My previous post concentrated mostly on the new Policy Targets Agreement, which will govern monetary policy, under the current Act, for the next year or so.

In this post, I want to concentrate on the announcements made by the Minister of Finance about the first stage of his planned legislative reforms. There is a summary graphic, and a set of questions and answers.

The proposed reforms represent a step forward. We’ve been in the peculiar position for almost 30 years in which one individual, not even appointed directly by the Minister of Finance, made all the monetary policy decisions. It made it easy to know who to fire – that was the argument made for the model in the late 1980s – but it was a model that was out of step with how almost every other public agency was run and (as became increasingly apparent) with how monetary policy was run in most other countries. In a free and democratic society, committees – with ranges of views, and the implicit checks and balances a range of individuals provide – should be how major public authority decisions are typically made. It is little consolation that successive Governors drew on advisory committees to assist their decisionmaking: on the one hand, all members of those committees owed their positions to the Governor, and on the other, institutions need to be resilient to bad appointees, not just get along moderately well in normal times. And if some advisers were happy to disagree (and Governors sometimes even welcomed a range of views), others weren’t – I recall one Assistant Governor who told us that he saw his role on the OCR Advisory Group as being to back the Governor.

But that particular battle now appears to have been fought and won – albeit belatedly (Treasury – and the Green Party – were calling for structural reform years ago). The Labour Party campaigned on, and the government has now promised legislation to give effect to, moving to a statutory committee model. Today’s announcement fleshes out some – but not all – of the details.

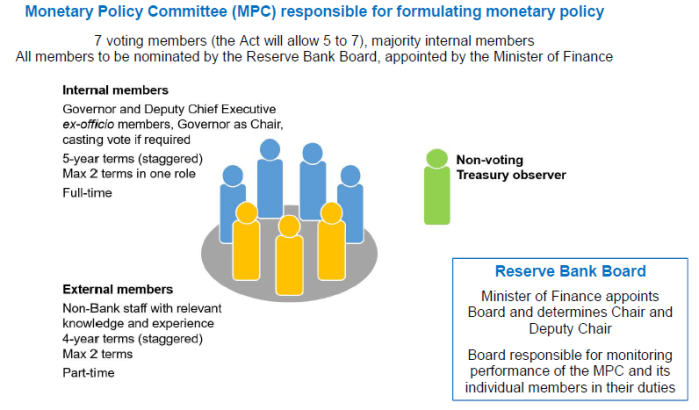

Here is the summary graphic

The key aspects are that

- there will always be a majority of Reserve Bank staff,

- there will be a minimum of two externals,

- appointments will be made by the Minister of Finance but s/he will be able to appoint only people nominated by the Reserve Bank’s Board.

This model is a slight improvement on what the Labour Party campaigned on. In that model, the Governor himself would have appointed all the MPC members, internal and external. But the improvement is slight, for two reasons:

- first, because a majority of the committee will be internal, all appointed to their executive day jobs (eg Assistant Governor, Chief Economist or whatever) by the Governor. No Board is going to turn down the Governor’s recommendation as to which of his staff should be on the MPC. Thus, the Governor in effect appoints the majority of the committee. For a good Governor – really welcoming diversity and debate – it mightn’t be a problem. For more average appointees, it reinforces the risk of continued groupthink and a voting bloc on the committee. Remember that the executive members have their pay and promotion determined by the Governor,

- second, because the Reserve Bank Board is likely to look largely to the Governor for advice on who should be the external appointees to the committee. Recall that the Governor himself is a member of the Board – even though its prime job is to hold him to account – and most of the Board members have no subject expertise, no resources, and little reason not to defer to the Governor (whom they themselves appointed). Perhaps some reasonable people will be found to serve, but it seems exceptionally unlikely that anyone awkward, or with a materially different perspective, will be allowed in the door. In all likelihood, we’ll end up with something not much improved on the model in place for the last 17 years or so – in which the Governor has had a couple of part-time external advisers, appointed mostly for their business connections and knowledge, rather than their perspectives on macroeconomic policy.

This simply isn’t the way public appointments should be made. The Minister of Health appoints people directly to DHBs, the Prime Minister directly determines who will be appointed as the Commissioner of Police, ministers appoint directly members to the board of all sorts of decisionmaking crown entities (including, in the financial areas, the Financial Markets Authority), and so on.

And direct appointment by elected politicians is the way most top central bank appointments are made in other countries. In Australia, it is true of the Governor, Deputy Governor, and all the RBA Board members. In the UK, all but two of the MPC members are directly appointed by the Chancellor, and in the US all the members of the Federal Reserve Board of Governors are appointed by the President, subject to Senate confirmation.

I hope someone asked Grant Robertson why he resisted bringing the appointment process for the Reserve Bank of New Zealand positions into the international mainstream, because I don’t understand it – and there is nothing to justify his choice in rhe Q&A material that has been released. Ministers may not have much subject expertise, but they have legitimacy – they are elected, and have to front to Parliament each week. The Reserve Bank Board members have no subject expertise, and no legitimacy – indeed, at any one time, half will have been appointed in the previous term of government. They might be competent behind-the-scenes professional director types, but that’s all. And yet they are being empowered to choose who will run New Zealand macroeconomic policy. It is a gaping democratic defict that really should have been fixed, not exacerbated. And it is not as if the Board’s practical track record might persuade one to set aside principled objections to the process – they’ve just been cheerleaders, more focused on having the Governor’s back, than on serving the public interest.

The appointment process is one reason why I call today’s announcement as a big win for Reserve Bank management. Committee appointments will safely be in the hands of the Governor and his team (Board and management).

The other reason why it is a big win for Bank management is the announcements about the processes that the new Monetary Policy Committee will be expected, or required, to adopt.

Here is part 2 of the Minister’s graphic

The idea of a charter makes sense. Arrangements around how the new MPC should work are probably better not legislated – although I think a requirement to publish minutes (although not the form of those minutes) should be in statute – and thus able to evolve with experience and individuals. Beyond that, I think the Minister has made the wrong choices when articulating what he will be looking for, largely caving to the preferences of the Bank’s management, who were horrified by the idea of open debate and a transparent recording of views and associated individualised accountability.

Several of better inflation-targeting central banks are much more open – notably, those of the UK, the US, and Sweden. But here is what the Minister proposes

How will the MPC take decisions?

It is expected that the MPC will aim to reach decisions by consensus. Where a consensus cannot be reached, decisions will be taken by a majority vote, with the Governor having the casting vote if necessary.The Governor will chair the MPC and will be the sole spokesperson on its decisions.

What documents will the MPC publish?

In addition to Monetary Policy Statements, it is intended that the first Charter agreed between the Minister and the MPC will require the MPC to publish non-attributed meeting records that reflect differences of view between MPC members where they exist. It is also intended that the MPC will publish the balance of votes for any decision where a vote is required, without attributing votes to individuals. This approach will balance the need for transparency about the decision-making process with the need for clarity and coherence in communicating the MPC’s decisions.

Frankly, it seems unlikely we will ever see vote numbers. Recall that the Governor has an internal majority on the MPC, who can – and may well – caucus before the meeting and agree a collective view. The externals start out in a minority, will have already passed some sort of inoffensiveness test to get appointed, and they appear unable to articulate their views in public, so the incentive to record an anonymous dissenting vote seems pretty low. A management-driven “consensus” seems likely to be the default option, and over time that will become the self-reinforcing norm, because the signal in one external insisting on recording a dissenting vote will be sufficiently attention-grabbing that often enough people just won’t go that far. Far better to normalise the fact that there is – and should be – quite a range of views, whether about how the economy will unfold and how monetary policy should respond to the risks. As I’ve noted before, it is not clear how the citizens of the US, the UK, or Sweden or worse off for an open and transparent process of individual responsibility and accountability, and an ongoing moderately open contest of ideas. Bureuacrats don’t like it – of course – but we should be designing public agencies around the interests of the public, including those scrutiny and accountability, not around the interests of the bureaucrats. In this case again, Grant Robertson appears to have bowed to the personal interests of the officials.

There are some good aspects to what the Minister has announced:

- as I noted in my earlier post, the move away from a Policy Targets Agreement model to a system in which the Minister sets the operational objectives, and the associated official advice is pro-actively published, is a step forward, and almost inevitable with the move to a committee. But there are lots of operational details to be clarified, including (for example) how frequently the Minister can change such objectives (the default PTA has been for five years),

- on-balance, the inclusion of a non-voting Treasury observer on the MPC is probably a modest step forward, but it depends how it works. The documents suggest this person is simply there to pass on information about fiscal policy, and given the substantial time commitment the MPC role is likely to entail it could end up filled by a fairly junior Treasury person (by contrast, in Australia the Secretary to the Treasury sits on the RBA Board),

- the Minister is moving to provide for the appointment of the Board chair and deputy chair to be made directly by him (the normal model) rather than chosen by Board members themselves. At the margin this will help remind the Board that they work for the Minister and the public, not for the Bank. To be fully effective, however, the Minister should also amend the Act to allow him to dismiss Board members for failing to be sufficiently vigorous in holding the Governor and MPC members to account.

But there are also lots of issues that aren’t sorted out in the announcement today and which will only become clear when the legislation emerges (or in some cases when the charter is signed). For example:

- what are the limits of what the new MPC will be responsible for? The Q&A material says that “For example, the MPC will also have responsibility for strategic choices around the monetary policy tools used by the Reserve Bank”, but does this include foreign exchange intervention strategy, issues around issuing digital currency, the terms of which the Bank issues physical currency etc (all relevant to zero lower bound issues). Then again, perhaps these things don’t matter because the Governor has a built-in majority on the MPC?

- what can individual MPC members be fired for (given expectations of consensus decisionmaking), or will the formalised accountability model – which never amount to much in practice – be largely got rid of?

- whose will the forecasts in the Monetary Policy Statement be? At present they are, formally, the Governor’s forecasts.

And then there is the Stage 2 part of the review of the Reserve Bank Act. The Q&A document says

Phase 2 of the Review is currently being scoped. It will focus on the Reserve Bank’s financial stability role and broader governance reform. The Panel is due to give the Minister of Finance its recommendations for the scope of Phase 2 of the Review shortly. Announcements on this will be made in the coming months. Subsequent policy work will commence in the second half of 2018.

But given the increased role for the Reserve Bank’s Board in today’s announcement, the government seems to have already decided to retain something very like the current governance model and in particular the role for the – historically useless – Board. I guess there is still time to reconsider before the Stage 1 proposals are legislated, but they’d be better off splitting up the Bank, setting up a Prudential Regulatory Agency, taking appointment powers directly into the Minister’s hands (perhaps with some non-binding confirmation hearings) and getting rid of the Board altogether.

Meantime, they will be celebrating at the Reserve Bank tonight. As far as possible, the (effective) status quo has won out, and a more open and contestable system has lost out.

The first thing that needs to be identified is what are all the levers that are available to the RBNZ. Obviously there is Monetary policy and there are macroprudential tools. But the banking licence and the conditions of the licence can be also used and I have been told is being used to curb credit availability.

There is no point dropping the OCR if credit availability conditions are tightened at the same time. It nullifies the effect of the wealth effect. People can’t spend if they can’t borrow money to spend even if the OCR falls.

Banks being large monopolies as well has been able to reprice their margin higher due to restrictions on the new competing based on capital adequacy and local savings. Our 4 Australian banks control $170 billion in local savings compared with the new competing banks with no local savings and entirely reliant on paid up capital injected into the local subsidiary bank. They are not able to leverage off their parent company balance sheets. In effect behaving like our small rural banks.

LikeLike

If we compare to a Board of Directors of a public company we would have

The executive team, CEO, CFO, CIO which would be the equivalent to the 4 RBNZ Executive team.

Then you have the 20% shareholders that can demand a board director to represent their interests plus there would be independent directors for governance.which would be the equivalent to the 3 industry appointments to the RBNZ. In theory would represent the views of industry but given that they are the RB governors appointees then the question is a question of independent scrutiny. No one usually bites the hand that feeds them.

The Chairman usually would adjudicate disputes and call for the final vote which I would guess would be the role of the Treasury appointment to the RBNZ. The main difference is the lack of any casting vote in the event of a split vote. But given there is only 7 reprensentatives the final vote is always in favour of the RB governor anyway.

More transparency and more research is a definite must otherwise we continuosly get this stone walled approach ie silence in the interest of National Security BS.

LikeLike