Your main focus today, as mine, may well be this afternoon’s Budget, but I’m not letting the Monetary Policy Committee’s statement yesterday go by without comment.

Back in February, the Committee was really rather upbeat. There was this temporary disruption to some exports to China, but it really wasn’t much to worry about. Once we got beyond that things were looking good this year. In fact, a couple of weeks later they were still singing from that upbeat songbook, tweeting out their upbeat message. It wasn’t just management, but also the silenced ciphers who sit as external members of the Committee, collecting generous fees – no word of any 20 per cent cuts there? – while never being available for questioning or any serious accountability.

Since then, of course, they’ve been mugged by events, but always with the sense that they were never quite taking things seriously enough, never willing to do what might make a real and material difference. So they cut interest rates once, and then firmly pledged not even to think about doing any more of that for another year. They claim to have (very belatedly, given that they had 10 years notice) discovered that some banks weren’t “technically ready” for a negative OCR – a very fishy story, given we heard it nowhere else in the world in the last decade – but even having “discovered” that there appears to be not the slightest urgency to resolving the matter. The government can get in place wage subsidy schemes or company tax clawback schemes paying out within days, but the Reserve Bank is still just asking nicely that could the banks please, please, think about having systems ready by the end of the year – still the best part of eight months away.

I saw one funds manager quoted in the media suggesting that the Bank really wanted to cut the OCR yesterday but just couldn’t. With respect – and I like and generally respect the person concerned – that has to be nonsense. Even if there really really are technical obstacles in one or two banks – and why do no journalists go round and ask them individually? – nothing stopped the Bank cutting the OCR to zero. Nothing would have stopped them letting it be known they’d insisted that any technical obstacles be resolved before the end of June. But there was nothing of the sort.

Instead, there was the repeated pretence that a gigantic asset swap – buying government bonds and issuing government deposits instead (which is what Reserve Bank settlement cash is) – was somehow a fully effective substitute. This little clip is from the cartoon version the Bank does for the general reader (never clear how many of them there are).

So, yesterday’s substantive policy announcement was an 80 per cent increase in the (maximum) amount of government and local body bonds the Bank may buy over the year.

This was my initial reaction

Now as it happens, the exchange rate appears to have fallen by about 1 per cent on yesterday’s statement, and interest rates are down as well. But much of that appears to be not because of the bond purchase programme – which was widely expected – but because of the explicit references to the possibilities of a negative OCR next year. It wasn’t really new, but apparently some must have focused on it afresh, and as a contrast perhaps to the outlook in the US and Australia. Apparently, the OIS market is now pricing negative rates for much of next year. The Governor may get his reported wish and retail interest rates may fall a little.

The bond purchase programme itself, however, remains largely theatre. What isn’t clear is whether the Governor knows it and doesn’t care, or is a true believer. There are hints in the text of the document that the staff know there is less to the programme than the Governor likes to make out.

As I noted in that tweet, there would be a credible case that big bond purchase programmes would make a real macroeconomic difference – what we look for from monetary policy, as a key countercyclical actor – if:

- insufficient settlement cash were an important constraint on banks’ activities, willingness to lend etc. There is no evidence of that at all (and the Bank does not emphasise this channel either),

- a lot of New Zealand borrowing was taking place at long-term fixed interest rates, and the interest rates on those products were significantly linked to interest rates on long-term government bonds.

But that isn’t so either. Most New Zealand borrowing is done either at variable rates – where the OCR is a key influence – or short-term fixed rates (lots of action in the mortgage market tends to centre on 1 or 2 year fixed rates). Even when corporates go out and issue long-term bonds, they typically enter into swaps to shift back to floating rate terms (but with secure long-term funding). The key entity that borrows long-term and is directly exposed to long-term rates is…..the ultimate non-market actor, the government. In fact, it was telling that the MPS specifically claims one of the benefits of the asset purchase programme as being lowering the borrowing costs of the Crown – but monetary policy is generally supposed in a neutral way across all sort of savers/borrowers.

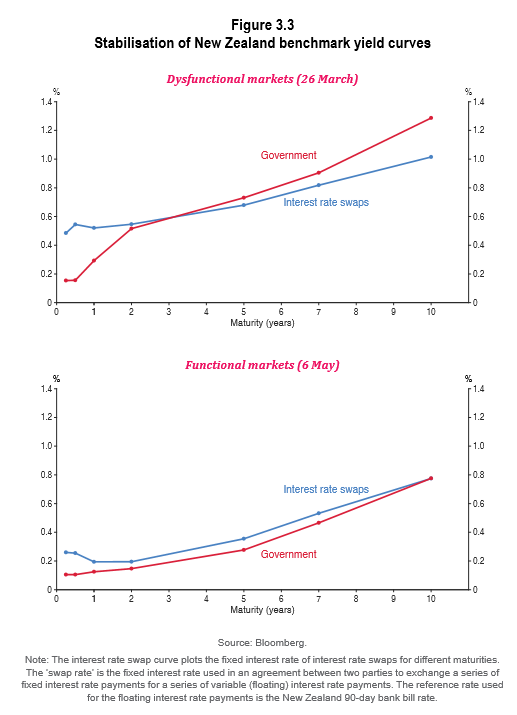

There were a couple of interesting graphs in the MPS which seemed make my point.

In late March, there was a huge sell-off in all sort of asset markets, including global government bond markets. The Bank has another chart nicely illustrating the blow-out in bid-ask spreads (which flowed through to investors more generally). The bond market was not functioning very well, and you can see in the top chart how far long-term government bond rates rose relative to rates on interest rate swaps. But it is the swaps that matter for general credit pricing in the economy, not the bonds themselves. In the second chart, from a few days ago, government bond yields had come right back down again relative to swaps, but the swaps curve itself was only down about 20 basis points.

To repeat, I am not opposed to the Reserve Bank doing a bond purchase programme – although I think they would be more sensible to follow the RBA and focus on targeting a short-term bond rate (say, the three year rate, as per the RBA). Their activities helped stabilise markets – which would probably have settled down eventually anyway – and have lowered bond yields, but the scale of the effect on rates that really matter to the wider economy is small – and not really consistent with the scale of the Bank’s claims.

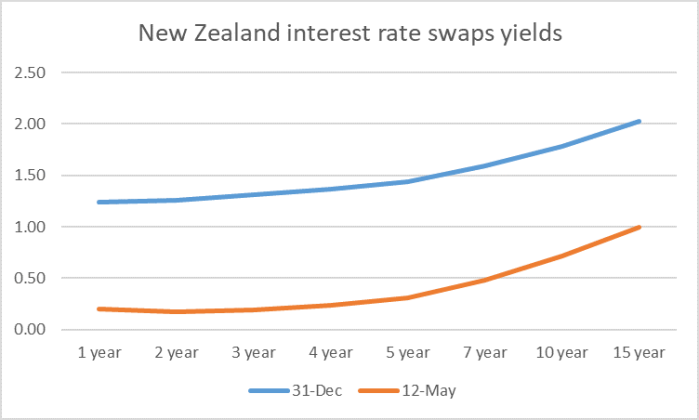

Did I mention real interest rates? Curiously, as far as I could tell in the entire document yesterday there was not a single mention (and certainly not in the upfront material the MPC itself more clearly owned). Here is the interest rate swaps curve for 31 Dec last year and the close of business on Tuesday (with the market then fully expecting a big expansion in the bond purchase programme).

The whole curve is down about 100 basis point since the end of last year. Unfortunately, inflation expectations have fallen about 70 basis points, so that even real wholesale rates have not fallen very much at all. In face of the biggest sharpest slump on record.

As even the Bank acknowledges – a point I’ve made here repeatedly – there has not been that much action on retail rates, and in particular retail deposit rates have not fallen much at all. In fact – the Bank doesn’t point this out – they’ve risen in real terms. The Bank is reduced to plaintive appeals to banks to lower retail lending rates, even as they acknowledge that wholesale term funding costs also remain relatively expensive, in turn influencing what banks are willing to pay for term deposits.

The Bank’s final argument is to claim that the large scale asset purchase programme (LSAP) has reduced the exchange rate. The Governor made that bold claim, while the staff are (rightly) more nuanced.

In addition to lowering interest rates, LSAPs put downward pressure on the New Zealand dollar exchange rate. The New Zealand dollar has depreciated in response to the COVID-19 outbreak (see chapter 4). It is difficult to disentangle the precise impacts of the Reserve Bank’s actions from a range of other factors that influence the exchange rate, in particular the volatile swings in risk sentiment over recent months and the actions of overseas central banks.

In principle, if the Reserve Bank has bought $10 billion of so of bonds, some of the sellers will have been foreign holders. Some of them will have been unhedged holders of NZD, and they may now have closed out those positions. But when the Governor and Bank were making these claims, the TWI was about 5 per cent below where it had been late last year, in total, from all influences. Perhaps the LSAP had an effect at the margin, but if so it must have been relatively small, since the overall movement in the TWI was small relative to past, less severe recessions, and our overall yield curve is still not extremely low by international standards.

To repeat, I’m not suggesting the LSAP has had no effect, just that relative to the scale of the challenge – the collapse in economic activity, employment and prospects for inflation – what has been done is just not remotely comparable to the scale of monetary easing that a serious central bank would normally have done previously.

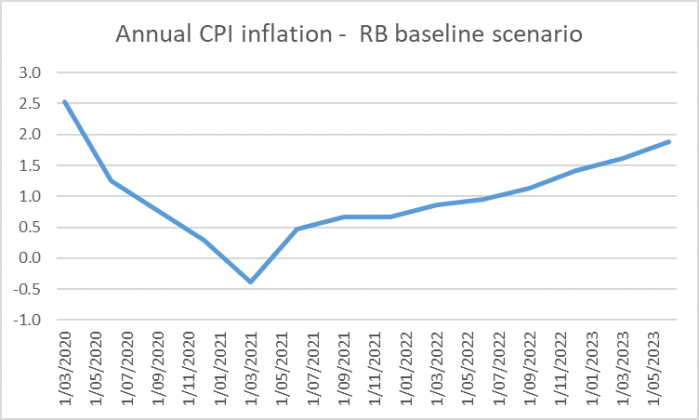

And, actually, once you dig just a little into their numbers, even they tell you as much. I reckon the Bank’s baseline scenario is rather too optimistic about the extent of the economic recovery, on current policies, over the next few years. Their view on the unemployment rate in particular seems almost incomprehensibly optimistic on announced policy as at yesterday (which is what they said they were basing things on) But even if one takes them at their word, this is their inflation outlook.

Under the Remit given to them, the MPC is required to focus on the 2 per cent midpoint of the target range. The bottom of the target range is 1 per cent. They now expect annual inflation to be below 1 per cent for the next two years, on current policy. At the end of 2022, on these projections inflation is still only 1.3 per cent, about as low – core inflation terms – as it ever got in the last 10 years. I’m almost certain that the Bank has never published inflation projections that have annual inflation outside the target range for so long. And it is not as if somehow there is overfull employment during this forecast horizon – even on the (optimistic) Reserve Bank numbers, the unemployment rate is still 5.5 per cent three years from now.

It is really pretty inexcusable. The MPC is keen to shift responsibility onto the government, claiming that fiscal policy has to carry the load. But MPC has been given a task by Parliament and the Minister and are just abdicating responsibility for it.

The related thing I find troubling is that while the MPC acknowledges that the risks are to the downside, there is no sustained discussion of inflation expectations at all. Neither the word nor the notion appear in the minutes of the committee’s deliberations. I was talking to someone yesterday who told me he’d searched the document and the word “deflation” didn’t appear at all, and there is no hint of the Committee being alert to the risks, or even highlighting the powerfully deflationary nature of this shock. If inflation expectations have already fallen so much, and yet the Committee is now content to deliver inflation below target for several years, isn’t it likely that expectations will fall even further? Given the self-imposed limits on nominal interest rates, doesn’t that create a risk of further retarding the recovery, by driving up real interest rates? Whether it does or not, you’d expect a serious MPC to at least engage with these sorts of issues and risks?

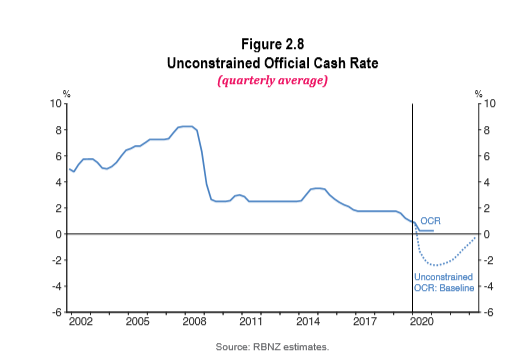

The unseriousness of it all was perhaps highlighted by this new chart, showing some sense of where the OCR might go if there were no (self-imposed) constraints.

Something like -2 per cent would certainly be a great better than we have now (0.25 per cent, with a bit of help from the LSAP), but that would still amount to only 300 basis points of monetary policy easing – small compared to 2008/09 or to 1990/91, even though the adverse shock this time is almost certainly much larger. As I’ve noted before there were standard Taylor rule estimates for the US in 2008/09 suggesting that even then -5 per cent interest rates would have been helpful (although clearly not critical as the economy eventually recovered without them). And I noticed yesterday one of investment banks estimating that for Australia – with a less severe economic shock than New Zealand – something like -5 per cent might be a Taylor rule recommendation now. As it is, we have a tiny – quite inadequate – easing in real monetary conditions.

The MPC and the Governor are simply not taking things anything like sufficiently seriously. They’ve deferred to fiscal policy, claiming (not very credibly) no inside knowledge of today’s Budget, but (a) it is four months from an election and who knows what fiscal policy will actually be delivered over time, and (b) as noted above, even with all that support, inflation still materially undershoots the target they have been formally given.

Finally, of course, there is no suggestion that the MPC is interested in doing anything at all to ease the rules – imposed the Bank – that create something like an effective lower bound (modestly negative) on nominal interest rates. That is just irresponsible. If the MPC won’t act, the Board should insist. If they can’t make any headway – or, more likely, won’t even try – the Minister needs to act. At present, the MPC appears to be frustrating the clear intentions of Parliament and the Minister – price stability with monetary policy doing all it can to support maximum sustainable employment. Laws are written to provide remedies for these exceptional circumstances. If the Minister refuses to use them, he shares the blame.

For his Zoom press conference yesterday, the Governor was flanked – excuse the grainy photo – by his billboard boasting of/aspiring to being “Best Central Bank”

You be the judge. But however well the people down the organisations are doing, the statutory appointees – those we are supposed to be able to hold to account – are again/still falling well short, led by the Governor.

The fall in the kiwi was most definitely due to negative rates comments. Only three companies I know of have been calling for negative rates, mine being one of them. All the rest have held the line at 0.25%.

Absent the comment, kiwi wouldn’t have fallen, nor would front end rates.

LikeLiked by 1 person

The NZD fell to 0.55 against the USD when 0.75% was cut in the OCR. It is now back to 0.60c within a few weeks. The rest of the world is also economically impacted. NZD value is all relative to what Currency speculators believe and nothing really much to do with interest rates going negative or not.

LikeLike

Hi Michael,

The PM says she’s taken a 20% pay cut – and enjoyed all the benefits of that publicity – yet as far as I can see on Scoop, it hasn’t happened yet with Grant Robertson and then Chris Hipkins objecting and blocking the legislation.

Yet the cut in pay is 20% on salary for a 6 month period. The PM received $471,049 pa in salary and another $22,600 in allowance. She also receives significant non-salary perks such as flights, meals, a chauffeur driven car and Vogel House. Assuming Vogel house rents for say $2k/week, a car and driver costs say $100k and meals and flights another $100k, this gives her about $250k in non salary expenses.

So her salary deduction for 6 months is $47,104 but her total all in package is $743,650. So her pay cut – if it’s ever passed – amounts to the grand total of 6.3%!

My figures are chicken scratches over the dinner table so my numbers may not be precise, but I think they’re indicative.

Don’t get me wrong, I think it was an appropriate gesture, but it’s not 20%, and it’s not been enacted.

Funny how they can pass legislation allowing police to walk into my home without a warrant but they can’t do this.

LikeLiked by 1 person

It is astonishing mismanagement (execution having been a key weakness of the govt) not to have ensured this was effected immediately. I’m pretty sure the cuts head of govt depts took, and many other pte sector workers had little choice but to take, have been put into effect.

I am a bit surprised no journalist has asked whether Adrian and Geoff are taking a cut.

LikeLike

incidentally, i think you are overvaluing the package. the flat at Premier House won’t be worth anything like $2000 per week, and for the PM accommodation in Wgtn – and flights – is more like work-related expenses, normally reimburseable, than remuneration.

LikeLike

Agreed the PM pay is less than $500k a year. Now Watercare CEO is on $770k a year. That is a crazy amount of money for a civil servant that really does not do much when it is a monopoly with no competition and no accountability to the ratepayers. Watercare CEO pay is just ridiculous. Whoever agreed and authorised that pay level should be sacked immediately.

LikeLiked by 1 person

Cabinet ministers have already had their pay cut as have the CEs in the Public Service.

http://www.legislation.govt.nz/bill/government/2020/0266/latest/LMS345153.html is the Bill to allow the reduction of salaries in other CEs outside the Public Service as well as MPs and councillors (including mayors).

LikeLike

Hi Michael,

– maybe there’s not much private sector borrowers in the longer part of the curve, but isn’t there an argument that lowering longer term govt bond yields should flow into equity prices and cost of capital, which in turn will lower the hurdle rate for longer term investment.

– i think the increased settlement cash in the system has likely reduced short term money market rates (bkbm) which a lot of borrowings are priced off either directly or via the swap market.

Thanks,

Ben

LikeLike

Hi Ben

Re the short-end, yes I agree RB actions prob helped get short rates back into line with the OCR (may have got there in time anyway as things settled down, but it helped) – altho it won’t have taken another $20bn of settlement cash to do that.

On the share market, yes I had really thought of that channel (consistent with how little equity market developments tend to play in thinking about the macro economy in NZ). Perhaps there is something to that channel, altho again it is likely to be a weaker effect here than in, say, the US.

In the end, the bond purchase programme has prob been slightly helpful macroeconomically, but on nothing like the scale the situations really calls for – the more so given the extent of the fall in infl expectations.

LikeLike

Keep up the pressure. I think you are getting traction. Hard to know why this is not a main stream issue, good or bad.

LikeLiked by 1 person

What struck me yesterday was the feeling that the Gov was not actually over all the issues. I understand that he wanted to bring his team into the discussion however I came away from the P.Conference that 1. He didn’t appear to have a good gasp/technical ability on some of the issues/questions at hand and 2. He needed to show more leadership by answering the questions and only deferring as/when required.

Look at Powell at the FOMC – it’s him and him alone facing the questons. He does not require 3 off-siders and is able to answer questions as required.

LikeLike

I think Orr is relatively weak technically, but there is also the Rb corporate culture to consider, which has always tried to be quite inclusive like that. Mostly I think that is a good thing if there is a really strong top team. Unfortunately of the four internals on MPC, only one really begins to reach that standard.

LikeLike

Being technically correct does not equate to being practically correct. So far I have only good things to say about Adrian Orr’s pragmatic approach. The solutions and actions so far has been thought through and practical. The property market so far is rock solid. The sharemarket after a massive drop is recovering and with retail investors piling in, including myself now with $60k invested from zero prior to lockdown.

Back to work and had my first cooked sushi sandwich from a shop in the city after almost 7 weeks of lockdown and tonight it is a dinner date in a restaurant. Time to spend some dollars to support the hospitality sector. I am totally happy to be out of the house. It got rather hard towards Wednesday. Anyone who says working from home is more productive has rocks in their brain. I think dementia was starting to set in real quick in the final 3 days

LikeLike

Yes I thought it was weird the RBNZ was forecasting inflation below its target yet not telling us what it was going to do differently. Very much the elephant in the room of the MPS

LikeLike

What I really dont understand is – how did they determine their LSAP quantity? Surely if they think that LSAP is sufficient to do the job of keeping inflation at target, they would announce a sufficient quantity to do so. If the calculation of $60b gave them deflation then below target inflation for several years based on their own model, why did they stop there? Why not $600b?

LikeLike

The scale of the money print is important. If you want to shift NZD around with a wheelbarrow to buy a loaf of bread then certainly go ahead and print $600 billion. The Japanese during WW2 printed huge amounts of Japanese war bond related Yen issued freely to conquered countries in the Pacific. No one wanted it. It was called banana money, worthless.

LikeLike

Yes but there are intermediate points between hyperinflation and their projected deflation. Including their policy target that they are supposedly committed to.

LikeLike

Personally, I am thinking printing $50 billion is a good number relative to the size of our $280 billion economy. Currency traders will be taking a global view because our currency is relative to what the others countries are doing. The NZD at 40% discount to the USD and 45% discount to the Euro keeps our export products cheaper to access the China and Asia markets and already considered as borderline product dumping in the US and European markets. That is why we can’t get and FTA with the US and Europe since our privilege position into Europe through UK has lapsed with Brexit.

LikeLike

It doesnt really matter what the amount of QE is, what matters is whether they use monetary policy to keep inflation at 2%. They are failing to do that, but havent explained why they think thats ok. If they credibly committed to doing whatever it takes to keep inflation at 2% (including negative rates), a lesser amount of actual QE etc might be required. As it stands they have done the opposite. They have published an MPS with below target inflation. Given their past performance, they have very credibly committed to “doing what it takes” to have an extended period of low inflation and high unemployment.

LikeLike

Super efficient mega distribution retail chain stores like The Warehouse, K-Mart and Walmart move low cost products from mega chinese factories into the hands of consumers. No amount of Mon Pol is going to change that. I thought Warehouse products were cheap, but if you wander into K-mart you’ll be surprised that similar products are even cheaper but the Warehouse is much better represented in the community. Walmart wants to get into our market as well so they believe they can compete likely with even cheaper consumer products.

Hot on the heels of China mega factories are now India and Vietnam. Indonesia is now also making a play for cheaper products than China can produce.

LikeLike

They have been quoted as saying they don’t want to hold more than about half the bonds on issue. I don’t have a strong view on the merits of that, but note that the RBA approach – explicitly targeting the three year rate – appears to have allowed them to scale back their bond purchases. They never had a quantity specified, just a “whatever it takes”.

Sadly, I haven’t seen any journalists ask them the question of why not do more if projected inflation is persistently below target.

LikeLike

Projected inflation is persistently below target because China’s mega factories are mass producing at a massive scale that has imported deflation throughout the world. On the heels of China are India and Vietnam hoping to copy China’s economic model of mega factories. Any sign of price inflation and the super efficient distribution chains like The Warehouse or K-mart or Walmart are building brand new outlet stores to shift products from Chinese factories at cheaper and cheaper prices. Motto of these mega retail stores is, you manufacture it cheaper and I will sell it for you.

LikeLike

Hi Michael – a quick question on LSAP and inflation. I heard somebody on Nine to Noon suggesting that one of the main effects of QE is inflation in financial asset prices (rather than the consumer inflation measured by CPI), benefitting the already-wealthy. Your thoughts?

LikeLike

It was an argument used in the US for much of the last decade. The LSAP certainly boosts bond prices. The equity market channel is less significant here than in much of the world, but to the extent it is a channel here it certainly tends to favour first the existing wealthy.

The key problem is that whatever it is doing, it isn’t doing much for demand or employment.

LikeLike

+1 on negative rates.

NZ needs to innovate.

A yield curve with -5% OCR & 2%+risk free return at the long end would help drive risk taking & allow debt reduction for those able to borrow at the short end.

It really should be coupled with a comprehensive capital gains tax to focus the productive use of money rather than blowing more asset bubbles.

Point of interest – if term deposits turn negative does that become a tax credit or simply a capital loss?

LikeLike

Interesting question (your final point). I don’t know the answer at all.

LikeLike

Tax Deduction

LikeLike

If it shows up as negative interest rates paid or as bank charges then it would be a tax deduction.

LikeLike

Equivalent to a Trading Loss – negative revenue

LikeLike

The thing that gets me is the dissonance between the Governor’s view and the staff view… its almost like he is an external commentator on what the staff are saying down in the detail… this is most surprising – neither has the other’s back… either he doesn’t understand it or the staff are wrong, yet the difference in view is allowed into the public arena… why??

The end can’t come soon enough for the Governor’s reign… its has been a major disappointment.

LikeLike

Reign? I would have thought what is needed is more like a good butler – invisible, self-effacing but the work gets done quietly. Is that why they are called public servants?

LikeLike

I agree, RBNZ governors should not be superstars. They are there to ensure banks are stable and the NZD is stable so that we can actually buy our cheap deflationary products. Both of which are rock solid at this time.

LikeLike

Michael, just so I have this correct, are you saying you ‘want’ the RBNZ to aggressively go to -2-5% OCR? Regardless of mandated inflation targets if so…what kind of message would that send to “main st”?

LikeLike

No, the key point here is not “regardless”, but “consistent with”. The Bank itself is forecasting that it will fail to meet its inflation targets, which is a strong prima facile argument for a looser monetary policy for a time. A better world might be one in which an OCR of, say,+2% was warranted but for now that isn’t the world we live in.

The message would be that “we are passionate about getting the economy back to full employment and keeping inflation close to 2%.

LikeLike

Given the demand/health shock, tend to think the situation is one where “borrowers don’t want to borrow; lenders don’t want to lend” so the government has to do the spending – at least initially (and preferably efficiently).

Relying on negative interest rates to spur demand and enable the resurrection of positive real interest rates, I think, overlooks the spending of money as a much more powerful impulse than its price.

LikeLike

Lenders do want to lend to residential property owners. With a phone call I did manage to secure $30k in emergency Overdraft at 2.9% interest rate. The tenant it was supposed to have covered decided they will keep paying their rents. I have therefore invested that $30k plus another $40k also from existing OD accounts into the NZX.

It is really the businesses. hotels and retail properties that struggle to get a loan

LikeLike