The Reserve Bank’s Monetary Policy Committee will release its Monetary Policy Statement tomorrow afternoon. We can expect substantial changes from the rather complacent, perhaps even dovish, statement/forecasts they released in May. The hard data have moved quite a lot and the Bank – with phalanxes of macroeconomic analytical resource – was far too slow to recognise what was going on.

Of course, it is anyone’s guess what the MPC will do. Unlike serious countries, or serious central banks, we’ve had no speeches from MPC members, and no position papers outlining how (and why) the MPC was likely to respond if and when the data indicated that tightening in monetary conditions was warranted. Normally, it isn’t much of an issue, since there is usually only a single moving part (the OCR) but we are now still living in the wake of last year’s extraordinary interventions. My focus here isn’t on what the Bank will, or won’t, do, but on what they should do, given the Remit the Minister of Finance has given the MPC.

NZIER run their Shadow Board exercise, in which a mix of (mostly) economists and (a few) people working in business or lobby groups offer their view on what the MPC should do. It is an interesting exercise, if only because respondents are asked to assign probabilities to their view (eg 25% chance the OCR should be 0.25 per cent, 50% it should be 0.5 per cent, and 25% it should be 0.75 per cent – an exercise the Governor used to ask his internal advisers to do, accompanying each of our specific recommendations). They’ve also this time asked not just about tomorrow’s OCR decision but about appropriate policy over the next year. Here are the last assessments.

I’ve always struggled with the idea of 100 per cent certainty about any macro view, especially one about periods a year ahead. If I learned anything in decades of working on monetary policy it was how pervasive uncertainty (and unforecastability) is. If I were answering this particular survey I’d probably run with something like an 80-90 per cent view that the OCR should be higher now, but not much more than a 50 per cent view that it should be higher over 12 months. We just don’t know, and can’t know.

And that would be my first recommendation to the MPC: do not act as if you know more than you possibly can. The Bank insists on publishing economic projections several years ahead, but they rarely contain any useful information about what will happen over the following few years. But the key thing is not to become wedded to your own numbers, or desire to offer more certain than is sensibly possible. The last OCR tightening cycle the Bank undertook in 2014 was a mistake – the case for it was very weak at the time (as I and a couple of others argued internally, a few externally) and even more so with hindsight – but part of what led them astray was that the Governor had become entranced by his own numbers (projections and trend assumptions) and went round openly talking of a programme of OCR increases that would raise rates by a couple of hundred basis points. It creates something of a self-fulfilling momentum, complete with a feeling of needing to follow through.

So whatever the MPC decides on actual policy adjustments tomorrow, the words should emphasise how uncertain and changeable the environment (here and abroad) is, and that the Committee will be guided primarily by hard data (on core inflation and excess labour market capaciity) rather than by castles-in-the-air projections or programmes of tightening. We just do not know what is happening to natural/neutral interest rates – the belief that people did led central bankers, and markets for a time, astray last decade. And when data change there is no harm or shame in changing course; rather than is what central bankers doing their job are supposed to do. The job of the MPC is not to give a clear steer about the future, but (in a stylised way) to adjust short-term interest rates consistent with overall incipient savings/investment imbalances (normally, doing what the market would do if we didn’t have central banks).

The situation at present is complicated because the Bank last year deployed three distinct tools:

- the OCR,

- the Large-scale Asset Purchase programme (LSAP), and

- the funding for lending programme, designed to narrow the wedge between wholesale and retail funding rates.

On the Bank’s own stated logic, I think an OCR adjustment should be the final step chosen if – as seems to be the case – policy tightening is warranted.

Take the LSAP as an example. The Bank has repeatedly claimed that the LSAP was highly effective in loosening overall monetary conditions, lowering both wholesale interest rates and the exchange rate. If so, surely an obvious response now would be to start selling the bonds back to the market, at scale if need be? After all, every day the Bank holds the bonds the taxpayer is exposed to unnecessary market risk (remember that they have lost us $3 billion or so to date), and there is no obvious good reason for the central bank’s balance sheet to be as bloated as it is for any longer than is strictly necessary.

Now it is true that other central banks have been reluctant – after the bond-buying of the last decade – to start actively offloading their bond holdings (although the Fed was doing so), but that was surely was mostly because economies and (in particular) inflation never recovered sufficiently robustly to warrant/require tighter monetary conditions. By contrast, in New Zealand right now there is a pretty strong case for such a tightening.

Of course, if the Bank really doesn’t believe its own rhetoric (about the efficacy of the LSAP) it would still make sense for them to be getting a sales programme in place, but then they couldn’t claim that bond sales were a substitute for other actions. As I’ve outlined in previous posts etc, my own view is that the New Zealand LSAP did little or nothing of any macroeconomic significance, but that isn’t what the Governor keeps telling us.

The next step the Bank should be taking is to end the Funding for Lending programme. It was a jerry-built crisis intervention that worked – at a time when the MPC reckoned it could not take the OCR negative – but we aren’t in a crisis now. It isn’t a competitively neutral instrument – only banks have access to it – and if an efficiency mandate is disappearing out of the Reserve Bank legislation, the concern with economic efficiency and minimising favourable treatment for particular types of counterparties shouldn’t. It should be discontinued now and the market left to settle the relationship between the OCR and retail and wholesale funding rates.

What isn’t clear is quite how much impact ending the Funding for Lending programme would have on deposit rates. The large positive margin between term deposit rates and either the OCR or bank bill rates that has prevailed over the last decade – often 150 basis points – is hard to make full sense of (and is larger than the comparable margin in Australia). But the best guess has to be that removing new Funding for Lending might see that margin widen out from the 50 basis points it got down to back to something at least somewhat wider (perhaps another 50 basis points).

I don’t think I’ve seen mention of selling down the LSAP bonds or ending the Funding for Lending programme in any of the commentaries I’ve seen. I presume that is a sign the Bank has either suggested to banks no change is coming there any time soon or (at least) by silence left that impression. But these crisis interventions really should be dealt with, and incorporated into the forecasts, before the Committee moves to consider OCR increases.

My read of the economic data is that there is a reasonable case for the MPC to validate quite a significant tightening in monetary conditions (I express it that way because both wholesale and, to some extent, retail rates have begun to move in anticipation). I don’t think that is even a particularly difficult call. I don’t base it on forecasts, but on where things stand right now (including, but again not to over-emphasise forecasts, how different things clearly are now from how most thought they would be late last year).

What are the key variables in that story? First, of course, is inflation itself – but core inflation, not the (currently high) headline CPI numbers. On the Bank’s sectoral core factor model – a pretty smooth and persistent series – core inflation is now above the target midpoint for the first time in a decade. That is a good thing – (core) inflation should fluctuate around the target midpoint, and not have the midpoint treated as either a ceiling (as it seemed at times in the last decade) or a floor (as it sometimes seemed the previous decade). But since the general sense was that it would take longer to get inflation back up, and we know policy works with a lag, it is a prima facie case itself for underpinning real interest rates at a higher level.

And then there is the unemployment rate, at 4 per cent (for the June quarter, centred in May) down to pre-Covid levels. I’m not going to run a strong independent view on what the NAIRU is for New Zealand but whatever it was a few years ago it is likely to be somewhat higher now, between things like higher benefit levels, higher minimum wages, higher statutory holiday provisions, reduced emphasis on getting people off benefits, and the disruption to labour-market matching from closed borders (both reductions in demand for certain roles and disruption in access to migrant labour). To be clear, I’m not taking a view here on the wider merits of any of these policies, just noting as a macroeconomist that they are, taken together, likely to raise the unemployment rate consistent with stable inflation.

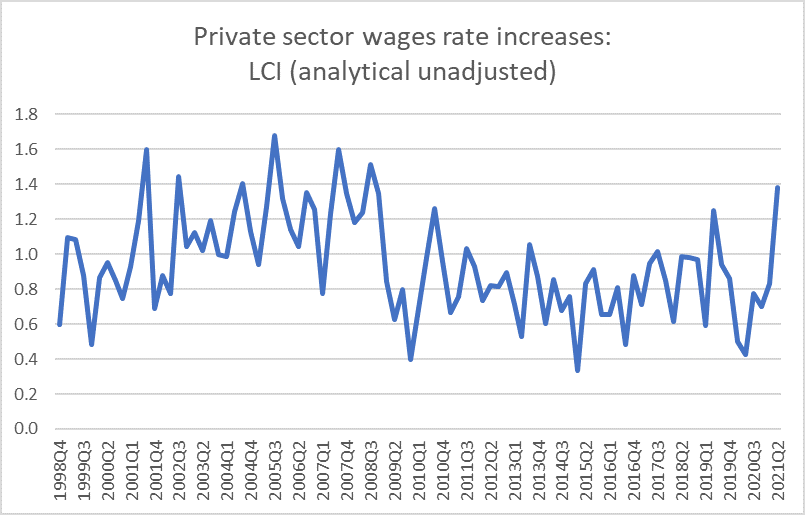

As it happens, in that same June quarter data we’ve already seen quite an acceleration in private sector wage inflation. It could, I suppose, be random noise, but it doesn’t seem sensible now to assume so (given that it isn’t out of line with anecdotes, surveys or the unemployment rate itself).

Even if there is a bit of seasonality in the series, it is the highest quarterly increase since the peak of the labour market boom in the 00s – when core inflation was definitely accelerating, and when there was still a bit more productivity growth to underpin wage increases than is likely to be evident right now (borders closed and all that).

June quarter data is centred on the month of May (SNZ survey throughout the quarter), but we also have the SNZ new monthly employment indicator that they take from hard (tax) data. The number of filled jobs is reported to have risen by a further 1.1 per cent in the month of June. and in a series that goes back to 1999 there have been only a handful of months with faster growth in this series. And over the last 22 years inward migration has mostly been quite strongly, adding to both demand for and supply of labour. Since Covid, we’ve had consistent modest net outflows of people. And yet according to SNZ there are now 2.1 per cent more jobs than there were at the end of 2019 (when the unemployment rate was also 4 per cent). With fewer people here now than then (despite some natural increase), it all points to the unemployment rate heading lower again this quarter.

Then, of course, there is inflation expectations. In the Bank’s latest survey of semi-experts (I’m usually included, but somehow the survey email ended up in my Spam folder) , two year ahead expectations rose quite a bit to 2.27 per cent – the highest the survey has recorded since June 2014. Since shocks happen, these expectations measures aren’t great forecasts (nothing is) but as a read of how people are feeling and seeing things now they are what we have.

The Bank also does a survey of household expectations, which gets very little coverage. Again, there is no information in the survey on what future inflation will be, but what people think about inflation affects how they think about any specific level of nominal interest rates. In the latest survey, a larger percentage of respondents expect higher inflation over the next year than at any time in the survey’s history.

Point estimates – which are harder for household respondents – have also moved up quite a bit, for both 12 month and five year horizons.

It is a fairly elementary part of thinking about monetary policy that, all else equal, if inflation expectations move up and you don’t want inflation itself to go much higher, you want interest rates to move up at least as much as the expectations themselves have risen.

If I wanted to mount a counter-argument to my own case, I might cite – as I often have over the years – the breakeven inflation rates calculated using nominal and indexed government bond yields. Very long-term breakevens are still well below 2 per cent (but have moved up) but using the 2025 indexed bond, implied inflation expectations for the next four years are now almost exactly 2 per cent – not troublesome in a level sense, but far far higher than we were seeing pre-Covid.

The case for not acting now seems, frankly, threadbare. Will the Australian economy be weaker this quarter and perhaps next? To be sure, but it isn’t obvious there is a substantial impact on New Zealand (especially as travel flows were already very modest). Sometimes there is a case for seeing how low the unemployment rate can be driven – there was a good case for that for much of the pre-Covid – but not when (core) inflation is already at or a bit above target, and most of the demand indicators suggest that core inflation would – all else equal – rise further from here.

That doesn’t mean it is time to panic either. Full employment and inflation near-target are good outcomes in themselves – especially against the backdrop of the previous decade. It isn’t time to over-react, or for whippings about how policy settings were too loose for too long, but simply for calmly and deliberately getting on with the job.

For me – and given the rapid easing last year – that would mean a policy package tomorrow of (a) a programme of bond sales back to the market of $2 billion a month (which over two years would clean out the holdings), (b) a discontinuation now of the Funding for Lending programme, and (c) a 25 basis points OCR increase.

But if they don’t do either (a) or (b) – the former more symbolic on my telling than substantive, but wouldn’t be on their own – the case for a 50 basis point OCR increase tomorrow looks pretty strong. Not to foreshadow a string of future increases, but simply because we are at full employment, perhaps going beyond, and inflation is at or a bit above target, and perhaps looking to go beyond. It would simply be a good solid sensible response to some good cyclical economic data (note that the structural fundamentals of the economy are as poor as ever, but that matters to the Reserve Bank only in, eg, interpreting wage inflation data).

Hi Mike

Nice commentary. I agree on the need to end the FLP and to wind back the balance sheet. Not sure why no one has really been talking about this but these measures would push up wholesale rates to an extent, and that in turn would hit mortgage rates so the case for it seems pretty obvious.

The case for a 50bp move seems to me just as threadbare as no move. If the Bank wants to raise rates in an orderly and businesslike fashion then 25/quarter should be fine as while core inflation is rising, it’s still very close to target and activity has been boosted by massive fiscal support last year, which is now gone. Overall, monetary and credit conditions have been tightening already and much of the squeeze on capacity and inflation has been caused by COVID disruptions. Given uncertainty about the future, 25bp increments can still get the bank to where it thinks we should go, while keeping options open regarding risk.

Two things that really stand out to me as notes of caution: 1) given the rise in short term wholesale rates, the impact on the term structure has been minimal with the IRS curve flattening, 2) despite a solid ToT and a surge in the NZ-ROW rate differential, the TWI has been falling. None of this should be happening If the market believed the reflation story.

LikeLiked by 1 person

Shouldn’t hold any such view with certainty, but just a couple of points in response.

First, the Tsy’s estimates of the structural fiscal deficit for 21/22 are still v large, so altho fiscal consolidation is probably coming i don’t think it is here yet.

Second, your final para is a fair point, but could cut both ways. Is it possible there is a reluctance abroad to recognise that the NZ economy is at full employment, and perhaps going further?

But to reiterate, I’m not signing on to any view about where the OCR will be or ought to be at the end of next year, just noting that the return to full employment has been unprecedently fast (which is great in and of itself) so it probably makes sense to pull back quite a bit of last year’s monetary stimulus now – in a way it wouldn’t have at the May MPS even if these numbers had then been forecast.

LikeLiked by 1 person

<<>>

No definitely not. People offshore see what’s going on in NZ very clearly.

Remember, most of those of us who are offshore are very well versed in NZ – having traded NZ products for many years, often at major NZ institutions, having worked for those institutions including the RBNZ. Also, we do do our homework. My note on interest.co.nz was backed up by a 22 slide PowerPoint presentation that drilled down deep into the numbers for instance, looking at the CPI down to over 100 subcomponents.

The comments some bank economists made about offshore analysts this week was really insulting and condescending.

As a now offshore analyst, I’ve found it amusing to watch two banks flip-flop on their views. Pathetic.

LikeLiked by 1 person

Only just read your interest.co piece now. Interesting case, and I guess only time will tell.

LikeLiked by 1 person