Yesterday’s Q&A discussions on immigration seem to have attracted quite a bit of coverage.

Of course, most of that focused on the comments made by Winston Peters, and I don’t have anything much to say about those except to note two things.

First, I was interested to hear him talk of targeting 7000 to 15000 annual migrants, which was quite similar to my suggested target for residence approvals of perhaps 10000 to 15000 per annum. The United States issues around 1 million green cards a year, and as the US had about 70 times our population that is about the same rate of per capita immigration as would be implied by my 10000 to 15000 annual range. It isn’t a level that amounts to shutting the door.

Second, Peters has twice before been a senior minister and has never made the rate of permanent immigration a central issue in negotiations to form a government. Perhaps this time will be different.

Of my comments, most of the coverage has been around the suggestion that if the residence approvals target was cut as I suggested, house prices might be 25 per cent lower in a couple of years. It wasn’t intended as a precise estimate, more an indication that population growth (and especially unexpected changes) make a material difference to house prices in markets where the supply response to impaired by the thicket of land use and building regulations. However, it is quite a plausible estimate, consistent with some past empirical research on the link between population change and New Zealand house prices.

A decade ago, Coleman and Landon-Lane, in work done at the Reserve Bank, estimated that a 1 per cent shock to the population would shift house prices by 10 per cent, and more recently Chris McDonald’s Reserve Bank work produced not-dissimilar estimates (especially for non New Zealand migrants). Adopting my proposal to cut the residence target by 35000 per annum would, all else equal, lower the population by 1.5 per cent in the first two years. But, more importantly, it would materially lower the expected future population, and asset markets (such as the urban land market) work on the basis of expectations. Over a decade, again all else equal, the population would be around 7.5 per cent lower on my proposed policy than on current policy. All else equal, urban land prices would be much lower. Of course, all else is never equal, and with less population pressure some of the pressure to liberalise housing supply would dissipate. But the direction of the effect on house prices is pretty clear, and the magnitude would almost certainly be quite large.

Perhaps one thing that disappointed me a little about yesterday’s programme was that discussion tended to focus on the immediate cyclical pressures, and especially those on Auckland house prices. I guess those issues are most immediately salient, especially in Auckland, and perhaps most easily accessible to a lay audience. My own arguments have tried to focus (a) not on the cycles in net migration, much of which are about New Zealanders coming and going, but on the trend target level of residence approvals, and (b) on the impact of New Zealand’s disappointing overall economic performance (ie the continued trend decline, over many decades, in our relative productivity). We could fix up the land supply market – and should – and many of those questions and issues would, almost certainly, remain outstanding. That said, when the advocates of the current policy can show so little evidence suggesting real economic gains to New Zealanders (as a whole) from our really large scale immigration policy (repeat, policy – the target level of residence approvals) then the appalling house price situation cries out for winding back the level of migration approvals, as one way of mitigating the adverse effects of the land use restrictions. One could envisage an alternative world in which the real economic benefits of large scale immigration were large, clear, and demonstrable, and yet the housing market was still severely dysfunctional. In that world, there would be some nasty potential tradeoffs if reform of land supply couldn’t be achieved. But we aren’t in that world. Here, it looks as though winding back migration approvals might well improve productivity prospects and improve housing affordability. There would, and will, always be cycles in net measured migration, but the policy component is relatively easy to adjust, and to maintain at a different target level (lower or higher) than we’ve had for the past 15 years.

I was pleasantly surprised at the moderate and reasoned approach the Q&A panel took to the immigration segment. They recognized that there are some real issues that need rational and thoughtful debate. Nonetheless, they all still seemed in the thrall of the idea that “skill shortages mean we need migration, just perhaps a “better quality” of migrant”. There are really just two points that need to be made in response. The first is that empirical research suggests – and historical casual empiricism does too – that an influx of migrants adds more to demand rather than to supply in the short-term. People who live in a modern economy need lots of real physical capital, and it doesn’t build itself. So although an individual migrant might ease an individual employer’s problem, in aggregate high immigration simply further exacerbates any existing excess demand for labour (skilled or not). Economists have recognized that for decades. It doesn’t, of itself, make immigration a bad thing – long term gains might still make it worthwhile – but immigration isn’t a way of dealing with systematic skill shortages. By contrast, a flexible domestic labour market is quite a good way: changing wage rates should signal difficulties in attracting people to particular roles/regions. It doesn’t work overnight, and it doesn’t work in aggregate if the economy is overheating, but it works when given the chance.

The panellists also seemed taken with the idea that more should be done to get more of the migrants who do come to go to regions other than Auckland. That seems, at least in part, to reflect a sense that something is wrong about things in Auckland (whether short term or long term) and perhaps a sense that a more successful New Zealand is likely to be one less strongly skewed away from the regions. But it risks leading to even more wrongheaded policies. We’ve already seen that last year, when the government amended the rules to give additional bonus points to people with job offers in the regions. Unfortunately that has the effect of lowering the average quality of the migrants who get in. The residence approvals target is largely fixed, and the changes in the scheme rewards those who can get to particular locations, not either (a) the most highly-skilled migrants, or (b) the most rewarding and productive New Zealand jobs. Auckland’s economic performance has been quite disappointing, suggesting it isn’t a natural place to funnel ever more people into. But that doesn’t suggest that the solution is to funnel more people to other places instead. It suggests focusing on the whole economy – in particular, getting the real exchange rate sustainably down – and letting a rather smaller number of total permanent migrants locate where the jobs and rewards are best. In that sort of world, Auckland’s population might be materially smaller than it would be on current policy, but the population of the regions might not be much larger. But the share of the regions in overall economic activity would be larger than it is now. Better to cut the overall residence approvals target, and focus in on a modest number of really highly-skilled people. The regions aren’t short of people, but Auckland seems to be awash in them (relative to the high-returning opportunities that seem to exist in Auckland).

As a final observation on the Q&A discussion, I was interested in Andrew Little’s response to questions about immigration. He continues to toy with the idea of some sort of short-term cap on migration. I don’t think that is particularly sensible or meaningful. No one can accurately forecast short-term fluctuations in net migration (ie the combination of New Zealanders and foreigners) and if those fluctuations can’t be forecast, one can’t run meaningful short-term caps. In the nature of things, and well-intentioned as they might be, they would simply risk exacerbating the short-term cycles in net migration: pull back approvals when net migration was at a cyclical peak, and by the time those changes took effect, often enough the natural cycle would have turned down anyway. And vice versa when net migration is at a trough. We are much better to run a stable and predictable programme of residence approvals, and live with the natural variation that results mostly from New Zealanders coming and going. In my view, the target level of approvals should be lowered quite substantially, but wherever it is set it shouldn’t be messed around with – up or down – in response to short-term cyclical pressures.

But my concern about Little’s comments was more about the underlying message. Twice in the space of thirty seconds, he repeated the line that “New Zealand has always been a country dependent on bringing in skills from abroad”, stressing that he would never want to change that. It is simply a mistaken model of growth. The prosperity of any country depends primarily on some combination of the natural resources it has and, most importantly, on the skills and talents of its own people, and the institutions (political and economic) that those people nurture. That was true of the United Kingdom or Holland centuries ago, it was true of the United States century or more ago, it was true of twentieth century New Zealand, and it is true of every advanced successful country today. Of course, every country draws on ideas and technologies developed in other countries. In some cases,. immigration may even have helped the recipient country a bit – but any such gains look to be quite small – but prosperity depends mostly on a country’s own people and own institutions. The line Little is running is certainly consistent with the implicit stance of the New Zealand elite, across the main parties, but there is little or no empirical foundation for it. Indeed, it risks sounding like a cargo-cult mentality – waiting for just the right people from over the water to come and bring us prosperity. Things simply don’t work like that. It is a shame that our political leaders aren’t willing to put more faith in the skills, talents, and energies of our own people and firms, rather than (so it seems) wanting to “trade us in” for some better group of people. Countries don’t get successful by bringing in better people: rather, successful countries can afford to bring in more people, if they choose.

In this morning’s Herald, the other key prominent academic in the liberally-funded (by MBIE) CaDDANZ project, Professor Paul Spoonley of Massey, has an op-ed championing the current immigration policy. It probably warrants a post of its own, but his bottom line seemed to be “keep the faith”.

Spoonley starts with this:

The International Labour Organisation estimates a 1 per cent increase in population expands GDP by between 1.25 and 1.50 per cent.

I’m not sure the source of this estimate, but it is a huge effect. Stop and think about what it means for New Zealand, if it were true over the medium-term. We’ve had one of the fastest population growth rates in the OECD in recent decades, and yet one of the worst productivity growth performances. So perhaps the really rapid migration-fuelled population growth has been really really good for us, and everyone else has gone really really badly, to explain our overall disappointing performance. But where is evidence – the telling statistics that suggest that that is really what has gone on? Professor Spoonley knows about the disappointing New Zealand economic performance, so it is a shame that he didn’t try to relate his general claim to the specific experience of New Zealand.

Spoonley then argues

Auckland gains from the effects of agglomeration. Population growth and immigration is associated with economic growth and diversity. For example, Auckland and Canterbury between them accounted for almost all the new jobs growth in New Zealand last year.

Immigration is key to this as skilled immigrants add to the human talent pool that is available to employers. They also establish new businesses and contribute to demand, including for education. Regions and cities that are not attracting immigrants are losing out on this current windfall.

It is fine theory. It just bears no relationship to the experience of New Zealand, and Auckland in particular, in recent decades.

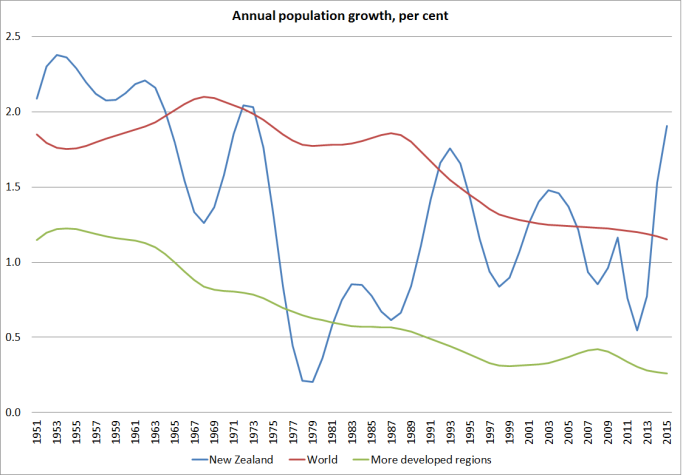

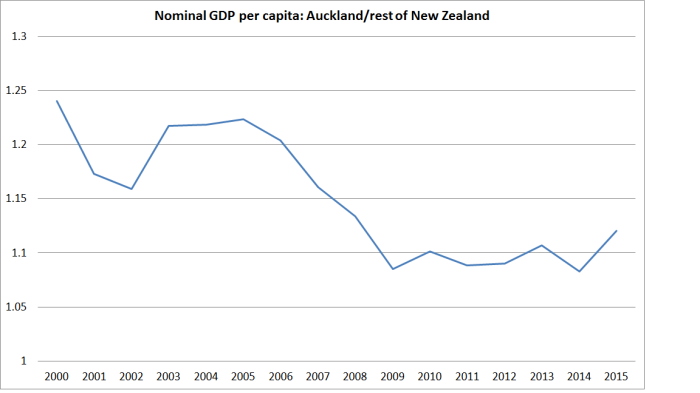

I’ve shown this chart before

No one disputes – Spoonley doesn’t – that Auckland’s population growth is largely migrant-driven. And yet Auckland’s per capita GDP has been trending down relative to the rest of the country’s over 15 years. And the margin of Auckland’s GDP over that of the rest of New Zealand was already low relative to what we see in most other advanced economies.

Perhaps Professor Spoonley and the other New Zealand pro-immigration advocates (many of them taxpayer funded) are right about the benefits to New Zealanders of this really large scale intervention. But even if so, surely we deserve much more evidence of those benefits than we get when leading academics simply assert over again that, whatever the short-term stresses, the Think Big programme is really working out just fine?

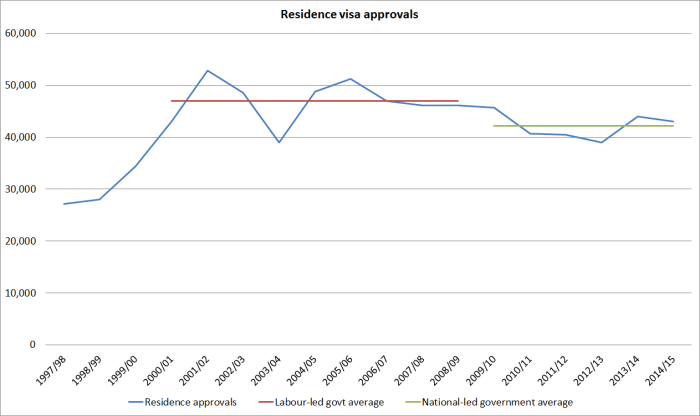

And to end a long post, just a simple chart. It shows residence approvals for each year since 1997/98.

The data are only available annually, but they are hard data on the number of people MBIE has given residence visas to. This isn’t SNZ arrivals and departures data, it is the policy core of the immigration programme – aiming at 45000 to 50000 approvals per annum. One of my commenters keeps trying to distract from this issue by citing PLT data. Those data are often interesting and useful (and in other ways quite limited) for various other analytical purposes, but if we want to think about the implications of the annual flow of residence approvals this is where the focus should be. Annual approvals under this programme are not very cyclical, and haven’t varied much across the last two governments. They are simply very high by international standard (per capita) – three times the US level. And on the (lack of) evidence to date of economic benefit to New Zealanders, the annual target should be wound back quite considerably.