The Reserve Bank’s year ended last week on 30 June and it will, thus, shortly be time for the Bank’s Board of Directors to turn their minds to preparing their Annual Report.

Most of the powers of the Reserve Bank rest with the Governor personally, although late in the year the new Monetary Policy Committee picked up responsibility for the conduct of monetary policy. The Bank’s Board has no day-to-day (or strategic for that matter) decisionmaking powers. The job of the Board is, primarily, to hold to account those who do have decisionmaking powers. In an ideal world, their Annual Report should be a masterpiece of real accountability – these people are paid (not that well admittedly) to act on our behalf in evaluating the performance of the Governor and the Bank.

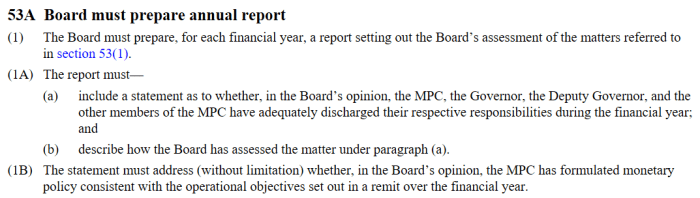

This is what the Act requires

Section 53(1) simply tells the Board, in slightly more detail, that their job is to “keep under constant review” what the Governor, the MPC, and the Bank are up to.

In many respects, this framework has long been a bit of a joke. The Board has limited expertise for some of its responsibilities (basically none re the monetary policy requirement above), has no resources, has the Governor himself sitting on the Board, and has been minded to set its role more as having the back of the Governor, rather than providing serious scrutiny (behind the scenes, let alone through the statutory Annual Report). And this has finally been recognised in the circles that count: the government’s consultative document on the Reserve Bank Act review proposes that in future the Board should be turned into a decisionmaking body, with monitoring and accountability responsibilities moving elsewhere.

The additional feature that made it unlikely that the Board would really provide serious scrutiny was their involvement in appointments. On paper, the Minister of Finance appoints the Governor and MPC members. But he can do so only on the recommendation of the Board. The Board – with no real expertise or democratic mandate – controls the appointments and – as is human nature – will want to validate their own choices and judgements. Perhaps it might be different four years into a Governor’s term, but the current Governor has been in office for little more than a year, and the MPC members only three months. There is some turnover on the Board, but the majority of the current Board members collectively made all thse appointments.

Each year since starting this blog, I’ve done a post on the Board Annual Report, sometimes one in prospect and one in retrospect. Possibly there has even been some useful impact. As I noted in last year’s post, the Board Annual Reports have improved somewhat over recent years. In my view, last year’s report even warranted a (bare) pass mark. But it was easy last year. The new Governor had been in office for only three months – honeymoon period and all that – and his predecessors, lawful (Wheeler) and unlawful acting (Spencer), had gone. If there were issues, mostly they were still the responsibility of the departed.

It will be interesting to see what the Board comes up with this year (we won’t see the published version until October). There are a lot of issues they really should be addressing. And as I was pondering the other day writing a post like this, my old Reserve Bank colleague – now a consultant – Geof Mortlock sent me a copy of an open letter he had sent to the Board chair, Neil Quigley, copied to the Governor, the (acting) Secretary to the Treasury, and to Grant Robertson, Paul Goldsmith, James Shaw, and David Seymour (but not to the other Associate Ministers of Finance, Shane Jones, David Clark and David Parker). In his letter, Geof outlines a series of questions/issues he believes the Board should be addressing in this year’s Annual Report. I’m reproducing it here.

Mr Neil QuigleyChairmanBoard of the RBNZDear Neil,Further to my previous emails, I have given thought to the types of questions I would be addressing if I were a director on the RBNZ Board. Given that one of the Board’s main roles is to assess the performance of the Governor and the RBNZ across all of its functions, I would expect the Board, in its forthcoming annual report, to address a number of key matters that call into question the adequacy of the RBNZ’s performance in the last year.Previous Board reports have been fairly light in content and uncritical of the RBNZ’s and Governor’s performance. This has been a contuining weak point in the RBNZ governance arrangements. I am hoping that this year’s report will be much more substantial and probing, given the rather troubling performance issues that have arisen in the past year (and indeed in prior years, for that matter). If the Board is to have value in the RBNZ governance process, it needs to demonstrate in its report that it has asked probing questions and held RBNZ senior management to account. It also needs to identify, in its report, the matters on which it has given advice to the Governor. In addition, I would expect to see in its report a summary of the extent to which the Board has sought the views of external parties to provide it with supplemental information with which to assess the RBNZ’s performance and that of the Governor. This is important, given the need to avoid excessive dependency on the views of RBNZ management and staff in performing the Board’s assessment function.In this context, I thought it might be useful to set out the types of questions I would expect the Board to enquire into and to report on in its annual report. These are set out below. I would be happy to elaborate on any of these matters if that would be helpful.Questions the Board should be asking and forming a view onBelow is a list of the main questions I believe the Board needs to ask and form a publicly reported view on.Monetary policy– Given that the inflation rate (on a range of measures) has been consistently below the mid point in the target range, why has the RBNZ not lowered the OCR to a greater degree and earlier than it has? Is the Board satisfied on the analytical processes undertake and judgements made by the RBNZ in this regard?– Is the Board satisfied with the degree of transparency that has been revealed to date in statements made by the new Monetary Policy Committee, particularly as regards the possible divergence pr differences of views on the Committee and the capacity for individual members of the Committee to have their respective views publicly revealed so as to enhance transparency and accountability.– Is the Board satisfied that the Monetary Policy Committee is operating on the basis of a free and frank exchange of view and not hindered by undue dominance from the Governor? Has the Board spoken one-on-one with members of the committee in this regard?– Is the Board satisfied that the RBNZ is giving sufficient attention to how it would seek to respond to a significant economic recession, having regard to the fact that the OCR is already very low and, in all likelihood, may be further reduced in coming months, and hence there is reduced scope to use the OCR to combat recessionary forces? Is it satisfied that the RBNZ is putting in place a robust contingency plan for addressing the risks of a recession in a very low interest rate environment, and if so, on what basis has the Board reached that view?Prudential policy– What enquiries has the Board made as to why the RBNZ did not discover the ANZ capital model breach at a much earlier stage than actually occurred?– Is it satisfied that the RBNZ has the systems, staff and policy framework required to enable it to reliably detect non-compliance by banks and insurers, and to detect emerging financial stress?– Is the Board satisfied that the RBNZ was sufficiently proactive in evaluating the adequacy of the bank director attestation issues that arose in ANZ (and might exist in the case of other regulated entities)?– What enquiries has the Board made with RBNZ senior management and external parties as to the adequacy of the RBNZ’s approach to banking and insurance supervision, having regard to the fact that the IMF assessed the RBNZ as being non-compliant with around 50% of the Basel Core Principles (i.e. the international standards on banking supervision), and that a similar failure applies in the case of insurance supervision?– Why does there appear to have been no significant actions taken by the RBNZ to make the necessary changes to its approach to banking and insurance supervision to bring it into alignment with international principles and best practice? What has the Board done about this lack of action?– Is the Board satisfied with the adequacy of the RBNZ’s consultation processes on prudential policy issues, having regard to the serious concerns raised by many parties about the lack of meaningful consultation, the lack of transparency in RBNZ responses to issues raised in submissions, the failure of the RBNZ to adequately take into account many of the legitimate criticisms made of its policies and processes, and the lack of robust cost/benefit analysis? What is the Board doing to address these concerns – eg raising the issues in question with the Governor and Minister?– In the case of the bank capital proposals, what enquiries has the Board made of parties outside the RBNZ to satisfy itself as to whether the capital proposals were well thought-through, thoroughly costed, and subject to rigorous external scrutiny (before they were released)? Is the Board concerned at the level of criticism being made of the Governor and the RBNZ in respect of the bank capital proposals, and if not, why not?– Is the Board satisfied that the RBNZ has done sufficiently robust analysis of the issues in question to justify the extremely large increase in capital ratios being proposed, including in respect of assessing the existing probability of bank default, the level of economic contraction needed to trigger bank default (based on reverse stress testing), whether alternative approaches (such as bail-in debt, as being proposed by many other jurisdictions) would be a more cost-effective approach), and the assessment of the economic impacts of the proposals? Has the Board made enquiries with external parties on these matters or merely relied on information and views provided to it by the RBNZ’s senior management?– Is the Board satisfied with the Governor’s handling of criticism made of him and the RBNZ with respect to the bank capital proposals, including as to whether the credibility of the RBNZ is being damaged by the way the RBNZ has been responding to criticism?– What performance metrics does the Board apply in assessing the RBNZ’s performance of its prudential regulatory and supervisory responsibilities? How does it reach a view as to whether the RBNZ is performing satisfactorily or unsatisfactorily? And, using whatever criteria the Board does use, what is its assessment? (The same question on performance metrics applies across all of the RBNZ’s functions.)– What analysis has the Board undertaken in relation to the RBNZ’s approach to bank recovery and resolution issues? Is it concerned that the RBNZ is one of the few prudential supervisory authorities in the OECD that has not yet introduced recovery planning requirements for banks? Is it concerned that the RBNZ has not undertaken any resolvability assessments or resolution planning of the major banks, other than for the limited (and, frankly, very odd) purpose of facilitating the separation of the subsidiaries from the parent banks?– Is the Board concerned that the RBNZ’s OBR policy is widely regarded as being unworkable in a systemic crisis and likely to cause financial instability if ever a government was daft enough to implement it? Does the Board make enquiries as to why the RBNZ has not pursued resolution policies that entail a joint trans-Tasman resolution that seeks to minimise costs for NZ taxpayers by keeping the group intact, as opposed to making a presumption of separation of the NZ subsidiary from the parent bank?– Is the Board concerned that, in many key respects, the RBNZ has failed to implement policies that would bring it into alignment with international best principles and practice with respect to banking supervision, insurance supervision and bank resolution (as the IMF has pointed out)?– In all of these matters, to what extent has the Board engaged in an in-depth manner with external parties to enable it to be in a stronger position to assess the performance of the RBNZ?Communications– Is the Board satisfied with the quality and frequency of public communications made by the RBNZ in respect of all of its functions?– How does the Board respond to criticisms made that the Governor has not given any serious, in-depth speeches on monetary policy, prudential policy, financial stability or other matters relating to the RBNZ’s functions since he assumed office?– What analysis does the Board undertake to compare the RBNZ’s quality of public communications with that of other central banks, such as the RBA, Bank of England, Bank of Canada, etc?These are just a small selection of questions I would be asking if I were a director on the RBNZ Board. I do hope that the Board’s annual report sheds light on the Board’s enquiries into these matters and provides a robust set of views as to what its assessment of performance is and the reasons for reaching those views.Regards

(And lest anyone think we hunt as a pack, Geof and I disagree quite vigorously on various aspects of the Bank – including the nature, role of, and reasonable expectations from, prudential supervision, and regular readers of comments section here will have found various fairly strongly-worded criticisms of me and my views of various other issues.)

They are good questions and I’d echo many or most of them (although it isn’t the role of the Board to impose their judgement over that of the Governor’s on specific policy issues). I’d add some around the Maori strategy, the tree god nonsense, and the prioritisation of resources when the Bank tells us it is resource-starved. I’d want to ask about the performance of the Deputy Governor (recall that they are supposed to report on his performance) as the key line manager responsible for prudential policy initiatives (notably, the bank capital proposals), and around the approach taken by the Board itself in selecting MPC members (eg, whether the Governor was too heavily involved in a committee that should act partly as a check on him, and whether suitable classes of able, expert, and available people were excluded from consideration from the start.). I’d also be posing question about the adherence of the Bank to the letter and spirit of the Official Information Act and – more pointedly still – about the Reserve Bank Board’s own adherence to the requirements of the Official Information Act and the Public Records Act (on the OIA, see this recent post for their cavalier disregard for the law). Oh, and perhaps about their handling of the serious culture, conduct, and compliance concerns in the Bank’s superannuation scheme, where the Board appoints half the trustees, including the chair (each of whom serve solely at the pleasure of the Board).

The second terms on the Board of both the chair and deputy chair expire early next year and it is customary for Board members to serve only two terms. This is the opportunity for them, leading the Board, to show us – before the law is changed – what might have been, and to model at last serious monitoring and accountability. It isn’t as if there are not pressing issues on which they should be explaining to us how they have held the Governor and Deputy Governor to account. The shockingly poor process and seriously weak substance, all overlaid with populist spin. in the bank capital proposals should be central to that.