After the 1996 election, and as a small part of the deal whereby New Zealand First went into government with National, the Policy Targets Agreement governing monetary policy was amended. The first section now read, adding the text I’ve underlined.

1. Price Stability Target

Consistent with section 8 of the Act and with the provisions of this agreement, the Reserve Bank shall formulate and implement monetary policy with the intention of maintaining a stable general level of prices, so that monetary policy can make its maximum contribution to sustainable economic growth, employment and development opportunities within the New Zealand economy.

Going into that election, New Zealand First had campaigned for material changes to the way monetary policy was run. What it got was an increase in the target range (from 0 to 2 per cent, to 1 to 3 per cent) and those new words. Inside the Bank, we never paid any attention to the words ever again. They never came up in policy deliberations. They were seen as some mix of political rhetoric and a statement of the obvious – from our perspective, pursuing price stability was the best and only contribution monetary policy could make to those other worthy things. Note that in negotiating the drafting, Don Brash even got the crucial word “sustainable” in.

In the new Policy Targets Agreement signed yesterday, this is how the equivalent paragraph reads.

1. Monetary policy objective

a) Under Section 8 of the Act the Reserve Bank is required to conduct monetary policy with the goal of maintaining a stable general level of prices.

b) The conduct of monetary policy will maintain a stable general level of prices, and contribute to supporting maximum sustainable employment within the economy.

All but equivalent I’d say. Curiously enough, I didn’t see the parallel drawn in the material Treasury released (including the RIS) on the new formulation of the monetary policy objective.

To be sure, as I noted in yesterday’s post on the PTA, the new PTA does include a couple of other references to employment. Employment is added to the list of things where the Reserve Bank Governor is supposed to seek to avoid “unnecessary instability”. However, this is the clause the Reserve Bank has been relying on in the last few years to defend its belated and reluctant response to core inflation outcomes persistently well below the target midpoint. And the Bank will be required to discuss, in each Monetary Policy Statement, how current OCR decisions are contributing to supporting maximum sustainable employment. The Minister has attempted to suggest that this provision will give bite to the new employment focus. If he really believes that, then – despite all the time he spent on FEC in Opposition – he obviously hasn’t looked at all carefully at how the Reserve Bank complies with the current statutory provisions governing Monetary Policy Statements – formulaic at best. As I noted yesterday, it is easy to predict the formulaic language now – brand new recruits could write the words, (and may well do so).

I’ve been a bit ambivalent about changing the statutory (or PTA) goal for monetary policy. Active discretionary monetary policy exists for output and employment stabilisation reasons, and in principle it is worth recognising that. Since day one of the current Reserve Bank Act, that focus has been implicit in the way Policy Targets have been constructed. It is not a new thing. On the other hand, there has been a suspicion that Grant Robertson was more interested in things looking a bit different – like that wording Winston Peters had introduced in 1996 – than in things actually operating differently, and thus on occasion I’ve suggested this change was more about political positioning and “virtue-signalling” than anything else.

And that might be fine if the Reserve Bank had been doing a superlative job in the last decade, but somehow there was still debate in some quarters as to whether output/employment stabilisation was a legitimate objective at all. But they haven’t. Core inflation has been persistently below the target midpoint – the focus of the PTA – for years, and even on their own (diverse) estimates – see their chart below – the unemployment rate was above the NAIRU for almost all the decade.

That combination just shouldn’t have been. Monetary policy – again on the Bank’s own reckoning – works much faster than that. Instead, through some combination of forecasting mistakes and biases towards tighter policy – recall Graeme Wheeler’s repeated hankering for “normalisation” and his actual ill-judged tightening cycle – they allowed the economy to run below capacity for years, more people than necessary to stay unemployed for longer, and didn’t even come close to deliver inflation averaging around 2 per cent.

And yet when – as he was on Radio New Zealand this morning – the Minister of Finance is asked what difference the new PTA (and proposed statutory amendment) will make he flounders, and won’t even refer to the experience of the last decade. His officials seem to be as bad. In the Regulatory Impact Statement section on the proposed new objective, here is what The Treasury had to say

The main non-monetised benefit is to ensure that monetary policy decision-makers continue to give due regard to the short term impacts of monetary policy on the real economy. This is intended to improve the wellbeing of New Zealanders by ensuring that monetary policy seeks to minimise, or does not exacerbate, periods of economic decline.

The new Governor’s comments yesterday were along similar lines – just recognising how things are done already.

So the experience of the last decade is just fine is it? If so, the proposed law change really must be just about political rhetoric and positioning.

To be clear, there are limits to how much any new words themselves could have changed the Reserve Bank’s approach to monetary policy. And, as everyone recognises, in the longer-term, monetary policy can only affect nominal variables (inflation, price level, nominal GDP etc) not real ones (employment and output). But the government – supported by advice from The Treasury – appears to have chosen the weakest formulation possible, with little or no effective buttressing elsewhere in the Policy Targets Agreement. There is, for example, no requirement to publish estimates/forecasts of “maximum sustainable employment” or associated concepts such as the NAIRU, and no requirement to account, look backwards, for how monetary policy has done in effectively minimising cyclical deviations in employment/unemployment.

Individuals and organisational culture matter a lot. Arguably they matter more, at the margins, than precise wording in documents like the PTA. The Reserve Bank’s culture appears over the last decade to have backward-looking, constantly fighting the last war – surprisingly strong inflation in the years running up to 2008 – insular, and – as has been the case for decades – not really much interested in labour market outcomes at all. In all that, they’ve been backed by the Reserve Bank’s Board.

Adrian Orr is a strong character, and has an incentive – all those Stage 2 review battles to fight – to at least sound different than his predecessor Graeme Wheeler. Then again, he emerged through a selection process undertaken by the Board – which was explicitly happy with what had happened in the previous decade – and his Minister has given no indication that he is anything other than happy with the actual past conduct of monetary policy. A pessimist would suggest that, to the extent we see change, it will be cosmetic more than substantive. Cosmetics have their place, but substance – avoiding repeats of situations where at the same time core inflation is well below target and unemployment is well above a NAIRU, including in the next recession – matters rather more.

It is interesting to ponder how the new Governor – single decisionmaker for now – will address the question of what “maximum sustainable employment” is. I’m expecting something reasonably vacuous and circular – “since we (again) forecast inflation getting back to target in a couple of years time, by definition – by construction of our model – employment must be close to the sustainable maximum”. Doing so will be easier because the employment rate has no public resonance in the way that the unemployment (or even underemployment) rates do.

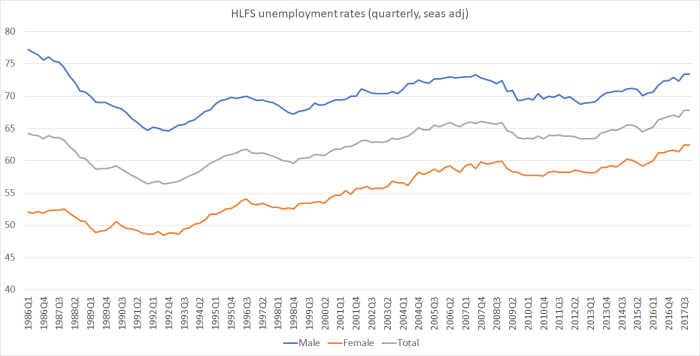

But here is a chart of HLFS employment rates since the survey began in 1996.

Female employment rates have been trending upwards, as one might expect as part of social changes. However, male employment rates (73.4 per cent) are still well below where they were in 1986 (77.2 per cent). In plain English senses, there is little reason to suppose we are anywhere near maximum sustainable employment rates for the economy as a whole. I’m sure the plain English sense isn’t intended, but still.

And those male employment rates aren’t just about more young people being in tertiary education – who are, in any case, outweighed by more old people working. Here are the three prime-age male employment rates

For all three groups, employment rates now are materially below those thirty years ago, in a more deregulated labour market.

For all three groups, employment rates now are materially below those thirty years ago, in a more deregulated labour market.

It just reinforces my sense that in making changes they’d have been better off using unemployment rates as a reference point, and requiring the Bank to produce a richer array of labour market analysis. The actual new wording will easily translate to nothing if that is what the Governor wants.

And, finally, almost in passing, there has been coverage of former Reserve Bank chief economist Arthur Grimes’s criticisms of the change in the monetary policy objective, in which he talked of a “disastrous route”, a “crazy target”, the potential for the changes to destabilise the economy and so on. He went on to assert that most episodes of financial instability in the world have flowed from the the United States, and a lot of that has been caused by their dual objective system.

I’m not quite sure which episodes Arthur has in mind with that latter comment, although I assume that the 2008/09 crisis is the principal one he is thinking of. It is perhaps worth remembering that our Reserve Bank itself has produced research suggesting that the way it was reacting to incoming data in the decade or two prior to 2008 was very similar to the way the Federal Reserve and the Reserve Bank of Australia were reacting. That isn’t surprising. In practice, whatever the precise wording of the respective mandates, all three were functioning as flexible inflation targeters. It hasn’t been easy to rerun the model for the last decade – since for a prolonged period the Fed was at an effective interest rate floor. The way the two Antipodean central banks have conducted policy have still been fairly similar and thus – even though neither reached the effective interest rate floor – both countries have had below-target inflation in the context of labour markets that haven’t exactly been overheating (the RBA still thinks unemployment there is above the NAIRU).

Of course, these comments are a bit of a double-edged sword. I think Arthur Grimes is quite wrong in his suggestion that our changes are very damaging and dangerous. On the other hand, they are also a reminder that individuals and institutional cultures (and blindspots) often matter more than precise specifications of statutory objectives. Changing the statutory mandate here, in deliberately vague ways, won’t make any helpful difference – other than perhaps in political marketing – unless the new Governor is about to lead some material culture change, and bring a fresh focus on avoiding prolonged periods of unnecessarily high unemployment.

It is his first day, so only time will tell. For now, the signs aren’t encouraging. But perhaps there will pleasant surprises in store.

I agree with your point on culture mattering a lot Michael. The Bank has a history of being hawkish. When I worked there I was happy to go along with it and arguably was at the more hawkish end of the spectrum. But that was the 90’s when the issue was to anchor inflation expectations and any indication that the Bank might lose its resolve led to a jump in inflationary pressure. Today’s environment is quite different. Inflation is low and expectations are well anchored. Households and (dairy) farmers are heavily indebted and any lift in rates will have a sharp contractionary effect.

I’m optimistic that over the past 12-18 months the Bank has learned this and I’m heartened when I talk with them about policy. Over the past 18-24 months the Bank has been more dovish than both market economists and market pricing and I think they’ve been closer to reality than both.

LikeLike

I really hope you are right Peter, altho it is worth bearing in mind that even in late 2013/early 2014, the Bank – bad as it was – was less hawkish than most domestic market economists and (from memory, so perhaps I’m wrong) market pricing. We used to constantly discuss at MPC how it was private forecasts of inflation were typically higher than ours.

(Like you, I’ve had my time as a hawk – sometimes episodes I look back on and think I was right, and at other times not. Actually, same goes for my – rarer – inside-the-Bank stints as a dove.

LikeLike

Most domestic market economists are paid by their respective banks to ensure that the banks profits are maximised rather than to ensure that the economy is at its best possible shape. I would not trust anything that a market economist has to say.

LikeLike

I think it is blogs like Croaking Cassandra does make decisions by the RB Governor a lot more transparent and therefore certainly assists the Finance Minister. The problem with elected representatives is that appointments have been more for political reasons rather than the experience, qualifications and wisdom that the person has. Especially so in Grant Robertson with no financial or economic training whatsoever. He does seem to be making some hard and tough financial decisions reasonably well, bringing some discipline to a rather flamboyant and easy spendup Prime Minister that seems to want to spend it all away.

LikeLike

It sounds like “sustainable” is going to mean anything to anyone and nothing new has been introduced by Grant Robertson other than a rehash of wording with no clear targets.

LikeLike

“Inside the Bank, we never paid any attention to the words ever again.”

Love it!

LikeLike

just another immeasurable among many immeasurables

LikeLike

1) An OIA request for discussion about whether to have an employment or unemployment objective might be interesting.

2) silly extreme scenario – presumably an employment scenario where everyone of working age has two jobs (maximum employment?) less 4% for NAIRU would be possible. Would it be sustainable? Would it be desirable? Might be possible by running the country into the ground so that everyone had to get two jobs.

LikeLike