It was pleasant to walk along Wellington’s waterfront this morning to hear the Governor of the Reserve Bank speaking at a local function centre. Given the numbers who turned up – many of them Bank staff – they could probably have saved a few dollars by holding the event on their own premises, but, I guess, it is other people’s money.

As the Governor explicitly noted that he would “look forward to the blogs”, I should probably do my bit.

A week ago when this event was announced, I devoted a whole (short) post to the announcement of the event, including the indication that they would be filming the speech and making that footage available on the web. Doing so is a genuine step forward and I hope it becomes standard practice.

In that earlier post I noted

I have been critical of the Reserve Bank Governor for not yet having given an on-the-record speech about either of his main functions, monetary policy or financial regulation/supervision. Next week marks a year since he took up the job

Unfortunately a year has now passed and we still haven’t had a substantive on-the-record speech about either of his main functions – the sort of speech that would be standard, and quite expected, under any other Governor and in any other country.

Today’s speech was billed this way

Reserve Bank Governor Adrian Orr will talk about the future of New Zealand’s monetary policy framework …..The revised monetary policy framework comes into effect on 1 April 2019. It is an outcome of the recent Phase 1 review of the Reserve Bank Act. Adrian Orr will talk about changes to how monetary policy decisions are made in New Zealand, including greater transparency and accountability.

But there wasn’t very much about the new monetary policy framework (any aspect of it) at all. You can read the text for yourself (and on this occasion the speech delivered was recognisably similar to the published text, which is not always the case I gather).

The whole event started rather oddly, with a fairly lengthy greeting in Maori from someone whose name I didn’t catch but who had no apparent connection to the Reserve Bank. Only a small portion of whatever he said was translated, so I suspect very few attendees had any idea what he’d been saying. He did, however, take the opportunity to make a few digs in English about the Foreshore and Seabed Act – of infamous memory – including at a former Labour MP from that era who was apparently in the room. That seemed rather inappropriate in a Reserve Bank function. Not even the Governor has yet claimed Reserve Bank responsibility for the foreshore and seabed.

The Governor did, however, tell us that someone else in the room had just agreed to be a “kaumatua” to the Reserve Bank – a title apparently quite in vogue in trendy government agencies, but not having an obvious place in way Parliament set up the governance of the Reserve Bank. Isn’t all that stuff – leadership, nurturing talent, resolving disputes – among the functions of those tedious prosaic statutory roles such as Governor, Deputy Governor, and Board members? But there is, we are told, a forthcoming Bulletin article, “RBNZ’s Strategic Approach to Te Ao Maori”. That will be something to look forward to, no doubt involving more expensive and tortured efforts to explain why a macro-focused government agency, which deals with general public hardly at all, needs such a strategy and not (say) a Catholic one, a secular humanist one, a Pacific one, or an NZRFU one? For an organisation that claims to be underfunded, they certainly seem to take every opportunity to spend resources on stuff other than their core business.

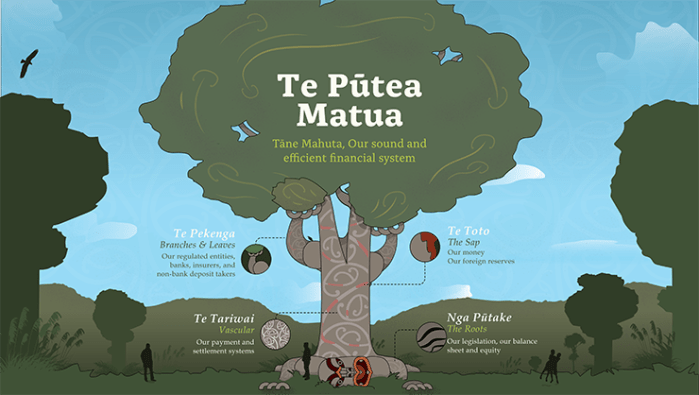

The Governor keeps on doubling down with his tree god nonsense, urging us to think of the Bank as akin to Tane Mahuta, the mythological forest god. He delivered his speech flanked by two screens of this cartoonish graphic.

He claimed this myth – which has precisely nothing to do with central banking – “is” (not “was”) “central to the Maori belief system”. Those who bothered by such things might suggest it was “cultural appropriation” – although, ever deferential, he did stress that he asked permission to use the myth – but as I’ve noted in an earlier post

Pre-evangelisation, Maori had their own tree god, Tane Mahuta. As far as I can tell, not many believe any longer in this local tree god: when I looked up the 2013 Census data, there were lots of Maori recording no religion, and there were plenty of Catholics and Anglicans. But there wasn’t a category shown for tree gods, or any of the other deities (Wikipedia has a list of at least 35 of them).

As a recent commenter on another post noted

Imagine the reaction if the Bundesbank president started discussing policy in terms of Odin and Thor…. he’d get locked up…

And in addition to those references, we got the same warmed-over inaccurate nonsense the Governor has run repeatedly about the creation of the Reserve Bank ‘letting the sunshine in” on the New Zealand economy and financial system. I happen to agree that the creation of the Reserve Bank was, on balance, a good thing, but you’d not know from listening to the Governor that we’d had a stable financial system and a highly prosperous and productive economy without one.

What the speech really tended to show was a Governor with not much interest in the core business of the Bank (price stability, financial regulation, notes and coins, and a few ancillary bits and pieces). Each of those functions matter. It is important they are done well. When they are done well, most people should have little interest in the Reserve Bank.

But, so he told us, the Governor is bothered that when they went out to “the community” (no polling results or the like, but I’ll take his word for it), people said they had significant trust in the Bank, but didn’t really know what it did. But then they don’t really need to, any more than (say) I need know anything much about many of the dozens of government organisations you can find listed here (and I’m a geeky policy person, and still have no idea what, say, the Accreditation Council does). How much does the person in the street know about, say, the organisation of our judiciary, or the distinction between the New Zealand Defence Force and the Ministry of Defence. I’d struggle to even tell you what the Ministry of Housing and Urban Development does.

But it isn’t good enough for the Governor. So, on the one hand, we get cartoon versions of Monetary Policy Statements and Financial Stability Reports. And on the other, considerably more worryingly, we get attempts by an overtly left-wing Governor to tie himself and the institution he leads to a whole series of trendy left-wing causes. I’m sure he is not directly partisanly political, but his colours are firmly staked to an ideological mast, in ways that are potentially quite damaging. After all, if he wants citizens to have confidence in his organisation around its core functions, those who aren’t sympathetic to his overt left-wing agenda will be less inclined to trust him even on the core issues he has responsibility for. A new centre-right government at some point (ok, just kidding, but at least a new National one) might also be less inclined to trust him. And, in championing these causes, he creates unrealistic expectations about what central banks can actually do, and opens the Bank up to pressure in future to join in promoting some other government’s set of ideological causes.

As an example of what I mean, here is an extract from the speech.

In the world today, the dynamics of global and national economies are interacting to a greater extent and, at times, working at cross-purposes. Underlying these interactions are social and political movements driven by a desire for greater well-being, both for current and future generations.

More recently we have been confronted with the issue of climate change, and its complex and powerful economic and financial impact.

We have barely scratched the surface in understanding the intergenerational impacts of these developments.

This desire for well-being is regularly reflected in discontent along the lines of economic, gender, racial, and intergenerational inequities – to name just a few. Therefore, ensuring social inclusion as a way forward in capitalist societies is necessary.

The first of those paragraphs barely even makes sense. The rest do, but none of it has anything to do with central banks doing their jobs. If this text appeared in a speech from Grant Robertson or James Shaw it might be quite unexceptionable – it is the sort of stuff left-wing politicians say – but what is a (supposedly neutral non-partisan) Governor doing spouting off about his views as to how “capitalist societies” should move forward. Since it is what he is paid for, I’d rather hear him on the New Zealand cyclical economic situation, financial stability risks, positioning monetary policy for the next serious downturn or whatever. Intrinsically less interesting perhaps, but that is the job he and his institution are paid to do.

The Governor – particularly in his oral delivery – was claiming a much wider mandate for himself from the newly amended Reserve Bank Act. He is wrong to do so.

Even the badly-worded new Remit (replacement for the Policy Targets Agreement) makes that clear

Whatever good monetary policy does – and it is only the monetary policy bits of the Act that are changed – it is “by” doing the same old stuff: leaning against cyclical fluctuations and maintaining medium-term price stability.

Here is the purpose statement from the amended Act

Yes, the current government’s waffly rhetoric about “wellbeing: and a “sustainable and productive economy” is enacted, but even this legislation is clear that – whatever else the rest of government does (or doesn’t) do, the Reserve Bank makes its contribution by doing (well) the same old basics: monetary policy, a focus on a sound and efficient financial system, and notes and coins.

Inclusion – gender, racial, religious, ideological, socioeconomic or whatever – just isn’t the Reserve Bank’s territory. Neither is climate change or other “social or political movements”. Some of those issues may be quite important. Most are very interesting. But if the Governor wants to pursue them perhaps he could create a blog in spare time (I wouldn’t recommend it), stand for Parliament, or put in a belated application to be the new Secretary to the Treasury. All that other stuff will either distract the Reserve Bank’s attention (and perhaps suggest it already has too many resources), and/or skew support for the Reserve Bank along ideological lines in ways that are quite unhelpful in the longer-term (the Governor talked often of “legitimacy” and that dubious left-wing concept “social licence”). The Governor talked of “our need to be a good global citizen”, but actually the New Zealand Parliament set up the Bank, and resourced it, to be a quite limited New Zealand government agency.

I could go on, but will bring this towards an end. Three final points:

The Governor did mention briefly his proposals to substantially increase bank capital requirements. Nothing much of the substance, but he claimed that the Bank is open-minded and urged people to get their submissions in. That is well and good, but it might be helpful to potential submitters – including those not from the banks, who the Governor claimed to be keen to hear from – if the Bank actually released the supporting material – for example, the Analytical Note on aspects of the economic impact that the Deputy Governor promised in his speech now more than a month ago, or the supporting information for ad hoc claims the Governor made on this issue at his MPS press conference more than six weeks ago. It is more than three months since the proposal was released, and process is looking increasingly shoddy, as if they hope to run out the clock rather than provide substantive evidence for their proposals. (Incidentally, in his delivered speech – but not in the published text – the Governor claimed that “we know” that significant bank failures cause significant damage for “all future generations”. Perhaps that is another claim he might like to substantiate. But it is probably just another one from off the top of his head.)

As I noted at the start, a former Labour MP was present. That former MP was Tim Barnett who now leads what looks like a worthy organisation called FinCap which is

a new entity driven by the public good, acting in the interests of New Zealanders seeking budgeting and financial capability advice.

Sounds worthy. The Governor seemed keen on it, and said that the Reserve Bank would be endorsing this organisation in public. Thus far, probably fine. What was much less acceptable was to hear the Governor of the Reserve Bank say that he would be “coercing banks” to support it. One hopes he wasn’t entirely serious, but when a regulator already wields a great deal of power on a wide range of fronts, they have to bend over backwards to avoid even suggesting any pressure (let alone ‘coercing’) on regulated entities to do things the regulator personally might like, but for which he or she has no statutory mandate.

Finally, the Governor ends the speech talking of how he and the Bank are going to “maximise their mandate”. I suspect he has in mind actually doing as much as possible to fulfil the mandate he has been given by Parliament, but it does sound awfully like a bureaucrat looking to expand – to the maximum- the role and scope of his bureau. That isn’t what we need. We need a pretty boring organisation getting on and doing the (important, but quite limited) basics well. At present, they are some very considerable margin away from the goal he articulates of being the “world’s best central bank” – and nothing in this speech, or the others the Governor has given (and his term is now one-fifth over already) suggests they are making any progress towards it. If anything – and as evidenced in this speech – they are drifting further away.

But they turned on a good sausage roll, it was a good chance to catch up with a few people I hadn’t seen for a while…..and it really was a nice morning for a walk.

Just a shame about the central bank that was on display.