How long have I been banging on about the potential limitations of monetary policy in the next recession and issues around negative interest rates? The first such post I could find on the blog was almost five years ago to the day, and as I’ve noted previously it had been a concern for some time before, going back to 2010 in the wake of the last serious recession and then the internal working group I chaired at the Bank when Alan Bollard rightly was concerned about downside risks at the height of the euro crisis. (That was the report, adopted by senior management, which recommended that steps be taken to ensure that banks could operate effectively with negative interest rates.)

Ken Rogoff has been writing about such issues, and publishing in various prestigious fora, for at least as long. And Rogoff is a Professor of Economics at Harvard and also served as Chief Economist at the IMF for a couple of years. He and Carmen Reinhart wrote the book This Time is Different: Eight Centuries of Financial Folly that attracted so much attention in the wake of the 2008/09 crisis. As I noted in a post a couple of years ago he and another former IMF chief economist Olivier Blanchard proposed dealing with the lower bound issues by raising inflation targets (the suggestion at the time was to something like 4 per cent), which would – if successful – raise neutral nominal interest rates and provide more policy leeway in the next recession.

In the last few years his focus has shifted to addressing the lower-bound issues at source. There was his 2016 book The Curse of Cash which I wrote about here in which – among other issues physical cash raises – he addressed the lower bound issues and proposed to address them in part by progressively removing higher denomination banknotes, leaving in time nothing higher than a $20 note. More recently still there have been various papers, including last year’s paper (with a PhD student co-author) “The Case for Implementing Effective Negative Interest Rate Policy”. And there have been a couple of short papers in recent weeks. There was a piece on Voxeu by Rogoff and LIlley about three weeks ago. This was the abstract

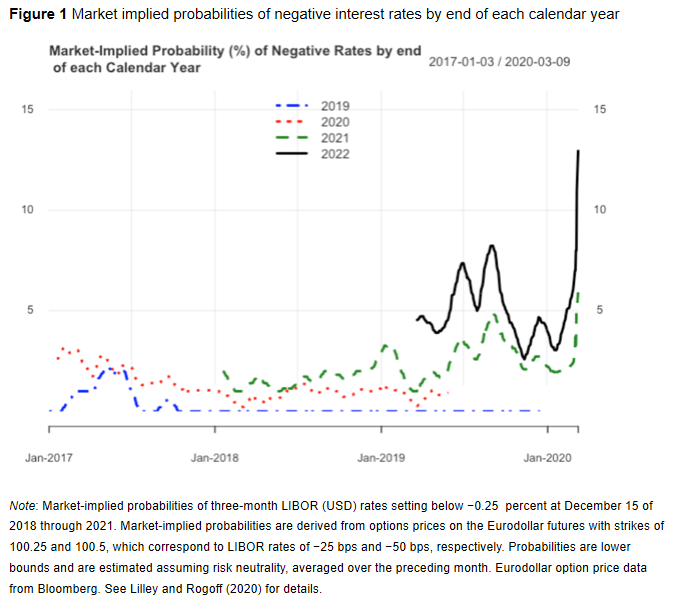

In the aftermath of the Global Crisis, conventional monetary policy has been constrained by low interest rates in many major economies. This has spurred debates on the possibility of introducing negative interest rates in the monetary policy toolkit. This column uses evidence from the US to show that not only do the markets expect the low interest rates to persist into the future, but they also expect the use of negative interest rates down the line. Moreover, markets no longer believe that even quantitative easing can bring inflation to target, which leaves very few alternatives for monetary policy apart from negative interest rates.

As here, breakeven measures of implied inflation expectations in the US are now well below target. There is a nice chart for the US suggesting that (at least then) markets there had already moved to put a non-trivial probability on materially negative short-term interest rates in the next couple of years.

Focusing on the medium-term implied inflation expectations they note that this

…suggests that the market’s change in beliefs has moved beyond the present crisis, and it now has re-evaluated the extent to which it expects the Fed to be constrained more generally. One problem with such a scenario is that it poses a perverse feedback loop. As the Fed becomes more constrained by the zero lower bound, the expected inflation rate falls, lowering the neutral nominal interest rate, which in turn makes the zero lower bound more binding.

Very much the same point I’ve been making here.

This week Rogoff has a very accessible piece on Project Syndicate (thanks to a reader for drawing it to my attention) under the simple and stark heading “The Case for Deeply Negative Interest Rates”. His summary

Only monetary policy addresses credit throughout the economy. Until inflation and real interest rates rise from the grave, only a policy of effective deep negative interest rates, backed up by measures to prevent cash hoarding by financial firms, can do the job.

Some of the emphases are a bit different in a US context (where much of government at all tiers is highly indebted)

For starters, just like cuts in the good old days of positive interest rates, negative rates would lift many firms, states, and cities from default. If done correctly – and recent empirical evidence increasingly supports this – negative rates would operate similarly to normal monetary policy, boosting aggregate demand and raising employment. So, before carrying out debt-restructuring surgery on everything, wouldn’t it better to try a dose of normal monetary stimulus?

More generally

It is not rocket science (or should I say virology?). With large-scale cash hoarding taken off the table, the issue of pass-through of negative rates to bank depositors – the most sensible concern – would be eliminated. Even without preventing wholesale hoarding (which is risky and expensive), European banks have increasingly been able to pass on negative rates to large depositors.

Some issues are relevant to the US and the euro-area but not in same form to us

A policy of deeply negative rates in the advanced economies would also be a huge boon to emerging and developing economies, which are being slammed by falling commodity prices, fleeing capital, high debt, and weak exchange rates, not to mention the early stages of the pandemic. Even with negative rates, many countries would still need a debt moratorium. But a weaker dollar, stronger global growth, and a reduction in capital flight would help, especially when it comes to the larger emerging markets.

In our case, a much lower exchange rate would make a material difference to the fortunes and prospects of the tradables sector.

Rogoff ends

Emergency implementation of deeply negative interest rates would not solve all of today’s problems. But adopting such a policy would be a start. If, as seems increasingly likely, equilibrium real interest rates are set to be lower than ever over the next few years, it is time for central banks and governments to give the idea a long, hard, and urgent look.

From which I’d depart only in replacing that “long” in the final line with a “short and intense” – this isn’t the time for year-long reviews, but for early and decisive action (as has been managed on so many other fronts in recent months).

There has been a view in some quarters over the last few years that negative interest rates don’t work (in the sense of boosting demand, credit, inflation or whatever) and could actually be contractionary in their effect. I’ve been sceptical of that, but also inclined to wonder whether results for slightly negative interest rates – where there might be threshold effects – would generalise to deeply negative wholesale and policy rates. Rogoff links to a recent paper, newly updated last month, by several researchers mostly at the ECB which uses very disaggregated data to suggest that actually negative interest rates in Europe have worked. Their abstract is as follows

Exploiting confidential data from the euro area, we show that sound banks pass on negative rates to their corporate depositors without experiencing a contraction in funding and that the degree of pass-through becomes stronger as policy rates move deeper into negative territory. The negative interest rate policy provides stimulus to the economy through firms’ asset rebalancing. Firms with high cash-holdings linked to banks charging negative rates increase their investment and decrease their cash-holdings to avoid the costs associated with negative rates. Overall, our results challenge the common view that conventional monetary policy becomes ineffective at the zero lower bound.

The channels they examine look to work a little differently with negative than with positive rates, but not less effectively.

Another central bank with significant experience with mildly negative rates in Sweden’s Riksbank. A year or so ago, a couple of Riksbank researchers published an accessible treatment of the Swedish experience, from a top-down perspective. They summarise their results (with all sorts of caveats in the body of the paper) this way

It has been suggested that the response of bank lending rates to interest rate cuts may become weaker when the policy rate passes below a certain level. This column argues that in the case of Sweden, the pass-through of policy rate cuts below zero to the economy has been reasonably good and monetary policy has been effective even at negative policy rate levels.

As all researchers in this area recognise, a big problem is that limited data. Only a few central banks have had negative policy rates, almost entirely in a single economic cycle, and none of them have taken the policy rate very deeply negative and dealt directly to the ability for big players to convert into physical cash. So we cannot say with certainty what would happen if we took the – fairly straightforward – steps that would enable the OCR to be cut to -3 or -5 per cent. But the signs look fairly promising, whether on the limited experience we have, or pretty basic economic theory (all else equal, holding New Zealand dollars will typically be much less attractive if NZD assets are earning a lot less than those in other countries). And the idea of simply letting the Reserve Bank sit on its hands and do almost nothing that matters macroeconomically (hand-waving around big bond purchase programmes is mostly a distraction in macroeconomic terms, whatever value it might initially have added to market functioning).

You’ll recall that Westpac’s economists last week came out picking that the MPC will abandon its firm pledge not to cut the OCR further and go modestly negative later this year. That would be welcome – better than the status quo – but inadequate, and not commensurate with the scale of the adverse economic shock. In my post the other day I argued that in next week’s Monetary Policy Statement

The MPC on 13 May should:

- abandon the “no change for a year pledge”,

- cut the OCR to zero,

- announce that the OCR will most likely be cut further in June (which would get many of the benefits immediately, but give a little time if there are some real system issues re a negative OCR), and

- commit to have in place by June robust mechanisms that for the time being removed, or greatly eased, the current effective lower bound on short-term wholesale interest rates.

As it happens there have been a few other contributions on monetary policy locally this week.

Yesterday morning I heard the local chief executive of Westpac on RNZ talking about all the system and documentation changes that would be needed – one has to assume he was talking about his bank, as he was quite specific in some cases – to cope with negative (retail?) rates. Unfortunately, the interviewer simply took Mr McLean at his word, and didn’t either challenge him on just how vital these things were or why – with 10 years global notice – a big bank like his appeared to have done nothing before now. (My initial reaction was a bit like that to the Governor – if Mr McLean had spent less time championing all the right-on causes he and the Governor are so fond of – especially climate change – and actually managed his bank, his borrowers might be rather positioned now.) Of course, from a public policy perspective, the bigger question is about years of failure from the Reserve Bank – under Wheeler, his “acting” replacement, and more recently under Orr – to ensure that the banking system could readily cope with the sort of cuts to the OCR that it was easily foreseeable some shock soon might make necessary. In Orr’s case, it is particularly inexcusable given that big interview he gave eight months ago articulating why he favoured negative interest rates as a policy option. “Saving the world” might seem more glamorous, but stabilising the local economy and keeping inflation target was actually his job.

Then there was a strange comment reported from the Leader of the Opposition.

Bridges said fiscal policy, rather than monetary interventions from the Reserve Bank, would need to do the heavy lifting in the Covid-19 response.

That clearly isn’t true – it is simply a choice by the MPC to do nothing, and by the government which does not use clear legal statutory powers to compel them to act differently. Sadly, it is still too much of the conventional wisdom. I’d probably have forgotten about except that this morning Bridges is reported as worrying about risks of too much public debt being taken on. Macro policy squares that circle – delivers accelerated recovery without lots more debt – by using monetary policy: yes, deeply negative rates in this context, to provide the support and stabilisation into the recovery towards full employment. Such, it seems, is the power of conventional wisdom and the fear of successive Oppositions – Robertson in Opposition was quite as bad, in less important circumstances – to challenge anything that the (on their record) not-overly-capable RB/MPC does.

And finally, another reader this morning sent me this clip from a recent BNZ research report, previewing next week’s MPS.

We would strongly argue that lowering the cash rate further would provide almost no assistance to the economy. The cost of debt is the last thing on anyone’s mind now. The lack of availability of debt might be a concern and, for many, the lack of income to repay debt will be a pressing problem. Pushing interest rates sub-zero will do nothing to ameliorate those issues. Moreover, even if the cash rate was to go negative, it would not be fully passed on to borrowers as the banks will still be funding themselves with positive interest rates. Term deposit rates are excruciatingly low for many as it is. The last thing the household sector would want is zero rates across the board. And even at zero, it would mean bank funding costs well above the cash rate.

The research report is headed “RBNZ Can’t Save the World”, to which one can only agree. What it can do – what it is charged with doing – is keep inflation and inflation expectations at around 2 per cent, and support as rapid as possible a return to full employment. At present, those two goals are tightly aligned, given how high unemployment is forecast to be, and how far medium-term inflation expectations have fallen.

Perhaps it as well to remember here that the BNZ has been the most consistently “hawkish” – pro tightenings, often uneasy about easings – of any of the local banks for many years. That has made them more wrong than most.

But that specific extract above simply makes little sense. Sure, most businesses would probably prefer a quick and full rebound in demand/activity over a fall in their debt interest rate, but it isn’t as if the two concerns are in conflict – in fact, lower interest rates and lower exchange rate will, in time, do their bit to support a stronger recovery. And despite the bank economist’s claim that no one much cares about interest rates, the evidence is pretty clearly against that in the very low interest rates being offered on the government’s scheme (and the Opposition’s proposal yesterday). In fact, the worst credits in the country – those who can’t raise funds elsewhere – get the cheapest rates, while deposit rates – in the middle of a savage slump – remain positive in real terms, barely down this year, sending all the wrong signals. And then there is the distraction: as BNZ knows only too well, if the OCR were taken to -0.5 per cent – as Westpac suggests will happen and should happen – retail rates, deposits and lending rates, would be still positive. For now, negative retail rates are some way away.

And if, perchance, depositors were reacting negatively to, say, 1 per cent term deposit rates, what are they going to do instead? Spend the money? Well, that’s good – that is monetary policy working. Shift it to another currency? Well, that’s good – a lower exchange rate would be monetary policy working. Seek to buy another asset? Well, that’s pretty good too – increasing both wealth effects and Tobin’s Q effects encouraging new investment, so that’s monetary policy working. And, of course, in aggregate it is not as if deposits are going anywhere – it is a closed system, with a floating exchange rate. Your purchase is my sale etc etc. Oh, if it makes people worry a bit about future inflation, that’s good too – that’s monetary policy working to hold up, or lift, inflation expectations to something like target.

Like Ken Rogoff, I think the case for deeply negative interest rates now is pretty overwhelming. It would ease the pressure on fiscal policy, it would support the tradables sector (on which our future prosperity rests), it would ease servicing costs on existing borrowers (and bring market rates closer to rates the government itself is happy to lend at). There is nothing particularly odd about negative rates, at a time when savings preferences are high and investment intentions are very weak – the interest rate simply serves to reconcile the two, while getting the economy towards full employment – and in the particular circumstances of New Zealand, a materially negative OCR would be needed to even get retail interest rates close to zero. As it is, recall that New Zealand now has materially higher retail rates than Australia, despite the deeper economic slump. That is a choice – an anti-stabilisation choice – made by the MPC, blessed by the Minister of Finance.