I was chatting yesterday to someone about what might be in the Reserve Bank speech today on “The Global Economy and New Zealand” . I noted that whatever else the Assistant Governor might have to say we could be pretty confident that he would be repeating the line that changes in the world economy typically affect New Zealand trade – as a commodity exporter – more through price changes (adjustments to the terms of trade) than through volume changes. That is particularly so for dairy – cows are still milked – but it makes us somewhat different from economies whose external trade is heavily manufacturing in nature, often as part of multi-stage international supply chains.

Sure enough, there it was in the speech

When considering global influences on New Zealand exports, we have historically focused more on export prices than volumes. This reflects that in the past New Zealand’s exports have been dominated by primary sector products whose production volumes are relatively insensitive to fluctuations in short-term demand. Export prices tend to fall in tandem with the global economy—low global demand should lower prices.

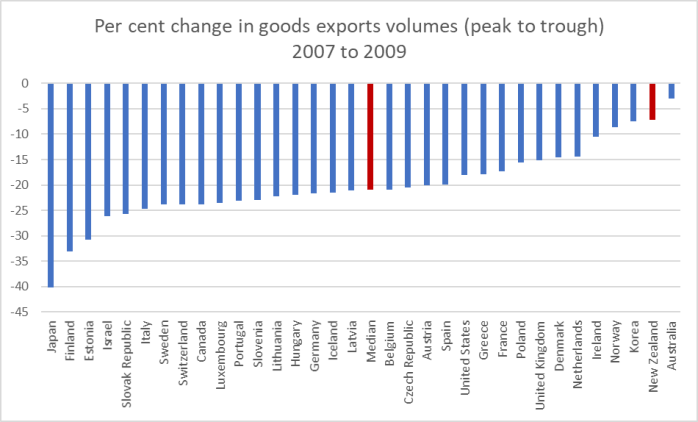

While waiting for the speech to be released I had been playing around with some numbers to illustrate the point, at least with reference to the last significant global downturn, the recession of 2008/09. Here is a chart of the percentage change in the volume of goods exported from each OECD country from peak to trough over the 2007 to 2009 period (both peak and trough quarters differ from country to country). Disruptions to trade finance was also a material factor in some countries during that particular period.

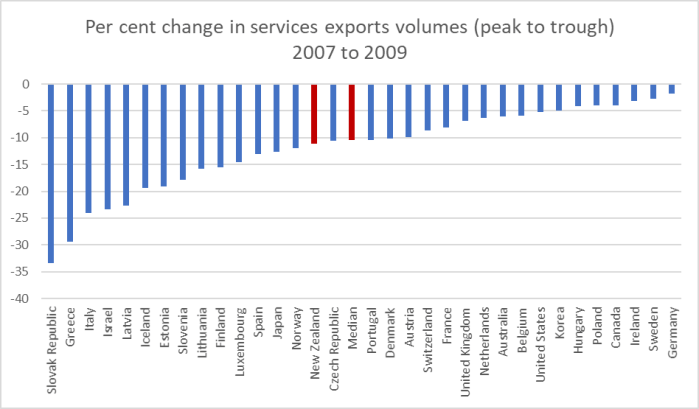

And here, by contrast, is much the same graph for the volume of services exports

Our services exports – concentrated in discretionary items notably tourism and export education – actually dropped slightly more than those of the median OECD country (as did that other commodity exporter Norway, and even Australia had a reasonably material fall in services exports). Note how different the Japanese and New Zealand goods exports experience were but how similar the services exports outcomes.

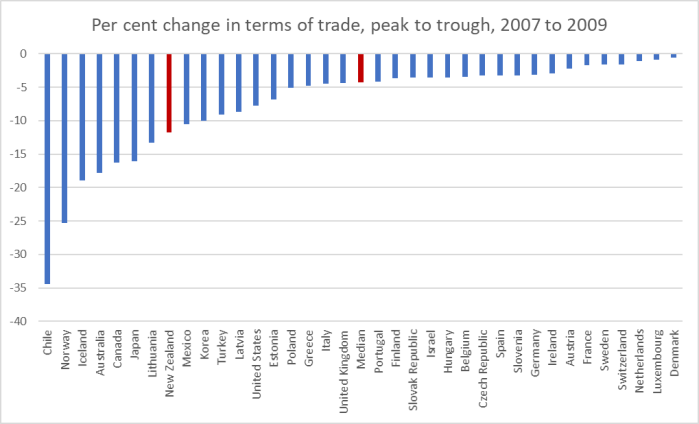

To illustrate the price effect I’ve chosen to use the terms of trade rather than export prices. Here is the peak to trough fall in the quarterly terms of trade for each OECD country over the 2007 to 2009 period,

Most of the countries with the largest falls in the terms of trade over this particular period were primarily commodity exporters. But although our terms of trade did fall by more than the median country New Zealand’s fall was not that severe (much less so than Chile and Norway, or even Australia), and was slightly smaller than the fall Japan experienced. (I suspect that if we could break out goods and services terms of trade separately, we might find that the services terms of trade improved (often happens, especially around tourism, when the exchange rate falls) while the goods terms of trade fell quite sharply.)

Some of these results will be idiodyncratic to the particular event, so I wouldn’t want to make too much of them, but the services chart in particular is a reminder that for some – quiter labour-intensive – components of exports, the volume channel is just as important here as in many other advanced economies.

What of the Assistant Governor’s speech itself? There wasn’t really that much there, and one can’t help suspecting that anything of interest was in the Q&A session afterwards, especially given the potential short-term disruptions from the coronavirus. Recall that whereas the RBA makes available recordings of Q&A sessions after speeches by its senior managers, the Reserve Bank of New Zealand does not. That is not very satisfactory.

I was, however, struck by a few errors and what looked like government-aligned spin.

Hawkesby asserted that

Another development worth noting is the increasingly diverse nature of our exports, with the growing importance of our service exports and the growth in the technology sector.

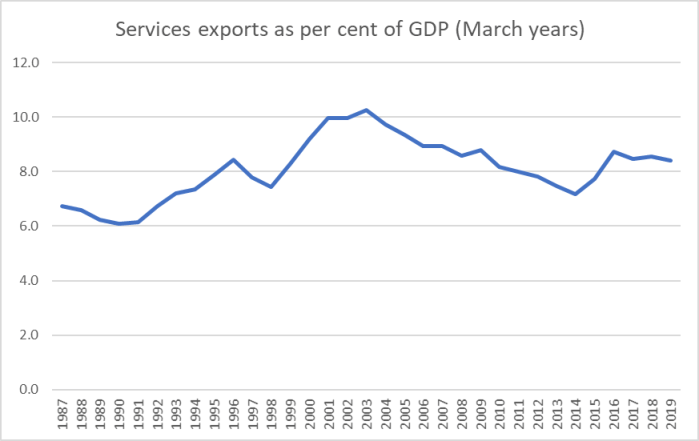

Well, here is the data from the latest annual national accounts

As a share of GDP, services exports peaked in the year to March 2003, almost 17 years ago now. Even over the last few years, there has been a slight shrinkage. Who knows what the Reserve Bank had in mind, but these are the official data.

Oh, and then there was the misleading statistic that will not die, because it keeps getting run out by ministers, industry advocates, journalists (who perhaps know no better), and now (apparently) the Reserve Bank.

While our exports are still dominated by primary goods and tourism, technology is now New Zealand’s third largest export sector, with exports growing 11% to $8b

There is a footnote on that statistic to the TIN Report. But even the TIN people will concede, if you dig deep enough in their reports, that this simply isn’t an apples for apples comparison. It might be quite interesting to know how much New Zealand owned companies sell globally, but that is quite different matter/statistic from New Zealand exports (which are about production here, whether by foreign or domestic-owned companies). I highlighted some of the problems in this tech story in a post a couple of years ago (when the underlying picture didn’t look flattering at all). I don’t expect the Reserve Bank to read my posts, but I do expect the Assistant Governor for economics to know what exports actually are. As it is, his is an apples and oranges “comparison”.

In fact, if he’d wanted to give his audience a fairer picture of New Zealand the global economy he might have mentioned that overall exports as a share of GDP are weak (well below peak, well below what one might expect for a country our size) and that tradables sector output has long been similarly subdued.

And then there was the final piece of spin

Climate change is also likely to impact New Zealand’s economy in a number of ways in the future. Growing environmental regulation of the primary sector, for example, could result in an acceleration in the diversification of our export industries.

No doubt that final sentence is some part of the story, but it seems to rather ignore the main event: whether or not one agrees with policies the government is adopting in this area, the overall effect seems more likely to be a shrinkage in the path of primary sector production, at least relative to the counterfactual. But I guess the Governor and the government wouldn’t have been too keen on him mentioning that. (I’m not really suggesting he should have – these long-term issues don’t have anything much to do with the Reserve Bank, but playing parts of the story that suit political masters wasn’t necessary either.)

But then on the final page there was another longer-term reflection that caught my eye

There are uncertainties, for example, about the future openness of international trade and labour markets. There has been a growing geopolitical trend globally towards protectionism and lower migration. Rising global protectionism could reduce our export opportunities and lower migration into New Zealand could dampen our growth, but might spur investments in domestic productivity.

I’m not sure that second sentence is empirically well-supported, at least as regards the migration bit. I’m curious which countries the Assistant Governor has in mind, and noted only the other day achart highlighting the significant increase in work visas being granted in the US in recent years (and governments in other big recipient countries, notably Canada, Australia, New Zealand and Israel, don’t show much/any sign of reduced enthusiasm for immigration). But what interested me was the final sentence and the suggestion that (structurally?) lower migration to New Zealand “might spur investments in domestic productivity”. I think so – it is a key element in my story, about reducing pressure on the real exchange rate, narrowing the gap between New Zealand and world real interest rates, reducing the need to focus investment (including public) simply on keeping up with population growth – but was (pleasantly) surprised to see the Reserve Bank saying so. Intriguing, to say the least.

Perhaps unsurprisingly, there was only passing mention in the speech – no doubt mostly finalised last week – of the coronavirus. There was a reference to the SARS experience providing some possible parallels – at least if the virus ends up being contained. But it is worth remembering that the PRC is a much larger share of the global economy than it and/or Hong Kong were in 2003, that the shutdowns already seem much more extensive than happened then, and that tourism from the PRC – almost entirely a discretionary item, much already interrupted by the PRC – is a much more important share of the New Zealand economy than it was then. And in 2003 SARS was one of the factors the Bank cited to justify cutting the OCR that year.