It was anything but a slow news week globally, but here in New Zealand not much seemed to be happening (not even much summer, at least in Wellington). Perhaps that was why the Sunday Star-Times chose to devote two full pages (with the promise of more in the next couple of weeks) to the hardy perennial cause of – in the words of the headline – “More financial literacy needed”. Especially (it appears) for kids, from schools. In years gone by, there have even been public opinion polls – paid for by people championing the cause – suggesting that the public agree.

I’m as sceptical as ever, perhaps more so as my own kids have progressed through the education system. What follows is mostly from a post I wrote on the issue a few years ago

I’m sceptical at a variety of levels. First, and perhaps most practically, these surveys (and the reported views of advocates) never ask what people would prefer schools to stop teaching. There are only so many hours in the day/year. I’d face the same question as to what should the schools stop teaching, but given a choice, personally I’d rather that schools were required to teach a sustained course in New Zealand and British/European history than that they teach so-called financial literacy. Kids are exposed every day to their parents’ attitudes to, and practices with, money and things. They aren’t directly exposed, to anything like the same extent, to maths, science, history, or foreign languages.

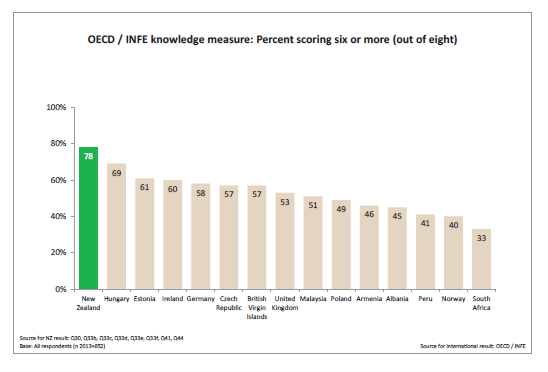

Second, as far as I can see, the evidence is pretty mixed as to whether teaching “financial literacy” makes any difference to anything that matters. Are countries with higher “financial literacy” scores richer as a result, more stable, happier? And a recent report (page 32) for our own government agency that deals with this stuff actually showed that, for what it is worth, the “financial literacy” of New Zealanders scored quite well in international comparisons. What is the nature of the problem?

Third, why would we expect that the government, and its representatives, would be good people to teach children about money? …at a bigger picture level, in one way or another governments are the source of most financial crises – Spain, Ireland, Argentina, the United States, China. Governments are more prone than most to undertaking projects that they know provide low or negative economic rates of return. Governments face fewer market disciplines than citizens. And governments don’t have to live with the consequences of their mistakes. So perhaps I could support a civics programme that included a section on critically evaluating election promises and government policy announcements.

Fourth, much of the discussion in this area is quite strongly value-laden. And no doubt it has always been so. I recall the day when our 6th form economics class was visited by a banker, to try to promote savings etc. He brought along a hundred dollar note – this was 1978, and it was probably the first time any of us had seen one. Trying to set up a discussion about the merits of bank deposits (probably with negative real interest rates at the time), he asked us all what we’d do with the $100 if we had it. Various class mates rattled off their spending wishes, but the banker was totally flummoxed when one of my friends, a strong Christian, told him that what she’d do was to give it away.

And where, for example, in all the discussion of financial literacy is there any reference to the idea that one of the best routes to financial security is to get married and to stay married? There are elements of both causation and correlation there, but finding the right spouse, and learning what is required to make a lifelong commitment work, is almost certainly a more (financially) valuable lesson that knowing that when interest rates fall bond prices rise. But it is not one we are likely to hear from the powers that be – particularly not under the current government.

And fourth, this becomes an excuse for yet more bureaucratic/political bumpf, reinforcing a sense that governments should have “strategies” about everything and anything. I was somewhat surprised to learn that our government has a financial capability strategy. Why?

Building the financial capability of New Zealanders is a priority for the Government. It will help us improve the wellbeing of our families and communities, reduce hardship, increase investment, and grow the economy.

The National Strategy for Financial Capability led by the Commission for Financial Capability provides a framework for building financial capability. It has five key streams:

- Talk: a cultural shift where it’s easy to talk about money

- Learn: effective financial learning throughout life

- Plan: everyone has a current financial plan and is prepared for the unexpected

- Debt-smart: people make smart use of debt

- Save and invest: everyone saving and investing

On this measure, might we assume that “debt-smart” would mean taking as much interest-free student debt as possible and paying it off as slowly as possible? Not an approach I will be encouraging in my children.

More generally, I’m not sure that any of these items represent areas where we should expect governments to bring much of value to the table. One might marvel that human beings had got to our current state of material prosperity and security – let alone how our pioneers built a country that was once the richest on earth – without the aid of government financial literacy/capability strategies. And since when has a traditional Anglo reticence about matters of money been something for governments to try to change? Better perhaps might be a focus on improving the financial capability of governments.

The Commission’s own research (p 26) shows what one might expect, people develop more “financial literacy” as they need it. So-called “literacy” is low among young people (18% of 18-24 year old males are “high knowledge”), who don’t need it much. It rises strongly during the working (child-rearing, mortgage etc) years (53% of 55-64 males are “high knowledge”), and then looks to tail off a little in retirement. All of which is unsurprising, and (to me) unconcerning.

I know the so-called Commission for Financial Capability doesn’t cost that much money, but as I’m sure they would point out, every little counts. The money they fritter away on national strategies and capabilities is money that New Zealanders don’t have to spend, or save, for themselves.

As an easy way into this, consider this US-government funded online quiz, a shop window for a US project on better understanding financial literacy. I imagine that most readers of this blog will score 6/6, while the average American scores 3. But then stand back and ask yourself why the average American (or New Zealander) needs to know the answers to these questions, phrased rather in the manner of a school economics exam. People who read blogs like this take for granted a knowledge of the answers, but in what way has that knowledge made your life, or mine, better?

Back to 2020. As ever, in the Sunday Star-Times articles there is no hint of what schools might sensibly cut back on to squeeze in more financial literacy teaching (or “money mojo” as a couple of middle-aged commentators suggest calling it). It isn’t as if our core school academic results – maths, English, science etc- are so impressive that the marginal time would be a zero cost resource. There are only so many hours in the day, weeks in the years, years in a school life. And in recent years, schools have been told to add “digital literacy” to their teaching, they are about to be required to teach New Zealand history (something I generally welcome), and seem to devote ever more time to climate change issues (“all we ever heard about in social studies”, in the words of one of my kids). And yet you’d have thought that binding budget constraints would have been one of the ideas anyone wanting to teach financial literacy would be conscious of themselves, and take seriously.

Similarly for all the talk in the articles about how tough life is, there is no hint of any recognition that (say) average labour productivity (the underpinning of average material living standards) even in underperforming New Zealand is now more than 50 per cent higher than it was when I left school. And equally no hint of any recognition of the role governments – the people who would be teaching “financial literacy” – have played in the alarming underperformance of our economy. There is some mention of housing challenges, but none of the conscious and deliberate choices governments made, and keep on making, to render decent houses all but unaffordable to young families in our larger cities. Fix that at source and life (financially) would be a great deal easier for many of our lower income people. But that would involve governments making good and responsible choices, not continuing to shred the prospects of each successive generation. Even then, there would still be no obvious role for governments doing “financial literacy” education, but at least our governments might have a little more credibility as some fount of discipline and financial wisdom.

Parents do “financial literacy” all the time – not necessarily in the words they use (some more reticent than others) but in the choices they make, and which kids see them making. About consumption, about debt, about giving, about choice and opportunity cost, about budget constraints (if not in quite those words), about celebration (and self-denial), about partnership – about casts of mind (extravagant, frugal or whatever). We model – often inadequately perhaps – the values we encourage our kids to live by. It is how society works, and always has.

And I’m quite sure I don’t want Jacinda Ardern, Chris Hipkins, Simon Bridges, Nikki Kaye (or the teachers’ unions) getting in the way with their corrosive views. Rather better that the politicians focused on fixing the stuff that governments messed up in the first place. I was having a sad conversation yesterday with my daughter, who asked if it was really true that houses had once cost less than $100000. I had to explain briefly the idea of general inflation, but went on to tell her that when I was first house-hunting in 1985 I’d looked at several decent places priced at around $80000. Adjust for the CPI and that would be around $230000 today, but try looking for a house in south Wellington for $230000 – even one with 1985 type fittings, decor etc – and you’ll be stiff out of luck. Even at twice that price it would be almost impossible. That is deliberate government recklessness.

Welcome back & happy new year. Good article, thanks. As a matter of interest, and picking up on your comment about ‘debt-smart’ young adults and their student loans…can you point me to any previous articles of yours on this in a general sense please? Thank you.

When I was at high school in the early to mid 70s I enjoyed what was then called ‘commercial practice’, which ranged from junior accounting to banking to commerce. It was a pleasant & interesting change from the more academic subjects. I took it for school cert I believe.

LikeLiked by 1 person

Thanks. I don’t think I can recall any post on the student loans/young adults point. Mine here was just a passing comment that I would never encourage a young person to borrow, even interest free, for the sake of borrowing (even just to put the proceeds on term deposit). There is something wrong and opportunistic about it.

LikeLiked by 1 person

So the student loans taken out to complete a University education is wrong and opportunistic?

LikeLike

The best use of funds for financial literacy should be towards the education or screening the members of parliament. The financial decisions of our politicians and civil servants are the most consequential. I have serious doubts about the numerical ability of many of them. The political system selects for particular types of individuals: those high in verbal fluency, high self-regard, and networkers. It does not select for critical thinking or basic numeracy. The policy failures such as a billion trees, affordable homes illustrate the consequences of the lack of basic skills.

I suggest that all MP should have a basic financial literacy test, at a level of a first-year university student.

For the rest of the student population, the syllabus should include the basics such as compounding interest rates etc. I am sure the syllabus already includes those topics.

The poor financial decisions many people make likely reflects behavioural traits such as impulsivity and going along with the crowd. If there is education on financial literacy for students, they should discuss why people make the financial decisions that they do, despite being against their long-term interest. But are teachers the best people to lead these discussions, many are not great in making financial decisions themselves.

LikeLiked by 1 person

I don’t think our politicians have a financial literacy issue. It is more a honesty and integrity issue based on self preservation and political survival and of course keeping that $350k per year cabinet MP job.

LikeLike

My mother-in-law was totally illiterate, couldn’t even write her name but she was financially literate. My mother worked in a bank 80 years ago and she read letters for customers who were illiterate farmers but they had no problem with financial literacy. Meanwhile my wife is an accountant and I love numbers and we are both money minded so I seriously doubt any school classes will have more effect that living in our home. But some of our six children are wise with money and some dumb.

The child who suggested giving the $100 away was right. Always avoid unearned money. A good rule to start life with.

Your article’s skepticism is correct. Education is preparation for adult life. Unfortunately it doesn’t solve the most important matters: telling right from wrong and choosing appropriately, learning how to get on with others, respecting those who deserve it, etc. What it can do is teach a child how to Read. Everything else is secondary. Those secondary skills are Writing, English comprehension, Numeracy, General knowledge. And the general knowledge will vary with the times but would always include maths, history, geography, science and languages.

Teaching financial literacy would be like teaching ethics. They might produce students who regurgitate the answers to pass exams but would they produce adults who always behave ethically and always manage their finances wisely?

LikeLiked by 1 person

Teaching kids relationship skills would help with the housing market supply too, not just wealth. One couple splits, 2 residences required. Of course recoupling makes the maths more complicated, but you can be sure that relationship breakdowns increase demand for housing, never mind the huge financial hit that breakups cause.

LikeLiked by 1 person

Get married ….

Many years ago, a conversation over a beer, tradesman client told me of his approach to wedded bliss. He was a panelbeater, came from a very stable family life .. met a young lady who was lovely, tall and gangly … they dated for 6 months and she pressed to get married … he told her that when she has saved up (in todays equivalent money) $300,000 he would marry her … she did … he did … they are still together these many years later

I got married to a dolly bird, much to my regret. Years later I recalled his story, and realised I should have done the same, and sat down with my prospective bride and negotiated “our plans” together. The marriage didn’t last and cost me dearly, including half my inheritance from my deceased fathers estate

LikeLike

This is the way

Financial literacy is built up over a long period of time. It is not instantaneous. One needs to follow all the news all the time wherever it happens in the world and watch how markets respond.

Look at the NZ Herald

All their entire Business Section on a Saturday is paywalled

During the week 90% of their Business Section is paywalled

OTH the NZ Herald property section nothing is paywalled

LikeLiked by 1 person

Two closely related thoughts on this. Financial literacy depends to a degree on numeracy and on more general literacy. This includes ‘media literacy’ which in this context means being able to read and understand advertising. A degree of healthy skepticism is also needed.

Armed with these skills, a citizen can work out for themselves that “nothing to pay for 20 months and $X a month” is not necessarily a great deal. On the flip side, someone in their late teens or early twenties can figure out that even a few percent compound interest can add up to a huge amount over 45 or 50 years of saving.

LikeLiked by 1 person

If you factor in inflation then savings interest alone equates to 1 step forward and 20steps backwards. Not exactly the best financial literacy to learn?

LikeLike

Correction: 1 step forward and 2 steps backwards.

LikeLike

If there was one thing they could usefully teach in NZ schools is ethics and civics… all your subjects are on point, but we lack in NZ any teaching of how to live in a community, being a responsible citizen etc etc… I agree with all your points on financial literacy… I just can’t see that there is a problem to solve… when push comes to shove most people will work it out for themselves…

LikeLiked by 1 person

Taking the US quiz as an example (it is broadly similar to ones I have seen from NZ) you can break the questions usually into two categories – either basic arithmetic ones where the answer reflects compound interest effects (giving sometimes counter-intuitive answers), or broader economics (school subject) questions… a third category, but not present in that quiz is more ethics/social justice style questions.

The first category is just applied maths and should be being taught as part of maths syllabus. If people are struggling with these questions then that is a failure to teach the core curriculum (I’m not surprised there is such a failure). The second category is more specialised and is already dealt with in school economics. I don’t think people need to know about this generally to have a financially secure life – if you are investing and what to know what is a wiser decision then get a broker or adviser. As in that US quiz, the questions are framed as “typcally what happens” – there will be exceptions and that kind of nuance ought to be taught in a proper academic setting.

The third category is what the bureaucrats have in mind (secretly) – “economic” questions around climate change, market failure etc. If taught it could be interesting and valuable for children, but as you point out, its broader than just pure monetary style questions… rightly belonging in a philosophy / ethics course. I would support that in principle, but not with the current batch of marxists we have running NZ.

LikeLiked by 1 person

My impression living among the Germans is that the financial literacy is much worse here in comparison to NZ – far more people rent homes and even those who buy tend to fix their interest rates for a very long time (I fixed ours as 10 years which would be viewed by most Germans as reckless gambling). Consequently you don’t need to follow reserve bank announcements with as much interest as you do in NZ, nor any of the things that go along with it. Nevertheless the German economy is, on balance, stronger than NZs. You hear some real howlers from people in government etc. where you can only conclude they have no grounding at all in basic demand/supply theory – e.g. rent controls are commonly proposed as a tool to alleviate rising rents (they are in place in many big cities) – this being the classic lesson you get taught in 6/7th form economics as a misguided solution to housing costs.

I think people, participating in a market, have the incentive to acquire the knowledge they need – if you own a car you will inevitably learn a bit about motors, gearboxes, etc. That doesn’t mean you need to learn motor mechanics at high school.

LikeLiked by 1 person

The Press is predicting more economic / population growth, but we will be a magnet for talent wanting to start high-tech industries.

Meanwhile there appears to be a slow down in tourism. My wife (Japanese) tells me people now have have a visa and that adds to the costs, I’m not sure if that’s the issue as cruise ships are up. 91 come to Akaroa/Lyttelton this season. Either way in the bus industry it feels like climate change action is happening (sit at home – garden).

LikeLike

The slowdown is likely due to the way customs treat tourists not as people but as animals. Firstly on arrival, the China Eastern Airline ran 2 spray cans of insecticide into passengers faces. Then it was announced additional spraying due to change in procedure and 2 Customs officers arrive and sprayed another additional 4 cans of insecticides right into the faces of passengers. I was almost choking on that insecticide as they stopped the air conditioning whilst they sprayed.

Then they queue you like animals at the Auckland Airport for bio security checks. There was a sign that said nothing to declare queue but they did not believe you anyway so all queues still led to the X ray machines jammed packed. This must be one of the most militant airports in the world.

In London the NZ passport was treated like royalty. No queues and super fast clearance.

.

LikeLike

So many comments about what is taught in schools and no mention of yesterday’s news about the removal of religious education from our schools. As a committed atheist for over 55 years I’m strongly in favour of religious education since getting people to think about religion is critical for the growth of atheism; Mr Reddell will not agree with this.

If you asked people throughout the world and throughout recorded history what truly mattered to them the majority would say their faith (maybe followed by their family). Out of respect for our ancestors and respect and understanding of the majority of the world’s population religion should be taught. We have reached a unique moment in history when religion is treated as a bizarre foible of a minority.

It will be a sad day when my grandchildren don’t understand me when I talk about Good Samaritans or Mary & Martha and they cannot appreciate the original impulse that created Handel’s Messiah or Europe’s cathedrals.

Judging by this change with religion out and finance in our Education Department believes our new supreme being is money.

LikeLiked by 1 person

I think the current religious instruction provisions are a bit anomalous, but I have no real objection to them since parents have always been free to opt out their kids (and when I was at school, there was no obvious stigma on any child who was opted out). That said, the half hour’s religious instruction would do v little to form anyone in the background to our literature, music, architecture etc.

It would be a shame if that background were lost (across a broad spectrum) but (a) it is probably inevitable (absent a serious revival of Christian faith in our societies) and (b) has largely already happened in demographics any much younger than you (I was reading a book over the holidays called “The Last Pagan Generation” – various key figures in the Roman world in the 4th C, and in a way people like you – raised in the 50s – are almost the last Christian generation (not that you personally are Christian, but that it was the default backdrop to western society).

As a new “religion” or “worldview” takes hold it seems almost inevitable to me that what went before – even its greatest creations – will be marginalised, scorned or at best forgotten, at least outside a few specialist academic depts, and lingering minorities of people adhering to the old faith. Perhaps a few bits will be adapted for new use, and the origins forgotten – as one small example, one the drive south last week we listened to the audiobook of the 19thC childrens’ classic Heidi. I had absolutely no idea how suffused it was with Christian belief/practice – not surprising that I was surprised as most modern versions write it out of the story.

LikeLiked by 1 person

I think the Bible went onto the wayside for many parents and teachers when the Sumerian Clay tablets written thousands of years before the first known bible in the cuneiform text got translated and many of the Bible stories were represented in the history and stories of the Sumerian people.

LikeLike

Reminds me of an Australian Muslim cleric who remarked about his city council celebrating seasonal festivities or some such rather than Christmas “It is not multi-cultural but no culture”.

Your prediction is gloomy; if true it will be like those Romans 1000 years ago squatting in the ruins of Imperial Rome without any idea who had built them.

LikeLike

One could argue that improving Financial literacy, would be best achieved by more adult education funding, but like much on the education spectrum it tends to be presented as something that should happen to other people, rather than we all need to keep learn.

There is a quote that I can never find the origin of, which goes something like this

“In poor countries the poor work hard and in rich countries the rich work hard”

And in our context would suggest the problem is the poor financial habits of our wealthy that is the issue.

LikeLike