In the wake of the Reserve Bank’s Monetary Policy Statement in February I wrote

As for the overall tone of the monetary policy conclusions to the statement, count me sceptical. …for the Governor to suggest that the risks now are really even balanced, even at some relatively near-term horizon, seems to suggest he is falling into the same trap that beguiled the Bank for much of the last decade; the belief that somewhere, just around the corner, inflation pressures are finally going to build sufficiently that they will need to raise the OCR. We’ve come through a cyclical recovery, the reconstruction after a series of highly-destructive earthquakes, strong terms of trade, and a huge unexpected population surge, and none of it has been enough to really support higher interest rates. The OCR now is lower than it was at the end of the last recession, and still core inflation struggles to get anywhere 2 per cent. There is no lift in imported inflation, no significant new surges in domestic demand in view, and as the Bank notes business investment is pretty subdued. Instead actual GDP growth has been easing, population growth is easing, employment growth is easing, confidence is pretty subdued, the heat in the housing market (for now at least) is easing. Oh, and several of the major components of the world economy – China and the euro-area – are weakening, and the Australian economy (important to New Zealand through a host of channels) also appears to be easing, centred in one of the most cyclically-variable parts of the economy, construction. …

From a starting point with inflation still below target midpoint after all these years, it would seem much more reasonable to suppose that if there is an OCR adjustment in the next year or so, it is (much) more likely to be a cut than an increase.

The Governor appears now to have come round to that view. If his re-think is overdue, it is welcome nonetheless.

I don’t take issue with much about his statement. but two lines did catch my eye. The first was this one (emphasis added)

This weaker [global] outlook has prompted central banks to ease their expected monetary policy stances, placing upward pressure on the New Zealand dollar.

Perhaps that is correct – although in the data the effect looks small – but it is quite a dangerous line to walk down. Either an easier stance of policy was warranted here on the New Zealand fundamemtals (including our exposure to the world economy) or it wasn’t (it was). The exchange rate should be largely irrelevant to that choice, and reintroducing it like this risks some sort of MCI mentality taking hold. He’ll remember those bad old days.

And the second, of course, was this claim

As capacity pressures build, consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

To which one can really only say two things, a) yeah right, and b) isn’t this the same story the Bank has been telling for almost the entire decade? Of course, as the former chief economist used to point out, in one sense they had to believe it – if it wasn’t something they could say hand on heart then they should have adjusted policy already. But if they really believe capacity pressures are going to intensify from here, they must now be in a pretty small minority.

Even though the data suggest that the Bank should have an easing bias in place (and perhaps should already have had a lower OCR in place), I was a little surprised that having walked past the opportunity in February, the Governor chose to act now. After all, this is the last OCR decision that he will take as the Bank’s sole decisionmaker on monetary policy. On Monday, the new statutory Monetary Policy Committee will take over responsibility. Even though I’ve been consistently running the line that the Governor will, in effect, control all the appointments to the MPC and will effectively control the overall votes, I’d assumed he’d want to observe the proprieties and at least pretend that the new voters might make a difference – might see things differently from him.

On paper, the Governor’s statement that

the more likely direction of our next OCR move is down.

doesn’t mean much. I’m sure he made this decision with two of the likely new MPC members (Deputy Governor Bascand and the very new Assistant Governor Hawkesby), but the new MPC will have four other members, most probably the new (as yet unannounced) chief economist, and three externals. Most likely the externals (in particular) won’t want to rock the boat – they’ll have been selected partly for that quality – but they might quite reasonably see the data differently than the Governor. That could get a little awkward. Perhaps the Governor ran risks whichever tack he took, but he could easily have explicitly noted the regime change and could then have eschewed any sort of bias statement (leaving the rest of the statement pretty much as it was).

(Presumably the Minister of Finance will finally announce the MPC members today or Friday. When he does, I would be delighted to revise my view that they’ll have been selected for their inoffensiveness, if such a revision is warranted. But I’m not holding my breath.)

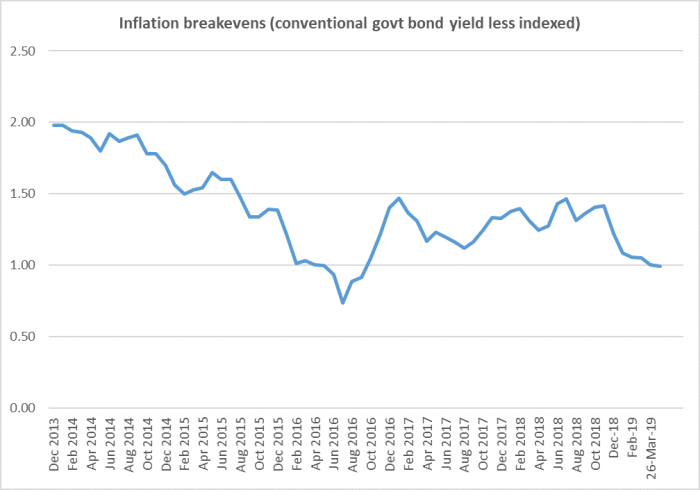

And what of inflation? As readers will know I have been tantalised by the implied inflation expectations derived from the indexed and nominal government bond markets. Here is the latest update of that chart, the last observation being yesterday’s.

Implied inflation expectations (for the average over the next 10 years) – implied by people with money at stake, or the opportunity to stake it to clear out anomalies – have been nowhere near target for almost five years now. In the last few months they have been dropping away again and now are barely 1 per cent. The Reserve Bank never references this series, but they really should, even if only to make the case for why they think there is no meaningful information in it.

Perhaps you are thinking this is just a global phenomenon. After all, nominal bond yields have been falling pretty much everywhere. But here are the 10 year inflation breakevens for the US

Not only have the breakevens rebounded (risen) in recent weeks, but they remain near the Fed’s target inflation rate (also 2 per cent).

With core inflation still below target after all these years, market-based expectations measures low and weakening, with increasing unease about the world economy (including the economies of our two largest trading partners), with most of forces that impelled the (productivity-less) growth in recent years having exhausted themselves, and with weak business survey measures, the case for a lower OCR already looks pretty strong.

What, realistically, would be the worst that could happen if the Bank had cut and the cut turned out to be unnecessary? Unemployment would be a bit lower, even if temporarily, and core inflation might rise to the height of, say, 2,2 or even 2.4 per cent. Perhaps not desirable outcomes in their own right – the focus is supposed to be 2 per cent — but after all these years undershooting the target hardly likely to destabilise public or market confidence in the Bank’s conduct of monetary policy and delivery of medium-term price stability.

UPDATE: The Minister of Finance has announced the appointments to the MPC this morning. My initial reaction is that there is no need to revise my judgement about the structure and likely dynamics of the MPC. It is quite disconcerting that one (internal) member has been appointed for only a one year term, which will place that person even more than usually under the heavy influence of the Governor. The Minister would have been better to have started the committee with 3 internals and 2 externals and made the final external appointment when the new permanent Chief Economist is finally appointed.