There were some good aspects to yesterday’s Reserve Bank Monetary Policy Statement:

- the Bank has abandoned its long-running over-optimism about future productivity growth and has thus revised down its estimates of potential (GDP) growth to more reasonable rates. Nothing in the economic strategy – this government or its predecessor – seemed set to deliver better, and it is good that the central bank has stopped spinning candy floss numbers (at least on that count),

- the Governor also seemed less effervescent, and perhaps consistent with the previous point there was little or no spin about just how well the economy was doing,

- in the document there weren’t even further direct calls for more government spending/borrowing. This change was defended on the grounds that the message had already been given, but I doubt that was all there is to explain the change (having said something once, even loudly, rarely discourages central banks from saying them again),

- oh, and the folksy Maori salutations at the start of the main statement – beloved by the tree-god Governor when it was his statement alone – seem to have quietly disappeared. Perhaps we might hope for the eventual quiet discontinuance of the cartoon version of the statement too?

But that was about all that could be said for it.

The document itself was weak on substance, building on consistently poor (largely non-existent) communications from the Bank.

You can tell that there are problems with communications when the Governor is reduced to repeating (numerous time in the parts of the press conference I saw) “we are trying to be as transparent as possible”. He isn’t seriously trying, and certainly isn’t succeeding. We’ve not yet had a serious speech on the economy and monetary policy from the Governor, after seven months we’ve heard not a word from four of the MPC members (including all the externals), background papers aren’t released even with a long lag, the MPS documents themselves offer ever-less insight or sense of how (or even whether) the MPC thinks in depth about the economy, and the Bank holds data close to its chest when it could release it more promptly (asked about this latter point yesterday the Governor did undertake to review their practice).

When two successive MPS OCR wrongfoot those paying closest attention to the data and to the Bank, it suggests the problem is with the Bank, not the observers. It would be interesting to know what advice the Bank’s financial markets staff gave the MPC about the market movements that were likely to occur as a result of yesterday’s decision.

It was only a few weeks ago that the Assistant Governor, Christian Hawkesby, gave a speech on central bank communications, probably mostly trying to fend off criticism of how they’d done in August. In that speech he highlighted – and overstated, at least in practical terms – the risks if central banks do what markets expect them to do

In this scenario there is a danger that markets end up paying too much attention to our communications for what we have said ‘we will do’, leaving no one left to analyse the incoming economic data for what ‘we should do’. As a central banker, I am far more interested in listening to what ‘we should do’.

And yet, yesterday’s MPS suggested that Hawkesby and his colleagues actually had no interest in that perspective either. As I noted in yesterday’s post, the MPC has had available to it throughout its deliberations the results of the Bank’s survey of expectations, the macro views of several dozen informed observers of the New Zealand economy. I wrote about the results yesterday. Those respondents expected the Bank to cut yesterday (and again next year) and even so they didn’t expect two-year ahead inflation to get above 1.8 per cent and expected no rebound in GDP growth either. Implicit in those numbers (and consistent with the mandate given to the MPC by the government) is a pretty clear view that the Bank should have cut the OCR, and should probably do so again next year. The Bank, apparently uninterested, chooses to ignore this weight of opinion and runs with its own idiosyncratic view that even with higher interest rates they were still get the growth rebound the outside observers couldn’t see (either three weeks ago when they completed the survey or – judging by comments from market economists in the last day – now). In the end, the MPC is charged with making decisions, but having got things wrong – below target inflation – for the last decade, the onus is surely on them to explain why they (mostly non-experts themselves) are so willing to back an away-from-consensus call. But they made no effort to.

In fact, if you started into the document without knowing the bottom line you’d think the case for easing yesterday was pretty unambiguous. They told us that the economy had slowed and risk were to the downside, the world economy was slowing, inflation expectations were very low and/or falling and, of course, core inflation was below target. And all that without even so much as a single mention – in the entire document, includung the minutes – of the apparently significant tightening in credit conditions respondents to their own credit conditions survey were foreshadowing, those same respondents having highlighted regulatory changes (ie most likely the coming big increases in minimum capital requirements) as a big issue.

Or perhaps the MPC is back to thinking that credit conditions really don’t matter at all? Surely, either way it would be reasonable to explain their perspective. Instead they seem to have simply ignored the issue (or tried to pretend the Governor’s whim wasn’t an issue – I heard Hawkesby on the radio this morning saying they had in fact taken account of credit conditions issues, in which case the OCR decision is still more mystifying, and the absence of any reference in the official documents looks even worse).

Or perhaps the MPC is back to thinking that credit conditions really don’t matter at all? Surely, either way it would be reasonable to explain their perspective. Instead they seem to have simply ignored the issue (or tried to pretend the Governor’s whim wasn’t an issue – I heard Hawkesby on the radio this morning saying they had in fact taken account of credit conditions issues, in which case the OCR decision is still more mystifying, and the absence of any reference in the official documents looks even worse).

One of the disappointing features of yesterday was that there were signs of the Wheeler Reserve Bank returning. Under the former, not widely lamented, Governor we heard endlessly from the Bank about how stimulatory monetary conditions really were – even as inflation just kept on falling below their forecasts. There was a lot of that line yesterday. As then, so now, the Bank does not have a good read on where the neutral interest rates are, and the best guide is really something like the rear-view mirror: all else equal, look at what is happening to demand (and early indicators like business activity measures) and inflation. In the Wheeler years, there was also a strong tendency to constantly be focusing on the merest hint that something might be picking up, because of the strong belief (see above) that conditions were “highly stimulatory”. It was all rather circular – we think we are right because we think we are right. There was quite a bit of that sort of flavour in yesterday’s statement too: both the forecast pick-up in growth (that few other observers appear to believe) and the repeated mysterious suggestions that inflation itself was picking up now.

In the MPS the Bank shows five core inflation measures, and also highlights as a preferred measure the (highly persistent and stable) sectoral core factor model measure

Across the wider suite of measures, there has been no lift since 2016. And the sectoral core factor measure has been flat at 1.7 per cent for more than a year. And core inflation is a lagging indicator in a climate where (to quote the Bank) the New Zealand economy has been slowing and the world economy has been slowing).

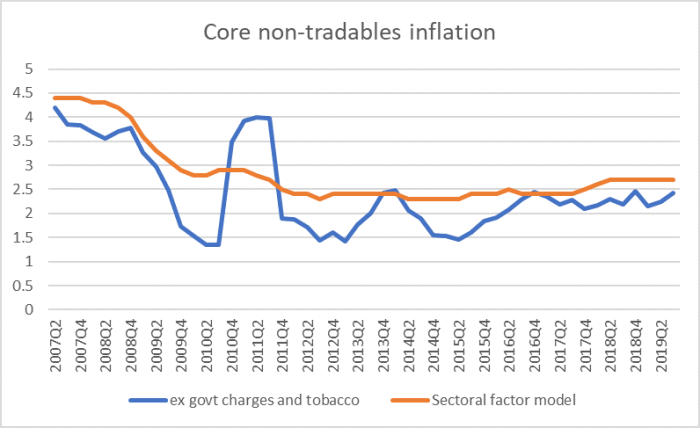

What about core non-tradables inflation? The headline non-tradables inflation rate did rise recently.

The blue line is an official SNZ series, while the orange line in an RB series. Again, no sense of any pick-up in core domestic inflation pressures – and nor, really, would one expect there to be in an economy where activity growth has slowed, unemployment has levelled out, confidence is low, policy uncertainty is quite high, and inflation expectations (remember them) are low.

In short, there was a (welcome and overdue) pick-up in inflation a couple of years ago, but there is no sign it is continuing. And – since the OCR cuts this year were against the backdrop of materially deteriorating fundamentals – there isn’t much reason to expect further increases in inflation from here on current policy (perhaps especially not when credit conditions are tightening, and RB announcements are pushing up interest and exchange rates).

Incidentally, one line – used several times yesterday – that you shouldn’t be fooled by was the one that “the projections were consistent with either choice – a cut or leaving the OCR unchanged”. Well, of course……. Unless practice has changed very very markedly from the way things were when I was closely involved in these processes, the final projections track – especially the interest rate track – is tailored to be consistent with the policy options and messages the decisionmakers (in my day the Governor, these days – at least on paper – the MPC) want to send. If the MPC wasn’t clear in its own mind last week what it was finally going to do, they’d prudently have ensured that the final track was consistent with either option. If they’d been clear but wanted to send a message that they’d been open to a possible cut, they have done the same thing. There is no independent evidence or perspective in (the first few quarters) of that track.

I want to circle back to the claims around the (asserted) high degree of transparency. One of the innovations in the new monetary policy governance model is the publication of the summary record of the meeting (aka “minutes). These are typically a bit longer than the initial policy announcement statement itself, and do provide the opportunity to note a few issues there wouldn’t otherwise be room for. But they are proving even less enlightening than one might have feared (given the way the Governor and the Minister got together to oppose a more genuinely open model, of the sort seen in central banks in places like the US, the UK, Japan, or Sweden).

Here are four examples from yesterday’s minutes. First, fiscal policy

The Committee discussed the impact of fiscal stimulus on the economy. The members noted that fiscal stimulus could be greater than assumed. The members also discussed the potential delays in implementing approved spending and investment programmes.

So far, so banal. As I noted earlier, in the official documents the Bank was back to staying in its line re fiscal policy (as the Governor said, “we take fiscal policy as announced and run on that basis” – which is how things are supposed to work). And yet this morning on Radio New Zealand Christian Hawkesby was heard stating that “we think more fiscal spending would be helpful in stimulating the economy”. If that is the Committee view, why isn’t it in the MPS or the minutes, if it was substantively discussed why isn’t it in the minutes, and if it is true then – given that the, as the Governor said, the Bank takes fiscal policy as given – isn’t Hawkesby’s statement further evidence that they should in fact have cut the OCR yesterday (if they think the economy needs more stimlus, and they are responsible for deploying the primary counter-cyclical tool)?

Then, the work programme on how the Bank might handle reaching the limits of conventional monetary policy

The Committee noted the Bank’s work programme assessing alternative monetary policy tools in the New Zealand environment, as part of contingency planning for an unlikely scenario where additional monetary instruments are required.

A statement which tells readers precisely nothing (especially as it is now three months since the Governor told a press conference that the work then was “well-advanced”). As it happens, reality seems a bit better than the minutes imply because when he was asked about this work programme yesterday and bringing it to light, the Governor revealed that they will release a document on frameworks and principles in the new year, and will (he says) be keen on feedback and discussion. That sounds more promising, but then where does the MPC fit into all this given the unrevealing comment from the minutes (and there are longstanding doubts about just who has power over any unconventional instruments – whether the MPC will get much say at all)?

Then we are told they had a discussion on an important immediate policy issue

In terms of least regrets, the Committee discussed the relative benefits of inflation ending up in the upper half of the target range relative to being persistently below 2 percent.

But that’s it. We are given no insight into the arguments deployed, the competing cases made, or the conclusion. Given their OCR decision we are left to deduce that the Committee would be quite worried indeed about (core) inflation getting above 2 per cent. But we are given no hint of why – despite 10 years now below that midpoint. And this is what the Governor calls being as transparent as possible?

And finally, the OCR decision itself

The Committee debated the costs and benefits of keeping the OCR at 1.0 percent versus reducing it to 0.75 percent. The Committee agreed that both actions were broadly consistent with the current OCR projection. The Committee agreed that the reduction in the OCR over the past year was transmitting through the economy and that it would take time to have its full effect.

And, again, that is it. No hint of the competing arguments – which could readily be done without identifying individuals – and no hint of why they chose to come down where they did? What were the key costs the Committee saw to cutting the OCR (especially when both market expectations and observer implict recommendations were to cut). There is no insight into the current decision or, importantly given the absence of speeches etc, no insight into the reaction functions/loss functions members (individually or collectively are using). It simply isn’t very transparent at all. The mantra overnight “just watch the data, just watch the data” isn’t really much use at all – especially when the MPC is going to run with such a non-consensus view of the data (and/or the risks around policy reactions).

It is all pretty underwhelming and confidence-draining. The point isn’t that a huge amount macroeconomically hung on any specific OCR decision. Nor for now is the economy in cyclical crisis – we aren’t in recession, inflation isn’t falling away sharply. The concern is that we have a central bank led by pygmies (no offence to the central Africans). Not one of the MPC members – all of whom are probably pleasant people (even the Governor if people aren’t challenging him) – command any great respect for their insight into the economy, their judgement or intellectual leadership, or for their willingness/ability to communicate a persuasive story or a sense that they themselves have a good and robust framework for thinking about the economy. In the case of the Treasury observer – who gets to participate not vote – it might have been her first ever significant meeting on advanced economy macro issues, but in the end responsibility rests with the voting members. They are failing us, corralled by the unconvincing Governor. Having substantially surprised the market (deliberately and consciously so) two MPSs in a row, and chosen to ignore consensus opinion on likely economic developments, you’d have thought we’d be hearing a lot from the MPC members – minutes that clearly outlined the issues and judgements, speeches articulating mental models and perspectives on the New Zealand economy, wide-ranging interviews (of the sort senior Fed officials give). Instead, we have weak official stories (the MPS), unrevealing minutes and – seven months into the new model – not a word in public from any of the external members nor from the Bank’s chief economist.

It isn’t good enough. The Bank’s Board should be demanding better, as should the Minister of Finance (including when he comes to appoint new Board members and the Board chair in the next couple of months). Transparency and communications aren’t about publishing forward tracks – one of the Bank’s own recently-departed researchers published research last year suggesting they make little difference – but about open and honest engagement, laying out the uncertainties and (inevitable) differences of possible perspective in a business characterised by so much uncertainty. How decisionmakers demonstrate that they handle uncertainty, competing narratives and even disagreement, is the sort of thing that helps build confidence, not rote publications (let alone poor, surprising, decisions) or Soviet-style phalanxes of grey bureaucrats all lined up with the Governor.

UPDATE:

You might think I sometimes put things fairly strongly (if often at considerable length). I wouldn’t have wanted people to miss this comment on my post left by a banker. It was both strident and succinct.

The Bank wrong-footed markets in August delivering what could only be described as a panic 50bp cut. Three months later, they argue there has been no meaningful change in the economy – not entirely true but close enough (dairy and housing up) – and then when the market is primed for a cut, they choose to sit on their hands.

I was advising my clients not to have exposure to the rates market and had FX positions well in the money (less so today) so was ok. But you only need look at the price action to know that the Governor has burned many people and people don’t take kindly to these types of loss.

If it was a line call, as the Governor repeatedly stressed, then given what was priced, he should have delivered. 25bp when it’s 70% priced in would do very little, but the damage he’s caused the bank is significant.

My clients respect for the RBNZ’s competence is very low.

LikeLike

I am unsure why speculators should be on a predictable gravy train? The NZ economy is moving in the right direction with its export prices for products moving up. Beef, lamb, milk, tourists, immigration all up. The big one is that the property market is heating up with the speed unseen previously. Best not to cut interest rates further. In fact Adrian Orr should be looking at tightening the LVR rules back to 35% equity to dampen what is looking like a fast heating property market.

LikeLike

Not the RB’s job to be beholden to currency trader positioning though.

I prefer central banks that don’t bow to market pricing and expectations. It will induce more volatility in markets (rates and FX, much needed) and consequently cause people to prepare for a wider “cone” of outcomes. This can only increase the robustness of the financial system.

LikeLike

Sure, but they survey measures and economist responses suggest that the people monitoring these things, and the Bank, most closely thought a cut was substantively warranted. They’ve chosen an outlier position, and could be proved right, but they haven’t exactly made a compelling, or consistent through time, case for it.

LikeLike

You’re too polite Michael… it was a bloody debacle!

LikeLike

I don’t really disagree, and it is good to have someone more strident (and succinct) than me.

Of course, and recognising the constraints they face (memories of Wheeler/Toplis) it would be good to see higher profile bank economistes speaking as firmly.

LikeLike

The RBNZ believes that the neutral OCR is currently 3%. If the neutral inflation rate is at target, then by definition, the RBNZ believes that r* is 1%.

If you include r* at 1% into a simple Taylor rule, assuming inflation is currently in line with the sector factor model at 1.7% and the negative output gap is -0.3%, then the OCR should currently be 2.4%. Hence their comment about policy being “already stimulatory”, and if you believe their forecasts, the next move in rates is higher, not lower.

BUT, if you were to say that the typical spread between the OCR and the 1yr fixed mortgage rate is around 250bp – as it is currently (more or less), then the Taylor rule with r* at 1% would imply fixed mortgage rates should currently be hovering around 4.9% and the equilibrium rate should be more like 5.5%.

The property market is buoyant right now, but I am guessing that if we saw mortgage rates rise back to 4.9-5.5%, the market would go stone dead (not to mention the tightening effect on monetary conditions of the rise in the NZD that would be engendered by that kind of interest rate).

which means that r* simply cannot be 1% right now…

…and therefore monetary conditions are not as stimulatory as the RBNZ thinks.

LikeLike

Which you would think someone at the Bank could work out. No doubt they can, but the message isn’t welcome at the top, so probably the good people who are left – mostly v young – just keep their heads down.

LikeLike

And monetary conditions became even less stimulatory after the market reacted entirely predictably to the decision. Would the MPC have had a view about likely market reaction when they reached their apparently unanimous decision? The bland statements about the committee’s deliberations and conclusions are mute on the subject of dissenting views. If there were none heaven help us.

LikeLike

I guess we don’t know when they made their provisional decision, altho probably late last week. At that point, the market wasn’t aware of the expectations survey data, but the Bank was, and so even then their fin mkts staff must have been able to anticipate some nasty adjustments if there was no change (and no strong easing bias either). By Wed morning, when in theory they made the final decision, it would be simply inconceivable that the Ctte wasn’t given pretty sound advice on the market reaction. And yet they plunged ahead….

Re unanimity or “consensus” as they officially put it, that is the problem with the current system: there is precisely no individual accountability and all those external members simply hide behind the Governor’s apron strings. Mind you, I’ve seen no sign of any journos ringing the externals and asking them to explain their decision/stance: the externals might have refused comment, but that in itself would be telling.

LikeLike

My property portfolio lost around $1 million in equity which represents about a 11% drop over the last 12 months and my Kiwisaver is running hot at 10% upwards returns for the year. Therefore the picture was rather mixed, although rising rents have given my cashflow a boost. However given that the property investment forums are running hot with new members and there is a stream of sell out crowds at Property investment conventions house prices are moving steadily upwards fast as more buyers enter the fray.

I did not expect the RBNZ to cut interest rates as beef and lamb prices are up. Milk prices are up and property prices are up. Tourist numbers are up and tourist spending is up. Internal migration numbers are also up.

I think Adrian Orr made the right and sensible call. By March 2020 the economy will be running hot even though inflation would stay low. Chinas production capacity is underutilised and its US markets are severely affected by rising import tariffs. The rest of the world just gets cheaper and cheaper products importing disinflation.

LikeLike

Peter and Michael,

Out of curiosity, may I ask your estimates of the r* ?

LikeLike

I don’t do formal estimates , but plausibly -0.5 per cent (bearing in mind that in most of the advanced world something like -1.5 looks more plausible, and that the factors that give us higher neutral rates than other advanced countries haven’t gone away). That might mean a neutral OCR here of not much above 1 per cent.

LikeLike

Hi Dean,

sorry just saw this. I think r* is closer to zero right now. That’s what I’ve been basing a lot of my analysis off, and it seems to work reasonably.

LikeLike

I wouldn’t take too much notice of the rise in dairy prices from a monetary policy perspective just yet.

My modelling points to a payout of around NZD 7.50/kgMS this season, rising to NZD 8.02/kgMS next season, and could be higher, but Fonterra are only paying out NZD 4.60/kgMS right now as the advanced payout, that’s below most farmers ongoing cost of production – and well below their all-in costs – so they have no surplus cash to spare from this. If Fonterra do deliver a payout in the region of NZD 7.50/kgMS, it will be a higher final payout made over the winter months, which remain some way off. To the extent that we have a higher payout, banks are going to make claim on surplus funds for many farmers, so the spill-over to spending will be modest. And the same dance will occur in 2020/21. So even if I’m right and we get a payout > NZD 8/kgMS, it’s going to be the winter of 2021 before farmers really get a boost to their income and bankers become more relaxed…

Sheep and beef farmers, a little different but they too have bankers breathing down their necks (just to a much lesser degree).

LikeLike

With the Australian Dairy lush wet greenary in brown drought and on fire, predictably as we progress the year and into the next those milk prices are going to lift considerably. I think it is a relatively safe bet that we would see rising milk prices.

LikeLike

Agree on prices. My chicken scratches suggest we could easily see a payout well above 8 next season, but not because of Aussie production. Aussie is moving inexorably to being a net importer of dairy products; ask OMF for my latest Monthly Dairy Report out Monday for a little article on it.

Key reason, EU and US production is weak – especially outside British Isles – and dairy profitability is terrible. Farming crisis in Wisconsin and the US North East at these prices while EU is adjusting to climate change.

LikeLike

A change or hold in OCR is a public power exercised for something like the public good. Surely, then, only the “substantive case” for or against a cut or hold can be relevant? This is to say nothing of mixed comms, or the robustness of underlying analysis. But seriously, tough cookies if non-productive economic activity like private FX trading has a tough day due to its mis-read of gibberish. Any other view on that issue is surely more than a tad entitled…

LikeLiked by 1 person