There was a little flurry of media coverage over the weekend about the latest set of cuts in retail mortgage interest rates. But it is worth keeping these changes in some perspective.

The Reserve Bank publishes monthly data for the “special” rates advertised for new borrowers (or those moving to another bank) and we can get a read of current rates from bank websites, as summarised in the tables on interest.co.nz.

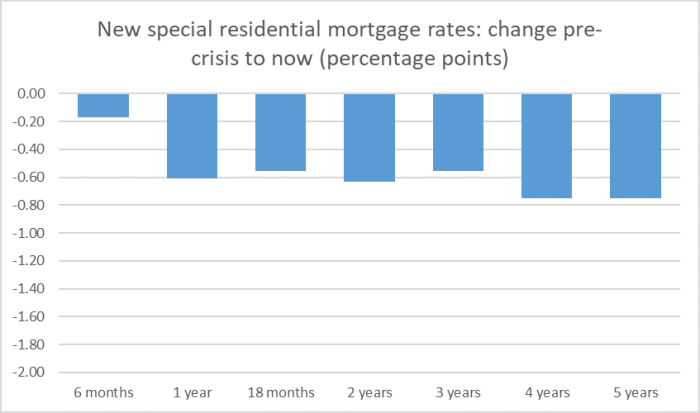

So how much have residential mortgage rates fallen since the coronavirus slump began? As it happens, rates had been pretty stable for several months up to February, so this chart compares the latest rates on offer with the average for the period November to February.

For most maturities, that’s not nothing.

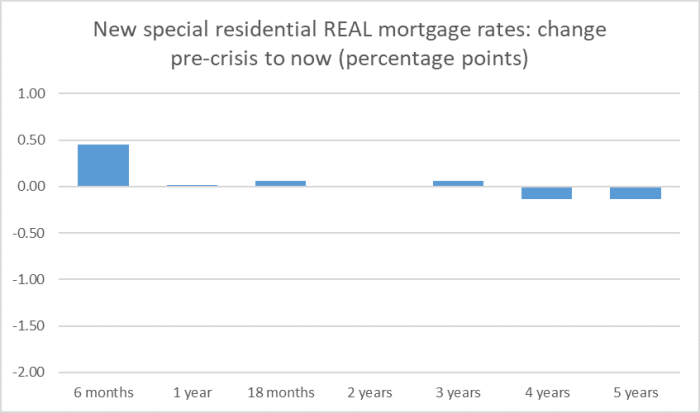

On the hand, these are nominal interest rates. And we know that the expected future inflation rate has fallen. There is a variety of measures, survey-based and market. The one the Reserve Bank has typically paid most attention to is the two-year ahead measure in its quarterly Survey of Expectations. On that measure, inflation expectations have fallen by 0.62 percentage points since the pre-crisis period (the one year ahead measure shows a larger fall, the ANZ one year ahead measure a smaller fall).

Apply that fall in inflation expectations to those “specials” and the real – inflation-adjusted – version of the chart now looks like this.

I guess there is still a slight reduction in longer-term real rates, but…..not many people in New Zealand fix for four or five years. The market is concentrated on the shorter-term fixed rates (at present, it appears, the 18 month term) and there has been no reduction in real interest rates there at all.

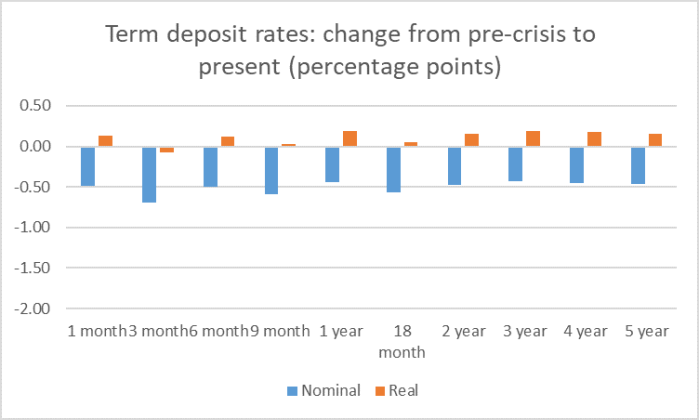

Term deposit rates have come down a bit more too. But here is how the chart of those rates looks if we compare current rates with those around the turn of the year. I’ve shown the nominal rates and real rates (using the same drop in inflationn expectations as above) on the same chart.

Pretty much across the board, real term deposit rates have risen slightly since the crisis began (including at what appears to be the most competitive part of the market, for terms of 6-12 months). It is an odd response to a really serious economic slump.

Don’t blame the banks, or depositors for that matter; this is about choices made by the Reserve Bank Monetary Policy Committee – the prominent ones (Orr especially) and those faceless unaccountable external ones (Buckle, Harris, Saunders), all appointed by the current Minister of Finance.

The Governor keeps talking about getting interest rates as low as possible. But they clearly aren’t – term deposits are mostly still a bit above 2 per cent (and far higher than in Australia) – and yet the MPC has pledged, and repeatedly reiterated its dogmatic commitment based on no published analysis, to not cut rates any further until at least next March, still 10 months away.

And yet this is a really serious downturn. Everyone seems to agree on that. All the unemployment predictions – even with the temporary cover (keeping people out of the official statistics) of the wage subsidy scheme – involve higher peaks than we saw in the 2008/09 recession. Even with big fiscal commitments, nominal GDP is expected to be way lower than previously expected, and the Bank expects to undershoot the bottom of its inflation target for a couple of years (for which there was nothing comparable in 2008/09).

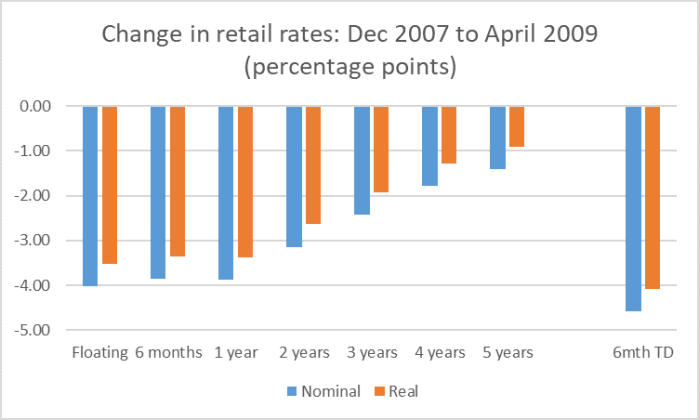

How, then, did retail rates (real and nominal) behave over 2008/09? Recall that that was an event that had its foundation in financial system problems, and even if the credit concerns weren’t specific to New Zealand the problems affected our banks’ access to funds, pricing etc.

The data are bit thinner for that period. The Reserve Bank was only publishing “standard” mortgage rates, and single (six month) term deposit rate. Oh, and it is a bit less clear when to date comparisons from. Retail rates had gone on rising into 2008 (with the Bank’s acquiescence) as offshore funding costs were rising, and at the other end, shorter-term rates kept dropping further into 2009 than longer-term fixed rates did. Inflation expectations also fell during that recession, on the Bank’s two-year ahead measure perhaps by about half a per cent.

But this is what happened from the end of 2007 to April 2009. (Changing start or end dates changes some of the numbers – either way – by up to perhaps 50 basis points, mostly small on the scale of this chart.)

In other words, falls in retail rates (at the horizons where most of the business was written) of hundreds of basis points. And that, in the Bank’s view (correctly as it turned out) was consistent with keeping inflation in the target range, even if not quite as high as they would have liked).

The Governor keeps claiming that his Large Scale Asset Purchase programme – buying huge amounts of government bonds now yielding less than 1 per cent, in exchange for issuing huge amount of Reserve Bank deposits currently yielding 0.25 per cent – is hugely effective and a fully adequate substitute for choosing not to do more with the OCR. One can get down in the weeds of detailed arguments about what the LSAP may or may not be doing at the margin to bond rates or swaps rates, but whatever those effects may be – and I reckon we are pretty safe in concluding that they are mostly small – the rates that firms and households are actually receiving/paying is the bottom line.

In real terms, the household rates shown above have hardly moved at all, and there is little or nothing to suggest that picture facing businesses will be materially better (eg headline SME rates have fallen no further, and many larger businesses have facilities on which they pay a fixed margin over bank bill rates. Bank bill rates have fallen by about 1 per cent since the start of the year, so in real terms a fall of perhaps 0.4 percentage points. The contrast to 08/09 remains striking.

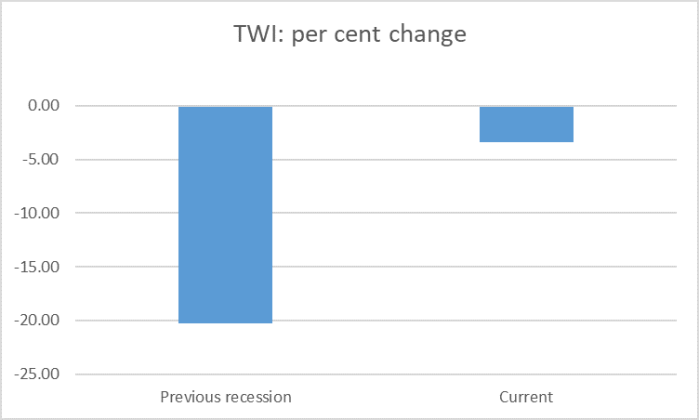

Of course, there is also the exchange rate. The Governor claims to be successfully influencing it as well. It is always difficult to know where to date comparisons for exchange rates, but here I’ve shown the fall in the exchange rate in the last two recessions:

- for 08/09 the average in April 2009 relative to the average for the second half of 2007, and

- for the current event, yesterday’s TWI relative to the average for the second half of 2019

Monetary policy just is not doing its bit, even once all the fiscal support is factored into the projections. That is a pure choice by the MPC.

We don’t know why they’ve just chosen not to do their job – aiming for 2 per cent inflation and, as much as they can consistent with that, supporting a speedy return to full employment. Last year, MPC seemed to embrace their mandate with some gusto. Now they appear like stunned animals caught in the headlights, uninterested in doing what they are paid for – all while their spokesman keeps claiming to be doing a lot.

It is pretty reprehensible, and I find it quite remarkable that the MPC – all of them, not just the Governor – have not been asked harder questions about their failures. Instead, much of the media seem to treat their acknowledged failure to ensure that banks’ operational systems etc were ready for negative rates as just “one of those things”, as if it could happen to anyone – never for example drawing the contrast with Y2K, when the Bank proactively ensured it and the banks were ready, with contingency plans as well. And notwithstanding that all of the data in this post are readily available, none has been yet heard to ask the Governor – and his MPC – why they are content with such trivial changes in real interest rates even when, with all their avowed enthusiasm for it, in combination fiscal policy and monetary policy in combination still have the Bank quite openly acknowledging that inflation will undershoot, and apparently not very bothered about the unemployed either.

Of course, the Minister of Finance bears responsibility for all this, and for all the individuals involved. Perhaps an Opposition that wanted to ask hard questions about the government’s stewardship at present – even perhaps flag a different more pro-active approach – might ask him just why he thinks it is appropriate for real interest rates to have hardly changed at all (and the real exchange rate not much more), even as he is willing to lend to the weakest business credits are far lower rates than his central bank’s monetary policy would support more generally.

You are the expert but six months ago you could not have expected our economy to be where it is now. What about another 6 months? I’m not so troubled by NZ: we seem to have an epidemic under control, everyone seems to be content to increase debt to keep our economy afloat. I am a little bothered that every commentator seems to be using this borrowing to resolve unrelated issues: homelessness, inequality, climate change, moving the port, etc. What seriously troubles me is the rest of the world – an epidemic that they may not be able to control and how will they borrow if they are already up to your neck in debt?

In what ways and to what extent will the rest of the world affect NZ in the next couple of years? Without that knowledge worrying about interest rates, both term deposit and mortgage, seems pointless.

LikeLike

One can really only set mon policy on what one knows now. No one, for example, holds it against the RB that in Dec last year they weren’t easing policy. Same mostly goes for all recessions (incl 08/09) – very few are properly forecast.

So, yes, who knows where to from here. But the current situation is one of huge excess capacity, here and abroad, and no one expects those gaps to disappear promptly without lots of policy support. At present, in many respects the world looks worse than NZ (although that isn’t totally clear since – still having the virus – European countries are opening to tourism again in a way we can’t, given our focus on elimination).

Not knowing how things might change in the future and doing nothing with econ policy is – best guess – a recipe for a continuation of large excess capacity, high unemployment (and falling inflation, falling inflation expectations).

LikeLike

Our problem is we have gone too far with our lockdown trying to eliminate. The evidence is that 96% of people will recover from this Covid19. By locking down so severely the virus have not run through the population so that the community develops a natural immunity. Our borders are going to be stuck in lockdown while the rest of the world will be back into normal open borders.

This means we will be a mini North Korea with closed borders. No one in and no one out. Jacinda Ardern has given us a legacy of closed borders economic poverty with no end in sight.

LikeLiked by 1 person

To be fair I’ve been following your blog for a couple of years and you have consistently pointed out the importance of having a robust systems capable of reacting to unexpected events. I can understand the frustration you express – it is similar to being a computer analyst telling users that backup and recovery is important and those users ignoring the advice because it involves effort for no apparent return.

GGS: you are allowing your dislike of Jacinda to influence your judgement. At present Europe has roughly 5% immunity; if European countries successfully lift their lockdowns with minimal difficulties then NZ can choose to do the same. Our govt learned from Italy and Spain earlier this year [it would have been wiser to have learned from Taiwan]; so we can do again although at present I wouldn’t risk it until there is more evidence.

LikeLike

” GGS – The evidence is that 96% of people will recover from this Covid19″

Not even that. The latest data out from WHO shows an infection fatality rate (IFR) projected as 0.26%. Given WHO have been very conservative at estimating the asymptomatic part of the population, the true IFR is probably closer to 0.2%. So 99.8% of people will recover from Covid. How big an over-reaction has this all been then? A Truly, monumentally insane one.

I wholeheartedly recommend lockdownskeptics.org both for medical and economic critique.

LikeLike

0.2% on average Look at the figures for Qatar and Singapore and that could be an over-estimate. You are right to be skeptical.

Everyone who is not a fatality cannot be considered recovered; maybe some will carry permanent health troubles.

As a 71 year old with blood pressure and heart issues I’d estimate my personal fatality rate would be 50%. My wife with a different medical condition about the same.

LikeLike

Huskynuts, you need to stick to facts under NZ climate conditions of higher UV sunlight levels and well spaced out population. You can’t use world statistics of negligently run rest homes that squeeze 50 people in a double bedroom like conditions and not expect the virus to wreck havoc. Or China clearly overstating the deadly effects in Wuhan because they lost political control of the city and the virus is a great excuse to lockdown the city and they have been busy killing off political dissidents. I would not be surprised if Hong Kong suddenly had a 2nd wave of infections, face another Covid19 lockdown with hundreds of dissidents dead from the viral infection.

The fact is of today in NZ there were 1504 infected and 1461 recovered. That is a recovery rate of 97% from a infected Covid19 case. Stick to facts.

LikeLike

GGS – you totally missed the point.

I was agreeing that the risk was small, in fact far smaller than your official numbers state.

We have 1504 identified cases in NZ, but there are almost certainly much larger numbers of people who are either asymptomatic or are positive but have not been tested.

The sick/dead count stays the same. Therefore the official recovered count is almost certainly an under-estimate. That’s why the real scientists like those at Plan B are calling for random serological studies to start getting some more accurate data.

From your previous posts, I took you to be a skeptic. Quoting the official NZ figures as if they were 100% accurate is not “sticking to the facts”. It’s pretending the official infected figures have some resemblance to reality, which all the data is saying is extremely unlikely.

LikeLike

Bob, you too need to look at facts under NZ conditions instead of fake news on Youtube. You cannot expect your highly skilled young people to look after you especially when old people are basically not dying. That is why we have a low skilled migrant problem. It is to look after our old and aging people. The health and aged care sector is the fastest growing sector in our economy.

LikeLike

Huskynut, apologies. I did misread your reply. I agree completely with you that there are likely thousands more cases that have not been tested or detected as many likely thousands in NZ have been infected and already recovered.

LikeLike

The great New Zealand shake-out

The lesson NZ will learn is not to invest in transient blue-sky business activity and not ro rely on mass-migration and mass temporary workers

Fletcher Building Ltd and Air NZ and Auckland International Airport are three businesses either directly or indirectly dependant on that segment

Fletcher Building has suspened all Capex immediately

Air NZ has cancelled $700 million Capex

Auckland Interational Airport has suspened all Capex

No more borrowing by them for the forseeable future. Any reduction in interest costs will go towards triage

Then there is the flow-on effect with the likes of H&J Smith closing 7 stores

LikeLike

In the current climate the largest beneficial effect from much lower interest rates is likely to come through a much lower exchange rate.

LikeLiked by 1 person

That makes sense. My mortgage will need to be refixed in August; it has about 10 years to go. Repayment of principal swamp interest payments so a change from 4% to 3% or with your preferred RB policy to say 1.5% really make little difference to me. However if the NZ$ sinks NZ is rewarded by improved profits on exports which ought to improve employment opportunities throughout the economy.

LikeLike

Bob, for every borrower like you and me there are 10 other younger savers who will lose out on lower interest rates. How does consumption demand increase when 10 other younger people lose out? We can’t keep protecting old people with the loss and the cost being carried by our future generations.

LikeLike

I agree with tour comment on the currency Michael.

AO has said that he doesn’t see negative rates before year-end due to banks being unable to handle them.

Q: could they handle a zero cash rate now?

Moving the policy corridor to set completely at zero seems viable to me, and it would dampen FX and help nudge down mortgage rates.

LikeLike

Indeed (and even the RBA – with a Governor apparently staunchly opposed to negative rates – has its deposit rate at 0,1 per cent).

LikeLike