One way of looking at developments in New Zealand’s monetary policy is to compare what has been done, and how that has affected market prices, in the country that is in many respects most similar to New Zealand, Australia.

There are no perfect comparators – and in many ways everyone is flying a bit blind at present – but the two economies do have many of the same banks, similar institutions (variable or short-term fixed mortgages) and a fairly similar experience of the virus. Sceptic that I am of the Reserve Bank of New Zealand, I am not starting from a view that the Reserve Bank of Australia’s monetary management is some sort of standard to which we should aspire. Coming into this crisis, for example, both central banks have presided over core inflation undershooting the midpoint of their respective inflation targets, the RBA by more than the RBNZ. And for reasons that are not very clear (at least to me), the Reserve Bank of Australia is more resolved not to adopt a negative policy rate than our own central bank.

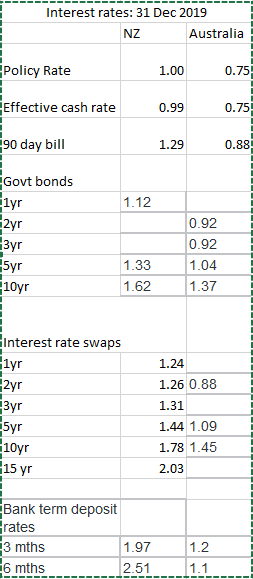

What was the starting point at the end of last year (a time when no one in either country had the coronavirus in focus)? Recall that Australia’s inflation target (centred on 2.5 per cent) is a bit higher than ours (centred on 2 per cent). Here are the interest rates I could find, all from the respective central bank websites, except the Australian interest rate swaps yields.

Every single one of the New Zealand rates was higher than the comparable Australian rates – the smallest gap of all being in the two policy rates, and by far the largest being in term deposit rates. Note that at the end of last year, markets were looking to the prospect of a cut in the RBA cash rate later this year, while in New Zealand attention was beginning to turn to the possibility of an OCR increase at some point.

So what has happened since then?

- the RBA cuts its cash rate by 50 basis points to 0.25 per cent, while the RBA cuts its OCR by 75 basis points to 0.25 per cent,

- both central banks have massively increased the volume of settlement cash in the respective systems. At the RBNZ, all those balances (currently around $28bn) are remunerated at 0.25 per cent, while at the RBA balances are remunerated at 0.10 per cent (both central banks changed their rules for remunerating large balances),

- the RBNZ announced its large-scale asset purchase programme, concentrated on government bonds, currently with a limit of $60 billion,

- the RBA announced a target rate of 0.25 per cent for the yield on three year government bonds, indicating that they would operate in the market (primarily that for government securities) to maintain market rates at or near that target.

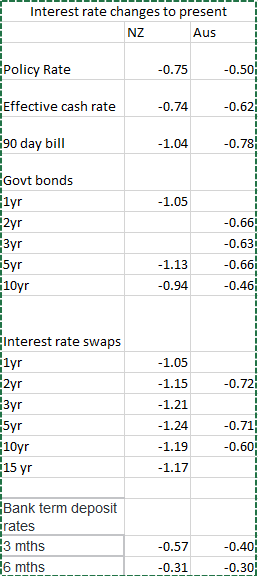

And here is how much those rates have changed to now (latest available data)

Tracking down old mortgage rates for Australia is beyond me, but note that both variable and fixed mortgage rates in New Zealand are well above those in Australia. But so are term deposit rates: averaging across the big four banks, in Australia for AUD six month term deposits the banks are paying about 0.8 per cent, and in New Zealand for NZD six month term deposits the banks are paying about 2.2 per cent.

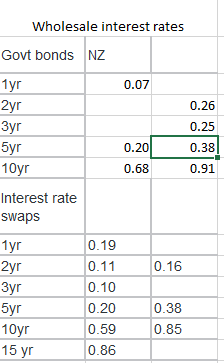

As you can see from the table, wholesale rates (bills, bonds, swaps) have fallen by more in New Zealand than in Australia. That is not inconsistent with the fact that the Reserve Bank of New Zealand cut its effective policy rate by more than the RBA cut its effective rate. Here are the current wholesale rates (Australia in the second column)

It is notable that longer-term rates are now lower in New Zealand than in Australia – quite a contrast to the situation at the end of last year.

Consistent with all that, incidentially, the NZD/AUD exchange rate fell by about 4 per cent over this period.

What might explain these developments?

On the one hand, quite possibly people trading the markets in the two countries may reckon the New Zealand recession will be more severe and/or longer-lasting than Australia’s. It is certainly true that forecasts of the decline in June quarter GDP are much steeper for New Zealand than for Australia, although beyond that – looking ahead a year or two – it isn’t obvious at this stage why things might be so very different at the sort of horizon more relevant to longer-term rates. So for now I’ll just note that possibility and pass on.

What about central bank words and choices?

The Reserve Bank of Australia has apparently been pretty clear that it will not lower than cash rate from here. The market seems to more or less believe them (the OIS rates on the RBA website are consistent with the current effective cash rate). By contrast, the Reserve Bank of New Zealand has opened the door to the possibility of a negative OCR next year. I don’t have access to New Zealand OIS data, but I did notice this chart in a Westpac market report, dated yesterday, that someone sent me.

Markets here are pricing a negative OCR throughout next year. In other words, our longer-term interest rates price in even more conventional monetary policy easing. Consistent with that, a reasonable chunk of the fall in the exchange rate has occurred since the Reserve Bank’s MPS last week.

All of which then leaves the question of quite what difference the Reserve Bank’s vaunted long-term asset purchase (LSAP) programme is making. The Reserve Bank repeatedly tries to suggest the answer is “a lot”. But there is reason to be more than a little sceptical that it is making much difference where it matters.

As I noted above, both central banks launched novel asset purchase programmes. The RBA’s approach involved purchasing whatever it took to keep the three year government bond rate around 0.25 per cent. In the early days – amid the global bond market liquidation – achieving that goal took a lot of purchases. But here are the RBA’s total bond purchases

| A$mn | |

| Total | 51348 |

| March | 27000 |

| 1st half Apr | 17500 |

| 2nd half Apr | 5748 |

| May | 1100 |

You’ll recall that the Australian economy is quite a lot bigger than New Zealand’s. A$51 billion in bond purchases there might be akin to perhaps NZ$7-8 billion purchases here.

But note what has happened: after heavy purchases in late March and early April, the RBA’s bond purchases have almost completely dried up. Despite the heavy expected federal government bond issuance, expectations about short-term rates are now sufficiently subdued that the three year government bond rate is holding at the target rate with no material bond purchases at all. And the purchases the RBA has been doing have been heavily concentrated in relatively short-dated government bonds, consistent with reinforcing monetary policy signalling and with the fact that, as in New Zealand, most private sector borrowing tends to be on variable or short-term fixed terms.

What about the Reserve Bank of New Zealand? Here is the same table for them (government bonds only – there is a small amount of LGFA purchases also).

| NZ$m | |

| Total | 11,228 |

| March (from 26th) | 950 |

| 1st half April | 3,833 |

| 2nd half April | 2,845 |

| May | 3,600 |

Relative to the size of the economy, total purchases here have been somewhat larger, but the real difference is that the Bank is buying just as heavily as ever. And as I noted in my post on Monday more than two-thirds of all their purchases have been for maturity dates from 2027 and beyond – and virtually no one I’m aware of, other than the government itself, takes funding exposed to rates that long.

In other words, it seems plausible that the LSAP programme might be knocking 20-30 basis points off long-term government bond yields and swaps rates, while making almost no difference at the short-end (where the RBA would seem now to provide a reasonable benchmark). And yet it is the short-end that influences borrowing costs for most households and corporates. At the long end……well, there is the government. It all looks quite a lot like a programme designed to do two things:

- by waving around very big numbers to suggest that monetary policy is doing a lot when it actually isn’t really doing that much at all, and

- to lower the marginal borrowing costs of the Crown, at a time when the Crown has a very big borrowing programme. At very least, that is a questionable use of monetary policy – not at all consistent with the MPC’s Remit (since fiscal policy will be what it will be whether or not bond yields are 20 points higher or lower) – and all while exposing the Crown to a really high degree of unnecessary degree of interest rate risk (if the authorities really believe interest rates are extraordinarily low they should be markedly lengthening the duration of the Crown’s debt to the private sector, not skewing it dramatically shorter by buying in government bonds and issuing variable rate settlement cash in exchange).

And, on the other hand, if the Bank were really serious about getting retail interest rates down – rather than anguishing in public and suggesting that commercial banks aren’t doing their job – it would just get on and cut the OCR quite a lot further. As it is, go back briefly to the changes table (the second one from top): nominal rates have fallen to a moderate extent this year, but survey and market measures of inflation expectations suggest that expectations of future inflation have fallen by probably 0.7 percentage points. Real rates generally haven’t fallen much at all, while retail deposit rates – held up by the combination of the Bank’s core funding requirement regulation (their choice) and the continuing relatively high cost of offshore terms finance (illustrated in the MPS last week) – have actually risen in real terms.

Quite a claim to fame that: to be the central bank, in a country with a highly safe banking system (as the Governor now repeatedly avers), that presided over a rise in real deposit rates in the face of the biggest economic slump in decades. Extraordinary.

Meanwhile, in the last 24 hours we’ve had the Deputy Governor offering interviews to both Stuff and the Herald reaffirming the MPC’s commitment to stick to its bizarre promise on 16 March not to cut the OCR further before next March, come what may. Apart from anything else, it has the objective effect of tightening monetary conditions relative to where they were – in effect, urging markets to price out those early negative OIS prices and, all else equal, push up the exchange rate.

There is, of course, something to be said for sticking to one’s word. But rash promises generally should not be followed through on. I suppose we should be thankful that the MPC in February – recall, they were upbeat about the rest of the year then – had not offered “forward guidance” committing not to cut the OCR this year, come what may. Perhaps they’d have felt obliged to stick to that rash pledge as well? As it is, this was a pledge made on 16 March, at a time when the Governor was reluctant to even concede that a recession was happening, at a time when the Secretary to the Treasury (observer on the MPC) was telling the PM that things might be not much worse than the 2008/09 recession. Perhaps (or not) those were pardonable calls at the time, but they were clearly mistakes, and not small ones. Sticking to a rash pledge made in some highly uncertain and fast-moving circumstances is almost akin to the suicidal person talked down from the edge, but still averring that “I promised I’d jump, I even left a note, I need to stick to my word”. Among the sick, such misperceptions might be pardonable. From highly-paid public figures charged with conducting a nation’s monetary policy, it is simply stubborn, verging on the crazy – the more so if the MPC thinks that sticking to that pledge in any way enhances the sort of credility that matters. After all, it was the MPC last week that published projections showing inflation below the bottom of the target range for two years, and unemployment unacceptably high. Those were supposed to be the considerations people judged the Bank on.

Finally, I see that Stuff’s Thomas Coughlan in his column this morning has picked up my call that if the MPC won’t move – won’t do the job that is really needed, to provide a lot more stimulus, to get us on the path back to full employment and price stability – that the Minister of Finance should use the override powers Parliament has long provided him with. They aren’t powers that should be exercised lightly, but these are exceptional times, and the Bank seems to be content to do little of substance, while pretending otherwise. Of course, the Act was initially written primarily to protect us from inflation-happy politicians, but also has to protect us from central bankers just not doing their job – in this case, on either the employment or inflation dimensions. If he fails to act – as surely, risk averse as he is, the Minister of Finance will fully share responsibility for the unncessarily slow recovery that he and his MPC seem set to risk. To what end?

According to the RBNZ (with agreement from most bank economists), a combination of cutting the OCR to 0.25% and engaging in aggressive QE, has the effect of lowing the “shadow policy rate” to between -2% and -2.5%. In other words, the flat yield curve we have now would have come about with either an OCR of -2%/-2.5% or a combination of OCR at 0.25% and large QE.

The RBNZ chose to get to a deeply negative shadow rate by keeping the OCR at 0.25% and adding QE.

The most negative policy rate in the world now is Switzerland at -0.75%.

Would you have the RBNZ go well under that level Michael, and stand out like a beam in the global market place ?

LikeLike

I went to a street vendor for a couple of sausages along the River Limatt in Zurich, Switzerland. It costs Euro8.50 which is NZ$15.50 for a sausage. Our street vendors serve up sausages for NZ$2.00

I do not think negative interest rates are the answer. It just makes consumer products unbelievably expensive.

There should be a travel warning for all NZ travellers. “If you are depressed from financial strife do not go to Switzerland for a holiday. You will end up suicidal.”

LikeLike

Of course, one of the reasons the SNB adopted negative rates was to temper the sharp appreciation in the Swiss franc. Inflation is low in Switzerland, and prices for domestic services are high partly because they are a so much richer country than we are.

LikeLike

On shadow rates, everyone is drawing on the work of former RBer Leo Krippner. I wrote about his work in this area last month

https://croakingcassandra.com/2020/04/02/measure-what-is-measurable-and-make-measurable-what-is-not-so/

In that post, I highlighted several reasons why I’m not convinced that, esp in a NZ context, the shadow short rate is really capturing something real than can be equated with OCR cuts.

An extract

“My bigger unease about this work, stretching all the way back to that 2012 paper (where I recognise a couple of sentences I insisted on being added) is the third in Leo’s own list of caveats above: the SSR is not a rate that can be transacted, and if much of borrowing and lending in an economy is either at (or swapped back to) or very close to a floating rate, the actual OCR (self-imposed constraint and all) will be a lot more important than the SSR estimate might suggest. In the US, for example, a lot of mortgage lending takes places at very long-term fixed rates (and so what happens to very long-term bond and swap rates has a direct transmission mechanism). That is much less so in New Zealand (or Australia or the UK). That is consistent with some of the doubts I’ve expressed in earlier posts around quite what difference the Bank’s large scale asset purchase programme really makes where it matters (thus, on my telling, the main advantange of that programme is that it should reveal quite quickly how severe those limitations are and turn the focus back on the OCR and that self-imposed floor).”

In addition, the SSR does not take account of the exchange rate effects we would usually expect to see from large OCR cuts. I don’t think I’m talking out of school to say that Leo himself would accept many of the points in that earlier post.

Looking ahead, I guess I have two reactions: if people genuinely believe the LSAP is doing good keep it, but it needn’t substitute for OCR cuts; we can do them too. Even, to start with, just moving to match the Swiss.

But yes I do think we should go well beyond that – echoing (in parallel) with former IMF chief economist Ken Rogoff who a couple of weeks ago called for “deeply negative” interest rates in the US. To do it would be a first, but so was going off gold in the Great Depression, and yet the countries that did also recovered fastest. And you are right that we would stand out – in a desirable way that would see the exchange rate fall quite a bit, in turn acting as one of the channels to accelerate our recovery.

Oh, and the third point, recall that even if the RB believes the shadow rate model, on their own published scenarios last week inflation is going to be so low, that more needs to be done for them adequately to be doing their job.

LikeLike

Would note the following article in The Australian this morning and which reflects that effectively Negative Interest Rates are a technical problem across the ditch:

So effectively both countries don’t have the ability currently to set negative interest rates (even if not required) – really is a massive fail from regulatory bodies not requiring the Banks to get their systems up to scratch – especially in light as you have highlighted – Post 2008 negative rates are not new.

“The nation’s banks are scrambling to prepare for the prospect of negative interest rates washing over the economy, despite recent assurances by the Reserve Bank that such a move is “unlikely”.

But with many banks operating on ageing technology, senior bankers fear their systems won’t be able to cope with negative rates, drawing parallels with the “Y2K” bug ahead of the millennium, with an urgent need to find a technology workaround.

In recent weeks, banks have been notifying some business customers of a change in their loan documents in the event that interest rates turning negative.

In doing so, banks have said that if a specific reference rate in their loan agreements falls to less than zero, the rate “will be taken to be zero”.

It’s one way of overcoming the problem of bank systems failing to recognise a negative interest rate number, mirroring fears as the new millennium approached in that computer systems could crash because they wouldn’t be able to process dates beyond December 31, 1999.

A Westpac spokesman said larger commercial businesses might be offered loans at interest rates determined by a margin applied to a benchmark rate, such as BBSY — a bid reference rate usually about five basis points above the bank bill swap rate.

“The purpose of the notification (to customers) is to ensure that, in the event that market benchmark rates were to turn negative, zero would be applied for BBSY in any relevant business loan,” the Westpac spokesman said.

The solution could expose Westpac and the Commonwealth Bank to criticism.

If a negative reference rate is “taken to be zero”, the bank’s profit margin, or the premium charged to the customer above the reference rate, would be preserved. Otherwise, the margin would be eroded.

RBA Governor Philip Lowe said last year it was “extraordinarily unlikely” that the cash rate would fall below zero in Australia. But that was before the COVID-19 pandemic crashed the economy.

The guidance was reaffirmed only last month, when minutes of the central bank’s March special board meeting said directors agreed that the 0.25 per cent cash rate was its “effective lower bound” — the point at which any further monetary policy adjustment lower was counter-productive.

“Members had no appetite for negative interest rates in Australia,” the minutes said.

Interest rate markets have priced in more than a 50 per cent chance that the central bank will cut the cash rate again at its meeting on June 2. This will see the current 0.25 per cent cash rate moved to zero.

Dr Lowe is scheduled to appear on Thursday at a webcast event with Australian Prudential Regulation Authority chairman Wayne Byres and Australian Securities and Investments Commission chair James Shipton.

One source said that, with key benchmark rates such as the bank bill swap rate trading at about 10 basis points, it was prudent for the banks to prepare for a scenario where they could dip below zero.

This could occur even when the policy rate remained above zero.”

LikeLike

Yes, I saw that too. It is an astonishing failure, altho more so by the RBNZ which has always been more open to negative rates than the APRA, and which has full powers as both the mon pol entitiy and the prudential regulator.

Having said that, the specific issue alluded to here just cannot be that hard to resolve (in a time when govts manage to get multi-billion dollar support schemes up and running in days), and borrowers would certainly be strongly incentivised to agree to any documentation changes that allowed negative rate benchmarks (BBSW or BKBM) to flow through fully.

Perhaps one day a serious media outlet will tell us why these sorts of issues never seem to have been a big obstacle in Japan or the large chunks of Europe.

LikeLike

“From highly-paid public figures charged with conducting a nation’s monetary policy, it is simply stubborn, verging on the crazy – the more so if the MPC thinks that sticking to that pledge in any way enhances the sort of credility that matters”

Like all ideologues, just because you are articulate and vociferous about the topic doesn’t mean you are right or that officials should be pilloried day after day just because they (and most other people) don’t see the world as you do. The stubborn, obsessive one is not the Bank in my view. The projections are little more than guesses based upon fairly broad assumptions for different scenarios at the moment because no one knows for sure how the recovery will evolve.

Frankly, sticking to their promise does enhance their credibility to me.

LikeLike

Yes, the scenarios are “little more than guesses”, but (in the Bank’s own words) they are descriptions of the sort of view the Bank says it is conducting monetary policy under. Decisionmaking is occurring under extreme uncertainty, and in extreme uncertainty it is v unwise to make pledges about levels of specific instruments that are desiged to be highly responsive to changing outlooks.

Clearly views will differ. I admire someone who sticks to their marriage vows through tough times, and I seek to have imprisoned someone who rashly says “i’ll kill you” and that reckons they need to follow through. Quite where the Bank’s pledge sits in such a spectrum is up for debate, but I will continue to seek to persuade people it is nearer the latter than the former.

LikeLike