Yesterday’s post was prompted by looking at the export and import data in last week’s GDP release. Today’s is prompted by looking at the investment data.

The latest quarterly data wasn’t that interesting in itself – business investment fell a bit, but from quarter to quarter there is quite a bit of noise, and not much can be read into a single quarter’s data.

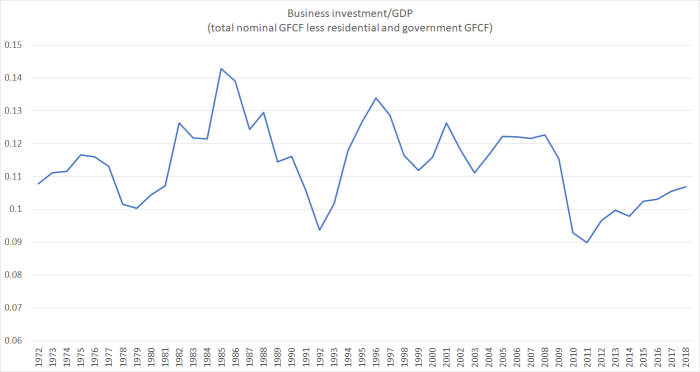

But here is a longer view on a proxy for business investment spending as a share of GDP (total gross fixed capital formation less residential investment less government investment spending), using the annual data back to the year to March 1972. The latest quarterly observation is almost exactly the same level as the final (annual) observation on the chart.

Years into the recovery, after several years of very rapid population growth, business investment as a share of GDP has crept back up to levels that are only higher than seen in past recessions. And by international (OECD) standards, business investment as a share of GDP has been low in New Zealand for decades. It is consistent with the story numerous analysts have highlighted over the years: one of the proximate symptoms of our long-term economic underperformance is that firms haven’t found it worthwhile to invest more heavily here. The last few years look as if they simply reinforce that story.

(And that isn’t, of course, because we have too many houses for our people. If anything, we have too few, so when people – like the Minister of Finance – talk of shifting investment from housing to other things, while not changing anything about population growth, it is meaningless or worse.)

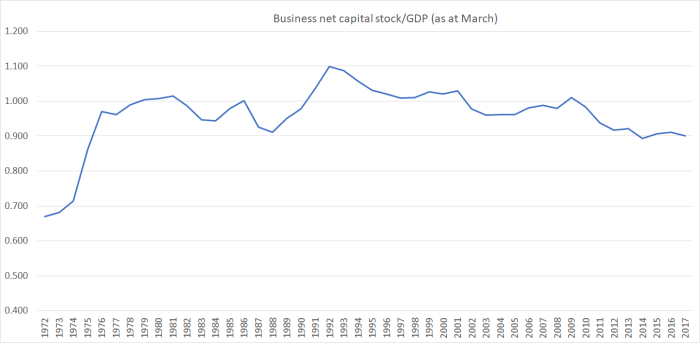

That first chart, which I’ve shown previously, is the flow – each year’s new investment as a share of total GDP that year. But this chart uses the stock figures: SNZ’s net capital stock (total less residential less government) relative to GDP. That takes account of depreciation, and also of the changing growth rate of the population.

The business capital stock (as estimated by SNZ) hasn’t been growing relative to GDP for over 40 years. Over most of the last decade that ratio has been shrinking (and although these data are available only to March 2017, it seems unlikely anything in the last 18 months will materially alter the picture). Businesses – as a whole – simply haven’t found it attractive to invest and grow here.

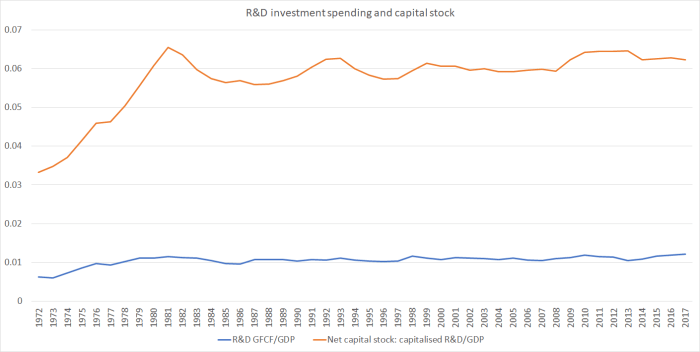

The government is very keen on promoting R&D spending, rushing to put in place new and bigger subsidies without much evidence of having thought much about why it might not be attractive to profit-maximising firms to spend more here.

R&D is included in both the annual new investment spending shown in the first chart above and in the net capital stock data shown in the second chart. SNZ don’t provide a breakdown between government and private components, but for what it is worth I found this chart interesting.

If anything, R&D spending seems to have been holding up quite a bit better than overall business investment and the business capital stock. Which tends to reinforce my doubts about why more taxpayer money should be thrown at this type of spending. Overall R&D spending might be quite low by advanced country standards, but so is business investment more generally, and so is foreign trade. My hypothesis is that all three things are related, and that there is no obvious reason (and no analysis the government has advanced) suggesting that the root cause of the problem is insufficient subsidies for R&D spending.

On a completely different note, tomorrow I’ll take a lot at the latest from the Reserve Bank: Adrian Orr and the tree gods.

I am guessing the gradual decline since 2000 is related to the high exchange rate and substitution towards low-capital using services and away from manufacturing and processing.

LikeLike

With now almost 4 million tourists per year, together with international students, export GDP is this services sector is reaching $17 billion in export GDP. The flow on and trickle effect into domestic GDP is in several multiples driving our NZ economy towards a $280 billion economy but of course with declining productivity and a country of low skilled bus drivers, cleaners and cooks(some would argue cooks are highly skilled).

LikeLike

Every so often I contemplate the three business opportunities that could make me wealthy:

1. Black palm handles for quality axes

2. Fridge door with child proof lock

3. Selling PNG bilums and bilum hats.

Then I realise I just can’t be bothered. The investment environment in NZ is wrong; if successful it would just put barriers between myself and my friends. But there are other problems:

1. Accessing black palm supplies requires a base in Cairns not NZ

2. Samsung will find a way round any patent and produce a finer better and cheaper product (maybe taking photos of who is raiding the fridge) so the only chance of success would be to set up in South Korea.

3. There are Papua New Guineans already doing it and I’d find it immoral to compete. The banning of single use plastic bags (Oct 8th for my nearest supermarket) is a market opportunity. It would be a fun business for a young brave person but most of the economic activity would be in PNG and NZ just a location for sales.

Finance wouldn’t be too difficult – just remortgage the house. It is hard to find “some location specific natural resource” to quote yesterday’s blog. The only resource I can think of is NZ’s clean green environment. There must be potential in high quality tourism and filming and the international growth in ecological interests, etc. But read Mike Joy’s superb passionate article in Monday’s Herald to realise successive governments just don’t give a damn about NZ’s environment so it would be unwise to make investments that assume it will remain or return to pristine purity.

LikeLike

I found interesting in the first chart about how in 2007/08 business investment fell – GFC – and it still hasn’t recovered to the level of pre-GFC (if the GFC was causative). That is some proof towards the assertion often made in this blog (using other sources) that we aren’t in a good position for the next recession (note today’s Herald article predicting the next recession will be worse than the Great Depression, and in 2 years).

LikeLike

When interest rates went above 10% a lot of businesses that rely on debt lost a massive amount of equity having to continue to service that interest obligation. Personally I burned $400,000 in equity just to keep afloat in my own property portfolio of 11 properties over that period. My debt level jumped from $1.6 million to $2 million. If the GFC did not occur I would have followed Terry Serepisos(NZ Apprentice fame) that lost his $500 million portfolio of property. Farmers and other land holders would have had to do exactly the same burning of equity. I blame that all completely on the RBNZ for engineering the NZ 2009 recession. The GFC saved the NZ economy.

LikeLike

It is only in NZ that our RBNZ central bank would intentionally engineer a recession that resulted in a financial crises causing the destruction of $6 billion of mum and dad funds in Finance Companies whilst the rest of the world was trying to prevent a GFC.

LikeLike

Its almost certainly the case that part of the issue of low investment/GDP is connected to the over-stimulation of the non-tradable sector (which incidentally has generally much poorer productivity growth) and the resulting over valuation of NZD on a long-term basis.

However, another aspect of the issue is also likely to be remittance of profit from foreign owned enterprises.

The government needs to analyse the scale of profit remitted offshore by foreign-owned enterprises in New Zealand to understand the sources of the leakage and then to determine whether they’re the result of super-normal profits.

I’m convinced that they’d discover that our enormously profitable – both in absolute terms and net interest margin – banks along with petrol companies and supermarket owners are key drivers of this capital leakage.

Greater focus on competition policy beyond just telecoms and electricity is needed. The government needs to focus on this. It amazes me how stubborn both sides have been regarding this. Plenty of focus on telco but none on petrol companies (whose margins have expanded almost continuously in the past decade).

LikeLike

Our Aus banks transfer bottom line profits of $5 billion after tax to Australia every 12 months. They should be forced to pay their staff equally in NZ equal to Australian employees. It is unfair that banks pay their their staff 30% higher in Australia than they do in NZ.

LikeLiked by 1 person

The real exchange rate has a part to play in the business investment question, however, the issue is more broad than that – core question is whether the return on investments (however measured) is high enough to offset the risks of increasing business investment here… the charts suggest a ‘muddle through’ mentality, which as one commentator above noted… could do it but can’t be bothered… The old saw of boat, BMW and batch may have something to do with it, or just lifestyle.

NZ management as a whole is pretty average (looking at you Fletcher Building and Fonterra, amongst others) and while there are good people there are just not enough good people compared to the rest…

More local processing of commodities will increase business investment to be sure, but does the expected ROI support the capital spend? And is the capital even there? Well perhaps, but investment managers love the ‘big end of town’, love hugging the index (NZSX50) and offshore diversification…

‘Tis a conundrum methinks….

LikeLike

Fletcher Building and Fonterra was not NZ management. The senior management team that lead to the losses by those companies were overseas imports. The problem with overseas imports is that they were trained in large economies where sales volume was king and margin was sacrificed. In NZ it is all about margin given the small size of the NZ economy and finding suckers(sorry customers) that would pay the margin.

LikeLike