A few months I signed up to get the e-mail newsletters of US analyst Aaron Renn.

Aaron M. Renn is a senior fellow at the Manhattan Institute, a contributing editor of City Journal, and an economic development columnist for Governing magazine. He focuses on ways to help America’s cities thrive in an ever more complex, competitive, globalized, and diverse twenty-first century.

There is an interesting mix of material on urban issues. But this morning, one newsletter in particular caught my eye. The title was a warning: “Sprawl in its Purest Form, Cleveland edition”. The article began this way.

…..the image below contrast[s] the amount of urbanized land in Cleveland’s Cuyahoga County in 1948 vs. 2002. The county population was identical in both years: 1.39 million.

And the piece goes on to lament how costly the spread of suburbia is, concluding that

As a rough heuristic, development of new suburban footprint should largely be limited to the growth rate in households to avoid saddling a region with excess fixed cost.

It might be music to the ears of some of our own planners, and the politicians who continue to enforce their policies.

Renn laments the fact that, at least in this case, when cities can spread and new houses can easily be built, while the population doesn’t change much, existing houses lose value

If you keep building new homes but you aren’t adding households, then older homes at the bottom of the scale will be abandoned. And all up the stack homes are devalued.

In the same way, when we had restrictions on importing cars in New Zealand for decades, secondhand cars didn’t depreciate much. Most of us prefer access to newer cars.

I had a look at some Cleveland data. And sure enough not only has that county’s population been largely unchanged, but greater Cleveland (MSA) with just over 2 million people also hasn’t had much change in population for 50 or 60 years (if anything falling slightly more recently).

I also had a look at house prices. Demographia reports that Cleveland median house prices are 2.7 times median incomes in Cleveland, averaging US$146000 last year. Average per capita GDP in the Cleveland metro area was around US$56000 in 2016.

On the other hand, a friend had mentioned the other day a house, perhaps 150 metres from where I’m typing, that had sold the other day for $831000. It is a small house (100 square metres) on a pretty tiny section (324 square metres) – with a major construction project almost on the doorstep for the next 18 months or so – and as far as I can see nothing out of the ordinary. That is the point – it isn’t egregiously expensive for Wellington (let alone Auckland) in this day and age. It is about what one might expect, given our laws and regulatory practices. Average GDP per capita in Wellington in the year to March 2016 was around $NZ67900 – a fair bit less than in Cleveland.

Homes.co.nz records that the same Island Bay house sold in 1985 for $76500. Apply the Reserve Bank’s inflation calculator and in today’s dollars that would be the equivalent of $207000. The actual recent sale price – the real increase in price – was four times that.

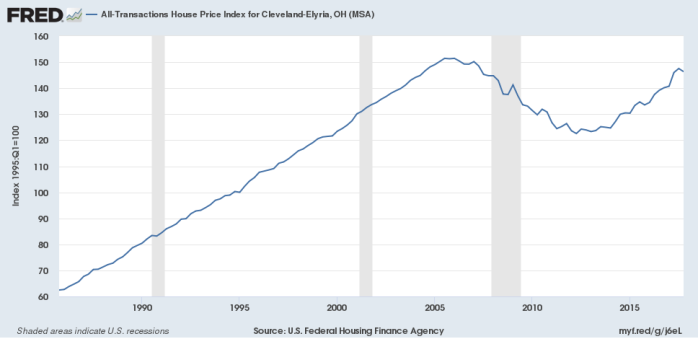

How have Cleveland house prices done over time? Here is a chart, back to 1985, from the FRED database.

Nominal prices have increased quite a lot. But in real terms, applying a US inflation calculator, Cleveland house prices have barely moved – up a bit in the boom years, down in the recession, but over 33 years virtually no change at all. Houses were highly affordable then, houses are highly affordable now. And lest you assume Cleveland is some economic wasteland, the FRED database also suggests that the unemployment rate there has been averaging about 5 per cent in the last year or two, very similar to that in New Zealand.

I usually focus on cities with fast-growing populations in discussing US examples of low and affordable house prices – eg Atlanta or Nashville. And I’ve never been to Cleveland, and have no particular idea how attractive or otherwise parts or all of it are (in Wellington, Porirua and Wainuiomata – for example – also have their downsides). But the ability of the citizenry to readily expand the physical footprint of the city seems like a success story, producing housing market outcomes that seem much more appealing – particularly to younger people trying to enter the market – and affordable than what we now seem to manage in our larger New Zealand cities.

We should steer well clear of “rough heuristics” or tighter rules that try to limit the expansion of the physical footprint of cities, or allow officials and politicians to determine which land can and can’t be built on, in what order. A competitive market for urban land – peripheral and central – remains the best prospect for once again delivering what should be a basic expectation: affordable housing.

Sadly, I noted in ACT’s newsletter earlier in the week, a link to a parliamentary question from a few weeks ago in which the Minister for the Environment indicated that “Cabinet is yet to make any decision about whether to review the Resource Management Act”. I’ve long been sceptical as to whether, even if some Labour parts of a left-wing government was willing to think about serious reform, such reform would be possible given the reliance on the Greens to pass government legislation. Sadly, for now it increasingly looks as if those fears are being realised.

House – and land prices – need to fall. This government, like its predecessor, seems at scared of such an outcome, and unwilling to take steps that offer the prospect of sustained much lower prices.