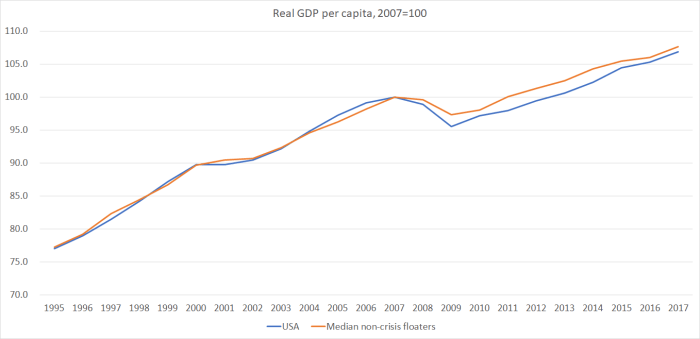

In my post yesterday, focused specifically on Geoff Bascand’s speech on financial stabilty, financial crises etc, I used this chart

to, again, raise questions about just how much of the poor economic performance over the last decade or so can really be ascribed specifically to the financial crisis (bank failures, large loan losses etc). After all, the US was the epicentre of the crisis, and my other group of countries (long-established advanced countries, also with floating exchange rates – Australia, Canada, New Zealand, Norway, Israel, and Japan) didn’t have domestic financial crises.

I’d been playing around with that data with a view to writing a post about an article in the latest issue of Foreign Affairs, “The Crisis Next Time: What We Should Have Learned from 2008″, by Carmen and Vincent Reinhart (she an academic researcher, and he a senior market economist and formerly a senior Fed official). The Foreign Affairs website is having open access this month, so the link should work for anyone wanting to read the (accessible and not overly long) article itself.

I thought the article was a bit of a mixed bag (and this post ends up only partly being about the article). Carmen Reinhart, in particular, has been at the forefront of efforts to remind that recessions associated with financial crises are often more severe than other recessions. That is a useful reminder, but hardly surprising. Mild recessions tend not to generate many loan losses, and even if the banking system wasn’t rock solid in the first place, nothing too serious is likely to follow. But if resources have been severely misallocated in the first place, supported by ample new credit, then when the correction occurs – and views about what is profitable have to be revised – it isn’t surprising that the associated recession can be deep and the financial system can come under stress. In New Zealand, for example, it wasn’t the financial system crisis (failure of DFC, repeated near-failures of the BNZ) that made the 1991 recession so serious; rather than pressures on the financial system were part of the same aftermath of excess – over-inflated expectations – that the entire economy was caught up in, combined with some serious efforts to break the back of high trend rates of inflation.

As the Reinharts point out, the problems can then be particularly severe in a country that has few or no macro policy levers left open too it – a fixed exchange rate or a common currency, tied to the fortunes of a group that may not share the particular problems you did (thus, for example, Ireland in a euro-area in which Germany is the largest economy). Adjustment can be a lot slower without the ability to adjust the nominal interest and exchange rates. Perhaps more than the authors, I’m a sceptic on the euro.

For my purposes, there is a convenient couple of sentences in the Reinhart article

Financial crises do so much economic damage for a simple reason: they destroy a lot of wealth very fast. Typically, crises start when the value of one kind of asset begins to fall and pulls others down with it. The original asset can be almost anything, as long as it plays a large role in the wider economy: tulips in seventeenth-century Holland, stocks in New York in 1929, land in Tokyo in 1989, houses in the United States in 2007.

It usefully highlights a key difference between, say, the US (or Ireland or Iceland) late last decade, and the experiences of the group of non-crisis floating exchange rate countries whose experience is reflected in that first chart above. Stock markets in those latter countries took a short-term hit, of course, but there was no sustained loss of (perceived) wealth akin to what happened in the crisis countries.

It isn’t entirely clear from the article how much the authors want to focus mostly on the depth of the initial recession and how much on the disappointing economic outcomes in many countries over the last decade. But both are mentioned, and there seems to be a tone that conflates the two in a way that I’m not surely is overly helpful (given the goal of learning lessons that can help better prepare us for future severe adverse events). There also seems to be a very strong focus on the demand side, and none at all on the supply side (no mention at all of productivity growth).

And yet, if we look across the OECD as a whole, the unemployment rate was right back down to where it had been in 2007. If (and there is) a disappointment about the last decade as a whole, it can’t be now about excess labour supply (unemployed workers) – slow as the unemployment rate was to come down, it did eventually. As it happens, the unemployment rate in the US (epicentre of the crisis) is now lower than in the median of my non-crisis floating exchange rate group – which wasn’t the case in the years running up to 2008.

I have plenty of criticisms for the way many central banks (including our own) handled the years after the 2008/09 crisis and recession. In some cases, actually tightening when it wasn’t necessary or appropriate, and often a hankering for some sort of return to “normal” interest rates (that may have prevailed in the previous couple of decades) when as has become increasingly apparent something about what is “normal” has changed. Throw in the lack of any pro-activity in addressing the existence of the near-zero lower bound on nominal interest rates (itself arising from regulatory and legislative choices), and it is clear that more could – and should – have been done in many countries.

But even if such changes (in macro policy) had been made, the differences in economic outcomes would probably have been at the margin: helpful (eg in a New Zealand context, getting core inflation back to 2 per cent, and getting unemployment down to the NAIRU perhaps two or three years earlier), but it is unlikely that it would have made much difference to productivity growth, or indeed to levels of real GDP per capita today.

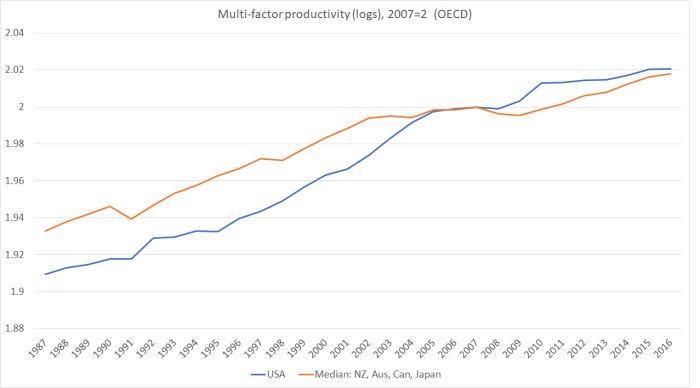

In yesterday’s post, I showed a chart comparing labour productivity growth trends in the US (epicentre of the financial crisis) and in the group of non-crisis floating exchange rate advanced economies. But what about multi-factor productivity?

The OECD only has MFP data for a subset of member countries. Of my sample of non-crisis advanced countries, they don’t have data for Norway and Israel. But here is the comparison for the US and the group of four non-crisis advanced countries, all normalised to 2007.

In both cases – although perhaps more starkly so for the non-crisis countries – it is clear that the slowdown in productivity growth was underway well before the recession (and crisis). The financial crisis (centred in the US) cannot be to blame for something that is (a) apparent across crisis and non-crisis countries (especially when the non-crisis countries are less productive than the US to start with), and (b) when the phenomenon got underway before the crisis or recession did.

(The Conference Board Total Economy database does have MFP estimates for my full group of non-crisis countries. They use a different model to estimate MFP, but the same two key observations hold in their data: the slowdown was apparent in both lots of countries well before the crisis/recession, and (if anything) the US has done better than the non-crisis group both before and since its crisis.)

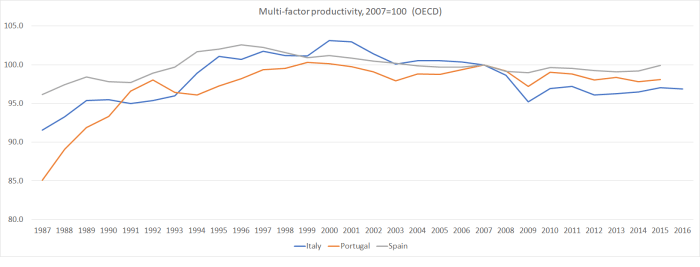

But what about some of the euro-area countries you ask? And the Reinharts themselves rightly point out how poor the economic performance of Italy (and Greece) has been. The OECD doesn’t have MFP estimates for Greece, but here are the estimates for three other embattled euro-area countries: Portugal, Spain, and Italy.

All three countries have been in deep trouble for a long time now – the estimated level of MFP peaking around 2000. On this score, the trends don’t look materially different over the last decade than over the years leading up to 2007. Whatever the cause of their problems with productivity, it can’t have been the financial crises these countries went through.

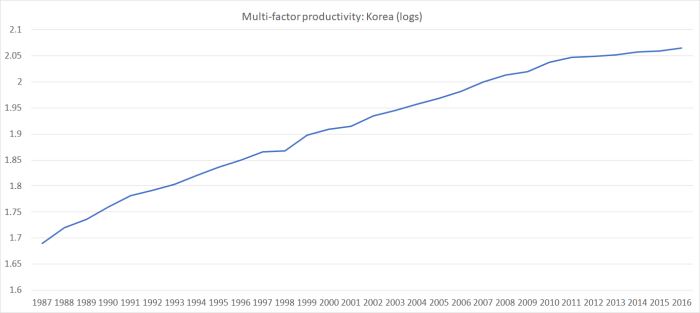

And perhaps nor would you expect it. Readers might recall a wrenching financial crisis that Korea went through in 1998. And here is the OECD estimate of multi-factor productivity for Korea.

You can see the 1998 crisis/recession in the data, but as a short-term blip. In the decade after the crisis, Korea productivity growth kept on at much the same rate experienced in the decade prior to that crisis – before (presumably) joining in the global slowdown this decade. (That had also been the experience of the United States in earlier crisis episodes – estimates suggest that the 1930s, for all its problems (around demand shortfalls) was a period of strong MFP growth.)

There is lots to learn from the searing experience of crisis, recession, and slow growth in the advanced world over the last decade or more. But I still reckon there needs to be a much more careful unpicking of the different strands of the story than central bankers – who tend to see the world through money and finance lenses, and who are often keen to champion their future role – are prone to. To me, the cross-country evidence just doesn’t square with a hypothesis in which the financial crisis itself plays any large part in the sustained disappointing performance of so many countries over what is now such a long time.

Central bankers meanwhile might be better off rethinking the merits of arrangements like the euro, or of the continued passivity around the near-zero lower bound, both of which look as though they have the potential for causing very major problems the next time there is a serious economic downturn.