Data from New Zealand’s inflation-indexed bond market has been a bit of a mystery for some time.

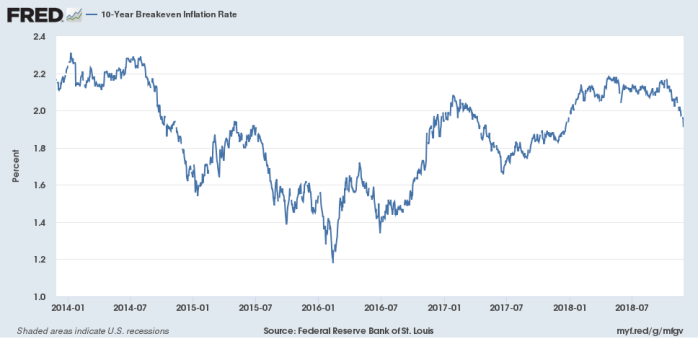

If one looks at US data, the gap between conventional and indexed government bond yields – the “breakeven” or implied inflation expectation – makes sense. Here is the data for the last five years or so.

The US inflation target is around 2 per cent and for the last couple of years the breakevens have been pretty close to that. There was a period of real weakness in 2015/16 but it didn’t last that long, and even then the breakevens were only averaging around 1.5 per cent. If you were inclined to focus on the severe limitations US monetary policy will face in the next serious recession, you might even think 2 per cent breakevens for the average of the next 10 years is a bit high – after all, the Fed has struggled to get inflation to average 2 per cent in the last decade – but that would be a non-consensus perspective, and I’ll leave it to one side for now.

The New Zealand indexed bond market was, for a long time, rather patchy to say the least. Indexed bonds were tried for a while in the 1980s, and then one more-modern-style long-term indexed bond was issued in the mid-late 1990s (about the time I and a colleague wrote this article). But The Treasury was never very keen, and there was a diminishing volume of public debt anyway. If there is any upside to the higher volume of public debt this decade (in general I’m not convinced) it is the advent of a range of government inflation-indexed bonds. There are four on issue now, with maturity dates out to 2040.

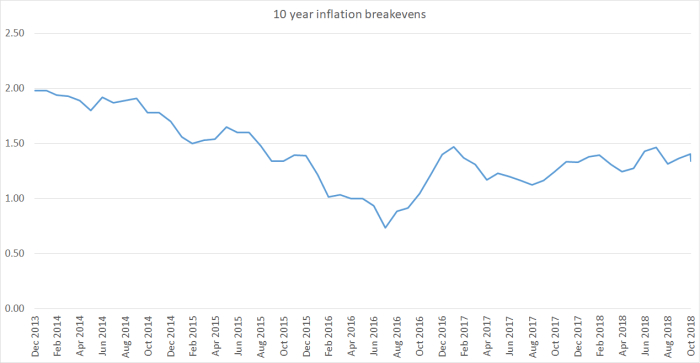

Unlike the situation in the US, no one makes readily available here constant-maturity data for either indexed or conventional bond yields. When the “10 year bond yield” is quoted here, it is rarely actually 10 years. But the Reserve Bank does publish a yield series for each of the indexed bonds. If one time-weights the (September) 2025 and 2030 indexed bond yields, one gets this approximation to a 10 year indexed yield since September 2015. (I’ve also show the yield for the 2025 bond from the end of 2013 to September 2016, when it was at least moderately close to 10 years).

The fall in long-term real interest rates is certainly striking – consistent with the fact that five years ago the Reserve Bank and most of the market thought short-term interest rates would be more like 4 or 5 per cent looking ahead. In fact, of course, the OCR has been 1.75 per cent for the last couple of years, and is currently expected to remain low pretty indefinitely.

And what if we then take the Reserve Bank’s “10 year bond yield” series for conventional bonds, and subtract the indicative indexed bond series in the previous chart?

This is the chart that parallels the US one at the start of the post. As you can see, the two charts (one daily, one monthly) look quite similar at the start. Breakevens here were also around 2 per cent, the target set for the Reserve Bank. But then they diverge – the short term cycles are similar, but the levels are very different. On this measure, it has been three years since the New Zealand breakeven rate got even to 1.5 per cent. As of yesterday’s data, the gap was 1.34 per cent.

Meanwhile, of course, at every opportunity the Reserve Bank assures us that inflation expectations – survey measures, which involve respondents staking no money, and rarely any reputation (since responses are published mostly in aggregated form) – are “securely anchored” at 2 per cent. And, rather than address the indicators from the indexed bond market, the Bank simply passes by in silence.

Over the years, there have been various stories put forward for why information from the indexed bond market should be discounted. For a long time, there was only one maturity, and there really wasn’t all that much of that bond on issue (just over $1 billion). Then there were stories about illiquidity – not much trading in indexed bonds and few or no price-makers. Glancing through the historical data for turnover in the Feb 2016 bond, there were lots of weeks when the outright trades totalled less than $5 million, and quite a few when there were no trades at all.

But these days there are four bonds on issue, totalling about $16 billion. Talking to a funds manager recently, I learned that another bank has just become a pricemaker in indexed bonds, such that there are now three local and three offshore institutions offering two-way prices in these instruments. And the Reserve Bank turnover data suggests that if these markets aren’t exactly awash with trade, there is now a respectable volume of secondary market turnover in at least the 2025 and 2030 maturities (and there isn’t much turnover in conventional bonds beyond 2030 either).

I queried the fund manager as to his view on why the New Zealand breakevens are so low. He argued that it wasn’t now a market liquidity issue (although you have to think that if you wanted to dump a $200 million position it would still be a great deal easier in the conventional market than the indexed market). His argument was the market was still new and that there limited interest still from the buy side, including the offshore market in particular. I was a bit surprised by that, as I recalled (long ago) when the indexed bonds were being issued in the 1990s that a lot of demand initially came from offshore (it surprised us at the time, and New Zealand inflation indexation seemed like something more naturally appealing to local pension funds than to offshore funds). But I looked up the data, and this is what I found.

| Per cent of bonds in market held by non-residents, Oct 2018 | |

| Conventional | |

| Apr-23 | 67.7 |

| Apr-25 | 52.2 |

| Apr-27 | 67.1 |

| Apr-29 | 75 |

| Apr-33 | 46 |

| Indexed | |

| Sep-25 | 50.7 |

| Sep-30 | 37.6 |

| Sep-35 | 21.3 |

And, sure enough, a materially smaller proportion of the indexed bonds is owned offshore than of the conventional bonds. The offshore proportion isn’t trivial by any means, but it is smaller (and, if anything, looks to have been shrinking a bit over the last few years).

I don’t have a good story for why that might be. After all, New Zealand indexed bonds offer some of the highest yields in the advanced world (our longest maturity yields 50 basis points more than the US 20 year indexed bond, and the US is now a high yielding advanced economy), and much of the story of the last few years has been of a search for yield. Search for yields often involves sacrificing liquidity. And (critical as I am of New Zealand economic performance) the creditworthiness of our bonds, indexed and nominal, looks better than ever in relative terms, as being among the handful of advanced countries with budget surpluses and low debt.

I did hear a story a while ago suggesting that the government has simply glutted the market by issuing too many inflation indexed bonds too quickly. At one level it is an argument that looks a bit hard to refute (the resulting yields are high relative to equivalent maturity and credit risk conventional bonds), but standing back a bit I’m not sure how persuasive a story it is. The world markets are big, New Zealand is small (and fairly sound), and the appetite for yield has been strong.

Which is partly why I don’t think it is safe for the Reserve Bank to simply ignore that New Zealand inflation breakevens. They may well be telling us something about medium-term expectations of inflation (implicit expectations as much as explicit ones). After all, core inflation this decade has averaged around 1.5 per cent, the Bank has (twice) proved too quick to tighten, and if inflation has picked up a little recently, it would be reasonable to think that there will be a downturn along again before too long.

Perhaps there is a more compelling story that “exonerates” the Reserve Bank. But it would be good to see them make it, and to be able to test the quality of their analysis and research. Simply ignoring a pattern that has now persisted for three years – breakevens averaging less than 1.5 per cent when the inflation target as 2 per cent – seems not particularly responsible, not particularly transparent, not particularly accountable.

I would bet that the market is right and the inflation expectations surveys are wrong. A point ably made by “market” monetarists such as Scott Sumner.

LikeLike

That is my inclination too, It would be consistent with the fact that, on their own NAIRU/output gap estimates, they need to overheat the economy to get core inflation averaging around 2 per cent

LikeLike

With trade war and the US shutting down their borders, the world would be struggling with excess inventory and production capacity. Inflation is pointed down. Even the banks have repriced residential loan interest rates below 4%.

LikeLike

Reblogged this on Utopia – you are standing in it!.

LikeLike