and supported a degree of profligacy and wasteful spending ignoring traditional cost/benefit analysis and real economic opportunity costs. I doubt that they are losing any sleep over the mere $4bn on the books.

LikeLiked by 1 person

On your question in the first para, they were all purchased on market. Of course, as you suggest the Bank’s presence in the market may have lowered market bond rates a bit, easing selling conditions for DMO, altho I’m sceptical as to how large that effect was, since (say) 5-7 years rate this time last year don’t look extraordinarily low given market views then about how low the OCR might go and how long it might stay v low.

LikeLiked by 1 person

I have come to realise that economists can’t read a Balance Sheet. From RBNZ Balance Sheet, this is how the transactions would have likely occurred.

Step 1. RBNZ buys $54 billion of Crown bonds from the market and paid a market premium of $59 billion.

The intent is to clear the market of shorter term Crown bonds. This in effect allows the government to issue new longer bonds which the market can buy from the Crown. The effect of paying $5 billion delivered a record 30% uplift in bank profits.

Step 2. RBNZ books the entry Dr LSAP asset $59 billion and Cr Market Settlement Cash Account liability $59 billion.

The RB did not pay for the purchase of the bonds with cash. Instead the RB created a book entry to record an IOU settlement cash with the market. The impression was given that Settlement Cash was paid to the market. But no actual cash was paid out. It was an adjusting book entry to Credit the Market Settlement cash account. The effect is an IOU Market Settlement cash of $59 billion.

Step 3. The RB having cleared the Market of short dated Crown bonds, this allowed the Crown to issue or sell new longer term bonds of $59 billion back to the market. The effect of which would have meant that the Crown has a fighting fund of $59 billion cash for its Covid fighting fund.

Step 4. The Crown spend $21 billion on wage subsidies and other covid projects. And transfers $38 billion to the RB. In effect paying off the RB IOU to the market. The entries are Dr Market Settlement Cash liability and Cr Crown Settlement Account

Most economists understood the Crown Settlement Account to be cash available for the Crown to draw on. However this is only possible if the RB has cash assets which it is clear the RB does not have cash assets to pay outv$38 billion on the Crown Settlement Account. The largest asset is the $59 billion in Crown Bonds.

What all this means is that what was originally planned as a $100 billion QE ended up being a $21 billion QE. The Crown paid off the RB debt to the tune of $38 billion via the Crown Settlement Account. It is no wonder that the Crown is scrambling to reopen level 3 with picnics, takeaways and construction. What Grant Robertson thought was cash that he could draw on from RB turned out to be RB debt repaid and cannot be drawn on to spend. The NZ QE must be the funniest QE in the world. A barrel of laughs.

LikeLiked by 1 person

The cost of RB QE is already known. The RB paid $59 billion to buy $54 billion in Crown Bonds. The effective QE is not $59 billion but only $21 billion as the Crown paid off $38 billion of RB liability owed to the Market via the Crown Settlement Account. The known cost upfront is $5 billion for only $21 billion of QE. The $4 billion in Crown indemnity on LSAP is an additional cost, likely due to interest payable of 0.25% on the Market Settlement Cash IOU of $21 billion plus a devaluation in the bonds.

I would read the cost of the LSAP as $9 billion for a $21 billion QE.

LikeLiked by 1 person

The RBNZ Balance Sheet is actually quite easy to read but there are a few confusing items.

1. Crown indemnity on LSAP of $4 billion

We know interest of 0.25% is payable to the market on the Market Settlement Cash liability account. But the amount is too large. I have attributed to bond devaluation but at the time interest rates was still expected fall. So my thinking is moving towards shorter term Crown Bonds ie between 1 year to 5 year bonds maturing. This could also explain why the Crown paid off RB debt in the Market Settlement Cash liability account of $38 billion which created the Crown Settlement Account of $38 billion. The RB bought up Crown bonds from the market with much shorter maturing terms perhaps between 1 year to 20 year maturing bonds. Still a thought in progress.

2. Funding for Lending of $5 billion actual but $28 billion on offer at 0.25%

I came to realise this narrative did not make much financial sense because the RB has no cash investments to promise $28 billion loans to the banks. Its only significant asset are those $59 billion LSAP Crown bonds. This must be an offset loan because the RB still owes $21 billion after crown paid off $38 billion to enable the purchase of $59 billion of Crown bonds from the market. That is why RB can’t get rid of FLP. It was negotiated at the time it bought $59 billion of Crown bonds. The interest rate of 0.25% on FLP was a giveaway clue. It matches the Market Settlement Cash liability Account interest payable which is also 0.25%.

LikeLike

Hi Michael,

Nice article today, particularly clarifying that the LSAPs are not a free lunch in a whole-of-government sense. The way I think about is: (1) the government can issue bonds to the private sector and pay interest directly over the lift-time of the bond; or (2) if the RBNZ then buys the bonds from the private sector, the bond interest essentially cancels out but the RBNZ pays the path of the realized OCR to the private sector over the lift-time of the bond. Either way, there is an actual interest cost to pay for the government borrowing.

And I’ve also enjoyed some of your more recent posts on inflation and monetary policy.

I thought I would take this opportunity to ask two questions that you should be able to help me with:

First, did you know if the RBNZ ever provided a basis for the unconstrained OCR that it used from May 2020 to February 2021 (e.g. $x billion and/or y%GDP of LSAPs are equivalent t0 z bps of the OCR? I suspect not, because I haven’t seen anything myself, but I just thought I would double-check with you. (Just to be clear, I know that the RBNZ published the uOCR with the intention of showing the amount of stimulus it wanted – from the May 2020 MPS:

We have opted to publish an unconstrained OCR (figure

2.8). This demonstrates the broad level stimulus needed to achieve the

Reserve Bank’s monetary policy objectives, much like the OCR projection

demonstrated in the past.

The Monetary Policy Committee intends to use the unconstrained OCR

outlook as a basis on which to form its monetary policy decisions. A range

of monetary policy instruments, including Large Scale Asset Purchases,

can be used to generate this level of stimulus and it does not necessarily

represent a negative OCR. Fiscal policy could also provide further stimulus

if needed to underpin domestic demand.

But I don’t think it ever commented on whether the stimulus from unconventional monetary policy actually achieved a given OCR equivalent.)

Second, if the RBNZ hasn’t already publicly commented as above, I had thought about writing an OIA to seek the information. You have lots of experience in such matters, so I would appreciate if you be able to give me the relevant steps (or shall I just check out one of your back posts for an example?).

The background to my questions is that I’m writing a note on the RBNZ UMP cycle relative to others. My analysis shows that New Zealand had the deepest cycle (and now steepest exit) relative to the other six economies that I track.

Cheers, Leo

LikeLiked by 1 person

Thanks Leo

I’m pretty sure they never provided a metric of equivalence between a unit of LSAP and a unit of the OCR. I don’t suppose they thought they needed to, Presumably they treated the impact observed in market rates at the time the forecast was done as a given, in the starting point, and just then ran the model as if the OCR was the only stimulatory influence from there (leaving unclear how much LSAP might be needed to contribute the OCR, if they were reluctant to take the actual OCR lower).

On OIAs, any request to anyone at the RB, or via the Bank’s general information email address has to be treated (no worse than) as an OIA, so all you need to do is stick in an email to them, perhaps including an offer to discuss with them to refine the request if necessary. Do note that they are very very reluctant to release anything re recent monetary policy (anything to do with actual mon pol decisions or content of MPSs), and have managed to persuade the Ombudsman to back them on that. You might get further with a chat with Yuong, who might be willing to clarify things without getting into the formalities of their OCR process.

Will look forward to seeing your note.

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLiked by 1 person

Did I understand correctly that the LSAP is also responsible in part for the house price boom? If so, that’s a double loss to the nation. Both will have effects for a very long time

LikeLiked by 1 person

Some people argue that. I don’t agree. I’ve consistently argued that the LSAP made little difference to anything useful. Bear in mind that if there was an impact of int rates it will mostly have been long-term interest rates, and mortgage rates are mostly refixed every year or two, and the relevant wholesale rates are mostly influenced by the OCR and market expectations about where it will go in future. A year ago there was still talk (yes, incl from me) of the OCR possibly needing to go lower still.

LikeLiked by 2 people

Thanks. By the way book recommendation that might be of interest to neophytes and masters: More, by Philip Coggan

LikeLiked by 1 person

Bought it secondhand just recently so will look forward to reading it.

LikeLike

Please feel free to correct me – the below could all be incorrect.

This is how I thought QE worked overseas.

I thought the central bank purchased an asset from the market – in this case $59bn short dated government bonds:

DR Government Bonds $59 bn

CR Cash $59 bn

The government bond was previously owned by a bank, or a customer of the bank (pension fund, hedge fund etc).

Assuming it was bank owned, the banks’ journal will be the opposite.

DR Cash $59 bn

CR Government Bonds $59 bn

Instead of owning a yield making asset, they will now own cash.

They need to invest this cash, because it is earning them nothing.

They could buy government bonds. This might make sense, if they know they could re-sell them to the CB for more profits!

The bank (or their customer) could buy cash equities. Indeed, after QE, we see all share-markets at all time highs.

If they are a bank, they could lend to customers to replace the yield. For example, they could lend to Cake to buy another investment property.

This has been the main effect of QE, as far as I can see.

In NZ, there has been a HUGE burst of bank lending, after QE. Was this coincidence? House prices have skyrocketed. I assumed that this was at least partially related to cash arriving on banks’ balance sheet from QE, being lent to the house buying public, to buy another rental…

In the scenario above, and overseas QE programmes, there is either incomplete or no offsetting government debt issuance.

LikeLiked by 1 person

Just a couple of points. First (minor point), in the NZ LSAP the assets bought have mostly been fairly long-term bonds not short-term. Second (and more importantly), the LSAP purchases boost settlement cash – and someone’s deposit with the commercial banks – but the RB now pays the full OCR on all settlement cash balances, thus neutralising the transmission mech in which banks each really want to get rid of the extra sett cash they are stuck with.

But it is also worth bearing in mind that RB govt bond purchases were less than govt debt issuance – in other words, over the Covid period more govt bonds ended up in private sector hands, so that in aggregate funds (Kiwisaver, pension schemes, overseas holders etc) weren’t short of bonds to buy hold.

Remember too that bank lending is not generally constrained by the availability of settlement cash, but (in aggregate) by credit demand and bank lending standards. My own story about the NZ housing market – and thus the credit growth, which is largely endogenous, puts more emphasis on the huge swing in the structural fiscal position (much larger than any mon pol induced change in interest rates)

LikeLiked by 1 person

Cakeface, the Cash that you are referring to on the RBNZ books was not actually cash. It was a liability Account and not a Bank account, better referred to as IOU Cash(or Settlement Cash liability). The corresponding asset on the banks books is RBNZ owes us Settlement Cash $59 billion.

LikeLike

Fair enough – this situation sounds different from elsewhere. I understand that initially the cash would sit in some sort of settlement cash account. I assume that most of the bond positions the subject of QE were actually owned by the banks’ clients (pensions, hedge funds etc).

In these cases, the cash will presumably move from the cb bank settlement account to the clients account as cash. $59bn is about 20% of GDP, so not an insubstantial figure.

However, it sounds like net at least the bond holders re-invested in government securities.

I think that this is a different situation from overseas, where the cb’s were massive net purchasers of government bonds (and shares) et al.

LikeLike

Cakeface, A Settlement Cash Account is a Liability Account on the RBNZ Balance Sheet. It is an IOU cash account ie a liability account not a Bank Account. Go look at the RBNZ Balance Sheet. If you are a economist then I can understand why you can’t read a Balance Sheet.

IOU cash is quite different from I paid U cash.

LikeLike

Michael, the reference LSAP might refer to long term but it has become very clear to me this is not the case. It actually means as many available Crown Bonds in the market likely between 5 years to 20 year bonds. The Crown then issues longer term bonds to replace RB purchased bonds likely 20 years to 30 years bond.

LikeLike

I guess we should thank Michael for starting this thread down this accounting rabbit hole by pointing out the RB’s “nominal “ losses” on it’s LSAP programme. 😀

The “real” point is the accounting treatments just don’t matter. The RB can create money to meet any and all obligations. It allocates created money it gives or loans to anyone as reserves. Unlike everyone else it doesn’t have to have any assets to meet its money obligations – it can create them. of course banks can too (they create private bank money through loans) but have to find at least a part of that amount as reserves when clients want to transfer money to other banks’ clients.

Michael’s original valid point was that the LSAP doesn’t appear to have had any “real” economic impact.

The RB’s website says the point was to support the economy (doubtful) and to keep down interest rates (its says overseas experience is that a 10% of GDP purchase reduces rates by 50 bp).

So the LSAP helped the Govt to borrow to finance its fiscal largesse (which did have a “real” impact – affecting economic behaviours) at lower rates, and allowed banks to lend more at lower rates.

The intention of the RB to drive rates lower is to stimulate lending to increase aggregate demand. I don’t think that worked (at least relative to the Government’s fiscal spending). Banks lend mainly on collateral, so mortgage lending increased but riskier business lending did not.

Keeping rates low just allowed the Govt to borrow more than it needed (interest costs low) and spend more on unprofitable redistribution rather than investment.

So on balance the LSAP was probably bad for the economy, not good. Interest rates should have been allowed to rise in anticipation of price rises from expansionary monetary and fiscal policy.

Also, as Michael says, continuing to pay Interest on Reserves (IOR) was bad policy in conjunction with OCR reductions and the LSAP, since it counteracted the expansionary transmission mechanism to get banks to lend more.

Other QE mechanisms to expand money availability and inflation expectations were available if needed (like Fx purchases) as well as negative OCR rates, but given the supply constraints from Covid the fiscal response was appropriate (just should have been more costly for Govt to make them more prudent). As always the quantity of Govt spending doesn’t matter – its what it spends it on that counts!

LikeLike

Bill Foster, you must be an economist. Yes the RB and the govt of any country in the world can print money easily but they do not do that. It is called Financial discipline. Thats where Accountants come in. They will test the Financial Statements to ensure there is supporting documents to support classifications. The QE by Central Banks around the world, none of it has been money printing. All are based around Debt.The US QE is based around releasing Fed Reserve cash deposits. US savings deposits require 10% cash to be held at the Federal Reserve or by Fed approved Banks to hold the 10% cash deposits. US QE released the requirement to hold 10% in cash of savers deposits and used those cash reserves to purchase US Treasury Bonds..

If money was printed the transactions would be

Step 1

Dr Cash in Bank Account $59 billion and Cr Equity Reserve – LSAP $59 billion

Cash is printed and banked would have been the first step. This would have strengthened the RB Balance Sheet. However this did not happen. Instead the RB Balance Sheet is weak with only $2 billion Net Equity position not $59 billion Net Equity if cash was printed.

Step 2 Dr LSAP $59 billion Cr Cash in Bank $59 billion

This did not occur for the simple reason that the entire NZ QE was based around Debt and Market Settlement Cash Account Liability Account ie IOU Cash.

LikeLike

Interesting. I would guess the weighted average coupon on the bonds might outweigh the future OCR track? So cash flow wise, it might look OK – assuming the bonds are held to maturity and the accounting treatment is same.

As an aside, what did you make of the AU government bond yield move this week? Yikes….!

LikeLike

Yes, dramatic in Aus. The previous RBA statements about tightening always seemed extremely implausible, even allowing for how far below target Aus inflation had been in recent years. This week’s inflation numbers just dramatically reinforced that.

Note that the RBA will also have been racking up really big MTM losses on its bond purchases – all the sadder for the Aus taxpayer given that the RBA only got into large scale bond buying well after the worst of the Covid crisis was over.

LikeLike