How long have I been banging on about the potential limitations of monetary policy in the next recession and issues around negative interest rates? The first such post I could find on the blog was almost five years ago to the day, and as I’ve noted previously it had been a concern for some time before, going back to 2010 in the wake of the last serious recession and then the internal working group I chaired at the Bank when Alan Bollard rightly was concerned about downside risks at the height of the euro crisis. (That was the report, adopted by senior management, which recommended that steps be taken to ensure that banks could operate effectively with negative interest rates.)

Ken Rogoff has been writing about such issues, and publishing in various prestigious fora, for at least as long. And Rogoff is a Professor of Economics at Harvard and also served as Chief Economist at the IMF for a couple of years. He and Carmen Reinhart wrote the book This Time is Different: Eight Centuries of Financial Folly that attracted so much attention in the wake of the 2008/09 crisis. As I noted in a post a couple of years ago he and another former IMF chief economist Olivier Blanchard proposed dealing with the lower bound issues by raising inflation targets (the suggestion at the time was to something like 4 per cent), which would – if successful – raise neutral nominal interest rates and provide more policy leeway in the next recession.

In the last few years his focus has shifted to addressing the lower-bound issues at source. There was his 2016 book The Curse of Cash which I wrote about here in which – among other issues physical cash raises – he addressed the lower bound issues and proposed to address them in part by progressively removing higher denomination banknotes, leaving in time nothing higher than a $20 note. More recently still there have been various papers, including last year’s paper (with a PhD student co-author) “The Case for Implementing Effective Negative Interest Rate Policy”. And there have been a couple of short papers in recent weeks. There was a piece on Voxeu by Rogoff and LIlley about three weeks ago. This was the abstract

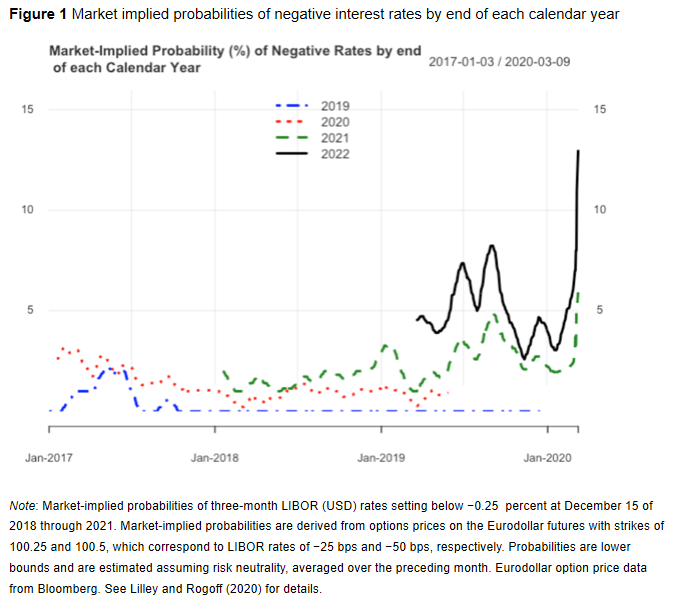

In the aftermath of the Global Crisis, conventional monetary policy has been constrained by low interest rates in many major economies. This has spurred debates on the possibility of introducing negative interest rates in the monetary policy toolkit. This column uses evidence from the US to show that not only do the markets expect the low interest rates to persist into the future, but they also expect the use of negative interest rates down the line. Moreover, markets no longer believe that even quantitative easing can bring inflation to target, which leaves very few alternatives for monetary policy apart from negative interest rates.

As here, breakeven measures of implied inflation expectations in the US are now well below target. There is a nice chart for the US suggesting that (at least then) markets there had already moved to put a non-trivial probability on materially negative short-term interest rates in the next couple of years.

Focusing on the medium-term implied inflation expectations they note that this

…suggests that the market’s change in beliefs has moved beyond the present crisis, and it now has re-evaluated the extent to which it expects the Fed to be constrained more generally. One problem with such a scenario is that it poses a perverse feedback loop. As the Fed becomes more constrained by the zero lower bound, the expected inflation rate falls, lowering the neutral nominal interest rate, which in turn makes the zero lower bound more binding.

Very much the same point I’ve been making here.

This week Rogoff has a very accessible piece on Project Syndicate (thanks to a reader for drawing it to my attention) under the simple and stark heading “The Case for Deeply Negative Interest Rates”. His summary

Only monetary policy addresses credit throughout the economy. Until inflation and real interest rates rise from the grave, only a policy of effective deep negative interest rates, backed up by measures to prevent cash hoarding by financial firms, can do the job.

Some of the emphases are a bit different in a US context (where much of government at all tiers is highly indebted)

For starters, just like cuts in the good old days of positive interest rates, negative rates would lift many firms, states, and cities from default. If done correctly – and recent empirical evidence increasingly supports this – negative rates would operate similarly to normal monetary policy, boosting aggregate demand and raising employment. So, before carrying out debt-restructuring surgery on everything, wouldn’t it better to try a dose of normal monetary stimulus?

More generally

It is not rocket science (or should I say virology?). With large-scale cash hoarding taken off the table, the issue of pass-through of negative rates to bank depositors – the most sensible concern – would be eliminated. Even without preventing wholesale hoarding (which is risky and expensive), European banks have increasingly been able to pass on negative rates to large depositors.

Some issues are relevant to the US and the euro-area but not in same form to us

A policy of deeply negative rates in the advanced economies would also be a huge boon to emerging and developing economies, which are being slammed by falling commodity prices, fleeing capital, high debt, and weak exchange rates, not to mention the early stages of the pandemic. Even with negative rates, many countries would still need a debt moratorium. But a weaker dollar, stronger global growth, and a reduction in capital flight would help, especially when it comes to the larger emerging markets.

In our case, a much lower exchange rate would make a material difference to the fortunes and prospects of the tradables sector.

Rogoff ends

Emergency implementation of deeply negative interest rates would not solve all of today’s problems. But adopting such a policy would be a start. If, as seems increasingly likely, equilibrium real interest rates are set to be lower than ever over the next few years, it is time for central banks and governments to give the idea a long, hard, and urgent look.

From which I’d depart only in replacing that “long” in the final line with a “short and intense” – this isn’t the time for year-long reviews, but for early and decisive action (as has been managed on so many other fronts in recent months).

There has been a view in some quarters over the last few years that negative interest rates don’t work (in the sense of boosting demand, credit, inflation or whatever) and could actually be contractionary in their effect. I’ve been sceptical of that, but also inclined to wonder whether results for slightly negative interest rates – where there might be threshold effects – would generalise to deeply negative wholesale and policy rates. Rogoff links to a recent paper, newly updated last month, by several researchers mostly at the ECB which uses very disaggregated data to suggest that actually negative interest rates in Europe have worked. Their abstract is as follows

Exploiting confidential data from the euro area, we show that sound banks pass on negative rates to their corporate depositors without experiencing a contraction in funding and that the degree of pass-through becomes stronger as policy rates move deeper into negative territory. The negative interest rate policy provides stimulus to the economy through firms’ asset rebalancing. Firms with high cash-holdings linked to banks charging negative rates increase their investment and decrease their cash-holdings to avoid the costs associated with negative rates. Overall, our results challenge the common view that conventional monetary policy becomes ineffective at the zero lower bound.

The channels they examine look to work a little differently with negative than with positive rates, but not less effectively.

Another central bank with significant experience with mildly negative rates in Sweden’s Riksbank. A year or so ago, a couple of Riksbank researchers published an accessible treatment of the Swedish experience, from a top-down perspective. They summarise their results (with all sorts of caveats in the body of the paper) this way

It has been suggested that the response of bank lending rates to interest rate cuts may become weaker when the policy rate passes below a certain level. This column argues that in the case of Sweden, the pass-through of policy rate cuts below zero to the economy has been reasonably good and monetary policy has been effective even at negative policy rate levels.

As all researchers in this area recognise, a big problem is that limited data. Only a few central banks have had negative policy rates, almost entirely in a single economic cycle, and none of them have taken the policy rate very deeply negative and dealt directly to the ability for big players to convert into physical cash. So we cannot say with certainty what would happen if we took the – fairly straightforward – steps that would enable the OCR to be cut to -3 or -5 per cent. But the signs look fairly promising, whether on the limited experience we have, or pretty basic economic theory (all else equal, holding New Zealand dollars will typically be much less attractive if NZD assets are earning a lot less than those in other countries). And the idea of simply letting the Reserve Bank sit on its hands and do almost nothing that matters macroeconomically (hand-waving around big bond purchase programmes is mostly a distraction in macroeconomic terms, whatever value it might initially have added to market functioning).

You’ll recall that Westpac’s economists last week came out picking that the MPC will abandon its firm pledge not to cut the OCR further and go modestly negative later this year. That would be welcome – better than the status quo – but inadequate, and not commensurate with the scale of the adverse economic shock. In my post the other day I argued that in next week’s Monetary Policy Statement

The MPC on 13 May should:

- abandon the “no change for a year pledge”,

- cut the OCR to zero,

- announce that the OCR will most likely be cut further in June (which would get many of the benefits immediately, but give a little time if there are some real system issues re a negative OCR), and

- commit to have in place by June robust mechanisms that for the time being removed, or greatly eased, the current effective lower bound on short-term wholesale interest rates.

As it happens there have been a few other contributions on monetary policy locally this week.

Yesterday morning I heard the local chief executive of Westpac on RNZ talking about all the system and documentation changes that would be needed – one has to assume he was talking about his bank, as he was quite specific in some cases – to cope with negative (retail?) rates. Unfortunately, the interviewer simply took Mr McLean at his word, and didn’t either challenge him on just how vital these things were or why – with 10 years global notice – a big bank like his appeared to have done nothing before now. (My initial reaction was a bit like that to the Governor – if Mr McLean had spent less time championing all the right-on causes he and the Governor are so fond of – especially climate change – and actually managed his bank, his borrowers might be rather positioned now.) Of course, from a public policy perspective, the bigger question is about years of failure from the Reserve Bank – under Wheeler, his “acting” replacement, and more recently under Orr – to ensure that the banking system could readily cope with the sort of cuts to the OCR that it was easily foreseeable some shock soon might make necessary. In Orr’s case, it is particularly inexcusable given that big interview he gave eight months ago articulating why he favoured negative interest rates as a policy option. “Saving the world” might seem more glamorous, but stabilising the local economy and keeping inflation target was actually his job.

Then there was a strange comment reported from the Leader of the Opposition.

Bridges said fiscal policy, rather than monetary interventions from the Reserve Bank, would need to do the heavy lifting in the Covid-19 response.

That clearly isn’t true – it is simply a choice by the MPC to do nothing, and by the government which does not use clear legal statutory powers to compel them to act differently. Sadly, it is still too much of the conventional wisdom. I’d probably have forgotten about except that this morning Bridges is reported as worrying about risks of too much public debt being taken on. Macro policy squares that circle – delivers accelerated recovery without lots more debt – by using monetary policy: yes, deeply negative rates in this context, to provide the support and stabilisation into the recovery towards full employment. Such, it seems, is the power of conventional wisdom and the fear of successive Oppositions – Robertson in Opposition was quite as bad, in less important circumstances – to challenge anything that the (on their record) not-overly-capable RB/MPC does.

And finally, another reader this morning sent me this clip from a recent BNZ research report, previewing next week’s MPS.

We would strongly argue that lowering the cash rate further would provide almost no assistance to the economy. The cost of debt is the last thing on anyone’s mind now. The lack of availability of debt might be a concern and, for many, the lack of income to repay debt will be a pressing problem. Pushing interest rates sub-zero will do nothing to ameliorate those issues. Moreover, even if the cash rate was to go negative, it would not be fully passed on to borrowers as the banks will still be funding themselves with positive interest rates. Term deposit rates are excruciatingly low for many as it is. The last thing the household sector would want is zero rates across the board. And even at zero, it would mean bank funding costs well above the cash rate.

The research report is headed “RBNZ Can’t Save the World”, to which one can only agree. What it can do – what it is charged with doing – is keep inflation and inflation expectations at around 2 per cent, and support as rapid as possible a return to full employment. At present, those two goals are tightly aligned, given how high unemployment is forecast to be, and how far medium-term inflation expectations have fallen.

Perhaps it as well to remember here that the BNZ has been the most consistently “hawkish” – pro tightenings, often uneasy about easings – of any of the local banks for many years. That has made them more wrong than most.

But that specific extract above simply makes little sense. Sure, most businesses would probably prefer a quick and full rebound in demand/activity over a fall in their debt interest rate, but it isn’t as if the two concerns are in conflict – in fact, lower interest rates and lower exchange rate will, in time, do their bit to support a stronger recovery. And despite the bank economist’s claim that no one much cares about interest rates, the evidence is pretty clearly against that in the very low interest rates being offered on the government’s scheme (and the Opposition’s proposal yesterday). In fact, the worst credits in the country – those who can’t raise funds elsewhere – get the cheapest rates, while deposit rates – in the middle of a savage slump – remain positive in real terms, barely down this year, sending all the wrong signals. And then there is the distraction: as BNZ knows only too well, if the OCR were taken to -0.5 per cent – as Westpac suggests will happen and should happen – retail rates, deposits and lending rates, would be still positive. For now, negative retail rates are some way away.

And if, perchance, depositors were reacting negatively to, say, 1 per cent term deposit rates, what are they going to do instead? Spend the money? Well, that’s good – that is monetary policy working. Shift it to another currency? Well, that’s good – a lower exchange rate would be monetary policy working. Seek to buy another asset? Well, that’s pretty good too – increasing both wealth effects and Tobin’s Q effects encouraging new investment, so that’s monetary policy working. And, of course, in aggregate it is not as if deposits are going anywhere – it is a closed system, with a floating exchange rate. Your purchase is my sale etc etc. Oh, if it makes people worry a bit about future inflation, that’s good too – that’s monetary policy working to hold up, or lift, inflation expectations to something like target.

Like Ken Rogoff, I think the case for deeply negative interest rates now is pretty overwhelming. It would ease the pressure on fiscal policy, it would support the tradables sector (on which our future prosperity rests), it would ease servicing costs on existing borrowers (and bring market rates closer to rates the government itself is happy to lend at). There is nothing particularly odd about negative rates, at a time when savings preferences are high and investment intentions are very weak – the interest rate simply serves to reconcile the two, while getting the economy towards full employment – and in the particular circumstances of New Zealand, a materially negative OCR would be needed to even get retail interest rates close to zero. As it is, recall that New Zealand now has materially higher retail rates than Australia, despite the deeper economic slump. That is a choice – an anti-stabilisation choice – made by the MPC, blessed by the Minister of Finance.

I couldn’t agree with you more regarding how bad BNZ economics have been for over 5+ years. I do not know how the Chief Economist there has kept his job!

LikeLiked by 1 person

Hi Michael. There are two questions here – whether deeply negative rates are considered acceptable by the general public and hence politically viable (different people will have different views, but a cohort of the population will be very unhappy). The second question is whether the benefits to modestly negative rates offset the costs. I know the riksbank produced research in 2019 supporting it (don’t central banks usually produce research that back up what policies they have in place?). But since then the Riksbank has gone back to zero and chose not to cut to negative the past two months, which for me is an admission they think the costs of modestly negative rates outweigh the benefits. Here’s an FT article on it – https://www.ft.com/content/4ade1675-2c23-409c-9140-f1722d8e3eb4. They haven’t ruled it out forever.

LikeLike

On the first point, given that retail rates are still so far above zero still there is way to go in confronting the political acceptability issue. As some authors point out, even then one can avoid negative deposit rates (headline) for small household deposits by use of fees. I guess there is a tradeoff: the (relatively wealthy) with material term deposits won’t like negative rates, but (a) they didn’t like a 2.5% OCR last cycle, and (b) the wider public won’t much like prolonged high unemployment. There are comms challenges that would have to be managed – but then that is true of the whole Covid response.

You raise a fair point re the Riksbank. Then again, the Riksbank has had quite big divisions over the years about appropriate policy – eg Lars Svensson pushing back strongly against early rate hikes some years ago (and being right). My impression is that Ingves leans to the more “hawkish” side – but it is a while since I studied their minutes.

LikeLike

The truth is that most people wouldn’t have a clue what it was all about. At the end of the day, there would be a few noisy people who made a fuss but could soon be shown to be wrong.

Sometimes leaders need to be leaders and do the right thing not the political thing.

Oh and clearly there are few pollies that would even know what a negative rate was and fewer still that cared.

It has been very obvious listening to people in the last few weeks that many who are paid by businesses have no idea what the owners of that business have to do to be there. Many have no idea other than money grows on trees and the employer should just pay up.

With an educated population like that, why would we worry about them being concerned about negative rates?

The other obvious thing is that few if any in Parliament these days have ever owned a business. Most have turned up and stuck their hand out.

Time for a few tough lessons.

Difficult as it will be.

I was working with a couple of mid 20’s fellows yesterday and we were having discussions about these things. They were sensible enough to realize that their generation had never known what a tough time was and reckon that 300k unemployed will cause their lot to sit up and learn. Was a sobering thought for them

LikeLike

Elegant theory but ‘gut feel’ it overlooks NZ culture/political economy dynamics: those depositors (voters/political donors..) that react negatively might do nothing pending a long walk to Wellington – I’m sure a few members of Grey Power New Zealand Federation Inc would be keen on such an outing.

LikeLike

In my 30+ years at the Bank it was always the experience that the Governor/Minister got more letters of complaint when interest rates fell than when they rose – even when deposit rates were double digits! So, yes, it is a real issuem but so will (or should) double-digit unemployment rates. And despite the left-wing enthusiasts for endless fiscal expanasionn (a) Labour tends to be quite cautious on that front, and (b) middle NZ more so. So if we are serious about getting quickly back to full employment – which we should be – we need mon pol deployed aggressively, and effective communications (whether from Governor, Minister, PM or whoever) to sell the approach and its implications. Crudely one could put it “we all stayed home and made huge GDP sacrifices to help protect old people, but part of the price is lower deposit int rates for a time”, Of course, most old people live largely on NZS.

LikeLike

Are negative OCR interest rates applied only to Cash Settlement Accounts?

Would they be applied to Government Bonds?

Anything else?

LikeLike

The OCR itself would apply only to deposits in bank’s settlement accounts. However, if (say) the OCR were set at -3% one might expect short-term govt bonds also to trade at modestly negative yields, In principle it is possible that longer-term yields could rise- if the policy is expected to work and lift activity faster and with it inflation expectations.

LikeLike

Thought so

Two issues ….

1. Guessing that at any given time cash settlement accounts represent a small fraction of a banks funds such that they should be able to eat that. Sure, it would incentivise each bank to get that money out on loan. Whether they are in debit or credit.

2. The pushback by the retail banks that they can’t cope with negative interest rates is a red herring in that they won’t be charging big depositors until OCR rates get below -5% and the quantum charge becomes significant over their whole funding structure. We are talking about a single calculation by the RB 10 or 20 banks. It is deducted from their cash settlement accounts. 30 minutes work for an RB clerk. The retail bank’s don’t have to do a thing – for the moment. But it sure as heck would get them off their backsides. Coming ready-or-not

LikeLike

On your first point, there is a lot more settlement cash now than usual, but in general yes settlement cash is a small proportion of total assets. That has not stopped monetary policy working effectively previously (indeed for years we pivoted the whole system on settlement cash levels of about $20 million).

LikeLike

Hello Michael

I have a lot of respect for Rogoff – I’m a former student of his – but I’m deeply skeptical about this proposal and your enthusiasm for it on many accounts – the main ones being that the theoretical case is far from proven, and the distribution consequences are unexplored. .

In commodity markets, real commodity interest rates are negative when the spot price is less than the future price( or, more precisely, when S(1+r)/F is negative, where S is the spot price, F is the future price, and r is the money interest rate.) Normally this takes place when spot prices fall relative to future prices, and the lower spot prices induce higher consumption. Your case for negative real interest rates seems to be built on the assumption that temporary declines in spot prices will not occur – presumably because firms do not want to temporarily cut their prices to increase their sales. This means there is a friction preventing higher sales/ and GDP. Your solution is to penalise current lenders – not current owners of assets or workers – for the failure of firms to temporarily cut prices. Your argument it is that it might work, because by punishing lenders you will make them spend immediately rather than late in time. Yes, it seems it could work. But, in a world of second best (the friction that firms will not temporarily cut prices to increase sales) do we know it will make things better or worse, or that it is better than other alternatives? Other people have suggested a temporary decline in GST, financed by higher taxes at another time. This has very different distributional consequences, put could potentially be more effective at increasing sales immediately.

An interest rate is a contract rate. The contracts implicit in negative interest rates are that people buying something new can either buy now and pay cash now for a high price, or buy now and pay a lower amount of cash later but only if they pay later. Unless you make cash hoarding very expensive, you are creating very large incentives for people to withdraw their deposits in a bank as cash and hoard them in a safe deposit box so they can take advantage of these strange contracts. Needless to say, this will require the Reserve Bank to act as a depositor to the banks to prevent banks from having liquidity problems when people withdraw cash . I presume you want firms to pass these negative interest rates to their customers in their hire-purchase or working capital finance agreements. Or do you want firms to be able to borrow at negative rates and not pass the lower rates on to their customers, as an alternative way to help them boost their profitability – they don’t need to temporarily cut prices to attract customers, and they don’t need to pass negative real interest rates to their customers?

When you have negative interest rates the contracts implicit in the purchases of second hand assets is that a person can buy an asset now at a cash price if they pay immediately, or buy it now and pay less in the future if they pay cash in the future. I wonder if you could be declared insane as a buyer if you agreed to pay cash now rather than withdraw cash and stick it in a safebox and pay later? One potential consequence of this is higher spot asset prices to compensate for the lower future payment. Again, this has distributional consequences. Another consequence is to increase the demand for temporary cash hoarding.Or do you envisage date stamped cash so that the government can redefine its value in the future to prevent cash hoarding.If so, exactly how does that interplay with the role of cash as legal tender – that the government now forces a person to accept as payment (for debts) something that legally loses value?

I remain unconvinced that this proposal is well thought though. If the fundamental problem is the the failure of firms to temporarily cut prices, this seems to be a very convoluted solution, especially relative to other possibilities such as a temporary cut in GST (which I am not yet advocating as i haven’t thought that through either.)

It seems to be that if the solution is negative nominal interest rates, we have found ourselves in a rather weird situation – and I wonder if central banker’s obsession with very low interest rates in the past is part of the problem. Perhaps central bankers have had a misplaced fear of falling price levels in the past, and that has lead us all to even weirder places. (I personally like the idea that technological improvements lead to lower prices, raising living standards for all and sundry.)

I am not sure, but this is possibly related to the work of Behabib, Schmitt-Grobe, and Uribe on the potential problems with Taylor rules that lead to solutions at the lower nominal interest rate bound. (happy to be corrected on this, or other matters.)

Andrew

LikeLike

No industry is more challenged than tourism in these times of peril and pestilence.

Hopes have been rising for a reopening of the Tasman border but on the broader issue of international tourism Prime Minister Jacinda Ardern had a stark message for the industry on Tuesday: “We will not have open borders for the rest of world for a long time to come.”

First, some numbers. These come from Statistics New Zealand’s annual tourism satellite account and are for the year to March 2019.

International tourism expenditure accounted for 20% of total exports and 42% of total tourism spending.

Tourism overall, domestic and international, represented just under 10% of gross domestic product – 5.8% direct value added and 4% indirect.

The sector employed 229,000 people directly, including 29,000 working proprietors, or 8.4% of the total number of people employed. When those whose jobs depended indirectly on tourism were included the share of total employment rose to 14.4%.

Of the 3.9 million overseas visitor arrivals that year 2 million were on holiday and 1.5 million or 38% were from Australia.

https://www.interest.co.nz/news/104855/brian-fallow-takes-look-tourism-sector-economy-perhaps-most-impacted-covid-19-and-travel

“We would hope to see the border open as soon as it can safely be done but we are probably looking at about October before it could realistically happen.”

—————————————————–

It is not about sales its about finding work for 230000 people and replacing the benefits etc they are going to be paid with income from an external source. Lower interest rates equal lower exchange rate equals more earnings for NZ and in tandem with that fewer imports and more import substitution.

and of course, ower rates will help with their day to day living costs with rent and mortgage payments.

Doesn’t seem too complicated to me.

LikeLiked by 1 person

More of NZ tourism is domestic than international, so less than half of those directly employed would lose their jobs, but obviously will vary from region to region.

LikeLike

Domestic Air travel must be allowed under Level 2. No point pouring a billion dollars of taxpayer dollars into Air NZ if you do not allow them to operate.

LikeLike

NZ exports only represent $60 billion of which tourism amd International students is $16 billion. The rest of the domestic industry is $200 billion. Lower exchange rates impoverish more New Zealanders than the few kiwis that rely on exports. It does not make sense to have a lower NZD. Anyway our NZ is already a pariah as far as US and Europe Free Trade is concerned. Not because we are world class but because we are cheap with the NZD trading at 40% discount to the USD and 45% discount to the Euro.

LikeLike

Hi Andrew

Thanks as ever for those comments.

What I’m not sure about is whether the questions you are posing are specific to negative nominal interest rates (the immediate issue people like Rogoff and I – and others – are raising) or with any active discretionary monetary policy. After all, NZ and Aus aside, most advanced economies have had negative real policy rates for the last decade. Is there anything in principle different about a negative nominal rate? (you may – or not – recall my post a few weeks ago noting that if the inflation target had been set at 10% not 2% we wouldn’t be having these debates – the OCR would simply have been cut a lot).

On physical cash, you are certainly right that negative nominal rates will increase the demand for cash (as, in fact, much lower positive nominal rates look to have). Hence the need to deal with that issue directly – whether with a cash-conversion fee (at the RB/banks level), a cap on the total physical currency issue (with tranches auctioned) or – at the extreme – elimination of all but very low denomination notes and coins).

I suspect you are overstating the legal tender point, since it is only relevant if the settlement mechanism is not pre-specified (which would be pretty rare now for materially-sized transactions).

I think there is an important distinction between deflationm driven by rapid productivity growth – which I’ve always liked the sound of, at least absent shocks – and that wrought by a collapse in demand in a low productivity growth climate. But even in the high productivity growth world – which would support higher real interest rates, cet par – one still risks being left with the inability to cut nominal rates much in a severe adverse demand shock event. That seems not to bother you – your apparent unease about active mon pol – but it still does bother me. The central banking story of the last 100 years is far from an unalloyed success, but my read is that in very adverse events active mon pol was better than the alternative.

LikeLike

Its very sad, I believe on Monday 17 people arrived in NZ and 25 left… total, meanwhile a few weeks ago….

5:17 pm on 22 April 2020

No international passengers will arrive in New Zealand today for the first time in decades.

Air New Zealand planes parked up at Auckland Airport two during the Covid-19 pandemic.Air New Zealand planes parked up at Auckland Airport two during the Covid-19 pandemic. Photo: Supplied / Air New Zealand

The only planned international flight from Tonga to Auckland was cancelled.

Tourism Industry Aotearoa chief executive Chris Roberts said it was a symbolic day.

“We’ve talked about international visitation falling to zero, well now it has precisely done that,” Roberts said.

“Tourism is going to be the last industry to recover from this crisis, and we know that recovery is a three to five year recovery horizon.

“It will be the longest recovery for any sector in the country. We’ve clearly hit the bottom today so the only way is up, it can only get better from here.”

Hundreds of passengers were expected to arrive tomorrow, he said.

There were still some domestic passengers today, with Air New Zealand confirming 175 passengers were booked to fly domestically using the airline on 14 flights.

The airline usually operated more than 400 domestic flights a day prior to the pandemic.

LikeLike

A couple of points

First, exchange rate values are determined by the view of NZ taken by the rest of the world and the yield of the NZD is a major part of that view.

How likely is it for much needed foreign capital to flow to this country country when baseline returns are negative?

Or do you think that we should sell our remaining NZ assets to pay for continuing consumption? I doubt there would be much appetite for that..

Secondly ,in a crisis such as NZ faces now ,there needs to be as much stability as is possible in financial settings so investors ,entrepreneurs and others can make informed sensible decisions.They are the people who will save NZ.

Without this certainty the required investment will not happen.

Thirdly deliberately revaluing or rather devaluing the NZD is for many savers(KiwiSaver) is actually stealing the proceeds of many years of hard work for those investors. It is also reducing the capital availability for recovery.

There needs to be respect for property rights, one of which is the value of people’s savings.

As a guess I suspect that other some foreign nations short on capital will be considering positive rates.

In a nutshell my opinion is that negative interest rates would be a disaster for NZ.right now.

LikeLike

Recall that in typical recessions the NZ exchange rate falls considerably; it is part of how we get back on the road to recovery fairly expeditiously. In general, a lower exchange rate now supports lower interest rates – since foreign purchasers of NZD can look forward to the prospect of some future appreciation to supplement the now-lower interest rate returns on offer.

My point isn’t, at a deeper level, that central banks should be determining where interest rates are, but that they need to adjust their policy rates consistent with the wider economic pressures. In a hypothetical free market, my proposition is that real risk-free interest rates at present would be deeply negative, esp for shorter-term maturities.

LikeLike

Agreed that the exchange rate should fall in a crisis..—- But

The big difference today is that this is a “ global “ crisis affecting the rest of the world.

This means every OECD/ or other central bank will be trying to adjust their exchange rates to compete better as a country in this global crisis.

Competition in exchange rates occurs anyway , but some stability or balance has been achieved. There is a risk that a lack of stability could destabilise trade or worse.

The need now is for stable settings that do not provoke international scrutiny or retaliation.

In passing ,NZ now needs to be focusing on productivity as you have often said. Fiscal policy is the best if only effective tool we have. Deregulation could make a huge positive difference.

Present government spends are not good quality but that is another story.

LikeLike

The US will emerge economically stronger because every week Covid 19 kills off 10,000 old folk a week that needed to be cared for. Superannuation funds are financially better off and wealth is transferred to the younger generation more prepared to invest in productive industries.

LikeLike

I obviously should be retired. The reckless, lunatic place central banking has taken us is an economic asylum.

I wake in the morning and see the US share bourses going back to historic highs on the Frankenstein command economy construct that the Fed has created, as the country and the global economy goes into a depression probably deeper than the 1930’s and realise either I haven’t got a clue, or the world has been taken over by madmen.

We’re down a rabbit hole here.

LikeLike

Addendum: I say the above as a former prudent saver who has seen my savings and any chance of a retirement income for acceptable risk destroyed totally by central bank stimulunacy. I say former because I got so desperate for yield, and would not touch these Harry Potter share valuations (created by central banking) that I put some savings pre-Covid into commercial property. Spectacular fail: and all to get a lousy 6% yield.

After the coming misery of the Big Reset, seriously, central bankers should be in criminal courts for their destruction of free markets and thus financial markets.

LikeLike

Kiwisaver averages 8% yield since implementation and is professionally managed with the Employer contribution covering the administration costs plus gives you additional yield.

LikeLike

The best returns are the leveraged returns of residential investment property averaging 50% per annum.

LikeLike

You ascribe far too much power/influence to central bankers.

LikeLike

But do I ascribe too much power, Michael?

Re RBNZ: probably yes. But BOJ? Fed? ECB?

Can do you see current Fed policy – including before Covid19 – as anything other than reckless? To me they are, and have been for a long time now, totally out of control: and that’s in their policy settings of seemingly infinite debt creation, including now buying – illegally – private company junk bonds (look at a graph of their balance sheet), soon they’ll be buying shares, but also in that they seem to be above the law, and certainly above any audit function at all in the US, yet their policies are totally distorting free market structures, and looking at their share markets, they’ve long ago destroyed price discovery: they have share valuations that can only be explained by a lunatic liquidity, not by earnings. Nasdaq & S&P indices will soon be rallying back to all time highs, in the greatest economic crisis any of us has seen and while their treasuries go negative.

Or consider this: can the Fed, the BOJ, the ECB, or even RBNZ ever normalise in the next two decades or even further out? When will savers ever be able to enjoy a sane environment with interest rates around or above 5% again? And in this environment, created by central bankers who have always found it easy to loosen over past decades, but never to tighten again, not really, what are prudent savers supposed to do? Because I’m at my wits end – I’ve already made one big mistake re commercial property, and as of this morning I now have two matured term deposits sitting in a BNZ savings account earning 0.1%pa (negative real returns): I don’t want to tie that up for a year on 2.4% before tax as frankly as our savings are so useless we’re thinking of buying a second house (not investment, just a holiday house); I’ve done well on bonds/treasuries and Harbour Asset Management’s Enhanced Cash Fund since 1 April, but as rates now approach zero, and heaven forbid negatives, that can soon turn into rout as with interest rates on zero every asset class once considered safe is toxic.

Again, we are totally down a rabbit hole here: free markets wouldn’t have got us here, loose monetary policy and loose fiscal policy from every politician campaigning on a free lunch, got us here. How do you unwind this?

I don’t think you do. Because we now have stimulunatic monetary and fiscal policy on steroids. So the next generation for us retirees, and the tail end of the existing one, are screwed. Most will end up having to scratch around in semi-poverty.

This is not a personal dig at you, MIchael: I’m just so angry with this economic Harry Potter land we all find ourselves in, and Covid was only the trigger; this was all well bedded in before anyone had heard of Wuhan.

LikeLike

Two brief responses:

I agree that some specific Fed (in particular) interventions appear to go beyond the law, and beyond the proper scope of an independent agency’s activities.

But the bigger difference between us (I think) is that you see the current level of interest rates as the creation of central bank monetary policymakers and I don’t. And so when people raise the “normalising” issue, we can really only have interest rates back towards some sort of normal historical level/trend when underlying preferences around savings and investment change. At present, there is more willingness to save at ‘normal” interest rates than there is desire to invest – and the response to that has to be lower real interest rates. Quite why those patterns exist isn’t clear. Some will blame excess regulation (deterring investment), some will blame demographics (declining population growth rates in most countries – altho not NZ/Aus), some will blame new technologies which are less capital intensive per unit of output than the old manufacturing core of advanced economies. I’m not committed to any of those interpretations, individually or in combination.

I’m of an age where I wish deposit accounts paid more (after-tax real) than they do – or than i think they need to for the next year or two – but all the indications are that there is not the demand to use those savings and therefore they don’t command a high price (and can’t if we want to get back to something like full employment).

LikeLike

Typo: that first sentence is ‘Can you see …

LikeLike

Thanks Michael, but how do I ‘command a high price’ on my term deposits from a bank whose loan book to farming, business, and increasingly unemployed mortgagees doesn’t work anymore with an even 2% rise in rates? There’s so much debt in the world which was dolled out without any real (enough) consideration of risk (because there’s certainly no risk premium included in the rates for some of the latter dairy conversions). And I do see totally dysfunctional markets particularly in Eurozone, Japan and now US as being almost totally the product of central bank stimulunatic monetary policy, because central bankers even if unconsciously work on the same behavioural impetus that politicians do: it’s easier to give (loosen), and offer the free welfare lunch (now this idiot UBI is gaining parlance), than it is to take away (tighten). Human nature. But in the long run a disaster which is exploding just on my retirement: wonderful (not). The only correction is total collapse now of this system and a huge global debt write off where another bunch of bureaucrats gets to decide which of us lose everything.

But I’ll leave it there, and go back to work – I’ve largely had to give up the notion or retiring; it won’t be happening. And I’m mad as hell about that.

LikeLiked by 1 person

The critical challenge – probably – is productivity (or lack of it). If there were lots and lots of highly productive opportunities out there firms would be champing at the bit to invest. Globally (and in NZ) they certainly aren’t right now, and haven’t been in aggregate for some time.

For what its worth, I have a little of sympathy with individuals at your age and stage (and, personally, am greatly relieved to have an indexed pension underwritten by the one entity that cannot ever be unable to meet its debts).

LikeLike

Mark: most of the economics on this site and in the newspapers goes over my head but I did understand “”they have share valuations that can only be explained by a lunatic liquidity, not by earnings.””

Michael: what happened to government pensions when Argentina defaulted on its debt? Or Zimbabwe? My father had a British Rail pension that was based on his final salary and then inflation proofed; those were the days. When my wife chose to live with me she told me not to worry about getting old because her children would always support us. You should have a chat with your children.

LikeLike

Are you trying to outbid me for the Cassandra title?

Call me a pessimist on NZ’s long-term econ prospects, but my confident expectation is that we will emerge from this crisis five years hence with govt debt less as a share of GDP than it was in the UK, France or the US last year.

But you may have observed my careful wording (“cannot ever be unable to meet its debts”), and by that I did not even mean the NZ govt, but the (money-supplying) RB. Between that and the NZ courts I don’t greatly trouble myself re risk of personal old age poverty (throw in a high-earning wife 10 years younger than me).

I should add that I am a trustee of said pension scheme and it is fully funded, with enforceable claims.

LikeLike

LOL. Oh to have a gold plated pension like that, Michael. I’ve public servants in family on same, and I don’t know if they realise how sheltered they are compared to those of us who ultimately pay the damned thing. Looked at my bank about an hour ago and thought I’d been scammed, but it was just Mrs H had paid the provisional tax … ouch.

In fact we couldn’t be more different: older wife here who is retiring courtesy of me 🙂

LikeLike

After 4 weeks of locked up I have decided that retiring ain’t all it’s cracked up to be.

I enjoy working. Perhaps not quite so hard would be good.

LikeLike

Must be why I write this blog……(not entirely but…)

LikeLike

I think Michael has laid out the benefits of using monetary policy quite clearly. The concerns (such as documentation challenges, distributional effects) seem like third-order effects at best (I say that as a net lender).

The more we can use monetary policy to stabilise aggregate demand (or at least match it to the new supply curve), the more we can preserve government spending for where it is really needed: keeping body and soul together for the sick and destitute, and recapitalising the wiped-out parts of the economy when the pandemic is finally over, lest they never return. It is going to need a Marshall Plan of sorts.

LikeLiked by 1 person

“In our case, a much lower exchange rate would make a material difference to the fortunes and prospects of the tradables sector.”

Shouldn’t we be worrying about the fortunes of the non-tradable sector too at a time like this? They don’t matter?

The USD exchange rate has already fallen 30% since the July 2014 peak and by 18% in just the last two years. It’s not enough? Why are the tradable sector so much in need of further support than other sectors in the context of this crisis? How far does it have to fall to satisfactorily improve their fortunes?

The reason I think you keep obsessively “banging on” about negative interest rates is not because there is any firm evidence they will help economic recovery – they will quite likely hurt more people than they will help – but because you want to push the exchange rate lower and believe monetary policy should be misused to achieve that.

This is nothing new, these columns have been pushing for lower interest rates for the last five years. (I daresay if you’d had your way we would have had zero or negative rates years ago!). This is also the reason you always believe inflation is always too low even when it’s comfortably within the target range. It’s the reason why you always downplay/ignore the harmful effects of inflation. Because, I think, you see everything through the lens of the exchange rate – will the policy action push it lower or not.

The fact that there are numerous reasons to be cautious about negative rates (and a “much lower” exchange rate for that matter), carefully explained even in the comments sections of these columns and more generally by other economic commentators are either ignored, met with disbelief (e.g the bank economist) or dismissed. Like the detached ivory tower ideologue who is so wedded to his paradigm he just can’t see there might be a better way.

LikeLike

I get that for some reason you aren’t too keen on me or my analysis. Not really sure why, but views will differ.

As I’m sure you know, aggressive use of mon pol will tend to support both non-tradables and tradables sectors. By contrast, heavy reliance on fiscal policy – esp direct govt purchases – tends to skew strongly towards non-tradables. Given the backdrop of NZ’s falling foreign trade shares, that should be more worrying that perhaps in some places.

Re negative int rates, I’d be very surprised if you can find any sign of me having suggesting the OCR should have been less than zero prior to mid March (I say that because I happened to reread the other day a post from about 13 March in which I then suggested there was a strong case for going to zero). What I have consistently argued for, over at least five years when my views have been public, is a more aggressive targeting of inflation at or slightly above 2 per cent, with a view to providing more room for nominal interest rates to be adjusted come the next serious downturn. That still seems like pretty sage counsel to me.

LikeLike

i have nothing against you at all. much respect for you actually on many topics, but yes I surely disagree with your views on monetary policy.

What I have noticed is that the obsession with negative interest rates seems to be present with increasingly disrespectful and self-righteous tirades against institutions whose only crime is to have an alternative view to you, which I’m sorry, I’m finding unpleasant.

On the comments re non-tradables, I presume you are referring to the knock-on effect to non-tradable business from increasing exporter returns? Wouldn’t there be lags though? The most immediate effect of a large depreciation will be to prices. Many non-tradable businesses (e.g. the perennial hairdressers) rely on imported products and will be forced to put up prices again. I’m sure you noticed that non-tradable inflation was escalating until this crisis, hitting 3.4% in the March 2020 quarter? Doesn’t affect you I know but it does most people! I suspect the weakening exchange rate to be a factor in this figure.

I simply don’t think this is the time to be worrying about “falling trade shares” and setting in motion economic restructuring that by design will put a large number of firms relying on imported products out of business. When the economy is already in a weakened state seems cruel.

I didn’t say you had advocated zero or below zero rates, only meant to suggest that if it had been in your hand to do so you would have blown that ammunition and cut the OCR to zero (or below) long ago.

I have always found the argument underlying your final comment to be practically incoherent because there are two opposing points. I’ll eat my metaphorical had if you have ever advocated for higher interest rates (as you are implying you would do once inflation increases) because the path urged for interest rates is always lower and higher inflation is always wanted. The higher interest rates will never happen in your paradigm because I think, because you want to maintain a lower exchange rate and that will outweigh other considerations. Inflation and interest rates are simply the means to an end: lowering the exchange rate.

I believe this objective, and the means of achieving it that you propose to be ill-advised and far from sage.

LikeLike

Not sure why you think non-tradables inflation doesn’t affect me – me just the same as anyone else as far as I can see. Do note however that pre-crisis core inflation was still a bit below the target midpoint.

Re whether I’d ever have recommended the higher nominal intcrest rates, who knows, but in 25 years or so as a mon pol adviser I was a not-infrequent advocate of higher interest rates. After all, in the medium term mon pol has no impact on the real exchange rate only on inflation.

LikeLike

There was a comment that stuck with me, and hopefully I am remembering it correctly, a couple of years ago probably when discussing inflation impacts and you remarked that you were relatively immune from the effects of inflation, due to your financial position. I wasn’t able to track down the reference so should have left it out

LikeLike

Ok. I guess it may be true relative to some, although I’ve also often made the argument that many people are relatively immune from inflation (since over time not only are welfare benefits indexed but wages tend to adjust more or less fully, as does the value of real assets). The people who are heavily exposed to inflation/deflation are those with fairly long-term fixed rate debt or fairly long-fixed rate financial assets.

LikeLike

Well it certainly hits you differently to someone on the minimum wage and that shows up, in my view, in your apparent disregard for the human impacts of what you advocate. The household living cost indices put out by SNZ demonstrate the unequal impact of inflation on different groups pretty clearly. You say “tend to”, “more or less”, which is hardly conclusive. Again the household indices show the result is quite often “not”, particularly in more vulnerable groups. The “it will all wash out” argument seems to be just an attempt not to have to worry about the collateral damage to real people affected by your inflationary, disposable income reducing policies. I know you are banking on a medium term payoff, but that hardly helps at a time like this? There are so many basic things like rent, power, rates that consistently increase by more than the headline inflation rate. Forgive me but you seem to be quite out of touch with the financial reality that significant groups of people face.

LikeLike

Again, different issues in my view. Unless relative price changes are themselves somehow influenced by general inflation, the sorts of effects you are talking about are not effects of inflation.

But of course economic life is toughest for the poorest. That is why ever effort should be made to get back to full employment ASAP and to lift economy wide productivity.

LikeLike