The Conference Board’s Total Economy Database is my favourite source for cross-country comparisons of productivity growth. I’m not close enough to the respective methodologies to know whether and where to prefer their methodology to that of the OECD, but the Conference Board has data for a lot more countries, and typically has estimates that go back a bit further in history.

Yesterday, I dug out their estimates of total factor productivity (TFP) growth. They’ve recently revised their methodology, although for the time being that means they only currently go back 20 years. I was curious to see how New Zealand had performed, on this metric, relative to other advanced countries.

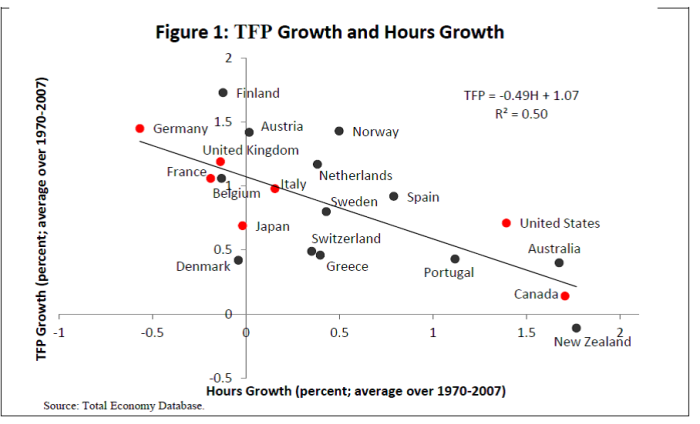

Some readers will recall this IMF chart which I’ve run a few times previously.

It uses an earlier vintage of Conference Board estimates, and on that basis, New Zealand had had the lowest TFP growth of any of these OECD countries for the full period 1970 to 2007.

How about the more recent period, since 1994? Here I’ve used a larger group of countries – all the OECD countries, all the EU countries, plus Singapore, Hong Kong, and Taiwan – very similar to the set of countries I used for a range of posts back in 2015 about New Zealand’s relative performance.

Over this period on this measure, we weren’t the worst, but we weren’t far off the worst. A lot of the former eastern-bloc countries, now given the opportunity to catch-up with the West, are bunched towards the left of the chart.

Over this period on this measure, we weren’t the worst, but we weren’t far off the worst. A lot of the former eastern-bloc countries, now given the opportunity to catch-up with the West, are bunched towards the left of the chart.

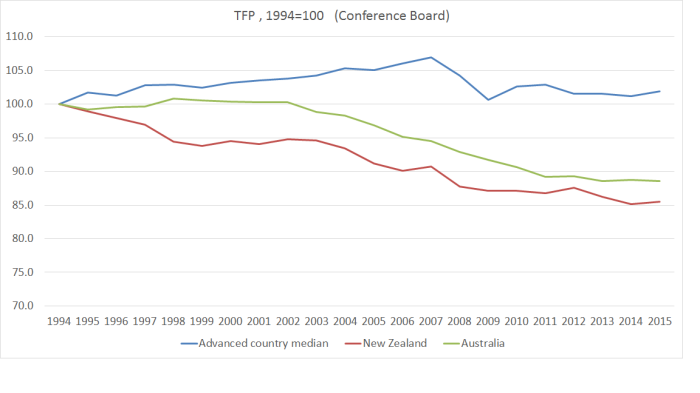

And here are New Zealand and Australia shown relative to the median of these advanced countries.

And New Zealand relative to the median of the G7 countries, and to the median of the former eastern-bloc countries. Recall, after all, that the narrative of economic reform in New Zealand had also been to allow us to catch up again with the richer advanced countries.

And New Zealand relative to the median of the G7 countries, and to the median of the former eastern-bloc countries. Recall, after all, that the narrative of economic reform in New Zealand had also been to allow us to catch up again with the richer advanced countries.

Not an altogether pretty picture.

Not an altogether pretty picture.

Of course, observant readers have probably noticed that there doesn’t seem to have been much TFP growth anywhere for the last decade or so, and that while New Zealand doesn’t look to have done particularly well during that period, we also don’t look much worse than usual. But here is how we have done relative to various other countries/sub-groups over that period.

Plenty of countries did worse than us, but among those that were quite similar to New Zealand and Australia over this period were Italy, Spain and Portugal (Greece was materially worse).

For these purposes, I’m mostly interested in how New Zealand has done relative to other countries. There is a reasonable question as to how the level of TFP can have fallen so badly in 20 years (almost 15 per cent in New Zealand if one believes this measure). TFP growth is a residual, after decomposing GDP growth into growth in the capital and labour stocks and – done properly – measuring both of those isn’t straightforward (eg it is one thing to measure total hours worked, another to get a good measure of the quality of the labour, or thus total human capital applied to production, especially in an era when tertiary education has become a lot more common). Different methodologies will produce different estimates, but so long as similar methodologies are applied for all countries we can still use the datasets for cross-country comparative purposes

All of which is a lead in to a perhaps slightly less discouraging picture for New Zealand. The OECD also produces TFP growth estimates, but for a much smaller range of countries – only 20 of their 34 member states, including none of the east European convergence economies. And there aren’t yet estimates for all the countries for 2015.

But here is the comparison for 1994 to 2014 between New Zealand and this sample of the really advanced OECD countries.

The gap between New Zealand’s cumulative TFP growth and that of the other advanced economies isn’t as large as that shown on the Conference Board data (second chart above). Then again, since the OECD data doesn’t include the catching-up eastern Europeans that shouldn’t be a surprise. But what is more striking is that until 2003 we were more or less matching the other OECD countries in this sample.

The gap between New Zealand’s cumulative TFP growth and that of the other advanced economies isn’t as large as that shown on the Conference Board data (second chart above). Then again, since the OECD data doesn’t include the catching-up eastern Europeans that shouldn’t be a surprise. But what is more striking is that until 2003 we were more or less matching the other OECD countries in this sample.

Here, for comparison, is the Conference Board data for New Zealand and the OECD’s sample of (20) countries.

In the end, perhaps the pictures aren’t really that dissimilar after all. We’ve done badly relative to other traditional advanced countries and, if anything, on this measure too, the last decade or so is looking relatively worse. In other words, if there was some convergence of growth rates, it looks to have been mostly only because TFP growth in the east European countries (in the TED sample but not in the OECD’s) slowed up so very markedly (as you can see in the third chart above). That might be unfortunate for them – and some combination of policy limitations, and substantial convergence already having occurred in some countries – but doesn’t put New Zealand’s underperformance in any better light.

In the end, perhaps the pictures aren’t really that dissimilar after all. We’ve done badly relative to other traditional advanced countries and, if anything, on this measure too, the last decade or so is looking relatively worse. In other words, if there was some convergence of growth rates, it looks to have been mostly only because TFP growth in the east European countries (in the TED sample but not in the OECD’s) slowed up so very markedly (as you can see in the third chart above). That might be unfortunate for them – and some combination of policy limitations, and substantial convergence already having occurred in some countries – but doesn’t put New Zealand’s underperformance in any better light.

It is the sort of underperformance that should be leading to hard questions about the overall direction of economic policy in New Zealand. After all, if TFP growth isn’t everything about economic performance and sustained prospects for prosperity, it is typically seen as quite a large part of the picture. And we’ve just kept on doing badly.

That 2003 divergence interested me, so I had a quick at what the Labour Government was doing at the time;

https://en.wikipedia.org/wiki/Fifth_Labour_Government_of_New_Zealand

Nothing particular struck me in that.

So I had a look at what dairy prices were doing at the time;

https://www.interest.co.nz/charts/commodities/dairy-prices

Couldn’t spot anything outstanding in that.

So I had a look at productivity stats here;

https://www.interest.co.nz/charts/economy/productivity

Which is sub-grouped under Labour and Capital – and if you have a look at capital, you can see a substantial decline starting around 2003, with a further marked slide down in 2008.

Then I looked at their median house price growth – and although 2003 is at the extreme margin of their series – we can see the peak around that time and then the slide down to the bottom in 2008.

LikeLike

Sorry, here’s the link to the median house price growth series;

https://www.interest.co.nz/charts/real-estate/median-house-price-growth

LikeLike

My story tends to emphasise (whatever was responsible for) the rise in the exchange rate around that time that has never sustainably been reversed. No doubt the population pressures on a supply-constrained housing market were part of an underlying common story (and 2003 was the year with the largest total net migration inflow – absolute and share of the population – we’ve seen for many decades). The terms of trade started to rise at about the same time, and that is probably also some part of the story (terms of trade increases make us better off, but aren’t always good for productivity growth).

LikeLike

Thanks Michael, interesting. Of course the TOP party is running the argument about a misallocation of capital toward unproductive uses – hence the reason I went to housing for a look. Very interesting about 2003 and the net migration inflow as well.

LikeLike

Always worth remembering when thinking about that TOP line that we almost certainly have too few houses (for the number of people we have) not too many. Land is ridiculously expensive of course – interaction of regulation and population – but overpriced land doesn’t involve material reallocation of resources (except discouraging building).

LikeLike

International student numbers leaped from 79k in 2001 to 127k in 2002 and held at 117k in 2003, dropped to 91k in 2007 and subsequently rising to currently around 115k spending $4.5 billion in the local economy each year.

LikeLike

However, from 2003 onwards, Aucklands share of the international student market has been escalating each year.

LikeLike

Also don’t forget that tourist numbers have been consistently moving upwards each year from 2.0million visitors in 2003 to 3.5million visitors in 2016

LikeLike

Correction; 125,000 international students in 2015 with 50% coming into Auckland.

Click to access 2045-ENZ-SnapShot-Full-Year-Report-VISUAL.pdf

LikeLike

I think the role of the competition regulators is incredibly important; we could be doing more on this front.

That’s in addition to the other changes you’ve recommended which go to increase the external-facing, competitive parts of the economy.

LikeLike

The problem with productivity poverty and the lack of public interest is that most of us actually feel really good about the current economic climate. Plenty of jobs paying pretty good wages with inflation and interest rates low, business activity and confidence is high. House values are high and those that have sold have moved out into provincial towns living a dream life with mortgages all paid up and cash in the bank waiting for future opportunities.

Bluff Oysters have also hit the Auckland restaurant menu and of course its also time for that 3 hour lunch downing those delicious Bluff Oysters

LikeLike

I suspect that is a particularly middle-aged middle class perspective (which is not intended to be derogatory – it describes me too). For younger people, or even those worried about their kids, unaffordable housing remains a big issue.

But, of course, it is hard to see/feel these productivity gaps emerging. They do so over time, and our living standards have corroded ever so gradually relative to those on offer in other countries over the last 60 years. And no doubt even in troubled countries many people continue to enjoy a very good life. We could just do so much better here.

LikeLike

My old man reckoned by the time you hit 50 you started to (re)question what life is all about with ‘working smarter not harder’ somewhat down the list: perhaps another way in which slow moving demographic trends are starting to take effect…..

LikeLike

So how do we fix it?!

LikeLike

Clearly, the technological frontiers are space and robotics. The aging baby boomers will need bio engineering, replacement parts, 3D printing body parts, food products, spare parts and food security. Perhaps insect protein to replace livestock protein.

LikeLike

Production of US$35,000 Tesla Model 3 Starts July 2017. Production of 50,000 – 85,000 units this side of Christmas is on the cards. Next year Tesla is planning on production of 500,000 Model 3′s per annum.

The news from Tesla gets better with three more Gigafactories, in Europe, Asia and another in the US planned.

https://ecotricity.co.nz/quad-copters-2017/

Too bad we did not get one of these Giga factories. Sure would have boosted our productivity. These factories are afterall fully autonomous and there is no minimal labour component and could have been build anywhere. But there is no way that Our restrictive planning and Auckland 2040 or the Character & heritage societies would have allowed for such a build anywhere in NZ.

LikeLike

Michael

The Penn World Table 9.0 for TFP measures relative to the US (US=1) from the 1950. New Zealand’s average was 0.77 of the US and Australia was 0.82 of the US on average.

The Conference Board computes the growth rate of TFP differently from the PWT. They estimate a Tornqvist index. PWT is probably use residuals from a Cobb-Douglas production function. The stock of capital in these data sets is different from SNZ data. So TFP could be anything and without a “theory,” it remains a slippery concept and a regression residuals at best.

Re competition, there is a conflict between “competition” and “growth.” OECD likes to say that there is empirical support for the hypothesis that competition causes growth. But growth in the most empirically tested (2nd generation) endogenous growth models requires the assumption that the firm is a monopolist. Without this assumption there would be no growth. This is basically a Schumpeterian world, whereby the growth in the R&D sector causes economic growth. R&D is costly so firms charge higher prices than under perfect perfect competition. In my work with Steve Stillman and Rob Johnson in Applied Economics we tested for R&D spillover in NZ over 40 years and found nothing. Our R&D sector is relatively weak. So we will have no productivity growth, but we will be happy when we have a positive terms of trade shock, i.e., a rise in the price of milk.

LikeLike

Thanks Weshah

I stayed away from levels comparisons, just looking at cumulative growth rates over a couple of decades. The PWT numbers/model are a key resource if trying to look at levels comparisons for TFP, but I’ve always tended – perhaps wrongly – to be a bit sceptical: there is enough uncertainty around the different TFP methodologies anyway, and then the PPP exchange rates issue is added into the mix. Focusing on growth comparisons allows one to stay with real national currency data.

LikeLike

Which rather begs the question as to why and what to do about it… I recall the Productivity Commission doing a series on this issue a couple of years back… any thoughts on what came out of that? Good? Bad? Indifferent??

We know the productivity performance of NZ has been a bit shit… but we know that. So what to do?

LikeLike

Here was my post on the Productivity Commission’s narrative/prescription from late last year https://croakingcassandra.com/2016/11/30/the-productivity-commissions-story/, which also includes a link to an earlier post of mine with some discussion of ideas for change.

There are lots of things that could/should be done, but I’ve become increasingly convinced that a sharp and permanent cut to our non-citizen immigration target would be the biggest and easiest change that would have a large positive payoff. I’d also be cutting taxes on business/capital income. Beyond that, there is lots of regulatory simplification that should be possible, including in the land use area.

When we stop growing the population so rapidly – perhaps even just match the developed country average for a few decades – we’ll see a lot lower real exchnge rate, and outward-looking firms more willing to invest in opportunities here, rather than progressively skewing the economy towards the non-tradables sector. However efficient those sectors might be – and it is difficult for them to be super-efficient here, on a fairly small scale – a big part of any economy’s catch-up/convergence – is that successful market-led growth in the tradables sector.

Incidentally, you make the point that we know productivity performance has been bad. Actually, our politicians and senior govt officials seem to like to pretend otherwise, so I like to repeat posts like that every so often. This one, in particular, is partly laying the ground for my next post on the NZI immigration report and the claimed gains from immigration, often said to come thru TFP channels.

LikeLike

Cutting immigration just makes the statistics look better but it does not change the fact that our industries are low productivity industries. Tourism requires feeding and requires accomodation. Cut immigration and you cut your ability to service this industry. Chefs top our list of skilled labour. The reality is foreign chefs need foreign food and foreign language speakers. That industry drives the need for more foreign chefs, more waiters, prostitutes, baggage handlers and cleaners. Service demands more people that are prepared to take their time.

10 million cows to generate $10 billion in export GDP which is extremely unproductive. 1.5 million people in Auckland generate $75 billion in GDP. People are infinitely more productive than cows. Government just needs to switch people to more productive type activities.

LikeLike

Correction: foreign tourists need foreign food which drives the need for foreign chefs. Service requires foreign waiters that speak foreign languages.

LikeLike

It is unlikely we willl see a lower NZD. Not when tourism continues to boom. Target this year is 4 million tourists and subsequently 7 million. If we take into account the 115,000 international students, there is an annual demand of $20 billion of new money that demands NZD at retail rates at different peak cycles. International students will demand NZD around 3 months in a year which boosts the NZD from Jan, Feb, Mar. Tourists will boost the NZD at differing peak holiday cycles. This is a massive external injection of $20 billion of funds into the local economy and largely focused in one city.

LikeLike

Correction: 125,000 international students in 2015 an increase of 14% over the previous year.

LikeLike

Michael

As Robert Gordon’s The Rise and fall of American Growth clearly shows, US productivity has flat lined since about 2004. He identifies many inputs to this decline, most of which are relevant to New Zealand. It would be pretty easy to just assume this is the new normal.

A couple illustrations of waste which look hard to budge are burgeoning health costs (according to World Bank figures NZ’s health spend is now 11% of GDP having risen from 8.4% over the last decade. A faster rate of growth than even the USA where health spending has risen from 15% to 17% of GDP. Theirs is probably even more wasteful than ours as at least NZ can point to increasing life expectancy), lousy rules around house construction which raise building costs, rising safety and security costs (did you know that safety and security measures at Wellington Airport are now cost more than airport charges), and the increase in the prison population by about 2,000 people over the last decade (a new cell costs $1m). I presume that one ray of sunshine for NZ is the falling government spending as a percentage of GDP (I couldn’t find the stats but I think NZ has now fallen behind Australia)

But a question for you. If productivity is flat lining, presumably that feeds through to the capacity for non-inflationary economic growth. Recent analysis of the USA indicates a potential rate of non-inflationary growth of a bit under 2%pa. I guess that our population growth and better demographics give us a slightly higher potential rate. But we must be at or past that rate now.

Yet you are an advocate for RBNZ to lower interest rates. Don’t you feel that RBNZ should now be hauling in demand a little? Especially in the context of rising US rates and the consequent fall in the NZ$.

Tim

LikeLike

Tim,

Agree with most of your list of concerns, and actually govt spending as a share of GDP in NZ is still about 4 percentage points higher than in Australia – using the OECD general government series to include all levels of govt..

Re NZ, recall that we have had population growth of around 2% per annum recently, and rising labour force participation as well so for now the non-inflationary rate of growth could be around 3 per cent, even with v little underlying productivity growth. Actual growth has been a bit above that recently, and presumably partly as a result inflation (core) appears to have stopped falling and even picked up a little. I’d not favour an OCR increase at present – altho don’t favour more cuts – because the unemployment rate is still above the NAIRU, probably by quite a margin, and core infaltion is still well below target. If growth continues at the current pace, some gradual tightening might be warranted next year, altho on that note I saw Westpac out this morning picking only 0.5% growth for the March quarter. We’ve had 2 false starts with mon pol since 2009, and I don’t think it would be in anyone’s interests for there to be a third – i’d rather we had the comfort of actually seeing core inflation at or very near target (especially when Labour is looking at revising the mandate anyway.

LikeLike

The Warehouse Group reported a 76% drop in first-half profit after the retailer took an impairment charge against its financial services unit, taking into account restructuring costs and lower earnings from red shed stores.

Profit fell $13.6 million from $57.2 million a year earlier.

The result included a $22.7 million write down against the Financial Service Group and restructuring costs of about $4 million. Adjusted profit fell about 13% to $39.7 million, within the guidance range of $38.5-41 million it gave in December.

https://www.nbr.co.nz/article/warehouse-first-half-profit-drops-76-financial-services-impairment-weaker-red-shed-earnings

Looks like inflation is not going anywhere too fast. The Warehouse is anticipating more online competition from Online stores like Amazon.

LikeLike

How do we fix it? The only robust and reliable evidence for higher productivity is for R&D sector.We don’t have it.

LikeLike