Six months or so ago the Reserve Bank announced that it would be conducting a review of capital requirements for banks. At the start of last month, they released an Issues Paper, inviting submissions by today (rather a short period of time, for an issue which has major implications for banks’ financing structures and, potentially, costs). I’m not going to make a formal submission, but thought I might outline a few thoughts on some of the issues that are raised in (or omitted from) the paper.

I’d also note that it is a curious time to be undertaking the review. Background work and supporting analysis is always welcome, but here is how the Reserve Bank summarises things.

Detailed consultation documents on policy proposals and options for each of the three components will be released later in 2017, with a view to concluding the review by the first quarter of 2018.

But the Reserve Bank is now well into a lame-duck phase. Graeme Wheeler – currently the sole formal decisionmaker at the Bank – leaves office on 26 September, and then we have an acting Governor (lawfully or not) for six months. Spencer’s temporary appointment expires (and he leaves the Bank) on 26 March 2018, which is presumably when a new permanent Governor will be expected to take office. The incentives look all wrong for getting good decisions made, for which the decisionmakers will be able to be held accountable. Big decisions in this area – and the Bank is raising the possibility of big increases in capital requirements – are something the new Governor should be fully coomfortable with (and, especially if an outsider is appointed, that shouldn’t just mean some pro forma tick granted in his or her first days in office.) We have constitutional conventions limiting what governments can do immediately prior to elections. It isn’t obvious why something similar shouldn’t govern the way unelected decisionmakers behave in lame-duck, or explicitly caretaker, periods. Some decisions simply have to be made and can’t wait. These sorts of ones aren’t in that category.

(In passing, and still on capital, I’d also note that there is something that seems not quite right about the Reserve Bank’s refusal to comment on why a couple of Kiwibank instruments have not been allowed to count as capital. The capital rules should be clear and transparent. The terms of the relevant instruments are also presumably not secret. Perhaps Kiwibank has been told why their instruments missed out, but it seems unsatisfactory that everyone else is left guessing, or reliant on things like the deductions and speculations of an academic who was once a regulatory policy adviser (eg here and here). I have no particular reason to question the Reserve Bank’s substantive decision, but these are matters of more than just private interest. It is an old line, but no less true, that in matters where government agencies are exercising discretion sunlight is the best disinfectant.)

High levels of bank capital appeal to government officials. To the extent that more of a bank’s assets are funded by shareholders rather than depositors then, all else equal, the less chance of a bank failing. And if avoiding bank failure itself isn’t a public policy interest – after all the Reserve Bank regularly reminds us that the supervisory regime isn’t supposed to produce zero failures – minimising the cost of government bailouts is. There might be various ways to do that – the Open Bank Resolution model is designed to be one, but high levels of capital are another.

High levels of capital should also appeal to depositors and other creditors. Your chances of getting your money back in full are increased the more the bank’s assets are funded by shareholdes, who bear the losses until their capital is exhausted. Of course, that argument is weakened if you think that the government will bail out anyway, but that is just another reason for governments to err towards high levels of capital.

Capital typically costs more than deposits (or wholesale debt funding). That isn’t surprising – the shareholders are taking on more risk. But, of course, the larger the share of equity funding then the lower the level of risk per unit of equity. In principle, higher capital requirements lower the cost of capital. Very low capital levels should tend to raise the cost of debt (debt-holders recognise an increased chance that they will be the ones who bear any losses). Modigliani and Miller posited that, on certain assumptions, the value of a firm was unaffected by its financing structure – to the extent that is true, higher capital requirements don’t affect the economics of (in this case) banking.

It won’t hold in some circumstances. For example, if creditors are all sure a government will bail them out, a bank is much more profitable the lower the capital it can get away with. In the presence of that sort of perceived or actual bailout risk, there is little doubt that increasing capital requirements is a real cost to the banks. But it is almost certainly worth doing: it helps ensure that the risks are borne by the people responsible for the decisions of the bank (shareholders, and their representatives – directors and management).

Taxes also complicate things. If the tax system has an entrenched bias in favour of debt, then increased capital requirements will also represent a real cost to the banking system. Many – most – tax systems do have such a bias. For domestic shareholders, and to a first approximation, neither our tax system nor that of Australia have that bias. That is because of the system of dividend imputation, which is designed to avoid the double-taxation of business profits (returns to equity). Unfortunately, there is no mutual recognition of trans-Tasman imputation credits, and most of our banking system is made up of Australian banks with (mostly) Australian shareholders. For most, but not all, of our banks increasing capital requirements is likely to represent some increase in effective cost. And the resulting revenue gains are mostly likely to be collected by the Australian Tax Office.

An open question – and one not really touched on in the Bank’s issues paper – is to what extent our bank regulators should take account of these features of the tax system. For most companies, capital structure is a choice shareholders and management make, weighing all the costs, benefits, opportunities and distortions themselves. But in banking, for better or worse, regulators decide how much capital banks have to raise to support any given set of assets. One could argue that tax is simply someone else’s problem: if higher required capital ratios increased costs, the Australian banks could simply redouble their lobbying efforts in Canberra to get mutual recognition of imputation credits, and if that didn’t work, there would simply be a competitiveness advantage to New Zealand banks. Perhaps that solution looks good on paper, but I think it is less compelling than it might seem. First, banks can and do lobby here too. The Reserve Bank might get to set capital ratios at present, but that law could be changed. And second, we benefit from having foreign banks, with risks spread across more than one economy.

Even if all the tax issues could be eliminated here – and they won’t be in time for this review, if ever – there is still the possibility that the market will trade on the basis that additional capital requirements will increase overall funding costs for banks, even if there is little rational long-term reason for them to do so. One reason that problem could exist is because the tax biases are pervasive globally, and it is therefore a reasonable rule of thumb for investors to treat higher capital requirements as an expected cost.

Over the years, I’ve tended to have a bias towards higher capital requirements. I’ve read and imbibed Admati’s book (for example). As recently as late last year I wrote here

My own, provisional, view is that for banks operating in New Zealand somewhat higher capital requirements would probably be beneficial, and that there would be few or no welfare costs involved in imposing such a standard. My focus is not on avoiding the possible wider economic costs of banking crises (which I think are typically modest – if there are major issues, they are about the misallocation of capital in booms), but on minimising the expected fiscal cost of government bailouts. As I’ve explained previously, I do not think the OBR tool is a credible or time-consistent policy.

But I have been rethinking that position to some extent. The Reserve Bank talks in its Issues Paper of the possibility of an “optimal” capital ratio (from the academic literature) of perhaps 14 per cent (with estimates that range even higher), well above the minimum ratios that are in place today.

But if there are additional costs from raising capital requirements – which seems likely, at least to an extent – we need some pretty hard-headed assessments of the real gains that might accrue to society as a whole to warrant those increased costs. And those gains are hard to find:

- for over 100 years our banking system has been impressively stable. If that was in jeopardy in the late 1980s, that was in unrepeatable circumstances in which a huge range of controls had been removed in short order (and when there were no effective minimum capital requirements at all).

- repeated stress tests, whether by the Reserve Bank, APRA, or the IMF all struggle to generate credible extreme scenarios in which the health of an indvidual bank, let alone the system, could be seriously impaired. In most of those scenarios, the existing stock of capital hasn’t been impaired at all, let alone being at risk of being exhausted.

- we have a banking system where most of the main players are owned by major larger overseas banking groups with a strong interest in the survival of the domestic operation, and the ability to provide any required capital support (the New Zealand regulated entities aren’t widely-held listed companies).

I’m still not sure what to make of the role of the OBR mechanism. As I noted earlier, I’ve never been convinced that it is a credible or time-consistent option, but our officials appear to, and even ministers talk up the option. If they really believe that they (and their successors) will be willing and able to impose material losses on bank creditors and depositors in the event of a future failure, there can’t be any strong case for higher capital requirements (indeed, arguably a very credible OBR eliminates the basis for capital requirements at all). Even if officials and ministers aren’t 100 per cent sure about OBR, any material probability of it being able to be used in future crises needs to be weighed into the calculations when a proper cost-benefit assessment of proposals for higher capital requirements is being done. At present, there is little or sustained discussion of the OBR issues in the Issues Paper. I look forward to the inclusion of OBR considerations in a proper cost-benefit analysis if the Bank does end up proposing to raise capital ratios.

My other reason for unease is that in the Issues Paper the Reserve Bank does not engage at all with, for example, the past stress test results. There is nothing in the paper to suggest that current capital ratios don’t more than adequately cover risks. Instead, they fall back on generalised results from an offshore literature, and arguments about why New Zealand capital ratios should be higher than those abroad. Those simply fail to convince.

Here is the gist of their argument

One of the principles of the capital review is that the regulatory capital ratios of New Zealand banks should be seen as conservative relative to those of their international peers, to reflect New Zealand’s current reliance on bank-intermediated funding, New Zealand’s exposure to international shocks, the concentration of our banking sector, the concentration of banks’ portfolios, and a regulatory approach that puts less weight on active supervision and relatively more weight on high level safety buffers such as regulatory capital.

I’m not sure what weight should rest on that “be seen as” in the second line. I presume not that much, as these seem to be presented as arguments that would warrant genuinely higher capital ratios than in other countries, not just something about appearances. But in substance they don’t amount to much:

- “New Zealand’s current reliance on bank-intermediated funding”. I’m not quite sure what point they are trying to make here. Does the Reserve Bank regard bank-based intermediation as a bad thing? If so why? I presume the logic of the point is something about it being more important than in most places to avoid bank failures, but that simply isn’t made clear, or justifed with data. Payments systems – a big focus of Bank concern around the point of a bank failure – tend to be based through the banking system everywhere. It is not even as if our corporate bond market – while modestly-sized – is unusually small by international standards. (Incidentally, it is also worth noting that there appears to be nothing in the Issues Paper about non-banks, some of whom the Reserve Bank also regulates. Making bank-based intermediation relatively more expensive – which higher capital requirements could do – would tend to lead to disintermediation.)

- “New Zealand’s exposure to international shocks”. Again, it isn’t obvious what this point amounts to. Presumably the sorts of shocks New Zealand is exposed to are reflected in the scenarios used in the stress tests the Bank and others have run? And it isn’t obvious that New Zealand’s economy is more exposed to international shocks than many other advanced economies – there was nothing very unusual for example about our experience of the crisis of 2008/09. I suspect that lurking behind these words is some reference to the old bugbear, the relatively high level of net international indebtedness – a point the Bank and the IMF often like to make. But this simply isn’t an additional threat to the soundness of the financial system. Rollover risks can be real, but they aren’t primarily dealt with by capital requirements (but by liquidity requirements) and as we saw in 2008/09 the Reserve Bank can easily temporarily replace offshore liquidity. Funding cost shocks also aren’t a systemic threat because, with a floating exchange rate, the Reserve Bank is able to offset the effects through lowering the OCR and allowing the exchange rate to fall. The difference between a fixed exchange rate country and a floating exchange rate one, in which the bank system’s assets are all in local currency, seems to be glossed over too easily.

- “the concentration of our banking sector” Is this really much different from the situation in most smaller advanced economies (or even than Australia and Canada)?

- “the concentration of banks’ portfolios”. This seems a very questionable point. Banks’ exposure in New Zealand are largely to labour income (the largest component of GDP, and the most stable) – that is really what a housing loan portfolio is about – and to the export receipts of one of our largest export industries. That is very different from, say, being heavily exposed to property development loans, to financing corporate takeovers, or other flavours of the day. The effective diversification is very substantial, including the fact that in any scenario in which labour income is severely impaired (large increases in unemployment) it is all but certain the exchange rate will be falling (boosting dairy returns). The two biggest components of the banks’ books themselves thus provide additional diversification.

- “a regulatory approach that puts less weight on active supervision and relatively more weight on high level safety buffers such as regulatory capital.” Is the Reserve Bank really saying they believe that on-site supervision would produce better financial stability outcomes? I’m sceptical, but if they are saying that, surely the case would be strong to change the regulatory philosophy. It would, almost certainly, be cheaper than a large increase in capital requirements. At very least, if they want to rely on this argument, it would need to be carefully evaluated in any cost-benefit analysis.

It all leaves me a bit uneasy as to whether there is really the strong case for higher capital ratios that the Bank might like us to believe. They’ll need to provide much more robust analysis if they really choose to pursue such an option.

And a final thought. The Bank devotes some space in their Issues Paper to considering the role of convertible capital instruments – issued as debt but converting to equity under certain (more or less well-defined) adverse event circumstances. In doing so, they provide vital loss-absorbing capacity, providing a buffer for depositors and other non-equity creditors. There are some practical problems with these instruments – the Bank touches on many of them – and they probably shouldn’t be marketed to retail investors (at least without very explicit warnings) lest the pressures mount for holders of these instruments also be to bailed out in a crisis. Nonetheless, in the presence of the tax issues discussed earlier, convertible instruments look like a generally attractive option for supporting the robustness of banks in a cost-efficient way.

Given that I was interested in this paragraph on convertible instruments from the Bank.

In New Zealand there has been no conversion at all of Basel-compliant AT1 and Tier 2 instruments, because banks have not been in financial difficulty, so there is even less certainty about the practical effects of conversion in New Zealand’s particular legal and institutional environments. In the Reserve Bank’s view these instruments should be regarded as essentially untested in the New Zealand environment.

Of course, the same can be said for OBR, and indeed for almost all the crisis-management provisions of New Zealand bank supervisory legislation.

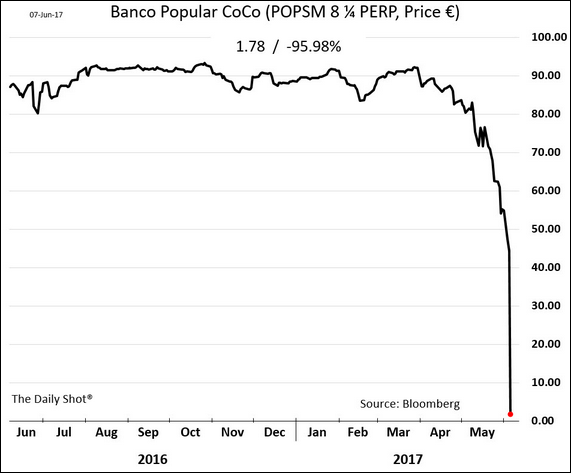

The Bank does draw attention to the risk of bailouts of holders of convertible capital (co-co) instruments. On the other hand, they can work when banks fail. Earlier this week, Banco Popular in Spain “failed”. It was taken over, for 1 euro, by Banco Santander, which will inject a lot of new equity into Popular. Popular had co-co instruments on issue. Here is what happened to the price of those bonds.

Banks can fail, banks should fail from time to time (as businesses in other sectors should), and when they do it should be clearly established who is likely to lose money. This looks like a good example, where the shareholders and the holders of the co-cos will have lost everything they had invested in these instruments.

To revert briefly to our own Reserve Bank’s review, perhaps there is a case for higher capital ratios. But, if they want to pursue that option, it isn’t likely to be cost-free, and any such proposal will need to be backed by a robust and detailed cost-benefit analysis. For now, it isn’t clear that the reasons they have suggested why capital ratios here should be higher than those in other advanced countries really stand up to scrutiny.

Hi Michael I was looking at some housing affordability videos yesterday and saw this one from July last year where John Key rejected reducing housing/infrastructure demand by reducing the immigration boom, instead he demanded/pleaded/begged the Reserve Bank to introduce loan to value ratios for investors.

Which the Reserve Bank duly complied with in its September announcement http://www.rbnz.govt.nz/news/2016/09/reserve-bank-confirms-nationwide–r…

I see over at Interest.co.nz that the Reserve Bank is considering more Macroprudential tools -debt to income limits. http://www.interest.co.nz/business/88195/rbnz-says-debt-income-restrictions-could-prevent-about-10000-borrowers-buying-house

I think it is interesting that in the 2000s to control inflation, a housing bubble and immigration boom the Reserve Bank ratcheted up interest rates to 10%? just before the GFC -which actually crashed the economy before the GFC really put the boot in.

Now in the 2010’s to control a housing bubble and a immigration boom the Reserve Bank is ratcheting up Macroprudential lending restrictions.

Surely what is needed is not Reserve Bank actions but for governments to stop abdicating their responsibilities and address the root causes of the problem -excess demand from immigration, foreign investment, speculation…. and unresponsive housing supply?

LikeLike

I don’t agree with every detail of your final sentence, but strongly agree with the general sentiment.

(I’ll offer some thoughts on the debt to income limits document in time, but suffice to say I think it is not necessary, quite possibly ultra vires, and really mostly about nanny-statism – to the extent it protects anyone it will be individuals from making their own choices, not the financial system)

LikeLike

Higher equity can mean a lower all in cost of capital if the starting point is excess leverage. Defining the latter for banks is inherently difficult given runnable liabilities but the crisis showed there was too little equity. So I think the push for higher equity – here and abroad – makes complete sense. Investors should realise higher equity means lower risk and, hence, lower returns i.e sliding down the MM II curve (from right to left) toward the minimum point…

LikeLike

I sympathise, but remember that required capital ratios have already been increased, and risk weights have also generally been increased materially. As I think i implied in the post, that shift seems likely to have been warranted – too much bailout risk was probably being priced in – but the marginal returns from material further increases in required capital must be smaller than from the first increase. The question of course is how large or how small.

LikeLike

Equity funding is hugely more expensive than debt funding.

The first issue is getting all the shareholders to agree to injecting more capital. If shareholders do not agree then the business has to shrink to cover the capital adequacy. Which shareholder is going to be happy with shrinking the business? Basically you are asking thousand of shareholders to stump up with more cash. How many people do you know will agree to coming out with more cash??

Perhaps issue more shares to new shareholders. But that means diluting control of existing shareholders and diluting dividend payments to the existing shareholders. Again not a happy proposition. The business has to pay out higher dividends percentages so that existing shareholders do not feel that they have lost out but loss of control is a big deal as well.

LikeLike

Higher capital adequacy just makes more cash available as working capital to the bank. The accounting entries are,

Dr Cash

Cr Capital

Therefore it is how the cash injected from additional capital is used that is the important part, not the amount of capital. Cash is lent out or invested.

If lent out to clients for a interest return

Dr Client Lending book

Cr Cash

Or if the cash is invested

Dr Investment Fund

Cr Cash

Therefore if there is a run on the bank on savings deposits or lost from poor investments or massive job losses causing a writedown of the Client Lending book, capital adequacy means nothing. Now the question becomes how much more micro managing does the Reserve bank want to do? Best to have a Chartered Accountant as the next Reserve Bank Governor. This bunch of economists definitely do not have a clue.

LikeLike

…..if current shareholders didn’t monitor management effectively such that the latter grew assets with debt funding and those assets proved less valuable than thought, fresh equity can be sold to new investors to repay debt – typically at a decent discount: old shareholders = sad face while new shareholders = happy face assuming the business is successfully restructured and dividends can resume e.g. UK householder rights issues during GFC – stonking returns for those that were new investors….

LikeLike

To me the macroprudential regs are prima facie evidence that bank capital is not high enough. Micromanaging the banks is nanny statish and encourages game playing.

Do we have a good estimate of the cost of higher bank capital? The estimates I have seen were not convincing.

LikeLike

Michael

The GFC put paid to the Efficient Market Hypothesis and the idea that the Invisible Hand can be relied on to preserve us all from bad bankers. However, its very questionable that central bankers rolling up their sleeves and managing the banks via all these new controls will do a better job than the bankers. “Better” meaning ensuring the ongoing provision of financial services on a cost and risk efficient basis.

It seems that a speculative frenzy in the USA and a dearth of lending standards in Europe has created some form of justification for a global extension of central bank controls.

Whether RBNZ is equipped for this expanded role is doubtful. It is not doubtful whether there is any justification for the expanded role… there isn’t. There is not any (zero) evidence that NZ’s banks have been badly managed since 1987. For 30 years they have done nothing to deserve the treatment now being meted out.

It is an appalling aspect of NZ’s lax approach to government encroachment. With no justification at all there is a huge expansion of government regulation, expropriation of all sorts of rights and value, and no cost/benefit analysis.

This is especially painful in the case of RBNZ due to their very modest accountability to anyone.

While you have railed at their lack of accountability for monetary policy and in a few other areas, the biggest over-reach is in their regulation of the banks.

NZ has very very poor protections of property rights (individual and corporate). This is just another example and already it means many people are earning less on their capital while others are being deprived of funding.

As for those who have responded before me by hazarding their views about appropriate levels of bank capital. Their opinions are based on absolutely no understanding of the facts and are a total diversion. What matters with bank regulation is whether the regulator has the skills, capabilities or values to somehow improve the lot of NZ borrowers and lenders. Of that there is no proof at all.

Tim

LikeLike

Couldn’t really disagree with any of that Tim. I’ve focused on the failures to hold the Bank to account over mon pol because there actually is clear statement of expectations written down. But as you suggest, in many respects the financial regulatory position is far worse, because there is no agreed standard for them to be held to, even if the Board, the FEC, the media were doing the job of attempting to hold them to account in this area.

LikeLike