I urged again the other day that there should be an open process of research and debate leading towards the negotiation of the next Policy Targets Agreement in 2017. These documents matter. Monetary policy is the main tool for short-term macroeconomic stabilisation, so the PTA sets the “rule” (well, loose guide) for how the short-term fluctuations in the economy will be managed. The Reserve Bank – and the Treasury and Minister – has often had a tendency to treat deliberations around the PTA as technocratic in nature (which in some ways they are), and hence not something with which to trouble the natives. The standard Reserve Bank response to any suggestion of greater openness was “but we already tell them what we want them to know”. But open government is not just about releasing finished products, after the event, in bureaucratically-approved formats.

Two other former Reserve Bank staff, Kirdan Lees and Christina Leung, both now at NZIER, have made a useful contribution to a debate about the future of New Zealand’s monetary policy. They put out a note the other day headed Time to reassess inflation targeting, which concludes with a pretty strong leaning towards adopting nominal income targeting instead. I don’t think they will get far with the current Governor on that one – he used to bristle and react very frostily whenever anyone so much as mentioned nominal income targeting – but he won’t be Governor for ever, in the end the Minister of Finance calls the shots, and whether the Governor likes debate or not, it is an important part of good public policy processes.

However, I’m not convinced by the Lees/Leung argument. In particular, I’m not persuaded that the form of the rule makes a great deal of difference to assessing the appropriate stance of monetary policy now. Nor am I convinced it would have made a great deal of practical difference over the pre-recession years. And if we were going to move away from inflation targeting, I’m not convinced that nominal income targeting is the alternative I would adopt.

Lees/Leung have a number of strands to their argument.

First, they argue that “supply shocks” have become more important relative to “demand shocks”. Perhaps, but where is the evidence for that proposition in New Zealand or in other countries? They seem, in part, to be arguing from the presence of a number of phenomena (fracking, the internet etc) which are improving productivity. All of them are real, but in aggregate productivity growth has been materially slower in the last half dozen or so years than in the previous decade. And, in any case, the issue for monetary policy would not normally be the trend rate of productivity growth, but shocks – surprises, which can go either way. There is, of course, one area where supply shocks have become more important for New Zealand – terms of trade volatility has been much greater in the last decade than in the previous 15-20 years (apparently driven mostly by the fairly extreme dairy price volatility). We’ll come back to terms of trade shocks.

Second, they point out that many advanced countries have seen inflation undershoot respective targets. That is, of course, true, but most of the countries on their chart have largely exhausted the potential of conventional monetary policy. Interest rates are basically at zero, and have typically been so for quite a few years. There are reasonable arguments that a different target might make it a little easier to get out of the current “trap”, but they aren’t relevant to New Zealand at present. Our Reserve Bank has undershot the inflation target not because it couldn’t cut interest rates enough, but because it chose not to. That failure probably wasn’t wilful – largely it was because they misread the data. They (and other central banks) misread the data on the other side during the boom years. Forecasting is difficult, but it is a problem that bedevils any of the rules under discussion.

Third, they point out the well-known proposition that, in principle, nominal GDP targeting can generate better short-term macroeconomic performance (eg less output variability) in the presence of supply shocks. In the example they cite, faced with drought, an inflation targeting central bank will tend not to adjust policy (since inflation, and especially core inflation, won’t change much) while a nominal GDP targeting central bank will tend to ease policy to lean against the drought-induced fall in GDP. But, in fact, whichever rule was adopted, the central bank would almost certainly be reacting to forecasts (whether of inflation or nominal GDP), since monetary policy only works with a lag. Droughts typically aren’t recognised by central banks until we are in the midst of them, and when they are recognised they are typically assumed to be shortlived. Faced with the prospect of a drought this summer, the Reserve Bank will typically (and reasonably) assume that next summer will be normal, and since monetary works with a lag they wouldn’t change policy under either regime.

Fourth, they argue that the difference between inflation targeting and nominal GDP targeting is quite material for where the OCR should be set right now. It is certainly feasible that in some circumstances there could be quite a difference, but they don’t make a persuasive case that this is one of those times.

They compare inflation rate targeting with nominal GDP level targeting. Either prices or nominal GDP can be targeted in rate of change terms (inflation rates) or in levels terms. No country in modern times has adopted levels targets for either prices or nominal GDP. The Bank of Canada looked quite carefully at the option of price level targeting a few years ago, and concluded that it would not represent an improvement over inflation targeting. One reason levels target don’t appeal to practical policymakers is that if one makes a mistake and prices or nominal GDP rise unexpectedly strongly, one can’t just treat bygones as bygones – one has to tighten to drive the level of prices (or nominal income) back down again. Whatever the theoretical appeal of such an approach, it seems unlikely to command much public enthusiasm or support – and hence seems unlikely to prove durable.

Much of the older literature around nominal GDP targeting was done in terms of rates of change (nominal GDP growth rates). But since the 2008/09 recession there has been renewed interest in the idea of a level target for nominal GDP. The argument made, most prominently by US economist Scott Sumner, has been that a target for the level of nominal GDP would have (a) prompted an earlier easing in monetary policy, and (b) would underpin expectations (especially in the US and Europe) that interest rates would stay low for a long time.

Lees/Leung acknowledge that the current inflation targeting framework invites further cuts in the OCR (we’ll see next week whether the Governor agrees, although recall that it is a forecast-based framework, so OCR cuts aren’t warranted if the Bank can convincingly show that core inflation is heading back to 2 per cent reasonably soon on current policy). But then they suggest that using nominal GDP levels targeting “interest rates are about right”.

They appear to base that observation on this “illustrative example”.

In this chart, they appear to have simply drawn a trend line through actual nominal GDP since 1998 and then calculated the difference between the trend line and actual. That difference is small.

But to adopt a nominal GDP levels target, one would need to define an appropriate trend period first. And it isn’t clear to me why this is the right one. Most advocates of nominal income targeting at present argue for using something like the pre-recession trend (since the arguments are about whether policy has been sufficiently loose in the year since 2008). In a New Zealand context, in both 1996 and 2002 policymakers decided that New Zealand should have a faster trend rate of nominal GDP growth (since they revised up the inflation target). Alternatively, a common approach in New Zealand has been to look at the entire period since low inflation (and lowish nominal income growth) was established, around 1992.

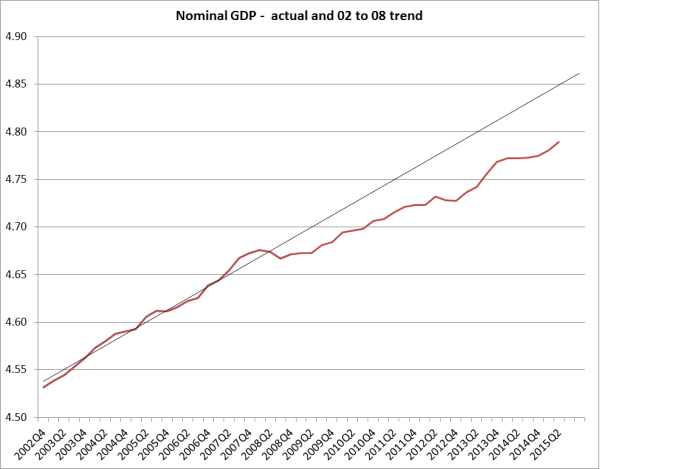

I’m not sure that a trend starting from 2002 to, say, 2008, is that enlightening. After all, there was a common view that monetary policy was too loose over at least several years of that period (Alan Bollard has openly acknowledged as much). But if we used that as the trend, this is what the picture looks like (using logged data).

Nominal GDP is well below that pre-recession trend (as it is in most countries), arguing for looser monetary policy now as well.

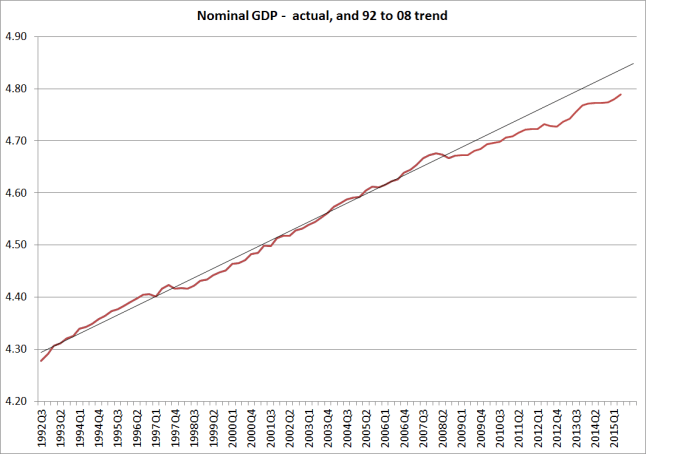

Or we could use a trend done over 1992 to 2008 and one ends with a similar gap.

Levels targeting does require identifying a starting level (which is neither easy nor uncontentious). But what if we just look at nominal GDP growth rates?

Not only has nominal GDP growth averaged far lower since 2008 than it did over the previous 17 years, but the most recent observation (annual growth of 3.9 per cent) is right on the average for the post-2008 period. If we are happy with something like 2 per cent inflation (few have argued for lowering the target) and have a population growth rate of almost 2 per cent per annum, then 5 per cent nominal GDP growth might be a reasonable benchmark. Current nominal GDP growth is well below that, just as current inflation (headline or core) is well below the 2 per cent inflation target.

So, shifting between CPI or nominal GDP based rules, levels or rates of change, looks as though it would not make much difference to how one thinks about appropriate monetary policy at present, at least on the current data.

But as I noted earlier, central banks aim to base policy on forecasts, so the issue is not so much where inflation or nominal GDP is right now, but where the central bank thinks it will be in a year or two’s time. My proposition is that most of the mistakes central banks have made in the last decade or two have been forecasting mistakes rather than policy rule mistakes. Monetary policy wasn’t tightened soon enough during the boom years partly because Alan Bollard was a dove, but partly because the Bank – and most other forecasters even more so – recognised the immediate inflation pressures, but forecast that they would soon dissipate. They were wrong, and as a result inflation and nominal GDP growth were higher than forecast. Similarly in the last few years, central banks have underestimated how weak both inflation and nominal GDP growth have been. If one could forecast nominal GDP more reliably than inflation, perhaps the case for change would be stronger, but outside recessions the big source of fluctuations in New Zealand’s nominal GDP is international commodity prices. They are highly volatile, and the volatility dominates any trend movements over the sorts of period relevant to monetary policy.

An international conference was held in Wellington a year ago this week to mark 25 years of inflation targeting, and the papers have recently been published. Several academics presented a paper looking at how inflation targeting compared with nominal GDP targeting for New Zealand. They looked at a variety of different time periods, including the pre-liberalisation period, the transition to a more liberalised economy, and the current period. The authors were sympathetic to the case for nominal GDP targeting. I was asked to be the discussant, bringing a practical policy perspective to bear on the issues raised in the paper. In my remarks, I set out some of the reasons why I’m not convinced that a practical nominal GDP rule would represent a material advance over (practical) inflation targeting.

One of the attractions of nominal GDP targeting is that it prompts a monetary policy tightening when export commodity prices rise, even if there is no immediate rise in consumer prices. But as I noted one needs to think specifically about the characteristics of the particular economy.

In thinking about an export price shock, it might also be important to understand the transmission of the shock across the rest of the economy. A highly open economy, in which a generalized export price shock affected firms across an employment-rich wide-ranging export sector, might look considerably different than a sector-specific shock in a moderately open economy where the commodity production sectors employ relatively little labor (the story in New Zealand dairy, and much more so in Australian minerals and gas extraction). If New Zealand experiences a surge in dairy prices, and much of the proceeds are saved by farmers—perhaps because they are very conscious of the volatility of prices—why would one want to tighten monetary policy against that lift, if there was little or no apparent spillover to domestic (wage or price) inflation? Perhaps if the shock destabilized wage expectations there could be a basis, but there has been little sign of that sort of wage-setting behavior in response to recent export price shocks. The issues are even more stark in Australia, where most of the profit variability in the face of export price shocks accrues to non-Australian owners of capital (whose consumption choices are likely to put few pressures on domestic resources in Australia).

Partly for this reason, over several years I have been drifting towards the conclusion that if one were to replace inflation targeting with another rule, in New Zealand’s case nominal wage targeting might have rather more appeal. I noted

Much of the academic discussion of inflation targeting focuses on the idea of stabilizing the stickier prices in order to minimize the real costs of adjustment to shocks. Since, as this paper agrees, wages are typically among the stickier prices, perhaps we should be more seriously considering the merits of nominal wage targeting, as Earl Thompson argued decades ago. I have noted elsewhere (Reddell 2014) that such a rule could even have financial stability advantages. Nominal wages are the prime basis for servicing the nominal household debt that dominates the balance sheets of our banks. Faced with adverse shocks, and especially deflationary ones, nominal debt is arguably the biggest rigidity of them all. It would be interesting to see such a rule evaluated in a suitable model.

But…..

If productivity shocks were the dominant source of dislocations in New Zealand, such a wage rule could also have considerable appeal— shifting the variability into the price level rather than into (sticky) nominal wage inflation. As it is, over the last twenty years, wage inflation has followed a rather similar path to core CPI inflation— and does not look much like fluctuations in the path of nominal GDP (or in NGDP per capita, or NGDP per hour worked). So perhaps, at least over that period, policy should have looked very little different under a wage rule than under the CPI inflation targets that successive ministers and governors have agreed upon.

Of course there might be considerable political/communications difficulties with wages-targeting. But this would be nominal wage targeting: actual real wages and the labour share of income would still emerge from the market process. But given these communications difficulties, the case for change would have to be stronger than it is right now (although for what it is worth, current wage inflation also probably argues for looser monetary policy – just like the CPI or nominal GDP).

I have little doubt that inflation targeting is not the “end of history” for monetary policy. But the choice between inflation, nominal GDP, or wage targets – in levels or growth rate terms – doesn’t seem to be the biggest issue we face in designing monetary policy and the related institutions. In practical terms, each would rely on forecasts, and our forecasts simply aren’t very good. And each still faces the issue of the near-zero lower bound. There are arguments that levels targets might help alleviate the ZLB, but only zealots think that in isolation it would make a huge (or sufficient) difference. We need much more energy being applied to either removing the ZLB constraints (which are essentially regulatory in nature) or raising the target for inflation (or nominal GDP or wages growth) sufficiently so that the zero bound is no longer likely to be binding. The Bank of Canada is right to be looking at this issue. Other central banks and finance ministries need to be doing so.

And I still think the other issue is one of just how much accountability there can actually be for autonomous central banks implementing monetary policy. As I have noted recently in both the New Zealand and US contexts, in practical terms there is very little. In the United States, John Taylor has argued for legislating something like a Taylor rule as a benchmark against which the Federal Reserve’s judgments can be formally evaluated, requiring the Fed to explain deviations from the recommendations of that rule. Some on the political right argue for a return to the Gold Standard. I don’t think either would be desirable, but in a sense both are reactions against the delegation of too much unchecked power to central banks. The original conception in New Zealand was of a high degree of effective accountability – an easy test as to whether or not the Governor has done his job. Money base target ideas had a similar conception – plenty of delegation, but plenty of effective accountability. It turned out not to be so easy. But if we cannot meaningfully hold these powerful independent agencies to account – in ways that mean real consequences for real people – I suspect the debate will begin to turn again as to whether the power should be delegated to unelected officials at all. Citizens can vote governments out of office, and that has real consequences for real decisionmakers.

Thanks Michael – very interesting to get your thoughts on this, in particular on the ZLB trap. On that question of the “end of history” – I imagine you’ve read this but thought I’d post here in case other readers haven’t;

http://www.alhambrapartners.com/2015/11/18/swap-spreads-refute-not-just-recovery-but-economics-as-a-science/

LikeLike

Great analysis, so I’m just going to pile on:

– why has inflation targeting, in the context of imperfect forecasting, allowed CBs to get away with lack of accountability for so many target misses? I suspect it’s because there’s an asymmetry between the consequences on both sides – i.e., a miss of the inflation target by 0.6% p.a. might be associated with a spike in the U-6 unemployment rate, at massive human cost. But on paper it looks like the CB has only missed its target by a few tenths of a percentage point. With a nominal wage target (which I support) the miss is more visible.

– level targeting would have one advantage in that repeated misses of the target would increase pressure on the CB. This is relevant given many CB’s haven’t even targeted their own forecast, let alone targeting market forecasts.

LikeLike

Much as I wish it was so, I’m not sure wage targeting (or NGDP) would lead to more effective accountability. The same debates and same forecast uncertainty will still pervade the system, and elites tend towards protecting other elites (instinctively, not as a conspiracy). After all, in truth no one really fully understands what is going on right now. I think our Rb is making a material mistake in which risks they are assigning to whom (I was going to say “which risks they are taking”, but they aren’t taking any personally), but I can’t prove it. And check out the Shadow Board – the “establishment” pretty consistently agrees with the Governor. With a different target specification, I’m not sure why it would be different. It would take time for the new system to bed in and the arguments to take shape, but they would.

LikeLike

The problem we have is that there is a general belief by NZ economists that higher interest rates would dampen consumption. The base assumption is that NZHouseholds and kiwis in general are highly indebted but in reality NZ households and kiwis in general are not highly indebted. There are more people with net positive savings in bank accounts than there are people with debt and the total NZ household debt almost equates to NZ household savings excluding investment property debt which is buffered by some ability to increase tenants rents and increased tax refunds as interest rates rises.

Therefore when interest rate rises there is no immediate impact on general consumption or on inflation until interest rates rise to such a level that it starts to affect businesses in general and employment. The belief by NZ economists that the tightening should have been done earlier would not have changed anything because it would still have led to a crashing of the economy to slow down consumption and to dampen inflation through the loss of jobs that affect both savers and borrowers.

In fact, the early part of a interest rate tightening actually contribute to inflation as businesses raise prices to maintain margins and banks ease up on lending controls in order to maintain their record margins as it is difficult to explain to shareholders why in a rising market that the banks costs and margins start to erode. The effect of raising interest rates therefore contribute towards destabilising a bank as lending controls are loosened to maintain bank profits.

LikeLike

Yes, but the people with the savings and the people with the debt are two different cohorts. The cohort with the debt and the ones yet to take on debt in the case of buying their first home, will indeed have their future consumption affected by interest rates. However, while house prices are as high as they are, future consumption by first home buyers is going to have a brake on it even with low interest rates; principal is actually more important when it comes to “share of income needed to pay off the house over 20 years”.

Systematically unaffordable housing is itself a trap for the economic future. The so called “wealth effect” is just a Ponzi; the long term outlook is “strangulation”.

LikeLike

Thanks Michael, interesting stuff. Given what has occurred overseas, is the ZLB any longer a major issue? e.g. -ve deposit rates, QE, QQE etc. On that, out of interest, are there constraints on what the RBNZ can do should it hit the ZLB?

I just wonder if small open economy central banks can materially influence domestic inflation (or any other nominal variable) using mainly one short term interest rate given all the changes to the structure of the global/domestic economy sine the ‘90s? (e.g. China integration; financial liberalisation via 80/90% LTV mortgages). I think (but haven’t fully grasped!) Keynes had the idea of a ‘cheap but tight’ money policy – keeping the long term interest rate low but watching money/credit growth? Seems to make some sense but I think it relied on managing the exchange rate/capital flows – not sure how that would go down these days…..!

LikeLike

QC

Can central banks influence nominal variables with the OCR? I reckon so. It would be good to have the experiment – if Wheeler were to cut the OCR to say 1.75% I’m pretty confident we’d be seeing core inflation in NZ heading back towards 2%, no matter how weak it was in other countries.

You are more optimistic than I am about the power of negative rates etc. Even the Swiss and Swedish rates don’t apply to all reserve balances, and of course in neither case are we seeing robust recoveries and inflation at target. As for QE, I’m pretty unconvinced by the story that it has made much difference in the US or Europe – at least since the very early rounds of US QE during the crisis. It has clearly affected asset compositions of individual portfolios, but I think you can pretty easily explain long-term bond rates in terms of slowly evolving pessimistic expectations of how long short rates will stay low, and one doesn’t QE for much, if any, of the story.

There are few/no legal obstacles to QE in NZ – altho a practical obstacle is the limited supply of marketable high-rated securities. But in practice – and this is what gives me some comfort – if our OCR was zero and expected to stay there for a while, we’d see the exch rate collapse. The only real reason for holding many NZD assets is yield, and if that isn’t there any longer, demand for the assets will rapidly fall away. In that climate we could revisit the 2000 lows, which would make quite a bit of difference to econ activity and, in time, to inflation pressures.

LikeLike

Cheers – will think on; I guess it relates to what defines a credible central bank: out of interest, in your experience, do central bankers consider themselves ‘guardians of the currency’? I was thinking perhaps households/media/politicians worry a lot less about below than above target inflation until the former starts to have a real effect (per your nominal debt comment) and pressure is then applied to the central bank; in any event, ‘feels’ like FX markets are in for a roller coaster ride at ‘some stage’….!

LikeLike

…..looks as if Mario failed to live up to market expectations (which could have been wrong?). One final thought then: if there is a change to the nominal anchor I guess the bond market would have to work out the new ‘reaction function’ which seems akin to asking it to go through puberty again – can you imagine the tantrums, emotional highs and lows etc? Seems awfully unfair so maybe better to stick with what we ‘know’…!!

LikeLike

“Guardians of the currency” – probably only in an internal purchasing power sense these days, and perhaps even then only the “harder line” among them.

Actually deviations of inflow from the midpoint either side probably don’t excite much public angst in and of themselves. I think it is what goes with the deviation. If high unemployment were to become a salient political concern – as say it did in the depths of 1991 – then the heat goes on the RB. Somewhat to my surprise, Oppositional politicians have made almost nothing of the cruelty and waste involved in an unemployment rate rising back to 6% – even as politicians slap themselves on the back over the economy doing rather well.

LikeLike

Many thanks Michael for the analysis. Very helpful.

I followed up with Bill English. He’s not convinced. http://www.interest.co.nz/news/78983/english-sees-little-advantage-changing-reserve-banks-policy-targets-agreement-pure

But he did seem to suggest that the RBNZ and Treasury had looked at the discussions overseas.

cheers

Bernard

LikeLike

THanks Bernard, Perhaps you could ask him some time about the open Bank of Canada research process and whether he, Tsy, and the Bank should not be commissioning something similar in the lead up to the 2017 PTA.

LikeLike

English is not that intellectual anyway. Captured by the current and past group think.

Time he went farming again along with lots of other “economists” that can’t predict anything.

Give me an inquisitive person every time.

Economists and the Weather Office.

Neither are any good at predictions.

ever matched the weather predictions with the actual results.

well i have and the old 80/20 rule applies. Right only when they can’t be wrong.

Economists and politicians are the same.

Just get them out of our lives.

They are all control freaks and mostly socialists who love spending OPM.

LikeLike

Hi Michael

I noted “After all, there was a common view that monetary policy was too loose over at least several years of that period (Alan Bollard has openly acknowledged as much)” which I’ve seen you say before. Do you have a reference to a document, speech in which he makes the acknowledgment? I’m interested in part because he never acknowledged as much to me, despite the issue – or rather, the repeated failed attempts on my part to have him engage on the underlying analysis that was taking him one way and me another – being one of our main points of contention. And I hadn’t seen him acknowledge it to others.

Cheers

David

PS I’m strongly inclined to an upwards-sloping price level target. In my view, the transition to the new regime would not be that difficult – agents would fairly quickly learn what to expect. That change in expectations is what would provide improved policy leverage at the ZLB, and it would simultaneously reduce the concern that one would often have deliberately to induce inflations or recessions which would not be politically feasible, so not dynamically consistent. This view on the relative ease of the transition, and the stabilising power of expectations draws on the experience with adopting inflation targeting. That was a completely foreign notion fairly quickly become normal. And it turned out to have far far greater stabilisation power than we expected at the outset (which I put down more to expectations, or rather the induced shift in agents’ heuristics, than to globalisation etc which surely also played a role).

David Archer | Secretary to the Central Bank Governance Group

and Head of Central Banking Studies | Bank for International Settlements

Basel, Switzerland | off. +41 61 280 8190 | mob. +41 76 350 8190

LikeLike

Michael

1) when the price of our commodities change the exchange rate also changes. You do not mention that. This is crucial to the targeting regime. Right? See J Frankel on this.

2) wages are functions of variables beyond the influence of the central bank, e.g. productivity, unemployment and reservation wage. How could this policy be feasible?

3)price level targeting can resolve ZLB problem because expected inflation changes.

4) If the CB use ONE model for forecasting it would be like one putting all the eggs in one basket! Hence large forecast error variance or high risk. No one knows the right model of the economy and no one can identify shocks.

LikeLike

Interesting article.

I think NGDP target is just a easy way to do Inflation Targeting correctly. It does the same things as inflation targeting if the central bankers correctly figure out whats supply shocks. If this is the case, I see the advantage of NGDP that you free yourself from human error.

However I agree that better forecasts, specially market forecasts are more important then IT vs NGDP. Level Targeting is probably also more important then IT vs NGDP.

So I think we should have prediction market and in-house forecasting for and then a NGDP Level Target. Now if you tell me that you prefer prediction market and in-house forecasting for Inflation Level Target. I am fine with that. Scott Sumner would probably agree with that line of thinking as well.

Seems to me that central bankers are resistant to this because it takes a lot of their work away. The same goes for using interest rates as policy tools. Its so much more fun then buying and selling assets in a almost rule like way depending on your forecasts.

LikeLike

Thanks Weshah

On your points

1. Yes, but the question is what role does policy play in putting additional pressure (short-term) on the real exchange rate. NGDP targeting,even in levels, would tend to put more pressure on than inflation targeting – to the advocates that is a feature of course.

2. Prices are functions of variables beyond the influence of the central bank. (ie, it is nominal variable, so the central bank can target it). There is nothing ex ante superior about stabilising one nominal variable over another – it is just which provides the best overall stabilisation properties for the economy. And since wages are generally the stickiest prices, I think there is a plausible story there

3. I’m sceptical that it can do very much (the sign is right, but the coefficient is probably small). I was similarly sceptical of Lars Svensson’s foolproof method of escaping Japanese deflation

4. Entirely agree, but in the end the forecast they do make (use) matters a lot. It might be a combination forecast, but it will still have very little information in it.

LikeLike

Michael, I argue that aggregate productivity growth is reduced by expansion in the sector of the economy that is “rentier” – and in the recent era, this is especially property prices and mortgage finance.

While urban planners love a cargo-cult assumption that “dense urban economies are more productive, therefore forcing all urban economies to be denser will lift production”, the reality in the longest working model for this policy, the UK (anti sprawl since 1947) is that a productivity GAP is caused. This is because land is a factor of production and over-pricing it results in its under-utilisation. It might be argued that it is used “more efficiently” the higher it is priced; but in fact there are major diseconomies to being forced to “do without it”. Anyone who has worked in a business that lacked space, will understand this.

Whole sectors in the UK economy have been strangled – the UK as a nation would be better off with some cities with low land costs and a bit more sprawl. While the USA has excessive sprawl, the Ruhr Valley is an excellent “best example”; it is around 1/3 the density of most UK urban areas (and less dense than Auckland). Housing is a labour force cost, too. I would strongly argue that the Ruhr Valley (and indeed the parts of the USA with considerable manufacturing still going on) is the sort of thing that anti-sprawl urban planning “foregoes”. Also foregone are “Silicon Valley” type new clusters – which begin on low-cost exurban land which is affordable to under-capitalised bright young entrepreneurs.

The LSE Spatial Economics Research Centre has been quite focused on this point for more than a decade.

Of course the planner types try to deny that there is any connection between them saving the planet, and urban land price inflation, cyclical volatility, housing unaffordability and foregone productivity; they are falsely assuming “win win” outcomes.

I would argue that the “beneficial supply shocks” (eg in natural gas) would have done a lot more good in the developed world in recent times, if it were not for the almost universal adoption of urban land rationing policies and the consequences. In fact there is a “US Growth Corridor” where cheap gas combined with low urban land costs, has resulted in a boom in rREAL production. The “US economy” in aggregate would be in a far worse state if it were not for this; and the UK economy would be in a far better state if it had equivalents of Dallas, Indianapolis and Salt Lake City instead of Birmingham, Liverpool and Bristol.

LikeLike

I think that the “guardian of the currency” view should be much more central than it seems to be in much discourse.

The role of Money – in Econ 100 – is the means of exchange, the unit of account, and the store of value

But with fiat money we do not have the sacred definitions that exist for the gram, the metre, the temperature, that objectively exist

Given that we have no longer have any objective definition of the value of money, the “social contract” for monetary policy to deliver is “whatever the dollar is worth today, it will be worth about the same in a year’s time”. There is a correlation with a US view (which I don’t know is still current) that inflation should be kept low enough that economic decisions are not distorted.

So – when earthquakes happen, we do not move the latitudes… we recognise that the earth has moved. When water freezes, we do not change the litre measure: we recognise that the frozen water is bigger. When the climate warms, we do not recalibrate the thermometers.

Similarly when there are economic shocks of any colour, we should not recalibrate the dollar

What I am saying is that the value of the dollar should be viewed as a “weights and measures” matter, and not anything more dynamic.

And that is why the RB Act talks of “price stability”. Not inflation targeting.

Most of the discussion about monetary policy and the PTA is about second or third order issues about how price stability should be measured. Those issues are not easy, but we should not get too lost in the detail and, more importantly, should not lose sight of the real prize

LikeLike

THanks Peter

I have a lot of sympathy with the “weights and measures” view, but with a few caveats. First, we do use changes in time zones (daylight saving) as a coordination device to facilitate a movement towards summer activities (or whatever), and relatedly we don’t have much evidence (or reason to believe) that, say, adjusting the official length of a metre could assist in the adjustment to shocks in the way that adjustment in the nominal exchange rate seems to have assisted (not always of course, but see for example the Great Depression).

LikeLike

> Droughts typically aren’t recognised by central banks until we are in the midst of them

I thought the entire point of NGDP targeting is that you /don’t/ have to make special consideration for supply shocks.

The central bank merely looks at the numbers and the adjustment naturally emerges from the fall in NGDP, effectively it’s the futures market and commodity prices that now assists the central bank in making better decisions.

LikeLike