There has been some interesting material around recently on how many advanced economies (in particular) have undershot over the last decade or so the trends they appeared to be on previously. Paul Krugman had an interesting column a couple of weeks back, and then the IMF had a whole chapter in their latest World Economic Outlook on “The Global Economic Recovery 10 Years After The 2008 Financial Meltdown”. Martin Wolf summarised and illustrated some of that chapter in his FT column last week. Much of this work attempts to associate (causally) subsequent disappointing economic performance with the financial crises of 2008/09, something I’ve long been a little sceptical of. The IMF also highlights that countries that didn’t have a financial crisis have shared in the underperformance.

I might come back to the IMF material (in particular) later but reading it prompted me to check out some New Zealand data.

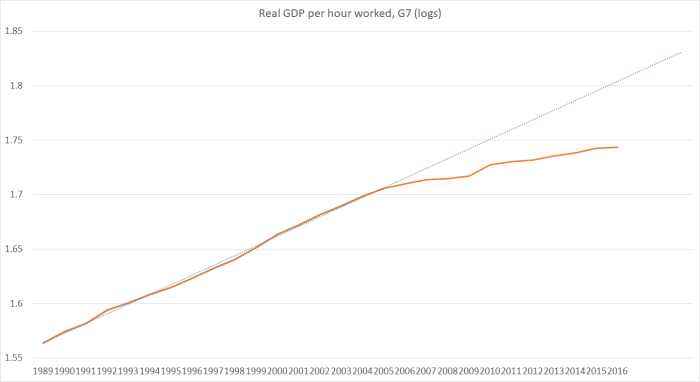

As context, here is some OECD data for labour productivity (real GDP per hour worked) for the G7 countries as a group.

The trendline shows what might have happened if the trend growth to 2005 had continued. The gap at the end of the period is equivalent to a productivity shortfall of around 15 per cent. Note that this productivity slowdown was clearly underway well before the financial crises.

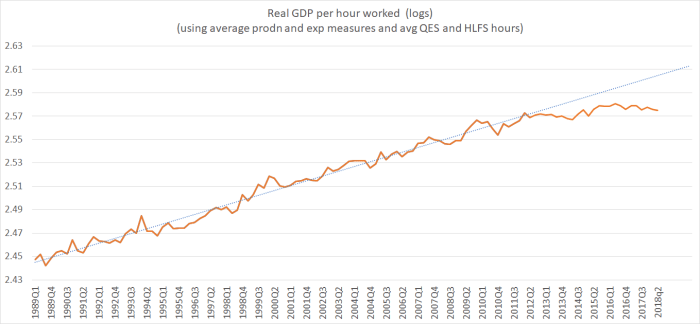

And here is the New Zealand data. Here I’ve used quarterly data, all the way up to 2018q2.

But this time the trendline extrapolates the trend in the actual data up to early 2012. Because up to about that time there was no particular sign of a change in the trend. (And thus between 2005 and 2012 we actually did a little better than the G7 as a whole).

Over the six years since 2012, the gap between the actual data and the trendline translates back to a shortfall of about 8 per cent. Real GDP per hour worked now would be around 8 per cent higher than it actually is – with all the attendant implications for wages, consumption possibilities, and even government revenue – if that pre-2012 trend had been sustained. And the pre-2012 trend had been pretty weak – mostly we’d still been falling behind the rest of the advanced world.

It is always possible that much of the recent productivity shortfall will be revised away – SNZ have, over the years, delivered some significant changes in history at times. But I’m not aware of any particular reason to expect significant revisions (in any particular direction), so we simply have to work with the data we have.

As the G7 countries didn’t have a financial crisis in 2005, we didn’t have one in 2012. In fact, we hadn’t had a systemic financial crisis at all since the late 1980s, and the localised (severe in the sector, but small economywide) finance companies crisis had been centred back in 2007 and 2008. For New Zealand, there simply isn’t a plausible story in which financial crises – domestic or foreign – can explain our dismal productivity performance over the last half decade or more. Neither the timing, nor the stylised facts around the New Zealand financial system, fit.

There are reasons why for countries at the productivity frontier a major financial crisis could impair domestic productivity growth even in a country that did not itself have a domestic financial crisis, but that isn’t a very relevant story here, New Zealand average productivity being so far below that in the leading group of countries (where productivity is about two-thirds higher than in New Zealand).

I’m not sure I have a fully compelling explanation for why New Zealand has done so poorly since around 2012 (my standard story encompasses several decades of persistent gradual – cumulatively stark – underperformance, and period since 2012 looks – on current data – to have been unusually bad). Perhaps the earthquakes, and the subsequent diversion of resources to a lot of vital, but low productivity, repair and reconstruction work is part of the story (as we knew from day one, in economic terms it was a nasty non-tradables shock that wasn’t going to be helpful). Then again, the peaks of that work are now well behind us, and productivity growth has yet shown signs of improving. Perhaps the strong terms of trade have been part of the story – not stimulating business investment, which has been persistently weak, but boosting incomes and perhaps crowding out other stuff. The real exchange rate – not an exogenous influence – got back to pre-recession levels from about mid-2011. And, of course, the very sharp and substantial turnaround in the net immigration numbers – also mostly not an exogenous development – was getting underway from later in 2012.

Whatever the full explanation, the symptoms (eg weak business investment, shrinking exports and imports as a share of GDP) should be worrying, the outcomes (productivity, and thus potential incomes) are dreadful – building on earlier decades of underperformance – and the explanation can’t credibly lie in financial crises, domestic or foreign.

And nothing serious is being done about addressing this failure, by the last government, by the present one. And The Treasury – principal adviser to the government on such matters – seems much more interesting in its Living Standards Framework and esoteric (and sometimes convenient) concepts of “wellbeing” than in actually advising on remedying the New Zealand productivity failure.

nnn

As you say, the local and international data suggests the lack of productivity growth has little to do with the global financial crisis. I think it is due to systemic and structural factors in mature Western economies including increased regulatory and compliance costs on business and investment, the decline in educational achievement in subjects that drive innovation (i.e. STEM), and the disincentives of relatively generous, long-term, non-contributory welfare and retirement programmes.

LikeLiked by 1 person

When a major city like Shanghai can clear its customs requirement in 2 minutes and I have to wait 40 minutes in a NZ militant bio-security queue and detention centre, showing Customs the chocolate I purchased and then wait to load my baggage onto baggage scanning equipment does show that our lack of productivity is largely in pursuing China’s Mao’s Gang of 4 preference for farming as the predominant economic activity.

LikeLike

Nonetheless, do bear in mind that average labour productivity here is still far higher than it is in China.

LikeLike

A visit to Shanghai Disneyland and various other theme parks in China does show a more significant emphasis on human actors. Whereas in the Tokyo Disneyland when I visited last year, there was a huge use of robot performers, China has chosen not to use any robot performers. Even the robots like the Big Hero Baymax robot was a human dressed up as a robot in Shanghai Disneyland.

Productivity is clearly not a major factor in a Marxist Communist ideology. The emphasis is on people working and contributing and wealth sharing.

LikeLike

I’m not aware of any economic papers that link anecdotal experiences at Disneylands around the world to hard economic data.

Are you able to point to any that can demonstrate a link of the use of human actors at the amusement park and the lowering of a countries Gini coefficient? As China’s workers paradise looks to have a consistently high Gini coefficient…?

Perhaps the results of the Disneyland strategy will appear in the data in due course…?

LikeLike

Just a anecdotal on site observation whilst busy holidaying but Apples CEO did give a interview of why Apple has no choice but to manufacture in China. His main reasons being the availability of high skilled human people resources available to set up mega assembly factories. Quite different from Elon Musks fully automated mega Tesla factories that can be built anywhere. Unfortunately fully automated has it’s share of delivery hiccups where mistakes can be hundreds of millions to fix compared with humans that just need a telling off to adjust a procedure.

LikeLike

Anyway there is plenty of hard economic data available. Just the poor interpretation by NZ economists of that data which has lead to poor decision making in NZ.

LikeLike

In the unlikely event I got to be in charge of the productivity ENIAC contraption I would call for a breakdown of the measurements of Labour and GDP into sector groups in a time series – then I would compare the two series for divergences. There has to be a divergence. In what sector we don’t know. And will never know until we look.

LikeLike

The data are there, and detailed papers have been written on some of the comparisons. But the big lesson is that it is an economy wide issue, not one where the main answers are available by focusing on policies/obstacles in individual sectors.

LikeLike

The lack of Productivity likely coincides with the rise in the tourism dollar where in NZ, Tourism and International Students is a massive $17 billion service industry and a aging population that have reduced productivity and an increasing reliance on health care. 41% of the governments spending is in Health and Welfare. Tourism/International students and Health are all service industries. tThe best service is always more people and not less. Easy answer so I am unsure why economists would struggle to grasp why developed countries productivity continue to decline.

LikeLike

I have troublle believing productivity can be measured. Is GGS being more productive making his comments or would be more productive spending his time developing more properties? Does it depend on whether the Treasury reads and acts apon his comments? It is not difficult to envisage situations where productivity can be measured – which farm produces most milk per unit of labourfor example but the nature of work has changed – as GGS points out most workers are not making things; they are in service industries. The owner of a hotel may take on more junior staff (cleaners and concierge) as the best investment to increase profits but it will reduce the productivity per employee and wages per employee.

LikeLike

The problem with productivity calculations is the reason why the government embarked on an ambitious Think Big Diary industry, they were told by our NZ economists wrongly that this farming activity would increase and add to productivity. But NZ economists were professionally negligent as they failed to count the 10 million cows that it would take that requires massive land and water resources equivalent to feeding and handling the food and waste production of 200 million people. People generate GDP by the various activities, working, creating and being entertained, cows do not. Very simple maths which economists fail to grasp. 10 million cows generate a GDP of around a meagre $17 billion by the production of milk and meat but using the same Land, food and waste planning resources as 200 million people in NZ would generate a GDP measured in excess of multiples in trillions.

LikeLike

Can you go a step further and quantify the GDP of those 200 million and then sub-divide it into Tradable and non-Tradable components

LikeLiked by 1 person

You might be getting ahead of yourself… 6.5m dairy cattle all up… there are certainly ways to lower the use of land and increase the production of the dairy herd… but that is via industrialisation of farming… which NZers don’t seem to be that keen on… so we are left with a second best outcome… its what you do with the milk powder after it leaves the farm gate that counts…

And Fonterra have been pretty shit at doing any useful value adding to it…

LikeLiked by 1 person

10 million cows is correct. Don’t forget meat production cows for slaughter and baby calves, the ones we don’t cull and bury.

LikeLike

Iconoclast, I did refer to GDP measured in excess of multiples of trillions or you could extrapolate from our current GDP of $270 billion on NZ population of 4.6 million, adjust for say the cow sector, you would still end up around $10 trillion in GDP. Throw in some new high tech manufacturing industry like Rocketlab or one of Elon Musks mega Tesla factories and your tradables go up. Anyway just look up any developed country with 200 million people and you would have an idea of the potential GDP and tradables and non tradables as an example.

LikeLike