What to say about the Reserve Bank’s latest Monetary Policy Statement?

Having just reread my comments on the September MPS, I could simply run most of those comments again.

The Bank’s stance doesn’t really surprise me very much, but it is disappointing to say the very least. New Zealand is being particularly poorly served by its central bank at the moment.

At least they cut the OCR. Some had doubted it would happen, but the Bank has now belatedly completed the reversal of the totally unnecessary tightening cycle the Governor and his advisers initiated last year. Even now, however, since inflation expectations have been falling, the real OCR is still higher than it was at the start of last year. Over the intervening period, core inflation has stayed well below the midpoint target, and headline inflation has been at or below the bottom of the target range for most of the period. The unemployment rate has risen, and per capita income growth has slowed markedly. Somewhat surprisingly, there was not a single question at the press conference about that succession of misjudgements.

I was also a bit surprised that the word “unemployment” did not crop up at all in the press conference. The structural unemployment rate is influenced by various structural features of the economy (labour market regulation, demographics, the welfare system etc), but no one really doubts that monetary policy choices affect the short-term fluctuations in unemployment. When the unemployment rate is above any reasonable estimate of the NAIRU, has been rising, and is forecast to continue to stay high, hard questions should be being asked of the central bank Governor. They weren’t. The Governor tells us that he is content not to have inflation back to the midpoint of the target range for another two years. But there will an output and unemployment cost to that choice. And a choice it is: the Governor probably can’t do much about inflation in the next couple of quarters, but a lower OCR over the next few quarters would, on the Bank’s own numbers, have got inflation back to target sooner. But the Governor tells us that, as things appear to him at present, there are no more OCR cuts to come.

On its own numbers (I’ll come back to criticisms of those numbers shortly), the Bank defends its choice by arguing that

with inflation expected to increase steadily, consistent with the inflation target, a much sharper adjustment in interest rates than projected risks being inconsistent with clause 4b of the PTA

Clause 4b reads

In pursuing its price stability objective, the Bank shall implement monetary policy in a sustainable, consistent and transparent manner, have regard to the efficiency and soundness of the financial system, and seek to avoid unnecessary instability in output, interest rates and the exchange rate.

The Bank does not explain how it thinks a more aggressive approach to easing monetary policy would be inconsistent with clause 4b (and no one asked).

Perhaps it is interest rates they are worried about? But the OCR has been between 2.5 per cent and 3.5 per cent since early 2009. If they were to cut the OCR to, say, 1.75 per cent, the worst that could happen might be that in 12 or 18 months time they might need to raise interest rates again, probably into that 2.5 to 3.5 per cent range. That doesn’t seem like particularly substantial variability by any historical standards.

Occasionally the Governor talks about avoiding output variability. I’m pretty sure the authors of that phrase in the PTA mainly had in mind avoiding unnecessary recessions, but even if we grant that growth could be too strong in some circumstances, it doesn’t seem like a relevant story right now. After all, on their numbers (Table 2:1) they think per capita GDP growth has been zero this year. They forecast that growth will pick up, and they have overall GDP growth peaking at about 3.5 per cent in 2017. Even with slower population growth that isn’t a troublingly high per capita growth rate. In past cycles, we’ve typically had a year or two of 4 or 5 per cent or higher GDP growth. Partly as a result of a succession of Reserve Bank misjudgments, we haven’t had anything like in the years since 2009. If anything, it is what we need now to reabsorb into work the high (and rising) number of people who are unemployed.

More likely, it is the not-very-meaningful statutory provision “have regard to the efficiency and soundness of the financial system” that the Governor has in mind. If so, he should be more upfront in making his case, and in identifying the tradeoffs involved in holding up interest rates to influence house prices and possible financial stability risks. The Governor did note that cutting interest rates further would raise the housing risks. But the Bank has other tools at its disposal to safeguard the soundness of the financial system, even if there were convincing evidence that that soundness was being threatened. Using monetary policy to try to manage the possible risks around a relative asset price change is a recipe for putting the rest of the economy through the wringer. The Governor’s monetary policy target is 2 per cent CPI inflation. The Reserve Bank is continuing to making the same mistake Sweden’s Riksbank made.

Perhaps relatedly, Assistant Governor John McDermott responded to a journalist’s question by arguing that “very very low interest rates increase the risks in the economy”. It is quite disconcerting to hear the Reserve Bank signing up to this BIS line – with no supporting analysis. And we should be wary of this “very very low interest rates “ line when the OCR today is sitting exactly at the level it has most often been at for the last six and half years (a bit higher in real terms). Like the Governor’s constant claim that global monetary policy is very stimulatory, it depends on assumptions about neutral interest rates that the data increasingly don’t seem to support. The Bank seems driven by a mental model that is deeply uncomfortable with a 2.5 per cent OCR, rather than by the data – low inflation, weak per capita growth, rising unemployment, and weak commodity prices.

But are the Bank’s own numbers even plausible? I don’t think so. They are projecting a material increase in GDP growth rates over the next couple of years, but it isn’t remotely clear what that optimism is based on. The Canterbury repair and rebuild process will be gradually tailing off over that period, some recovery in dairy prices is probably already factored into producer expectations and behaviour, and the rate of immigration is expected to fall away quite materially. Population growth in 2017 is more likely to be 1 per cent than 2 per cent. Even the Bank believes that the unexpectedly high rate of population growth has boosted GDP over the last couple of years. So what will counter the impact of a material slowing in the rate of population growth? It can’t really be the rest of the world’s economy. The Governor rightly sounds a bit worried about the risks in China – although the Bank seems blithely indifferent to the global deflationary shocks that China is representing – and there is nothing in the rest of rest of the world to suggest any material acceleration of growth next year. For what it is worth, global energy and metals commodity prices are continuing to fall – and while the direct effect of those falls might be modestly positive for New Zealand, they are only mitigating the impact of the weakening global environment.

Of course, forecasting is a mug’s game – which is why monetary policy probably shouldn’t be driven off medium-term forecasts of things we (and they) know almost nothing about). So it isn’t impossible that the Bank’s growth and inflation forecasts could come to pass. But what they’ve given us today is not a convincing story as to how this acceleration is going to happen. After all, their interest rate projections are no lower than those in September, and as the Governor noted the exchange rate has risen since then. It rose further this morning.

There were a number of other odd dimensions to the document and the Governor’s comments.

Once again, the prime policy discussion (chapter 1) discussed headline inflation, but not core. We are supposed to take comfort from headline inflation perhaps getting above 1 per cent early next year – itself a weaker outlook than they’ve run previously – but they offered no reasoning at all for why we should expect core inflation to rise. And yet these are the lines they want the media to use.

In the press conference, the Governor bemoaned the fact that monetary policy decisions were always tricky because everyone in the country has a view (and this is inappropriate why? It is, after all, our economy, not the Governor’s). He then claimed that it was very hard to move inflation expectations up once they start falling, and that this was so because in highly indebted economies people were reluctant to take on more debt.

Perhaps the Governor has not noticed that inflation expectations in New Zealand have already been falling – on many measures they’ve never been lower, at least since the target midpoint was raised to 2 per cent. The Bank quotes some carefully selected measures that average 2 per cent to suggest there is no problem, but (a) those expectations have fallen a lot over the last couple of years, and (b) they carefully ignore the indicative information revealed in market prices. The gap between indexed long-term government bonds and conventional long-term government bonds is currently about 1.4 per cent. It isn’t a perfect measure by any means, but it is a price reflecting the choices and assessments by people putting real money at stake. That is not typically so in the survey measures the Bank chooses to emphasise, which are often heavily influenced by the echo chamber of local market economists and media.

Inflation is very low, inflation expectations have been falling, and the Bank argues that in this climate it is hard to get inflation expectations up again. So why not foreshadow more OCR cuts to come? After all, the Governor was again anguishing about the exchange rate being too high. Perhaps what holds him back is concern about housing, but then as the Governor told his questioner, he thinks people are reluctant to take on very much more debt. He can’t have it both ways. Even in New Zealand credit growth and housing market activity has been pretty subdued in the last couple of years, across the whole country, compared with what we saw in the mid 2000s.

The Governor was also asked whether the government should loosen fiscal policy. I assumed the questioner had in mind an increase in government spending which would stimulate demand and perhaps take some pressure off monetary policy. But oddly, the Governor came out with a suggestion that he thought a case could be made for more infrastructure spending, especially in Auckland. My initial reaction was that reasonable people could differ on the case for more infrastructure spending, but I wondered if the Governor of the Reserve Bank should really be opining on such matters. But I almost fell off my chair when he went on to explain that more infrastructure spending would increase capacity in Auckland and lower inflation pressures. Perhaps in the long run, but had it not occurred to the Governor that putting infrastructure in place represents a material net increase in demand over the years when it is being put in place?

Perhaps more importantly, I am also puzzled about the Bank’s stance on immigration, and the evidence base that lies behind it. The Governor is clearly at one with New Zealand elite opinion – he told the news conference that he thought high levels of immigration were “a good thing for New Zealand” and that he did not think there should be any immigration policy changes. Views differ on the long-term economic impact of immigration, and many certainly agree with him, but why was this a subject the Governor is commenting on at all? Historically, the Reserve Bank has been studiedly neutral on the long-term issue, and focused (rightly) on the short-term cyclical implications. Governors who use the platform they have been given to advocate their personal policy preferences in other areas risk further undermining support for the autonomy they enjoy in respect of monetary policy.

But even the Bank’s view on the cyclical impact of the recent high levels of immigration seems confused. In chapter one (the press release) they assert that high levels of immigration have reduced capacity pressures and contributed to a lowering of inflation (ie supply effects exceed demand effects). In chapter 5, they produce a scenario about the impact of immigration staying unexpectedly high over the next year or two. In that scenario they explicitly articulate what appears to be their latest new view, in which a change in immigration has no net short-term impact on capacity or inflation pressures (short-term demand effects are just matched by short-term supply effects). There is no analysis in support of any of this. And there is no engagement with their own past research, or with the consensus view of New Zealand macroeconomists going back decades that whatever the possible long-term gains from immigration, in the short-term the demand effects dominate the supply effects (which shouldn’t be surprising, since the per capita capital stock requirements of each new person are materially greater than one year’s labour supply). It was only two years ago that they published a research paper which showed these results.

Demand effects exceed supply effects in the short-run (of several years).

The Bank seems all over the place on these issues. Perhaps they have fresh new research on the issue, but they put out two new Analytical Notes this morning, and there was nothing on immigration. I have asked for copies of any analysis they have produced in support of their new view, including how it might relate to the 2013 research.

It isn’t impossible that the effects of a surprise influx of immigrants could be near zero. If, for example, that influx just reflected the weakness in Australia, our largest trading partner, we’d have losses in demand for our exports to Australia offsetting the positive demand effects of the change in the net migration flow to Australia. But that isn’t an argument the Bank is running. In fact, we have no idea what their arguments and evidence are. It simply isn’t good enough, for such a major cyclical variable.

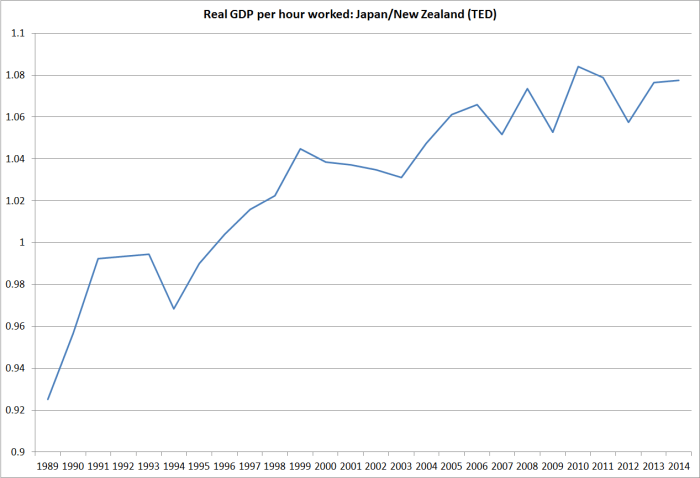

My overall take this morning was of an institution at sea. Even if their case is in fact strong, neither the Governor nor his Chief Economist seem convincingly able to make the case, despite all the resources at their disposal. The Chief Economist could not even effectively answer a simple question about why we wanted to get inflation up. He ended up falling back on line that we want to avoid becoming like Japan.

But, actually whether one starts from 1989 (the peak of the Japanese boom) or from 2007 (the peak of ours) Japanese productivity growth has somewhat outstripped that of New Zealand. And recall that one of the lessons of how the Japanese ended up with persistent deflation was that they kept monetary policy materially too tight for much of the 1990s. We might not have deflation yet, but persistently tight monetary policy – tighter than it needs to be – is only increasing our chances of ending up uncomfortably close to an undesirable deflation ourselves. It is all very well for the Governor to make the (accurate) point that no country has raised its inflation target since 2007. But in the sort of global climate we’ve now had for years, those who still can (countries that don’t have interest rates at zero) should be making full use of the scope to keep inflation and inflation expectations up.

“A bank adrift” is a good way of putting it. I watched a bit of the livestream Q&A, including the bit about infrastructure, and thought “was this really the best person we could find for the job?”. No mention of market based inflation forecasts at all. And apart from Bernard Hickey I didn’t hear a single interesting question from the journalists.

One question that might be asked is that, given the reaction of the NZD during the announcement, did the Governor actually just tighten monetary policy?

(If you see your ex-colleagues from the RB, tell them one of your commenters would be happy to step in as Governor after the current contract ends, and he guarantees to get market-based inflation expectations up to 2% within the first month, and give a decent press conference to boot, for half what they’re paying Wheeler.)

LikeLike

“He then claimed that it was very hard to move inflation expectations up once they start falling, and that this was so because in highly indebted economies people were reluctant to take on more debt” – hmmm: does that mean more debt is required to bring forward demand and shift those lethargic inflation expectations or, for now, are we stuck? Agree, perhaps he does need to be more honest if he is using the OCR to discourage borrowing – especially given the view that “…….low interest rates and rising house prices [could] combine to increase confidence and willingness to borrow for consumption”. And maybe the last bit is the problem: borrow to consume versus borrow for productive investment that generates demand for labour – where does NZ stand? Per the report, expectations for business investment appear relatively downbeat…!

LikeLike

Apart from the number of confusing contradictions in the Governor’s delivery I would be interested to know the demographics of the group the bank polls to gauge inflation expectations. I understand the bank believes these to be in the 2 to 3 percent for the medium term. As an old broken down farmer that has lived through 15 + % inflation, less than 1% inflation seems very low, I am more comfortable with 5% to 10% inflation ! I would be comfortable with the 2.5% as a natural level. When I talked to my son and his 30 year old friends they believe inflation will stay where it is or slightly decrease over the next year or so. They have only ever experienced inflation in the low single figures. Perhaps inflation expectations are very age dependent ?

LikeLike

The surveys they were citing yesterday put a high weight on the views of economists. One survey the RB pays for does survey a range of leading business people as well, and the ANZ monthly survey captures mostly small and medium businesses.

LikeLike

Thanks Michael – If I was being slightly flippant the results the bank uses do not necessarily bear any relationship to the “general public’s” expectations !

LikeLike

always an upward bias to general public and small business expectations of inflation

https://croakingcassandra.com/2015/12/01/weak-inflation-expectations-again/

of course, these are the numbers they tell pollsters, not necessarily what they act on if they ever (actively or implicitly) think about the inflation rate.

LikeLike