Your main focus today, as mine, may well be this afternoon’s Budget, but I’m not letting the Monetary Policy Committee’s statement yesterday go by without comment.

Back in February, the Committee was really rather upbeat. There was this temporary disruption to some exports to China, but it really wasn’t much to worry about. Once we got beyond that things were looking good this year. In fact, a couple of weeks later they were still singing from that upbeat songbook, tweeting out their upbeat message. It wasn’t just management, but also the silenced ciphers who sit as external members of the Committee, collecting generous fees – no word of any 20 per cent cuts there? – while never being available for questioning or any serious accountability.

Since then, of course, they’ve been mugged by events, but always with the sense that they were never quite taking things seriously enough, never willing to do what might make a real and material difference. So they cut interest rates once, and then firmly pledged not even to think about doing any more of that for another year. They claim to have (very belatedly, given that they had 10 years notice) discovered that some banks weren’t “technically ready” for a negative OCR – a very fishy story, given we heard it nowhere else in the world in the last decade – but even having “discovered” that there appears to be not the slightest urgency to resolving the matter. The government can get in place wage subsidy schemes or company tax clawback schemes paying out within days, but the Reserve Bank is still just asking nicely that could the banks please, please, think about having systems ready by the end of the year – still the best part of eight months away.

I saw one funds manager quoted in the media suggesting that the Bank really wanted to cut the OCR yesterday but just couldn’t. With respect – and I like and generally respect the person concerned – that has to be nonsense. Even if there really really are technical obstacles in one or two banks – and why do no journalists go round and ask them individually? – nothing stopped the Bank cutting the OCR to zero. Nothing would have stopped them letting it be known they’d insisted that any technical obstacles be resolved before the end of June. But there was nothing of the sort.

Instead, there was the repeated pretence that a gigantic asset swap – buying government bonds and issuing government deposits instead (which is what Reserve Bank settlement cash is) – was somehow a fully effective substitute. This little clip is from the cartoon version the Bank does for the general reader (never clear how many of them there are).

So, yesterday’s substantive policy announcement was an 80 per cent increase in the (maximum) amount of government and local body bonds the Bank may buy over the year.

This was my initial reaction

Now as it happens, the exchange rate appears to have fallen by about 1 per cent on yesterday’s statement, and interest rates are down as well. But much of that appears to be not because of the bond purchase programme – which was widely expected – but because of the explicit references to the possibilities of a negative OCR next year. It wasn’t really new, but apparently some must have focused on it afresh, and as a contrast perhaps to the outlook in the US and Australia. Apparently, the OIS market is now pricing negative rates for much of next year. The Governor may get his reported wish and retail interest rates may fall a little.

The bond purchase programme itself, however, remains largely theatre. What isn’t clear is whether the Governor knows it and doesn’t care, or is a true believer. There are hints in the text of the document that the staff know there is less to the programme than the Governor likes to make out.

As I noted in that tweet, there would be a credible case that big bond purchase programmes would make a real macroeconomic difference – what we look for from monetary policy, as a key countercyclical actor – if:

- insufficient settlement cash were an important constraint on banks’ activities, willingness to lend etc. There is no evidence of that at all (and the Bank does not emphasise this channel either),

- a lot of New Zealand borrowing was taking place at long-term fixed interest rates, and the interest rates on those products were significantly linked to interest rates on long-term government bonds.

But that isn’t so either. Most New Zealand borrowing is done either at variable rates – where the OCR is a key influence – or short-term fixed rates (lots of action in the mortgage market tends to centre on 1 or 2 year fixed rates). Even when corporates go out and issue long-term bonds, they typically enter into swaps to shift back to floating rate terms (but with secure long-term funding). The key entity that borrows long-term and is directly exposed to long-term rates is…..the ultimate non-market actor, the government. In fact, it was telling that the MPS specifically claims one of the benefits of the asset purchase programme as being lowering the borrowing costs of the Crown – but monetary policy is generally supposed in a neutral way across all sort of savers/borrowers.

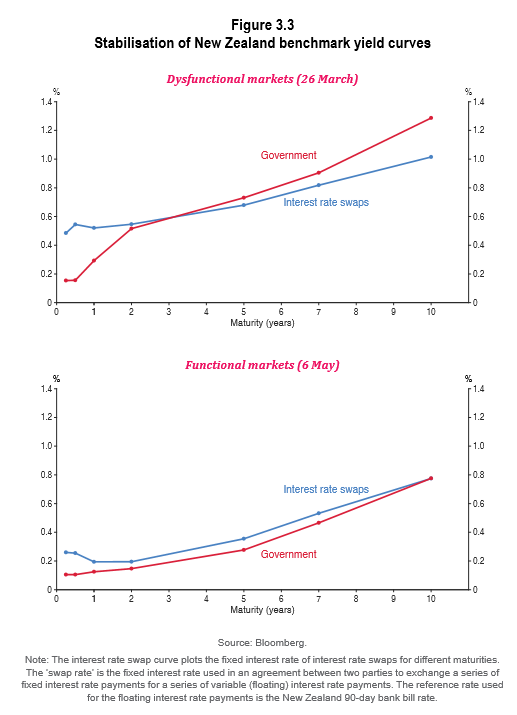

There were a couple of interesting graphs in the MPS which seemed make my point.

In late March, there was a huge sell-off in all sort of asset markets, including global government bond markets. The Bank has another chart nicely illustrating the blow-out in bid-ask spreads (which flowed through to investors more generally). The bond market was not functioning very well, and you can see in the top chart how far long-term government bond rates rose relative to rates on interest rate swaps. But it is the swaps that matter for general credit pricing in the economy, not the bonds themselves. In the second chart, from a few days ago, government bond yields had come right back down again relative to swaps, but the swaps curve itself was only down about 20 basis points.

To repeat, I am not opposed to the Reserve Bank doing a bond purchase programme – although I think they would be more sensible to follow the RBA and focus on targeting a short-term bond rate (say, the three year rate, as per the RBA). Their activities helped stabilise markets – which would probably have settled down eventually anyway – and have lowered bond yields, but the scale of the effect on rates that really matter to the wider economy is small – and not really consistent with the scale of the Bank’s claims.

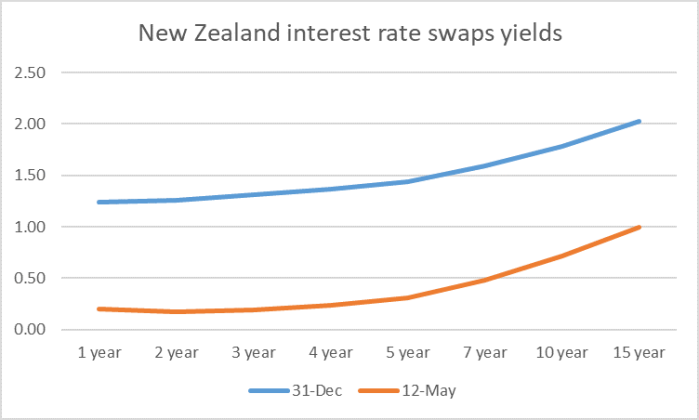

Did I mention real interest rates? Curiously, as far as I could tell in the entire document yesterday there was not a single mention (and certainly not in the upfront material the MPC itself more clearly owned). Here is the interest rate swaps curve for 31 Dec last year and the close of business on Tuesday (with the market then fully expecting a big expansion in the bond purchase programme).

The whole curve is down about 100 basis point since the end of last year. Unfortunately, inflation expectations have fallen about 70 basis points, so that even real wholesale rates have not fallen very much at all. In face of the biggest sharpest slump on record.

As even the Bank acknowledges – a point I’ve made here repeatedly – there has not been that much action on retail rates, and in particular retail deposit rates have not fallen much at all. In fact – the Bank doesn’t point this out – they’ve risen in real terms. The Bank is reduced to plaintive appeals to banks to lower retail lending rates, even as they acknowledge that wholesale term funding costs also remain relatively expensive, in turn influencing what banks are willing to pay for term deposits.

The Bank’s final argument is to claim that the large scale asset purchase programme (LSAP) has reduced the exchange rate. The Governor made that bold claim, while the staff are (rightly) more nuanced.

In addition to lowering interest rates, LSAPs put downward pressure on the New Zealand dollar exchange rate. The New Zealand dollar has depreciated in response to the COVID-19 outbreak (see chapter 4). It is difficult to disentangle the precise impacts of the Reserve Bank’s actions from a range of other factors that influence the exchange rate, in particular the volatile swings in risk sentiment over recent months and the actions of overseas central banks.

In principle, if the Reserve Bank has bought $10 billion of so of bonds, some of the sellers will have been foreign holders. Some of them will have been unhedged holders of NZD, and they may now have closed out those positions. But when the Governor and Bank were making these claims, the TWI was about 5 per cent below where it had been late last year, in total, from all influences. Perhaps the LSAP had an effect at the margin, but if so it must have been relatively small, since the overall movement in the TWI was small relative to past, less severe recessions, and our overall yield curve is still not extremely low by international standards.

To repeat, I’m not suggesting the LSAP has had no effect, just that relative to the scale of the challenge – the collapse in economic activity, employment and prospects for inflation – what has been done is just not remotely comparable to the scale of monetary easing that a serious central bank would normally have done previously.

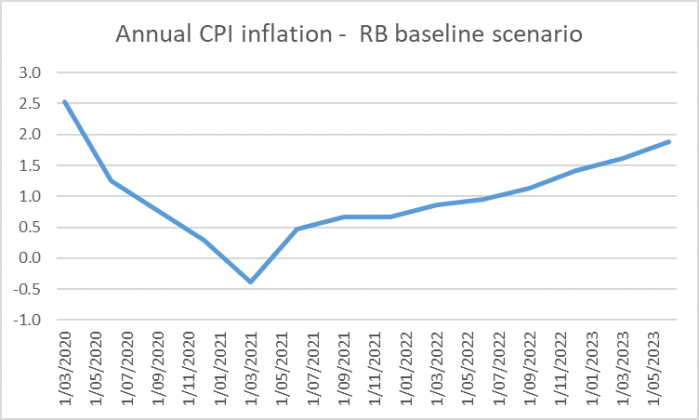

And, actually, once you dig just a little into their numbers, even they tell you as much. I reckon the Bank’s baseline scenario is rather too optimistic about the extent of the economic recovery, on current policies, over the next few years. Their view on the unemployment rate in particular seems almost incomprehensibly optimistic on announced policy as at yesterday (which is what they said they were basing things on) But even if one takes them at their word, this is their inflation outlook.

Under the Remit given to them, the MPC is required to focus on the 2 per cent midpoint of the target range. The bottom of the target range is 1 per cent. They now expect annual inflation to be below 1 per cent for the next two years, on current policy. At the end of 2022, on these projections inflation is still only 1.3 per cent, about as low – core inflation terms – as it ever got in the last 10 years. I’m almost certain that the Bank has never published inflation projections that have annual inflation outside the target range for so long. And it is not as if somehow there is overfull employment during this forecast horizon – even on the (optimistic) Reserve Bank numbers, the unemployment rate is still 5.5 per cent three years from now.

It is really pretty inexcusable. The MPC is keen to shift responsibility onto the government, claiming that fiscal policy has to carry the load. But MPC has been given a task by Parliament and the Minister and are just abdicating responsibility for it.

The related thing I find troubling is that while the MPC acknowledges that the risks are to the downside, there is no sustained discussion of inflation expectations at all. Neither the word nor the notion appear in the minutes of the committee’s deliberations. I was talking to someone yesterday who told me he’d searched the document and the word “deflation” didn’t appear at all, and there is no hint of the Committee being alert to the risks, or even highlighting the powerfully deflationary nature of this shock. If inflation expectations have already fallen so much, and yet the Committee is now content to deliver inflation below target for several years, isn’t it likely that expectations will fall even further? Given the self-imposed limits on nominal interest rates, doesn’t that create a risk of further retarding the recovery, by driving up real interest rates? Whether it does or not, you’d expect a serious MPC to at least engage with these sorts of issues and risks?

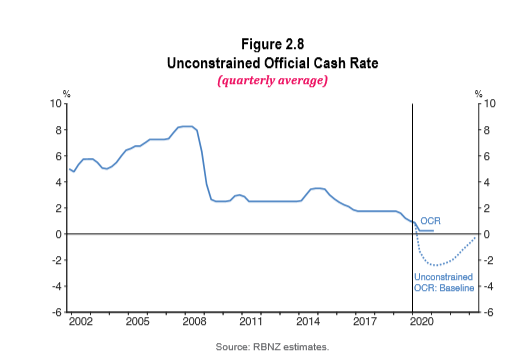

The unseriousness of it all was perhaps highlighted by this new chart, showing some sense of where the OCR might go if there were no (self-imposed) constraints.

Something like -2 per cent would certainly be a great better than we have now (0.25 per cent, with a bit of help from the LSAP), but that would still amount to only 300 basis points of monetary policy easing – small compared to 2008/09 or to 1990/91, even though the adverse shock this time is almost certainly much larger. As I’ve noted before there were standard Taylor rule estimates for the US in 2008/09 suggesting that even then -5 per cent interest rates would have been helpful (although clearly not critical as the economy eventually recovered without them). And I noticed yesterday one of investment banks estimating that for Australia – with a less severe economic shock than New Zealand – something like -5 per cent might be a Taylor rule recommendation now. As it is, we have a tiny – quite inadequate – easing in real monetary conditions.

The MPC and the Governor are simply not taking things anything like sufficiently seriously. They’ve deferred to fiscal policy, claiming (not very credibly) no inside knowledge of today’s Budget, but (a) it is four months from an election and who knows what fiscal policy will actually be delivered over time, and (b) as noted above, even with all that support, inflation still materially undershoots the target they have been formally given.

Finally, of course, there is no suggestion that the MPC is interested in doing anything at all to ease the rules – imposed the Bank – that create something like an effective lower bound (modestly negative) on nominal interest rates. That is just irresponsible. If the MPC won’t act, the Board should insist. If they can’t make any headway – or, more likely, won’t even try – the Minister needs to act. At present, the MPC appears to be frustrating the clear intentions of Parliament and the Minister – price stability with monetary policy doing all it can to support maximum sustainable employment. Laws are written to provide remedies for these exceptional circumstances. If the Minister refuses to use them, he shares the blame.

For his Zoom press conference yesterday, the Governor was flanked – excuse the grainy photo – by his billboard boasting of/aspiring to being “Best Central Bank”

You be the judge. But however well the people down the organisations are doing, the statutory appointees – those we are supposed to be able to hold to account – are again/still falling well short, led by the Governor.